Gaspard LEZIN

Swift Alternative: A 2026 Guide to Global Payment Rails

Looking for a SWIFT alternative? This guide compares modern settlement rails like stablecoins, card networks, and real-time bank transfers for global business.

A lot of teams start looking for a Swift alternative after the same kind of week.

A customer in one country pays on time. Treasury expects funds to arrive quickly. Finance sees a wire reference, then silence. Support gets asked for status updates it can't answer. Reconciliation drifts because the received amount doesn't quite match the invoice. Nobody feels the failure as a single dramatic event. It shows up as delay, manual work, FX uncertainty, and cash that arrives later than the business planned around.

That's why the core question usually isn't “What replaces SWIFT?” It's “Which payment rails should handle which flows, and how do we stop routing every global payment through the same slow, opaque path?” For most internet businesses, the answer isn't one network. It's a stack.

Table of Contents

Where the pain shows up first

Why “faster” isn't the full answer

What SWIFT does, and what it does not do

Why operators should care

Three categories that matter in practice

Why hybrid stacks win in practice

Payment Rail Comparison

Where each rail wins and loses

Three common operating scenarios

How one product can support different flows

The questions that matter

A practical rollout path

Do I need to replace SWIFT completely to modernize cross-border payments

What's the main mistake companies make when evaluating a Swift alternative

How should I think about compliance in a multi-rail setup

Is stablecoin settlement only useful for crypto-native businesses

How do I phase in a hybrid payment stack without disrupting finance operations

The Hidden Costs of Traditional Global Payments

The visible cost of an international payment is usually the fee on the statement. The expensive part is everything around it.

A finance team sends an invoice to a client abroad and expects a normal bank transfer. What they get instead is uncertainty. The client asks whether funds were received. The receiving team checks the bank portal, then a spreadsheet, then an internal Slack thread. Someone manually matches references because the remittance data isn't clean enough. A payout to a supplier gets held because upstream funds still haven't landed.

That's the operational drag many companies are trying to fix when they search for a Swift alternative.

Where the pain shows up first

Traditional cross-border flows often create problems in four places:

Cash flow planning: Settlement timing can be hard to predict, which makes treasury planning weaker than it should be.

Reconciliation: Amounts, references, and fee deductions don't always line up cleanly with invoices.

Customer experience: Clients and vendors expect fast, trackable payments, not “we're checking with the bank.”

Expansion: New corridors often add more exceptions, not more efficiency.

Practical rule: If your team needs a human to explain where a payment is, the payment stack is doing too much work manually.

The issue isn't that bank transfers are obsolete. It's that many businesses now run on internet-speed expectations while parts of their payment infrastructure still assume slower handoffs, narrower operating windows, and more manual follow-up.

That gap gets wider as you add more countries, more currencies, and more payout preferences. It's one reason teams end up rethinking processor design, settlement routes, and fallback options. A useful reference on that operational side is this review of common pitfalls with global payment processors.

Why “faster” isn't the full answer

A faster rail helps, but only if it fits the corridor, currency, and compliance model you need.

A domestic instant rail might solve a local payout beautifully and do nothing for a global supplier payment. A card payout might improve recipient experience but increase cost for the wrong use case. A stablecoin flow might remove banking-hour friction yet require a different treasury and controls setup.

That's why smart teams don't just ask which rail is fastest. They ask which combination reduces delay, manual handling, and failure points across the whole payment lifecycle.

Understanding SWIFT's Role in Global Finance

A CFO approves a cross-border payment in the morning, sees a SWIFT reference within minutes, and assumes the hard part is done. Operations learns later that the message moved fast, but the funds still had to pass through the banking chain behind it. That difference matters when you're choosing a Swift alternative or designing a hybrid stack around SWIFT.

