You've started selling globally. Revenue is coming from customers in new markets, your signup chart looks healthy, and then payments turn into an operations problem.

A customer's card works in one country and fails in another. A payout lands later than expected, and finance can't tell whether the delay came from banking cutoffs, an intermediary, or compliance review. Your team sees one fee in the pricing page, another cost in FX, and a third problem when support has to explain why the recipient got less than expected.

That's the point where organizations stop asking 'which provider is cheapest?' and begin asking a better question. Which payment architecture gives us predictable settlement, clean reconciliation, and a developer workflow we can maintain?

Here's the short version.

| Payment model | Typical strengths | Typical weaknesses | Best fit |

|---|---|---|---|

| Traditional banking and SWIFT | Familiar, broad institutional acceptance, useful for larger bank-led flows | Slower, less transparent, more intermediary risk, harder status tracking | Firms already built around bank operations |

| Fintech aggregators | Better UX, easier onboarding, local payment method abstraction, cleaner APIs than banks | Can still depend on banking rails underneath, pricing can be layered, payout logic can be opaque | SaaS and ecommerce teams that want easier deployment |

| Stablecoin settlement rails | Faster finality, more predictable settlement, wallet-based treasury, fewer cross-border banking steps | Requires wallet and compliance workflow design, conversion paths matter, finance teams need new operating habits | Internet-native businesses that want card acceptance with USDC settlement |

Table of Contents

- Total cost is more than the processing fee

- Predictability matters as much as raw speed

- Developer and operations fit decide the long-term outcome

The Growing Pains of Global Commerce

The usual pattern is easy to recognize. A SaaS company starts in one market, adds international customers, and keeps the same payment stack longer than it should. For a while, that works. Then support tickets pile up around failed international cards, delayed payouts, and invoices that don't match what finance expected.

The same thing happens in ecommerce. Orders come in from several regions, but the merchant still settles through a setup designed for one home market. Suddenly, the business is dealing with card acceptance on the front end and messy cross-border payout logic on the back end. Customers want familiar checkout. The company wants predictable settlement. Those are not always the same thing.

Most cross-border payment pain doesn't show up in the first transaction. It shows up when finance, support, and engineering all need different answers from the same payment event.

This isn't a niche issue. The cross-border payments market is projected to grow from roughly $195 trillion in 2024 to about $320 trillion by 2032, according to Circle's cross-border payments primer. Another estimate in the same market discussion says it could reach about $250 trillion by 2027, which tells you how central these flows already are to digital trade.

Why startups hit this wall early

A lean team can ship product fast, but payments expose every hidden dependency:

- Card acceptance varies by region, so checkout conversion can drop for reasons your product team can't see directly.

- Settlement timing affects cash flow, especially when subscriptions, contractor payouts, or supplier payments depend on funds arriving on schedule.

- FX handling creates support work, because “what the customer paid” and “what the business received” stop matching cleanly.

- Reconciliation spreads across tools, with data split between gateway dashboards, bank statements, and internal billing systems.

For a startup, that's not just back-office friction. It changes hiring plans, payout schedules, and how much confidence the team has in expanding to the next market.

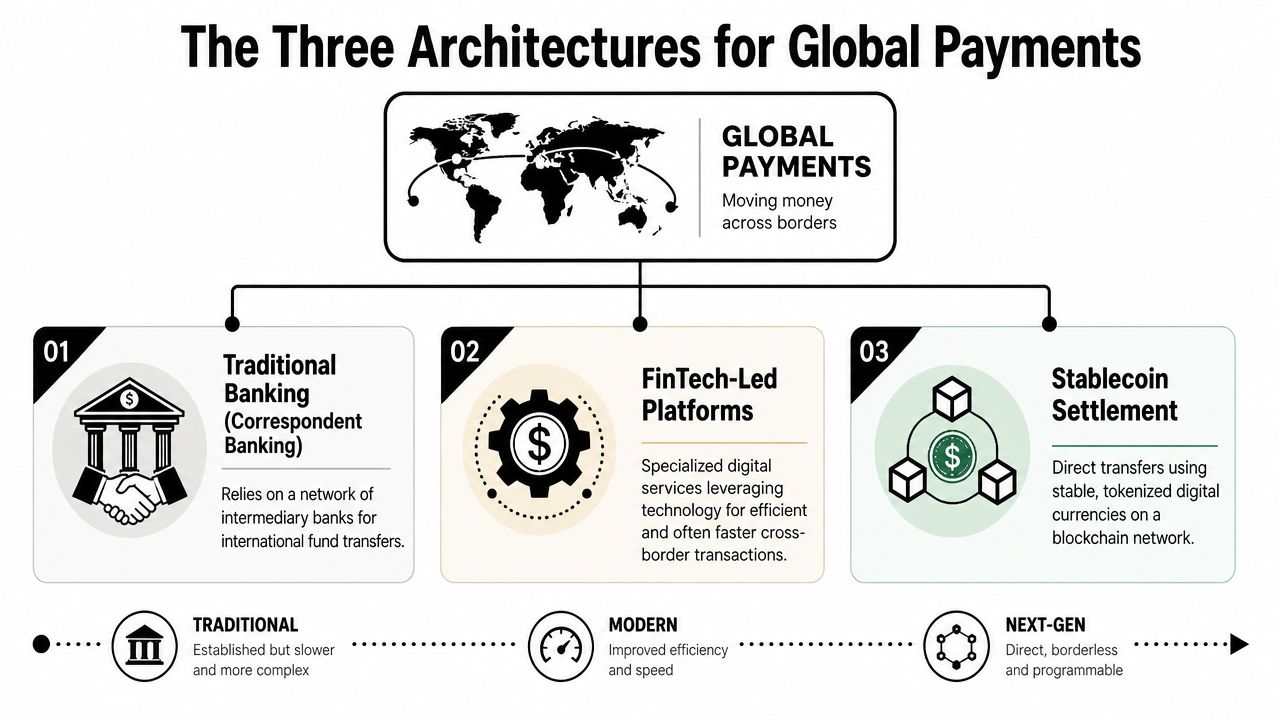

The Three Architectures for Global Payments

There are many vendors in this space, but most cross border payments solutions fit into three underlying architectures. Once you understand the architecture, the trade-offs become easier to evaluate.

