Gaspard LEZIN

Best Fintech Platforms for Cross‑Border Payments Without a Bank: 2026 Guide

Discover the best fintech platforms for cross‑border payments without a bank. Compare 2026's top tools for USDC, low fees, & global reach for SaaS & creators.

If you're trying to get paid globally without opening local bank accounts, waiting through payout holds, or guessing what FX spread got buried in the final settlement, you're not looking for another generic “international payments” list. You're looking for infrastructure that changes where settlement happens.

That's the dividing line in the best fintech platforms for cross‑border payments without a bank. Some tools make international payments easier, but still settle through banking rails in the background. Others let you stay wallet-native and receive funds without depending on SWIFT, correspondent banks, or local payout accounts. For online businesses, that difference matters more than almost any feature checkbox.

The market is moving in that direction fast. The global cross-border B2B payments market is projected to reach $1.67 trillion in 2026, with a projected 10.79% CAGR through 2035, according to HighRadius research on cross-border payment platforms. At the same time, a lot of businesses still get stuck with slow settlement, extra intermediaries, and pricing that looks simple until the payout lands short.

This guide focuses on the practical question: if you want customers to pay from anywhere, and you want to receive value without relying on a traditional bank account, which platforms fit? Some are better for SaaS billing. Some are stronger for crypto-native checkout. Some are good only if your team is comfortable managing wallets and on-chain treasury.

If you're building for developer-led flows, wallet settlement, and automated revenue operations, it's also worth looking at integration features for AI agent wallets.