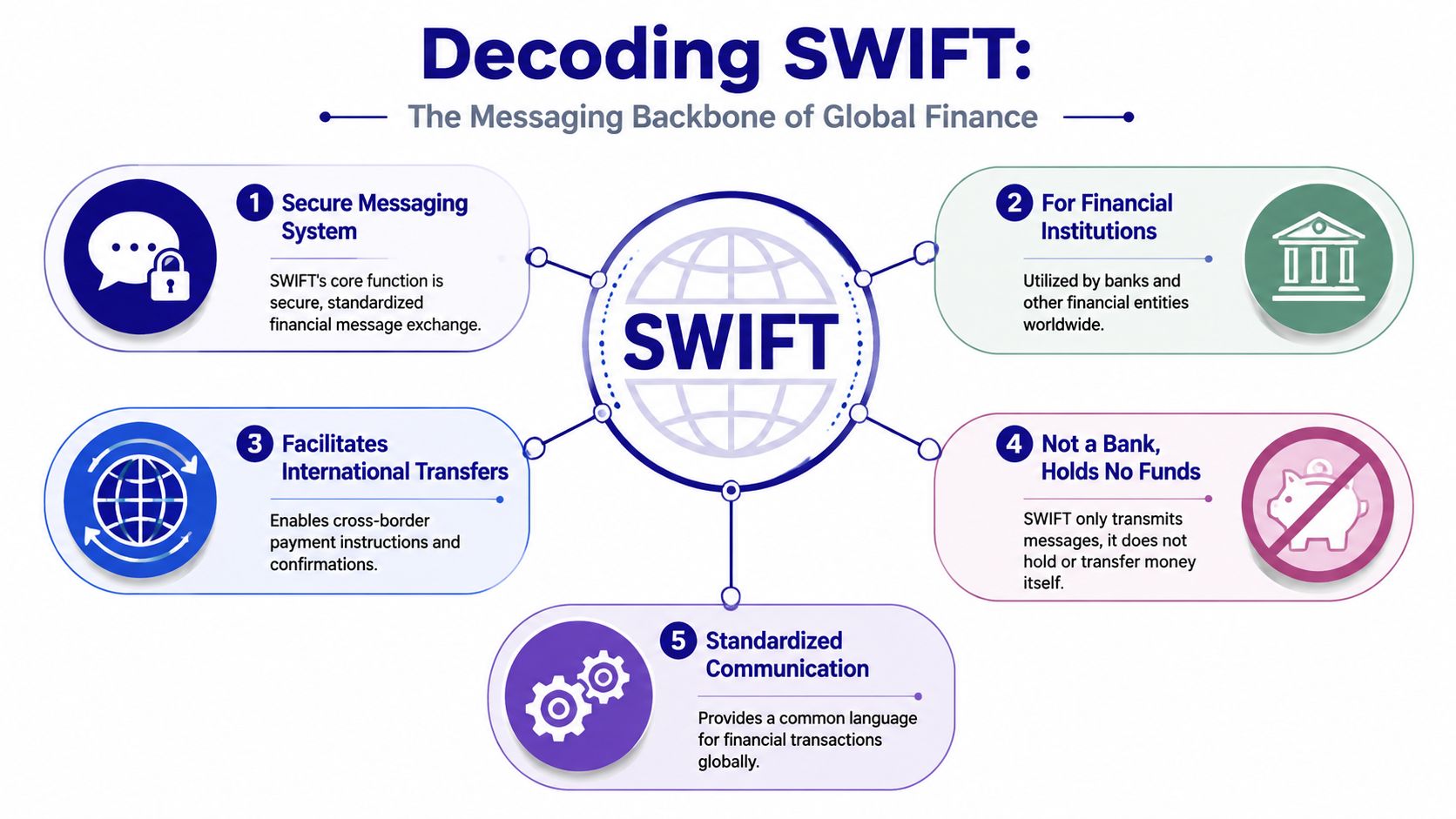

SWIFT is a secure messaging network for financial institutions. It gives banks a common way to send payment instructions, confirm details, and coordinate across borders. According to SWIFT's overview of its network and membership, the system connects more than 11,500 institutions and handles tens of millions of FIN messages per day. It remains one of the core coordination layers in global finance.

