Gaspard LEZIN

Online Payment Solutions for Businesses: Accept Cards &

Explore a complete guide to online payment solutions for businesses. Learn to accept cards & crypto, and choose the right global infrastructure for 2026.

A founder launches a SaaS product with users in the U.S., Europe, the Middle East, and Southeast Asia. Signups look healthy. Traffic is coming in. Demo calls go well. Then checkout starts telling a different story.

Some buyers want to pay by card. Others expect a wallet. Some finance teams ask for invoices. Some international clients are open to paying in crypto, but the business still needs reporting that makes sense and payouts that land where finance wants them. What looked like a simple “add payments” task turns into a messy operational problem.

That's the actual issue with online payment solutions for businesses. The hard part usually isn't adding a button to a checkout page. The hard part is building a reliable system that lets customers pay the way they prefer while your business receives funds the way it prefers, with clean operations behind the scenes.

Table of Contents

Introduction The Challenge of Global Internet Commerce

From checkout button to payment infrastructure

Why this matters now

The practical scope founders should think about

Think of it as a translator for money

What happens during authorization

What settlement means in plain language

Acceptance and settlement flexibility

Security operations and finance controls

Integration and team usability

Match the payment setup to the business model

Questions that prevent expensive mistakes

One product with four ways to use it

Why the card-to-USDC flow matters

Where it fits for different teams

Start with payment design not code

Rollout without creating finance chaos

Conclusion Payments as a Competitive Advantage

Introduction The Challenge of Global Internet Commerce

A lot of internet businesses hit the same wall after they find demand. It doesn't happen in product. It doesn't happen in marketing. It happens when money needs to move across borders, payment methods, currencies, and internal systems.

Take a creator selling paid community access. U.S. members may be happy to use cards. Some customers prefer wallets. Others ask for a direct invoice because they're buying through a company account. Now add a global audience, recurring billing, refunds, support questions, and payout preferences. The payment stack starts shaping the business more than most founders expect.

The same thing happens in SaaS. A customer is ready to buy, but their preferred method isn't offered. Or the business can accept the payment, but the finance team now has to reconcile inflows from several tools and settle funds into a bank account that doesn't match how the customer paid. Growth creates administrative drag.

Payments stop being a checkout feature once you sell internationally. They become part of your operating model.

That's why the phrase online payment solutions for businesses should be understood broadly. This isn't only about a gateway that approves cards. It's about the full path from customer payment choice to business settlement choice, with reporting, security, and reconciliation in between.

Founders usually notice the customer-facing part first. They see abandoned carts, failed payments, or support tickets asking for another method. The operational cost appears later, when finance has to answer simple questions that no longer have simple answers. Which payments settled? In what currency? To which balance? What belongs in revenue today, and what's still in transit?

A modern payment setup has to solve both sides. Customers need flexibility at checkout. The business needs control over where money lands and how it gets reported.

What Are Online Payment Solutions Really

From checkout button to payment infrastructure

A "payment solution" is often associated with a card form on a website. That's only one layer.

In practice, online payment solutions for businesses are a stack. They handle pay-ins, meaning how customers pay. They also handle the balance layer, where funds are tracked, and payouts, meaning how the business receives or moves money after the sale.

If you're evaluating providers, it helps to stop asking, “Can this take card payments?” and start asking more useful questions:

Customer choice: Can buyers pay by card, wallet, bank method, invoice, or crypto, depending on the business model?

Merchant control: Can the business settle to a bank account or in stablecoins like USDC, depending on treasury and operating needs?

Operational clarity: Can finance see one usable record of inflows, fees, refunds, and payouts?

That last point gets missed all the time. A payment setup can look modern from the outside and still create internal chaos.

A good primer on the provider layer is this explanation of a payment service provider or PSP. It's useful because founders often mix up gateways, processors, acquirers, and the business software wrapped around them.

Why this matters now

This category is growing because digital payments are now a baseline part of business operations. The global payment-gateway market generated around USD 26.0 billion in 2022, rose to an estimated USD 31.0 billion in 2023, and is projected to reach USD 131.0 billion by 2031 at about 20.5% compound annual growth, according to payment gateway market data. The same source notes that wallet-based payments are expected to grow from about 49% of consumer online payments in 2022 to around 54% by 2026.

Those numbers matter for one reason. Customer expectations keep widening. If your checkout only reflects how your business prefers to get paid, not how customers prefer to pay, you create unnecessary friction.

Practical rule: Your payment stack should reflect your customer mix, not your internal habits.