Table of Contents

Why Suby is different

Where it works best

Best fit

Where OpenNode makes sense

What it does well

Operational trade-off

Best use case

What to watch

Who should use it

Where it fits

The control advantage

Top 10 Fintech Platforms for Cross‑Border Payments, Comparison

Final Thoughts

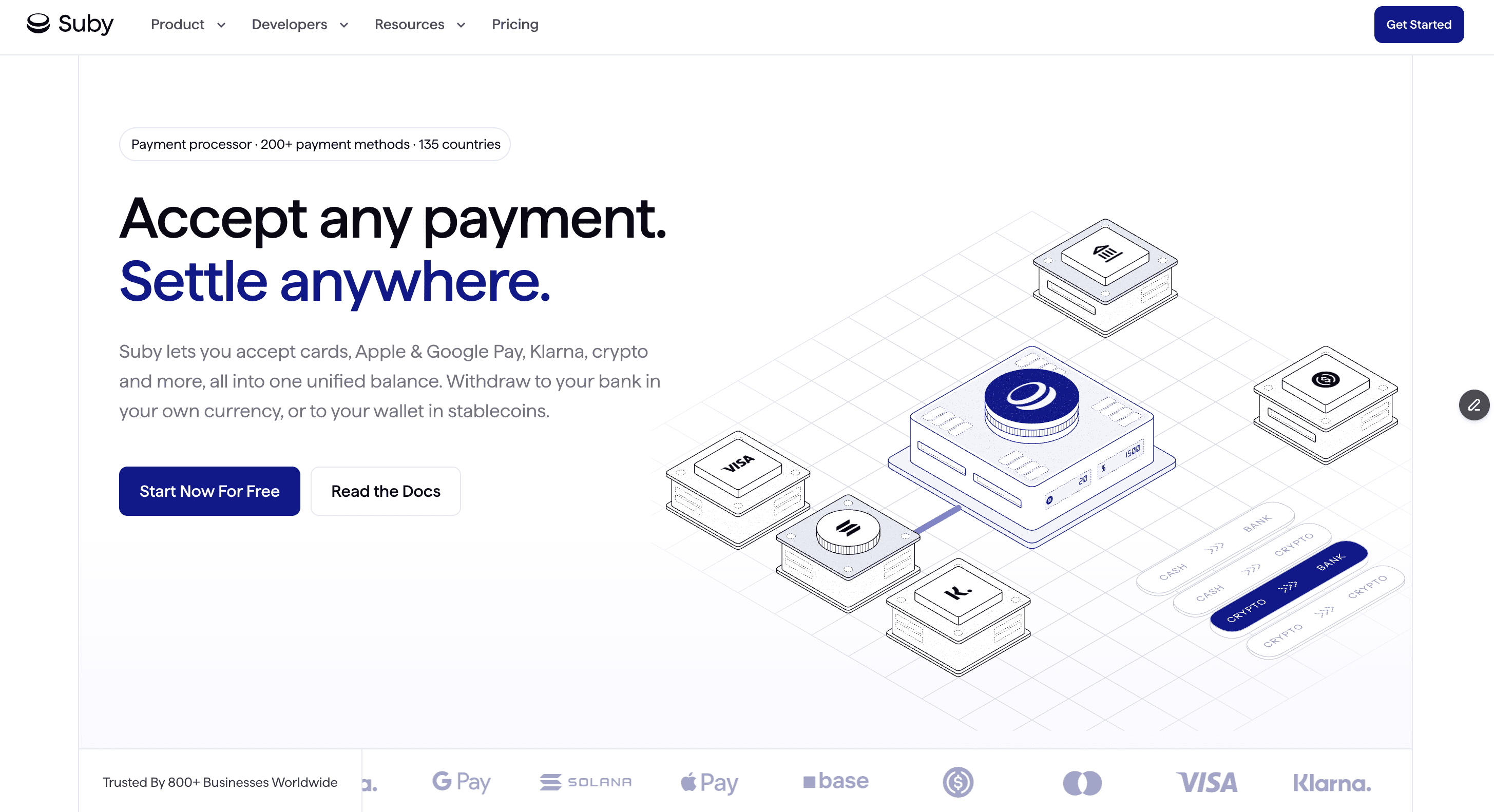

1. Suby

A common cross-border problem looks like this. The customer wants to pay with a card, the business wants to receive dollars quickly, and the founder does not want revenue stuck in bank payout queues, FX conversions, or regional payout limits. Suby is one of the few platforms in this category built around that exact settlement problem.

Customers can pay by card or crypto, and the merchant receives USDC. That settlement design is why Suby belongs near the top of a list focused on cross-border payments without a bank. For businesses trying to avoid traditional banking rails, the primary question is not just which payment methods a platform supports. It is how money settles, where it lands, and what operational work that creates afterward.

Why Suby is different

Suby is designed for internet-native businesses that need more than a basic crypto checkout. Merchants can launch with payment links, embed checkout, or connect through API and webhooks. It also supports one-time payments and recurring subscriptions, which makes it practical for SaaS, agencies, freelancers, community businesses, and digital product sellers.

The useful distinction is simple. Suby does not bolt stablecoin payout onto a card stack as a secondary option. It is built around letting buyers pay the way they already expect to pay, while the business settles in USDC. That changes treasury operations for merchants selling across borders because settlement no longer depends on opening and maintaining local bank accounts in every market.

The platform also includes Discord and Telegram integrations. That matters for operators selling access, memberships, or recurring community subscriptions, where payment and access control need to stay connected.

Teams that want to examine the mechanics can review Suby's guide on accepting payments (card, bank transfer, Apple Pay, Google Pay, Klarna, and more, or crypto) for business.

Practical rule: If customers expect card checkout but your business wants wallet settlement, filter platforms by settlement method first. Everything else comes after that.

Suby also covers the day-to-day merchant side well. The dashboard tracks payments, subscriptions, churn, and payouts. Based on its published materials, card processing runs through a PCI-DSS Level 1 certified partner, and the product includes fraud controls, strong customer authentication, dispute handling, and zero-fee refunds.

Where it works best

Suby fits best when the merchant wants normal checkout on the front end and flexible payout on the back end, to a bank account, or in stablecoins (USDC, EURC) to a wallet. That is a strong match for global SaaS companies, creators selling paid communities, agencies invoicing international clients, and e-commerce businesses that want to receive USDC directly instead of waiting on bank payouts.

There are trade-offs, and they are real.

Wallet settlement is required: Your team needs a compatible wallet and a clear internal process for receiving, tracking, and moving USDC.