What SWIFT does, and what it does not do

SWIFT standardizes how institutions exchange payment messages. It helps banks speak the same operational language across currencies, jurisdictions, and compliance environments.

It does not settle funds by itself.

That distinction is easy to miss inside a business, because the customer experience often compresses everything into one event: "we sent the wire." In practice, messaging, liquidity, correspondent banking, local clearing access, sanctions screening, and final credit to the beneficiary can all sit on different layers. Analysts at the New York Fed make this point clearly in their staff report on cross-border payment architecture.

Why operators should care

For a treasury or payments team, the practical question is not whether SWIFT is good or bad. The question is where SWIFT fits in the stack.

If SWIFT handles the instruction layer well, but settlement still depends on multiple correspondent banks, vostro and nostro account structures, cutoff times, and local market conventions, then the business outcome will reflect that full chain. A fast message can still end in a slow payout. A well-formatted instruction can still incur avoidable fees if the settlement route is inefficient.

This is why "replace SWIFT" is often the wrong framing. In many payment stacks, SWIFT remains useful for reach, bank interoperability, and exception handling, while other rails improve settlement speed or last-mile distribution in specific corridors. Teams that build well usually mix rails by use case. They keep SWIFT where it adds coverage or bank compatibility, then route selected flows through local clearing systems, wallet networks, card payout rails, or other settlement paths when those options produce better delivery times or lower operating cost. A practical way to frame those choices is this guide to cross-border payment solutions by payment flow and rail type.

One more operational point matters. Payment performance is shaped not just by whether a message is delivered, but by how many institutions need to touch the transaction before the beneficiary can use the money. Fewer handoffs usually mean fewer fees, fewer repair cases, and better visibility for support teams.

For an executive evaluating a Swift alternative, that is the useful lens. Compare messaging, settlement, liquidity requirements, and fallback coverage separately. The best answer is often not a single replacement. It is a controlled mix of rails, with SWIFT serving one role rather than carrying the whole cross-border payment job.

The Landscape of Modern SWIFT Alternatives

A CFO reviews a delayed supplier payment, a treasury lead tracks trapped liquidity across three regions, and support is still answering the same beneficiary question: where is the money? In that situation, buying a single "Swift alternative" is usually the wrong move. The practical decision is to choose the right rail for each job, then control how those rails work together.

The useful dividing line is simple. Some options improve bank messaging. Some change settlement. Others solve the final distribution problem, getting funds to a card, wallet, or local account faster and with fewer handoffs. That is the same operating model used in many cross-border payment solutions built around payment flow and rail type.