This isn't only relevant for software companies. A property operator collecting rent online still has to think about payment method convenience, timing, and reconciliation, which is why a workflow-focused guide for efficient rent processing is a useful parallel example. Different industry, same operational lesson. Payment design affects both conversion and back-office workload.

The practical scope founders should think about

A complete solution usually covers several layers at once:

Layer | What it does | Why it matters |

|---|---|---|

Checkout | Collects the payment method and customer details | Directly affects conversion and trust |

Processing | Routes and verifies the transaction | Determines reliability and approval flow |

Balance | Records what was paid and what's pending | Gives finance a source of truth |

Payouts | Sends money to the business destination | Impacts treasury, cash flow, and accounting |

Reporting | Shows fees, settlements, and status changes | Makes month-end less painful |

When founders skip this systems view, they often end up stitching together one tool for cards, another for invoicing, and a separate workflow for crypto or international settlement. It works at first. Then scale exposes the seams.

A modern payment solution isn't just a way to collect money online. It's financial infrastructure for how an internet business operates.

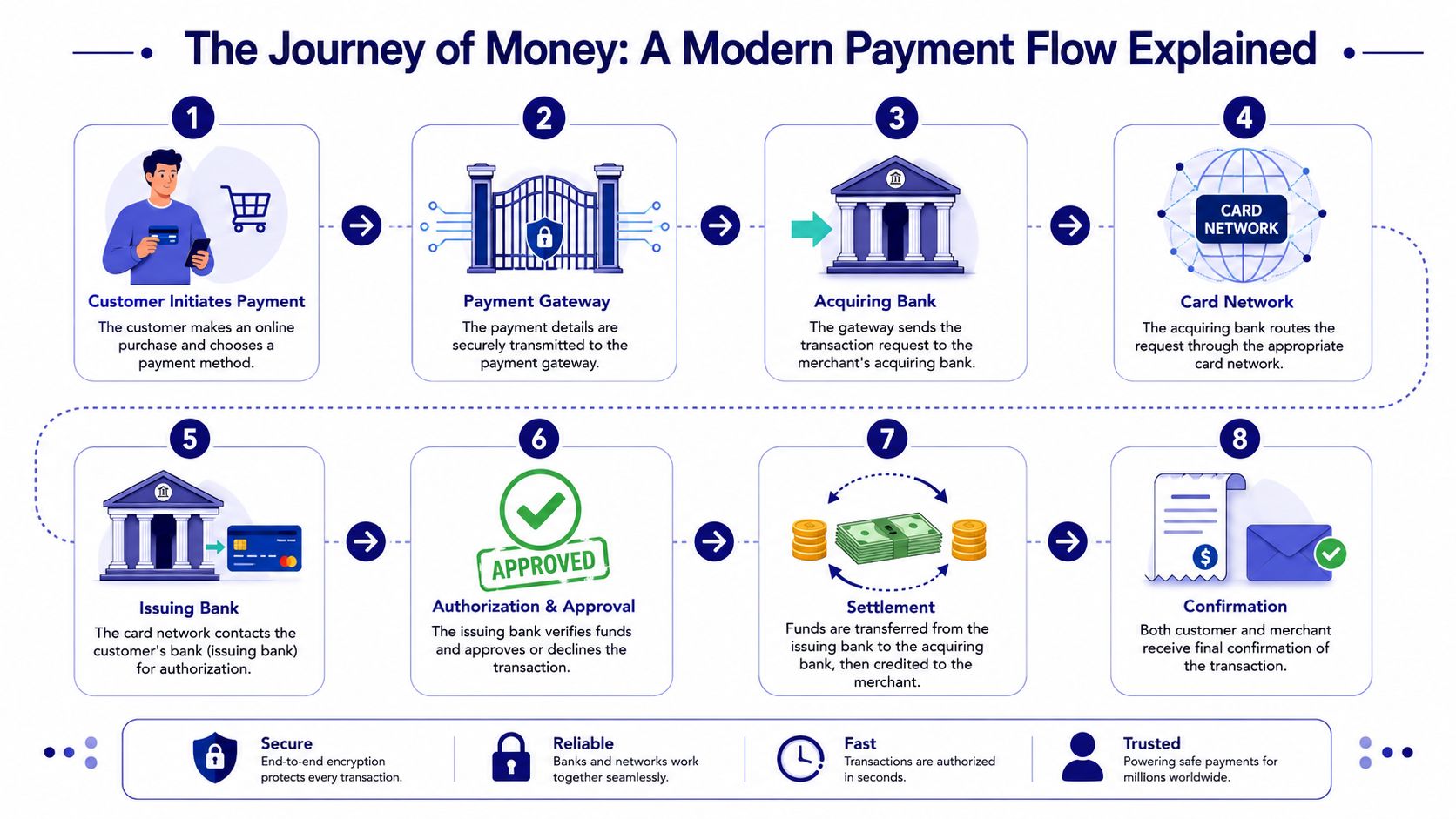

The Journey of Money A Modern Payment Flow Explained

The easiest way to understand payment infrastructure is to think of it as a translator. Your customer speaks one payment language. Your business may want to receive funds in another form. The system's job is to make that exchange reliable, secure, and understandable.