Finance workflows may need adjustment: Teams used to bank statements, fiat reconciliation, and traditional treasury controls will need a new operating process.

Pricing needs a direct check: Suby's published materials indicate pricing starts at 5%, so confirm the current plan details with the company before rollout.

If the goal is straightforward, let customers pay by card or crypto while the business settles in USDC without relying on bank rails, Suby is one of the more operationally practical options in this group.

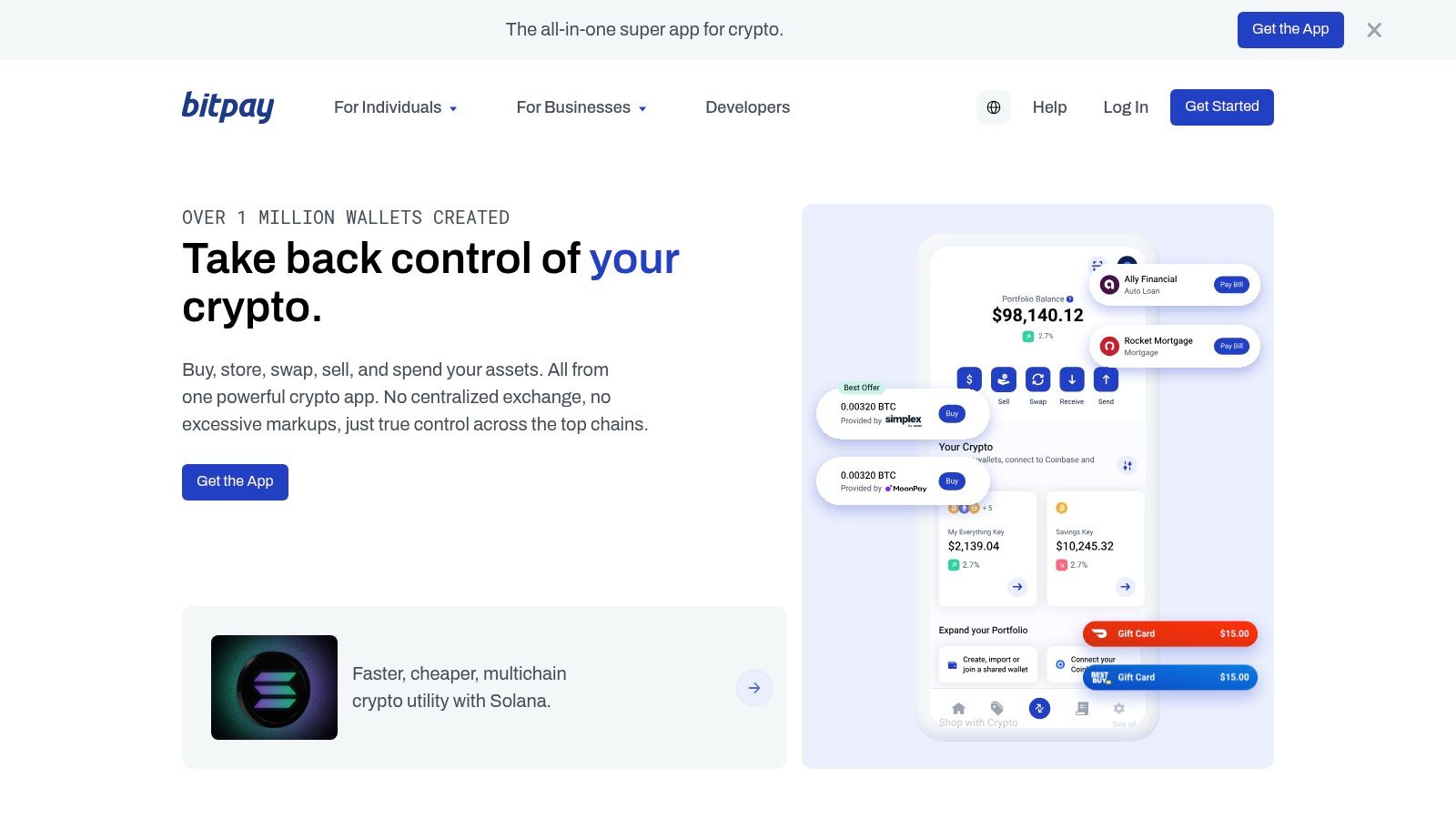

2. BitPay

BitPay is one of the older names in crypto merchant payments, and that longevity still matters. If your business wants a processor with established merchant workflows, hosted checkout, invoicing, and crypto settlement options, BitPay is usually on the shortlist.