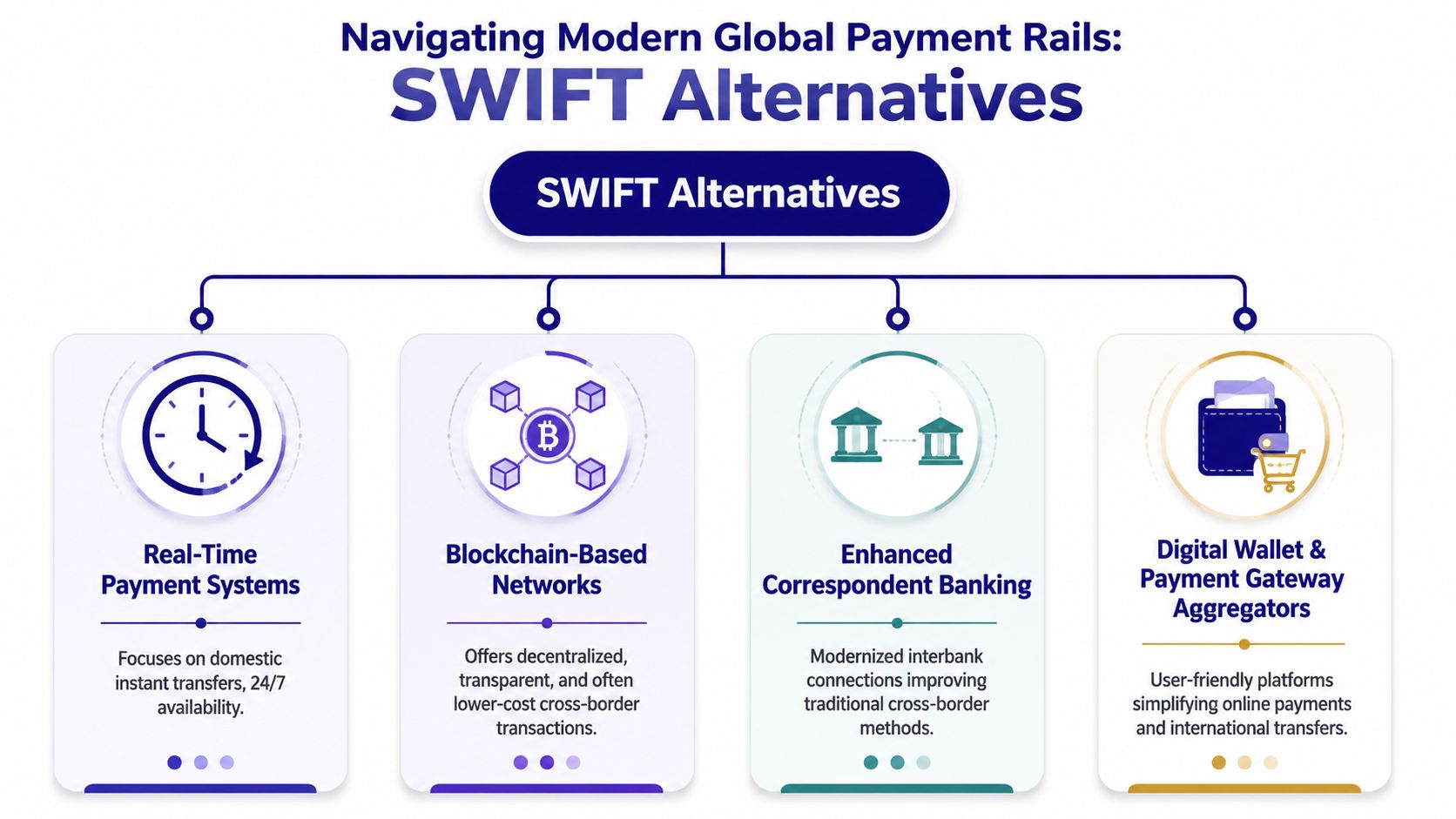

Three categories that matter in practice

Regional real-time and clearing rails are effective inside the markets they were built for. FedNow, RTP, SEPA Instant, Pix, and UPI can deliver strong speed and lower cost when both sides of the transaction can settle locally. For a business building a cross-border stack, these rails usually handle the in-country leg, not the whole transaction. They improve performance in specific corridors, but they do not replace global reach.

Card networks and payout rails solve a different business problem. They are useful when the priority is recipient access, especially for refunds, marketplace disbursements, gig payouts, or customer payments that need to arrive in a familiar endpoint. The trade-off is cost. Card-linked distribution can be faster and easier for the recipient, but it is not always the lowest-cost route for high-value B2B settlement.

Later in the section, the video below gives a broader market view of how newer global payment approaches are changing expectations.

Stablecoin-based settlement rails are gaining attention because they reduce dependence on banking cut-off times and long correspondent chains. They suit treasury transfers, platform settlement, and corridors where banking access is uneven or expensive. They also introduce real trade-offs. Firms still need compliance controls, liquidity management, redemption partners, and a clear plan for moving between digital settlement and fiat payout. The broader market case for these networks is reflected in this XRP and XLM global payment outlook.

Why hybrid stacks win in practice

The market is moving toward orchestration, not ideological replacement.