Think of it as a translator for money

Here's a simple version of the flow.

The customer chooses a payment method.

That might be a card, a wallet, a bank-based option, or crypto.The checkout sends the payment request into the infrastructure.

At this point, the customer just sees a loading state or confirmation screen. Behind the scenes, several systems start talking to each other.The provider validates and routes the payment.

Method-specific processing occurs. Card rails behave differently from crypto flows or bank methods, but the business ideally sees one clean operational layer.The payment is approved or declined.

Approval feels instant to the customer, but it's the result of a chain of checks.Funds move into a merchant balance and later settle out.

This is the part many founders don't model clearly enough at the start.

What happens during authorization

For card payments, the process is more structured than it appears on the screen. The payment gateway first encrypts and tokenizes sensitive card data, then forwards it to the processor. The processor routes it over the card network to the issuing bank, which returns an approval or decline in roughly 1–3 seconds, according to this explanation of online payment processing flows.

That quick approval window is the authorization step. It answers a narrow question. Should this transaction be accepted right now?

The issuing bank checks things like account validity, available funds, and internal risk rules. If all looks fine, the transaction is approved.

A useful mental model is this:

Authorization is reservation

Settlement is delivery

Your checkout usually celebrates authorization. Your finance team lives with settlement.

To make the flow easier to visualize, this short walkthrough is useful:

What settlement means in plain language

After approval, the money doesn't usually teleport into your operating account. Approved transactions go through batch settlement, where funds move from the issuer, through the acquirer, and into the merchant's account, typically within 1–3 business days in most major markets, as described in the same payment flow overview.

That delay is why founders sometimes get confused by dashboard states. A payment can be successful from the customer's point of view but not yet fully settled into the destination the business cares about.

A successful checkout and an available payout are related, but they aren't the same event.

For a global business, the journey can be even more layered. You may accept one method at checkout, aggregate funds into a single balance, and then choose a different settlement path later. That's the core shift in modern infrastructure. The inflow method and the payout method don't always have to match.

That's especially important when a customer wants the familiarity of card payment, but the business wants to receive funds in a different form, such as a bank payout in a target currency or settlement in stablecoins like USDC.

Core Features of a Global Payment Solution

A strong payment setup isn't defined by a long feature list. It's defined by whether the right capabilities show up in the right places for your business. The checklist below is useful because it ties each feature to an operational outcome, not just a technical label.

Acceptance and settlement flexibility

The first job is still customer acceptance. If people can't pay the way they expect, nothing else matters. But the second job is just as important. The business needs freedom over how money is received after the sale.

Look for these capabilities:

Multiple pay-in methods: Cards are still important, but many businesses also need wallet, bank, invoice, subscription, and crypto support.

Choice in settlement: Some teams want payouts to a bank account. Others may want part of their flows settled in stablecoins like USDC.

Currency control: International businesses need to think about where funds land, not just how they're charged.

For service businesses, this can dramatically improve the billing experience. A tutoring company, for example, benefits when clients can pay quickly and the business can keep billing organized. That's why a workflow page about how to get paid faster as a tutoring business is a good reference point. It highlights a simple truth. Payments affect speed to cash and admin burden at the same time.

Security operations and finance controls

Security is where payment conversations often become too abstract. Founders hear acronyms and assume the provider “handles that part.” Some of it does. Some of it still needs deliberate planning.

A global setup should make room for:

Area | What to look for | Why it matters |

|---|---|---|

Card security | PCI-DSS aligned handling and tokenization | Reduces exposure to sensitive card data |

Authentication | Strong Customer Authentication and related controls where applicable | Helps support legitimate transactions |

Disputes and refunds | Clear operational tooling | Prevents support and finance bottlenecks |

Reporting | Exportable transaction and payout records | Supports reconciliation and audit readiness |

Security features aren't only about fraud. They're also about reducing the number of places where your team has to touch sensitive payment details.

The best payment infrastructure removes data from your operational surface area. Your team should spend time on exceptions, not on manually handling payment risk.

Another feature founders underweight is unified reporting. Once you accept more than one payment method, finance needs a coherent ledger of what happened. Which transactions were approved, refunded, disputed, settled, or still pending? If that answer lives across several dashboards, month-end gets slower fast.