What BitPay does well is familiarity. The platform doesn't feel experimental. It gives merchants standard tools, a documented setup path, and settlement options that can stay on-chain if that's what you want. That makes it viable for businesses that want to avoid banks, but don't need a highly customized payment stack.

Best fit

BitPay works best for merchants that accept crypto directly and want a proven processor instead of building around open-source or stitching together wallets, invoicing, and reporting themselves. It's also workable for companies that may want the option of bank settlement later, even if they start with wallet settlement.

That said, BitPay isn't the most flexible platform here. Compared with newer tools built around developer workflows or stablecoin-first merchant ops, the product can feel more standardized. If your business needs subscription logic, community access automation, or a card-to-USDC flow, you'll likely want a more specialized option.

A processor can be mature and still not be the best fit. Stability helps, but settlement design matters more.

For businesses comparing processor-led crypto checkout against more modern wallet-settlement flows, this overview of business crypto payment options is a useful contrast.

Use BitPay if you want battle-tested merchant crypto payments and you're comfortable with a more traditional processor model. Skip it if your main goal is blending mainstream checkout with direct USDC merchant settlement.

You can review the platform directly at BitPay.

3. OpenNode

OpenNode doesn't belong on every shortlist, but when it fits, it fits well. It's best for businesses that want crypto-native payments with fast finality and don't mind a narrower asset focus.

That's also where the biggest limitation appears. OpenNode is not built around stablecoin-first merchant settlement. If your treasury goal is “receive USDC and keep accounting simple,” this won't be the most direct path. If your goal is crypto acceptance with fast transfer behavior and strong programmatic flows, it becomes more interesting.

Where OpenNode makes sense

OpenNode is strongest for businesses that already operate comfortably with external wallets and want hosted checkout, APIs, and payout tooling without pulling banks into the loop. For that use case, the setup is clean and the product is developer-friendly.

The broader market shift toward faster non-bank settlement is real. Platforms using stablecoin rails combined with instant payment integrations can settle cross-border payments in 30 seconds to 2 minutes, compared with SWIFT's 1 to 3 business day standard, according to BVNK's analysis of Swift alternatives. OpenNode sits inside that wider push away from slow correspondent-bank settlement, even if its asset focus is narrower than what many merchants now prefer.

For a merchant choosing OpenNode, the practical question isn't whether it's fast enough. It's whether you want your payment operations centered on that specific crypto payment flow rather than on card acceptance or stablecoin-first receivables.

Use it when: Your buyers are already comfortable paying in crypto, and your team wants fast wallet settlement.

Avoid it when: You need customers to pay by card while the business receives USDC.

Expect a narrower treasury path: Stablecoin settlement usually requires another step elsewhere.

OpenNode is a specialist tool. That can be a strength if your business model matches it.

You can review the product at OpenNode.

4. CoinGate

CoinGate is a practical middle-ground option. It supports multi-asset acceptance, offers plugins and APIs, and can work well for merchants that want crypto checkout without going deep into custom infrastructure.

What I like about CoinGate is that it doesn't force you into an all-or-nothing setup. You can use it for straightforward payment acceptance, and if your business has affiliates, vendors, or contractor payouts, the payout tooling adds operational value. That matters more than flashy feature lists.

What it does well

CoinGate is useful for merchants that want flexibility in what customers can pay with, while keeping the business side manageable. If you sell internationally and want to avoid banking rails where possible, a gateway that handles acceptance and crypto payout paths in one place reduces the number of moving parts.