The strongest payment teams split the problem into layers. They may keep SWIFT for bank interoperability and fallback coverage, use local clearing where corridor depth exists, route urgent recipient payouts through card rails, and add stablecoin settlement where 24/7 liquidity or fewer intermediaries improve the outcome. That mix is harder to design than a single-provider pitch, but it usually produces better speed, lower operational friction, and broader reach.

The main executive question is not which rail wins. It is which rail should handle each flow, and what sits behind it when a route fails, a bank rejects a transfer, or a corridor changes. That is how modern payment infrastructure gets built.

A Head-to-Head Analysis of Payment Rails

A CFO trying to cut cross-border payment costs usually starts by asking for a SWIFT replacement. The better question is which rail should handle each payment type, and what should happen when that route fails, gets delayed, or becomes too expensive in a specific corridor.

That shift matters because payment infrastructure is a portfolio decision. The right stack depends on the payment itself: supplier invoice, marketplace payout, treasury transfer, refund, or salary run. The rail that performs well for one of those can be a poor fit for another.

Five factors usually decide the routing choice: speed, fee visibility, FX control, compliance workload, and how hard the rail is to integrate into existing finance operations.

Payment Rail Comparison

Criterion | SWIFT | Regional Rails (e.g., SEPA) | Card Networks (e.g., Visa Direct) | Stablecoin Rails |

|---|---|---|---|---|

Primary role | Bank messaging across institutions | Direct movement on local or regional bank rails | Distribution and payout through card-linked infrastructure | Direct digital settlement on blockchain infrastructure |

Best use case | Broad bank reach, regulated bank-to-bank flows, fallback coverage | Domestic or regional payments in supported corridors | Fast recipient payouts and customer-friendly disbursement | Global transfers, treasury movement, 24/7 settlement |

Speed profile | Can be fast at the message level, but settlement path may vary | Strong where local rails are available | Often good for quick payout experience | Continuous settlement availability |

Fee profile | Can be harder to predict due to chain complexity | Often better for local recurring flows | Can be more expensive for some use cases | Different cost model than card or correspondent banking |

FX handling | Often tied to banking route and counterparties | Best when staying inside local currency contexts | May include conversion costs depending on corridor | Useful when businesses want digital-dollar style settlement before off-ramping |

Compliance model | Familiar banking framework | Local banking and regional compliance requirements | Network rules plus payout controls | Requires clear digital asset policies, controls, and counterparties |

Developer access | Usually indirect through banks and treasury workflows | Varies by market and provider | Often easier through modern APIs | Often strongest through API-first providers |

Coverage limits | Strong global institution coverage | Narrower, corridor-specific | Strong payout reach but not ideal for every transfer type | Depends on counterparty readiness and off-ramp strategy |

Where each rail wins and loses

SWIFT remains useful when a business needs broad bank-account reach, regulated counterparties, and a familiar operating model for finance and compliance teams. Its weakness is variability. The message may move quickly while the funds take a slower, less transparent path through correspondent banks, which creates support tickets, reconciliation drag, and uncertain landed cost.

Regional rails work best where corridor depth is real, bank participation is high, and the payment stays close to the domestic banking system. They break down when companies expect global coverage from local infrastructure. A strong SEPA route does not help much with a payout into a market where local clearing access is fragmented or unavailable through your provider.

Card networks are often the practical choice for disbursements because the recipient experience is strong and the endpoint is already in the customer's wallet or bank-card setup. The trade-off is cost. For high-volume or larger-value treasury flows, card economics and network rules can become hard to justify.

Stablecoin rails are strongest where settlement speed, time-zone independence, and fewer intermediaries have direct business value. They also create new operational work. Treasury has to manage wallets or custodians, finance has to reconcile on-chain movements with internal ledgers, and compliance has to define which counterparties, tokens, and redemption paths are acceptable.

This is why hybrid design wins. SWIFT can cover bank interoperability and exception handling. Regional rails can carry routine domestic or intra-region volume. Cards can handle urgent payouts. Stablecoins can move value outside banking hours or reduce friction in difficult corridors.