Integration and team usability

Some teams need a full API. Others need payment links, hosted checkout, invoicing, or subscriptions that can go live quickly. Most growing companies eventually need both.

A practical evaluation should include:

Developer options: API access, webhooks, and documentation that let engineering automate key flows

Operational tools: A dashboard finance and support can use without filing tickets for every change

Flexible surfaces: Checkout pages, pay links, invoices, recurring billing, and embeddable experiences

Scalability: A setup that won't force a platform migration as transaction complexity grows

Many online payment solutions for businesses separate into two camps. Some are easy to start but narrow in settlement choices. Others are powerful but fragmented enough that non-technical teams struggle to operate them day to day.

The best fit is usually the one that lets engineering move quickly without creating dependency on engineering for every routine payment task.

How to Choose the Right Solution for Your Business

A payment system should fit the shape of the business, not the other way around. The right setup for a subscription SaaS company won't look identical to the right setup for a cross-border e-commerce brand, a digital agency, or a creator running a paid community.

Match the payment setup to the business model

Here's a cleaner way to think about selection.

International SaaS

Recurring billing matters. API quality matters. Dunning, subscriptions, invoicing, and finance exports matter. If customers sit across multiple regions, checkout flexibility matters too.

Cross-border e-commerce

The priority is broader payment acceptance and a smooth checkout. Settlement options still matter, but conversion usually gets the first vote.

Agencies and freelancers

Invoices are often central. So is payout preference. Some teams want clients to pay in familiar methods while the business receives funds in a different form that better matches how it operates.

Creators and community businesses

Paid access can be the whole product. Discord, Telegram, downloads, and course access all depend on the payment flow connecting directly to access control.

One of the biggest blind spots in this decision is reconciliation. Existing content on online payment solutions rarely addresses how to reconcile a single balance that receives payments in hundreds of methods while settling to multiple assets like fiat and stablecoins. Most guides stop at listing processors without explaining how finance teams can track a single revenue stream when inflows include crypto and fiat in real time, as noted in this discussion of payment gateway guidance gaps.

A broader comparison of provider categories can help sharpen the shortlist. This overview of the best payment gateway options is useful as a starting point when you want to compare different models rather than just features.

Questions that prevent expensive mistakes

Before choosing a provider, ask questions that reveal operational fit:

What do customers want to use at checkout? Don't answer this from internal preference alone.

Where should funds settle? Bank account, stablecoins like USDC, one operating currency, or several.

Who needs access after launch? Engineering, finance, support, growth, and operations all use payment systems differently.

What will reconciliation look like? If you accept more than one payment method, someone has to close the books on that complexity.

How will pricing work by method? Payment costs vary by payment type, so you need method-level clarity rather than assuming one flat rate.

Choose the system your finance team can close books on, not just the one your growth team can launch fastest.

That usually leads to better long-term decisions than optimizing only for the shortest integration timeline.

Suby A Unified Payment Solution in Action

A useful example of this newer model is Suby. It's positioned as a single payment product that can be used in four distinct ways: Suby Payments, Suby Crypto, Suby Gating, and Suby Invoicing, all leveraging the same underlying API and infrastructure, as described in officially summarized product documentation.

One product with four ways to use it

The important framing is that this is one product, not four disconnected tools.

Suby Payments is the API-first payment stack. A business can accept payments by card or crypto through one checkout, and it's aimed at teams that want a developer-ready setup with operational tooling behind it.

Suby Crypto is the crypto layer, one option alongside card, bank transfer, Apple Pay, Google Pay, Klarna, and more in Suby's payment gateway. According to the official product context, it handles the swap, sponsors the gas, and settles either to a non-custodial wallet or to the Suby balance. That matters because many teams want crypto acceptance without making customers deal with a clunky flow.

Suby Gating is built for paid access. The documented use cases include Discord, Telegram, downloads, and courses. With it, payments stop being only a checkout event and become part of product access itself.

Suby Invoicing is for billing workflows where the client pays how they want, while the business receives what it wants. That model is especially relevant for agencies, freelancers, and international service businesses.

A few practical points stand out from the documented setup:

Single API model: The same underlying infrastructure supports different use cases.

Mixed acceptance: Businesses can accept payments by card or crypto.

Native integrations: It offers native integrations with Discord and Telegram for subscriptions, paid access, and online communities.

Settlement choice: Customers pay any way they want, and businesses get paid the way they choose, whether to a bank account or in stablecoins like USDC, in the currency they want.