This is also where total cost matters more than sticker pricing. Traditional SWIFT-based transfers can carry effective costs that are multiple times higher than surface-quoted fees once FX spreads, correspondent charges, and settlement delays are included, according to OpenDue's analysis of cross-border payment cost structure. That's why even a gateway with its own conversion and refund nuances can still be operationally better than a bank-led payout stack.

CoinGate's trade-off is that availability and full feature access can vary by jurisdiction and onboarding status. That's common in this category, but it matters if you need a predictable rollout across multiple entities or regions.

Don't evaluate a crypto payment tool only on checkout. Evaluate payout controls, reconciliation friction, and how many manual steps your finance team inherits after payment succeeds.

CoinGate is a good fit if you want broad acceptance options and crypto-native payout capability, but you don't need a card-plus-USDC specialist.

You can explore it at CoinGate.

5. Triple-A

Triple-A is one of the more compliance-forward options in this list. If your team wants stablecoin acceptance and settlement, but also wants a provider that presents itself in a more enterprise-friendly way, Triple-A deserves a look.

That positioning matters because some merchants aren't trying to be fully crypto-native in every layer. They just want to receive cross-border payments without local bank dependency, while keeping internal compliance teams comfortable with the provider choice.

Operational trade-off

Triple-A's biggest strength is focus. It isn't trying to be everything for every merchant. The product is generally easier to understand if your use case is stablecoin-centric and your company values documentation, controls, and a structured onboarding path.

The trade-off is that pricing is less transparent in public materials than some merchants would prefer. That usually means you'll need a sales conversation before you know whether it's competitive for your volume, vertical, and geography. For larger businesses that's normal. For smaller operators, it can slow evaluation.

There's also a simpler product trade-off. A narrower asset list can be a benefit if you want less complexity, but it can be limiting if your business markets to a broad crypto-paying audience.

Good choice for: Merchants that want stablecoin-oriented acceptance with a compliance-heavy posture.

Less ideal for: Businesses that want open, self-serve setup and fully public pricing.

Worth checking early: Supported payout paths, supported jurisdictions, and merchant category fit.

Triple-A makes sense when operational trust matters as much as payment flexibility.

You can evaluate the platform at Triple-A.

6. Request Finance

A common cross-border problem looks like this: a client in another country is ready to pay, but your team does not want to open local bank accounts, chase wire confirmations, and manually match incoming payments to invoices. Request Finance is built for that workflow.

The platform is strongest when payment starts with an invoice and settles on-chain. That is the key distinction. It is less about checkout conversion and more about how a business issues invoices, receives crypto or stablecoin payments, pays vendors or contractors, and keeps records clean enough for finance and accounting teams to work with.

That settlement model matters if the goal is to stay off traditional banking rails as much as possible. Instead of routing cross-border collections through correspondent banks, Request Finance centers the process around wallet-based payment flows and on-chain settlement. For a business that already holds part of its treasury in stablecoins, that can reduce banking dependency and cut a lot of operational drag.

It also changes the trade-offs.

Request Finance is a better fit for agencies, SaaS companies, DAOs, and remote teams sending invoices across borders than for merchants selling through a typical ecommerce checkout. If your buyers expect a card form and a familiar consumer payment flow, this will feel like the wrong front end. If your revenue comes from billed clients, retainers, milestone payments, or contractor payouts, the product lines up much better with how money moves.

I have seen teams make the same mistake here. They choose a gateway first, then try to force invoicing and reconciliation into it later. That usually creates extra manual work for finance, especially once payment volumes grow across multiple wallets, assets, and entities.

Best use case

Request Finance makes the most sense for businesses that need wallet-native invoicing plus payable workflows. The advantage is not just that it accepts crypto. The advantage is that the settlement method, invoice records, and back-office process are designed to work together.

The main trade-off is customer experience on the payer side. Invoice-based collection is efficient for B2B payments, but it is less suited to broad, conversion-focused checkout use cases. Businesses should also check asset support, accounting exports, approval flows, and how easily their team can operate in stablecoins without creating treasury headaches later.

Request Finance is a strong option when the business wants cross-border collections and payouts built around on-chain settlement, not bank rails.