The market argument around blockchain-based cross-border systems is still evolving, but the XRP and XLM global payment outlook is a useful directional read if you want to track how some participants expect these networks to compete with established global payment models.

A practical routing test looks like this:

Local, recurring flows usually belong on local or regional bank rails.

Payout-heavy flows often fit card-based distribution.

Time-sensitive global transfers may justify stablecoin settlement.

Regulated or failure-prone corridors should keep a bank-route fallback, even if it is not the default path.

Teams comparing providers often miss that the harder problem is orchestration across rails, not access to a single rail. This overview of cross-border payment platforms that reduce direct bank dependency is useful if you are evaluating how that orchestration can sit inside one operating stack.

Suby A Modern Platform for Global Settlement

A lot of businesses don't need another single-purpose rail. They need a way to accept payments from customers in the methods customers already use, then settle those funds the way the business wants. That's a different problem from pure bank transfer replacement.

Suby fits that model as a single product with four ways to use it. It provides an API that lets businesses accept payments by card or crypto, and it also offers native integrations with Discord and Telegram for use cases like subscriptions, paid access, and online communities. The core operating idea is straightforward: customers pay the way they want, and the business chooses how to receive funds, including settlement to a bank account or in stablecoins such as USDC.

Three common operating scenarios

A SaaS company selling subscriptions globally often wants one checkout, recurring billing, and flexible settlement. In that case, the sensible design is to let the customer pay with familiar methods such as card, wallet, bank, or crypto, while finance chooses the settlement format that best fits treasury.

A freelancer or agency invoicing international clients usually cares less about elaborate checkout flows and more about getting paid with less friction, which is the whole point of modernizing international business payments in the first place. In that case, invoicing matters more than storefront optimization. The client should be able to pay how they prefer, while the recipient chooses whether funds land in a bank account or as stablecoins.

A paid online community has a different shape entirely. The business doesn't just need to collect money. It needs to control access. That's where payment-linked gating for Discord, Telegram, downloads, or courses becomes more relevant than traditional bank-transfer tooling.

How one product can support different flows

Suby's four usage modes line up with those scenarios:

Suby Payments: An API-first payment stack to accept cards and crypto through one checkout.

Suby Crypto: A payment gateway where customers can pay by card, bank transfer, Apple Pay, Google Pay, Klarna, and more, or crypto, that handles the swap, sponsors the gas, and settles either to a self-custody wallet, a bank account, or a unified Suby balance, keeping the same assets the customer paid or auto-converting everything to USDC on Base.

Suby Gating: Paid access for Discord, Telegram, downloads, and courses.

Suby Invoicing: The client pays how they want, while the business receives what it wants.

The product model is also broader than a simple “crypto checkout” story. One practical flow the company highlights is that customers can pay by card and the business can receive USDC, but that's only one option among several. The wider point is that payin and payout don't need to be locked to the same rail or format.

Businesses usually get the most leverage when customer payment choice and merchant settlement choice are separated.

Operationally, that matters because it lets a company optimize conversion on the front end and treasury on the back end without forcing both sides into the same payment method. It also means a business can use API integrations, webhooks, or shareable paylinks depending on how technical the team is. Pricing depends on the payment method used, so the exact fee structure should be checked on the pricing page rather than assumed as a flat rate.

Decision Framework Choosing Your Payment Stack

A CFO approves a faster payout option for overseas contractors. Treasury likes the speed. Support gets hit with edge cases in markets where recipients still need bank deposits. Finance then spends month-end matching references across two systems. The rail was not the problem. The design was.

The right Swift alternative depends on how money moves through your business. A company paying suppliers in regulated bank corridors has a different requirement from a platform sending frequent low-value payouts, or a digital business collecting by card and settling in USDC. In practice, the strongest setup is usually a hybrid stack. One rail handles reach, another handles speed, and a fallback handles exceptions.

That is the core decision. Build around payment jobs, not around a single network.