Why the card-to-USDC flow matters

The card-to-USDC path is worth highlighting because it captures what many older payment guides miss.

A customer might prefer paying by card because it's familiar and simple. The business, however, may want to receive settlement in stablecoins like USDC. That can be useful for treasury workflows, cross-border operations, or internal fund movement. The key point is that the checkout method and the settlement method don't have to be the same.

That's not the only pattern available. It's one option among several. A business might instead settle to a bank account, keep funds in its balance, or use another supported operational path. The broader idea is flexibility on both sides of the transaction.

The modern model separates customer convenience from merchant settlement preference. That's a meaningful design improvement over older one-rail setups.

This approach also matches the broader need for unified balance management. If a company accepts different payment types across customers and regions, the value of the system increases when all those inflows can be viewed and managed coherently rather than in separate operational silos.

Where it fits for different teams

This structure makes sense for several kinds of businesses.

For developers, the API matters. Payment teams often want one integration surface rather than one project for card checkout and another for crypto.

For finance teams, the important part is that payments can land into one operating layer before payout. That's easier to reason about than several unrelated merchant tools.

For creators and community operators, the native Discord and Telegram integrations are the relevant detail. A payment can trigger access rather than just generate a receipt.

For agencies and freelancers, invoicing flexibility matters most. The client can use the method that suits them, while the business chooses where and how to receive funds.

Suby also documents shareable paylinks, conversion-focused checkout, subscriptions, webhooks, dashboard reporting, dispute handling, Strong Customer Authentication, two-factor authentication, PCI-DSS Level 1 certified processing partner support, and zero-fee refunds in its official product materials. Pricing depends on the payment method used, so there isn't one flat rate to quote. The right place to verify current figures is the Suby pricing page.

For a founder evaluating online payment solutions for businesses, that makes the offering easiest to understand as infrastructure for the global internet economy. Customers can pay by card, wallet, bank, or crypto. The business chooses how to receive the money, either to a bank account or in stablecoins like USDC, in the currency it wants.

Implementing Your New Payment Infrastructure

Changing payment infrastructure sounds bigger than it usually is. The reason it feels intimidating is that founders picture a long engineering project. In reality, the biggest mistakes usually happen earlier, during planning.

Start with payment design not code

Before you compare implementation options, write down the flow you want.

List the customer payment methods you need to support. Then list the merchant outcomes you need after the payment. Where should funds land? Which teams need visibility? What should happen for recurring charges, refunds, disputes, and failed payments?

That planning step avoids a common trap. Teams integrate the fastest checkout they can find, then discover later that finance can't reconcile payouts or support can't explain payment states to customers.

If your team is deciding between hosted checkout, pay links, and direct integration, this overview of payment gateway API integration is a useful frame. It helps separate what needs custom engineering from what can be launched quickly with lower operational overhead.

Rollout without creating finance chaos

A smooth rollout usually has three parts:

Launch one or two high-value payment paths first

Don't migrate every edge case on day one. Start with the flows that matter most to revenue.Map finance reporting before volume arrives

Decide how transactions, fees, refunds, and payouts will be exported and reviewed.Prepare support for payment edge cases

Customers don't ask about “authorization versus settlement.” They ask why they were charged, why access hasn't updated, or why an invoice still looks unpaid.

A practical implementation plan also names ownership clearly.

Engineering handles integration and event handling.

Finance validates payout and reconciliation workflows.

Support or operations owns customer-facing exception cases.

That cross-functional setup matters because payment infrastructure isn't just a developer tool. It becomes part of how the company runs cash flow, support, and reporting every day.

Conclusion Payments as a Competitive Advantage

The businesses that handle payments well usually remove friction in two places at once. Customers get a payment experience that feels familiar. The business gets settlement and reporting that fit how it operates.

That's why payment infrastructure is no longer a background utility. It shapes conversion, international reach, finance operations, and customer trust. For small businesses, that shift is already clear. 87% of new owners who started during the pandemic cited access to electronic payment options as important, according to the ETA white paper on electronic payments and small business success.

Online payment solutions for businesses have become a strategic choice. The strongest setups let customers pay any way they want, while the business gets paid the way it chooses.

Suby is a payment gateway and payment processor. Your customers pay with card, bank transfer, Apple Pay, Google Pay, Klarna, and more, or stablecoins, and you get paid out to your bank account, or directly in stablecoins (USDC, EURC) to your wallet, anywhere in the world, no bank account required. It runs on a single API, with native Discord and Telegram integrations for paid access and subscriptions. As an online payment solution for a global business, that is how you let customers pay any way they want while the business gets paid the way it chooses, without stitching together separate tools for cards, invoicing, and crypto.