You can learn more at Request Finance.

7. CoinsPaid

CoinsPaid is built for businesses that care about scale, operational controls, and treasury tooling more than a lightweight self-serve setup. If you process meaningful volume and want crypto payment processing tied to broader merchant operations, it's one of the more serious options in the category.

This isn't the tool I'd suggest to every early-stage startup. It leans more enterprise in feel, onboarding, and evaluation. But for higher-volume merchants, that can be a plus rather than a drawback.

What to watch

CoinsPaid supports multiple assets and settlement options, including stablecoin-oriented paths that can keep the merchant bankless if that's the chosen setup. That makes it relevant for businesses that want payout flexibility without handing all treasury decisions to a processor.

The practical issue is complexity. Enterprise-oriented products often solve bigger problems while asking more from the merchant up front. Expect more review, more onboarding steps, and more attention to eligibility. That's not friction for the sake of friction. It's part of how these providers manage risk.

For the right merchant, the benefit is operational depth. You're not just getting a checkout widget. You're getting a system that's better suited to volume, controls, and long-term payment operations.

Strong fit: High-volume merchants that want payment processing plus treasury and settlement options.

Weak fit: Small teams looking for a fast, low-touch launch.

Decision point: Make sure your team needs enterprise structure before taking on enterprise onboarding.

CoinsPaid is worth considering if scale is already your problem, not just your ambition.

You can review the platform at CoinsPaid.

8. NOWPayments

NOWPayments is appealing for one simple reason: it's easy to start. If you want broad asset support, direct wallet payouts, and a setup path that doesn't feel enterprise-heavy, it's one of the more approachable options on this list.

That simplicity is valuable. A lot of merchants don't need a big compliance-first platform or a custom treasury workflow. They need a gateway that lets them accept crypto, route funds to their own wallet, and avoid storing balances with the processor.

Who should use it

NOWPayments is best for merchants who want non-custodial-style settlement behavior and broad token support. It's especially practical for online businesses that want to test crypto acceptance without redesigning their entire payment stack from scratch.

The trade-off is support depth and operational consistency. Simpler gateways can be fast to launch, but the merchant usually takes on more responsibility for wallet management, fee awareness, and workflow design. That's fine if your team is comfortable with it. It's less fine if you want a provider to hold your hand through complex cross-border revenue operations.

If you're comparing lightweight crypto gateways with tools built specifically for card-to-USDC settlement, this review of a NOWPayments alternative for merchants that want direct USDC outcomes is a useful lens.

Choose NOWPayments if: You want fast launch, broad asset support, and direct wallet settlement.

Look elsewhere if: You need subscriptions, community access automation, or a more structured merchant operations layer.

Remember: Broad coin support is only useful if your finance workflow can handle it.

NOWPayments is a solid fast-start option. Just be honest about how much operational structure you'll need after launch.

You can check it out at NOWPayments.

9. Crypto.com Pay Merchant

Crypto.com Pay Merchant benefits from brand recognition. That matters more than some operators admit. A buyer is often more willing to complete payment when the checkout option comes from a name they already know.

For merchants, that brand familiarity can reduce buyer hesitation. If your audience already uses crypto payment apps and wallets, the platform can offer a smoother customer-side experience than a lesser-known processor.

Where it fits

This is a better choice for businesses that care about customer familiarity and promotional ecosystem effects than for teams optimizing around treasury design. It can work well as a merchant checkout option when your buyer base overlaps with that consumer ecosystem.

The caution is regional variation. Features and payout modes can differ by market, and that makes implementation planning more important. If you operate across multiple countries, verify exactly what the merchant experience and settlement options look like in your target regions before you commit.

Another practical point: consumer-facing crypto brands often optimize first for payment acceptance, rewards, and user growth. That's not the same as optimizing for a finance team that wants clean USDC receivables and minimal payout ambiguity. Sometimes those priorities align. Sometimes they don't.

Well-known checkout brands can improve payer confidence, but merchant ops still win or lose on settlement clarity.

Crypto.com Pay Merchant is a reasonable option if your audience already trusts the brand and your team is comfortable validating regional details up front.