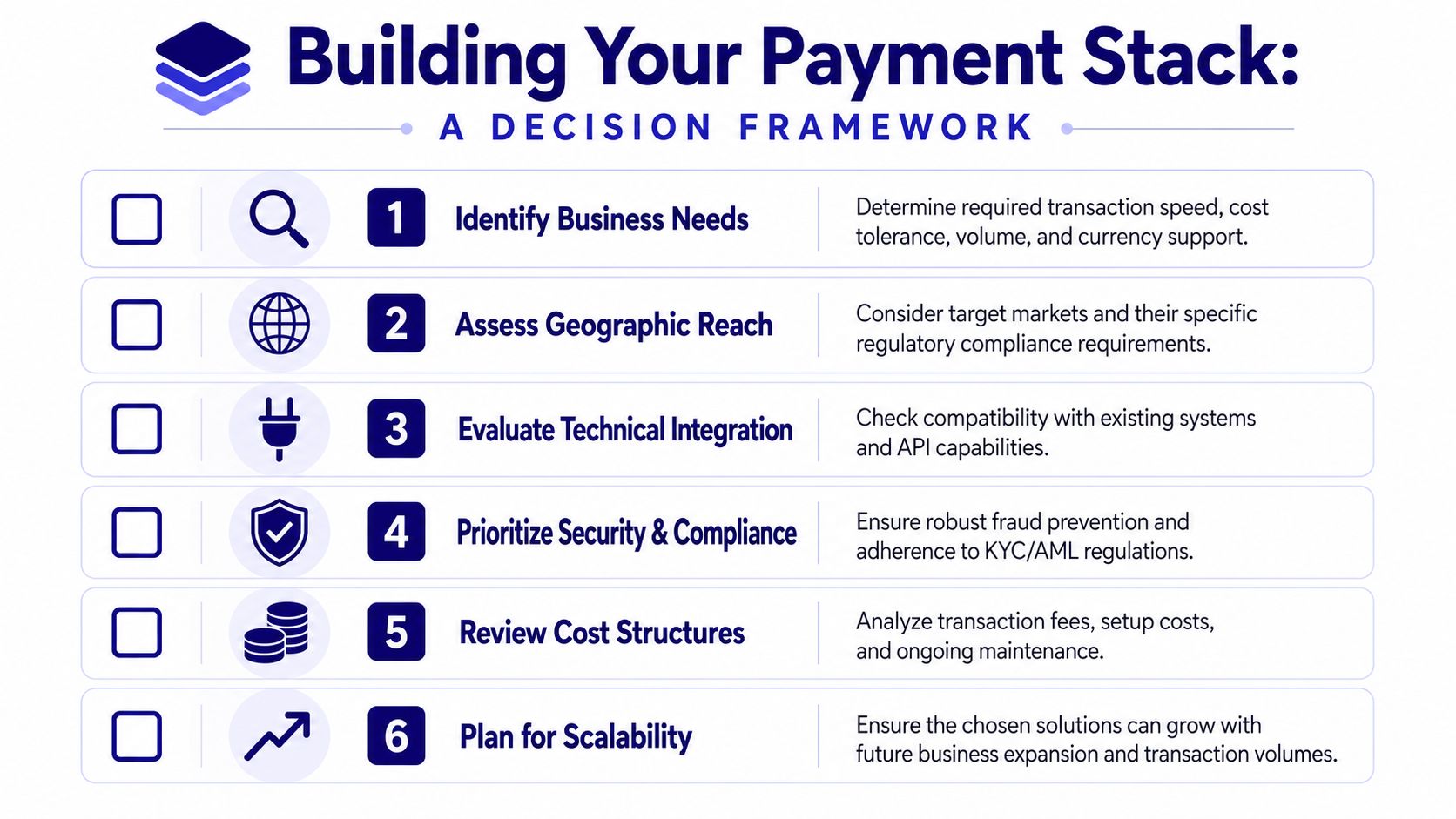

The questions that matter

Start with six operating questions.

Where are funds coming from and going to?

Domestic collections, regional transfers, and global payouts should be treated as separate routes. If you group them together, you usually inherit the cost and delay profile of the hardest corridor.What form of receipt does the counterparty require?

Some recipients need money in a bank account. Others can accept stablecoins and prefer immediate availability. That one constraint determines which rails are even viable.Are payins and payouts solving different business problems?

This matters more than teams expect. Customer checkout is a conversion question. Supplier settlement and treasury movement are control and liquidity questions. They do not need the same rail.What happens when the primary route fails or is restricted?

Coverage changes by country, partner, and compliance posture. A payment stack without a fallback path looks efficient until the first blocked corridor or payout exception.Where is operations carrying hidden cost today?

Manual reconciliation, missing references, delayed settlement files, and exception handling often cost more than the headline fee difference between rails.How much control does your team need in implementation?

Some businesses want API and webhook control because payments are part of the product. Others need dashboards, approvals, paylinks, and a lighter deployment path.

A practical rollout path

Start by mapping payment flows by business purpose, not by provider. Separate customer collections, supplier payments, treasury transfers, and user payouts. Then split each of those by corridor and recipient requirement. That exercise usually shows that one portion of volume still belongs on bank rails, another works better on local or regional rails, and another can move faster through stablecoin settlement.

Next, assign a default rail and a backup rail for each flow. Keep the rule simple enough that operations can follow it without debate. For example, use bank settlement where beneficiary accounts and regulated documentation are required. Use faster digital rails where timing, availability, and cost matter more than universal bank reach. Keep SWIFT where it still earns its place, rather than using it as the default for every international payment.

Then fix reconciliation before you scale volume. Standard reference fields, webhook events, settlement reporting, approval rules, and exception queues matter because they determine whether finance can close the books without manual cleanup. Many multi-rail projects often fail in this regard. The payment can arrive faster while the back office gets slower.

The best payment stack is usually a routing strategy. It assigns each flow to the rail that fits its speed, cost, compliance, and reach requirements, then keeps a second path ready for the cases that do not fit the default.

Teams that follow this approach stop looking for a single Swift replacement. They build a stack that fits the way their business collects, settles, and manages risk.

Frequently Asked Questions

Do I need to replace SWIFT completely to modernize cross-border payments

No. Many businesses keep SWIFT as a fallback for specific bank corridors or regulated flows while moving other use cases to regional rails, card payouts, or stablecoin settlement. Full replacement is often less important than reducing the number of payments that rely on the slowest or least transparent path.

What's the main mistake companies make when evaluating a Swift alternative

They treat all international payments as the same job.

Customer collections, supplier payments, treasury transfers, and user payouts often need different rails. When companies choose one method for everything, they usually overpay in one area and create operational friction in another.

How should I think about compliance in a multi-rail setup

Treat compliance as a rail-specific operating model, not a generic checkbox.

Bank rails, card rails, and stablecoin rails each come with different counterparty expectations, controls, and review processes. The more important question is whether your team has clear ownership for onboarding, screening, exception handling, and settlement approvals.

Is stablecoin settlement only useful for crypto-native businesses

No. It can also be useful for ordinary internet businesses that want faster global settlement, especially when customer payment choice and merchant payout preference are separated. The value is often operational rather than ideological.

How do I phase in a hybrid payment stack without disrupting finance operations

Start with one corridor or one payment type that already creates visible friction. Keep the existing route as backup, compare reconciliation quality and settlement predictability, then expand. The goal is controlled substitution, not a big-bang migration.

Suby is a payment gateway and payment processor. Your customers pay with card, bank transfer, Apple Pay, Google Pay, Klarna, and more, or stablecoins, and you get paid out to your bank account, or directly in stablecoins (USDC, EURC) to your wallet, anywhere in the world, no bank account required. For a global business building a multi-rail stack, that separates customer payment choice from merchant settlement choice, so cross-border collections and payouts route cleanly without leaning on the slowest correspondent-banking path.