You can review the merchant offering at Crypto.com Pay Merchant.

10. BTCPay Server

BTCPay Server is the purest “no processor dependency” option in this list. It's open-source, self-hosted, and built for merchants that want direct control over infrastructure and settlement.

That control is the appeal. No processor is holding funds. No one can freeze payout logic because there is no managed payout layer in the usual sense. For the right technical team, that's powerful.

The control advantage

BTCPay Server works best when your company has real devops capacity and a strong reason to own the stack. If you care about self-custody, infrastructure independence, and eliminating processor risk, it's hard to beat.

But control is not free. You take on hosting, maintenance, updates, monitoring, and the practical burden of keeping payments reliable. A lot of teams underestimate that cost because they compare software fees and ignore internal operational time.

There's also a product-fit issue. BTCPay Server is not the right answer for businesses that want card acceptance, subscription management, or a polished non-technical merchant workflow. It's best for teams that deliberately want infrastructure ownership over convenience.

Best for: Technical teams that want self-hosted payment processing and direct wallet control.

Not best for: Mainstream SaaS and e-commerce merchants that need card checkout or all-in-one subscription tooling.

Decision test: If you don't already manage critical self-hosted systems well, this probably isn't the first payment stack to self-host.

BTCPay Server is excellent at one thing: removing processor dependence. Just make sure your team is prepared to become the operator.

You can explore the project at BTCPay Server.

Top 10 Fintech Platforms for Cross‑Border Payments, Comparison

Product | Payment methods & settlement | Target audience | Key strengths / USPs | Security & compliance | Pricing (typical) |

|---|---|---|---|---|---|

Suby | Visa/Mastercard + crypto (USDC, USDT, ETH, SOL, BNB); merchants receive revenue in USDC to their wallet | SaaS, e‑commerce, agencies, freelancers, creators & communities | Card-like 3‑click checkout + crypto-native USDC settlement; paylinks, embeddable checkout, API/webhooks; Discord/Telegram access automation | PCI‑DSS Level 1 processing partner; multi-layer fraud controls, SCA/2FA, zero-fee refunds | Starts at 5% (all‑inclusive); public materials also reference 4% in places, verify on Suby pricing page |

BitPay | Major crypto & stablecoins; settle to crypto wallet or fiat bank account | Merchants wanting established, regulated crypto payments | Mature integrations, hosted checkout & invoicing, configurable settlement split | Regulated, enterprise controls for payments, reporting and refunds | Varies by flow, check vendor pricing |

OpenNode | Bitcoin (on‑chain) and Lightning; instant or scheduled BTC transfers to external wallet | Lightning-first businesses; BTC payouts for contractors | Very low network costs and fast finality via Lightning; developer-friendly APIs | On‑chain finality; platform payout controls (bank settlement reintroduces banks) | Network fees + platform fees vary |

CoinGate | Multi-asset acceptance with rate lock; crypto payouts (single & batch) | Merchants needing EU-licensed gateway and broad coin support | Plugins/APIs, automated exchange, 180+ country payouts | EU-licensed operations; region/KYB-dependent feature availability | Public references ~1% (check current terms) |

Triple‑A | Stablecoins (USDC/USDT) plus BTC/ETH; stablecoin settlement options | Compliance-focused enterprises, e‑commerce, SaaS | Enterprise integrations, stablecoin-centric settlement, regulatory-aligned docs | U.S. MSB registration (FinCEN) and KYB/fraud screening | Pricing by quote; not fully public |

Request Finance | Invoicing, mass payouts, payroll across crypto/fiat; receive USDC to wallet | Finance teams, agencies, SaaS, contractor payroll | AR/AP, mass payouts, accounting exports (QuickBooks/Xero) | Built for reconciliation; off‑ramp to fiat available (reintroduces bank rails) | Varies by usage and off‑ramp needs |

CoinsPaid | 20+ cryptocurrencies with automated exchange & settlement to wallet | High-volume merchants and treasury teams | Scale-ready processing, EU license, ISO/IEC 27001 security | EU licensing and security certifications; enterprise onboarding | Quotes vary; public pricing limited |

NOWPayments | Non‑custodial routing to merchant wallet; hundreds of assets & stablecoins | Merchants wanting broad asset support and bankless flows | Wide coin support, plugins, auto-conversion to stablecoins | Non‑custodial model (merchant controls funds); network fees apply | Platform fees + network fees; check site |

Crypto.com Pay | Wallet and hosted checkout; settle in crypto or convert to fiat | Consumer-facing brands and merchants seeking rewards/promotions | Recognizable consumer brand, promotions/cashback ecosystem | U.S. merchant terms available; features vary by region | Varies by region/flow; verify current terms |

BTCPay Server | Bitcoin & Lightning with direct self‑custody settlement | Teams wanting full control and no processor dependence | Open-source, self-hosted, no processor fees (only network/hosting costs) | You control keys and infrastructure; requires maintenance | No processor fees; hosting & network costs only |

Final Thoughts

The biggest mistake businesses make in cross-border payments is comparing providers as if they all solve the same problem. They don't. Some help you move money internationally with fewer headaches, but still depend heavily on banking rails in the background. Others change the settlement model so you can receive value without the usual bank account dependency.

That's why “without a bank” needs a stricter definition. A lot of platforms marketed that way still rely on local banking partners for settlement, conversion, or payout execution. That can still be useful. Wise, for example, processed over $185 billion in cross-border payments in FY2025 for 15.6 million customers and reported saving users about $2.6 billion in fees through its model, according to Airwallex's discussion of cross-border payment solutions. But that same category of provider often still sits on top of banking infrastructure. If your goal is total removal of banking dependency, that distinction matters.

There's also a practical market reason this category keeps growing. Traditional SWIFT-based transfers can involve costs above the headline fee and delays that stretch over days, while domestic instant rails and non-bank orchestration are pushing settlement faster and making pricing more transparent. In the US, RTP processed 125 million transactions totaling $405 billion by Q4 2025, with 1,130+ participants, while FedNow launched in July 2023 with 30-second settlement and a $0.045 credit transfer fee, as summarized in the FXC Intelligence overview of cross-border payment infrastructure. Those rails don't solve cross-border settlement alone, but they show how far the market has shifted away from accepting slow, opaque flows as normal.

So what works?

If you want crypto acceptance with established processor workflows, BitPay is still credible. If you want invoice-centric crypto finance ops, Request Finance is stronger than a checkout-first gateway. If you want broad wallet-settlement support with simpler launch, NOWPayments is practical. If you want processor independence and full infrastructure ownership, BTCPay Server is the extreme version of that choice.

But if you want the closest thing to a practical mainstream cross-border stack for internet-native businesses, Suby stands out. The reason is simple. It solves the core merchant contradiction better than most tools here. Customers want to pay with cards or familiar payment methods. Businesses want predictable settlement, no banking drag, and no hidden FX surprises. Suby bridges that cleanly by letting users pay with card, bank transfer, Apple Pay, Google Pay, Klarna, and more, or crypto, while businesses get paid out to their bank account, or in stablecoins (USDC, EURC) to their wallet.

That makes it a strong fit for SaaS, global subscriptions, online communities, agencies, freelancers, and digital commerce teams that don't want to keep rebuilding payment ops around local banks. It also helps that Suby wraps payment acceptance, recurring billing, payout visibility, and Discord or Telegram access control into one system instead of pushing those jobs into separate tools.

The right platform comes down to one question: where do you want settlement to end? If the answer is “in our own wallet, predictably, without bank friction,” that narrows the field fast.

Suby is a payment gateway and Merchant of Record. Your customers pay with card, bank transfer, Apple Pay, Google Pay, Klarna, and more, or stablecoins, and you get paid out to your bank account, or directly in stablecoins (USDC, EURC) to your wallet, anywhere in the world, no bank account required. That makes it the platform I'd start with for cross-border payments without a bank, especially for SaaS, subscriptions, digital products, agencies, and online communities that want global checkout without local bank accounts or slow correspondent-bank payouts.