Traditional banking

This is the oldest model. Funds move through banks, often across correspondent relationships, with SWIFT used as the messaging layer. It's familiar, institutionally accepted, and still necessary for many treasury-heavy businesses.

Its weakness is operational drag. The Financial Stability Board identifies four persistent problems in cross-border payments: high costs, low speed, limited access, and insufficient transparency, as outlined in the FSB work on cross-border payments. The same guidance notes that some cross-border transfers can cost up to 10 times more than domestic payments, and only about half of wholesale payments settle within an hour.

That doesn't mean banks are obsolete. It means they're often the wrong default for an internet business that needs fast iteration and clear payment status.

Fintech-led platforms

Fintech aggregators sit on top of multiple payment rails and package them into one product. They usually improve onboarding, dashboard visibility, API design, and access to local payment methods. For many startups, that's a major upgrade over dealing directly with banks.

The catch is architectural. Many of these providers still rely on the same banking infrastructure beneath the surface. So the user experience may feel modern while settlement remains constrained by older rails, banking windows, or partner dependencies.

If you want a practical overview of that broader environment, this guide on cross-border payment models is useful because it frames the problem in terms of payment flow design, not just provider branding.

Stablecoin settlement rails

This model changes the payout side of the equation. The customer can still pay through familiar methods, but settlement can happen on stablecoin rails instead of waiting for traditional cross-border bank movement. That reduces the number of intermediaries and makes fund movement easier to track.

Practical rule: Don't compare architectures only by checkout experience. Compare them by what happens after the customer has already paid.

For startups, this matters because the biggest operational headaches usually begin after authorization succeeds. The question isn't just “can we collect money?” It's “how reliably can we receive, account for, and use it?”

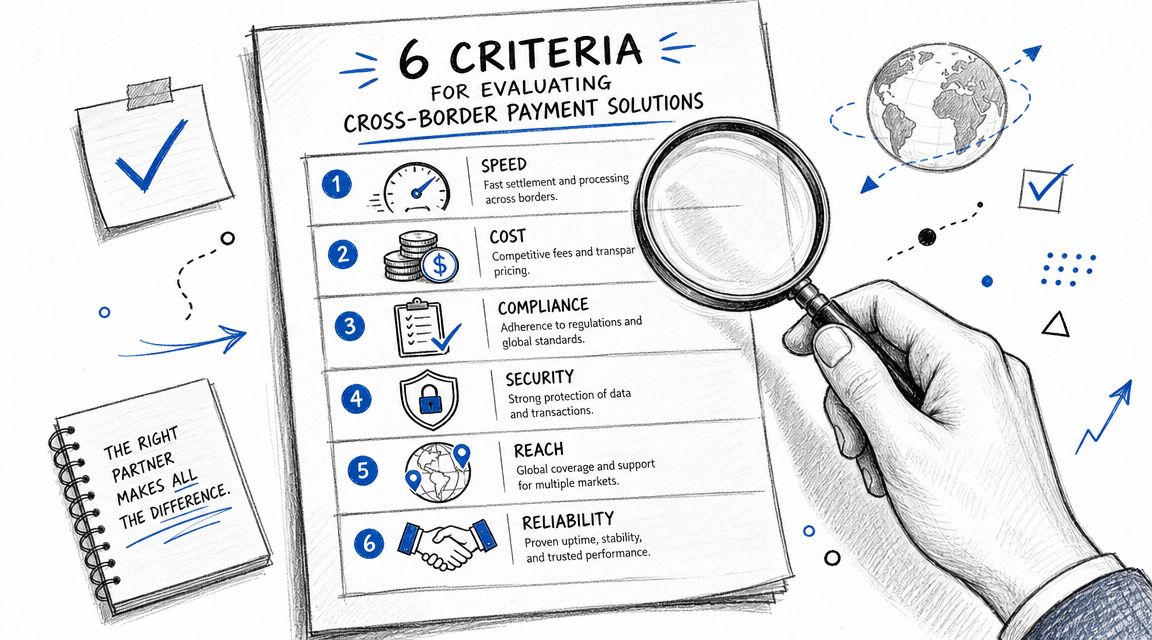

Key Criteria for Evaluating Solutions

The headline fee rarely tells the full story. Strong cross border payments solutions are judged by how they behave in production, under support pressure, and at month-end close.

Total cost is more than the processing fee

A payment stack can look cheap at checkout and still be expensive in practice. You need to look at processing fees, FX spread, intermediary deductions, payout costs, dispute handling, and the internal labor needed to explain exceptions.

Transparency is a real market weakness. A global survey cited by ACI Worldwide found that only about 56% of payment services provide clear cost and speed information to end users, according to ACI Worldwide's review of cross-border payment challenges. If your buyer or recipient can't tell how much will arrive or when, support costs rise immediately.

Predictability matters as much as raw speed

Fast settlement is useful. Predictable settlement is what finance teams build around.

When I review a payment design, I care less about the best-case path and more about variance. Does settlement arrive in a narrow, understandable pattern, or does it drift based on corridor, bank behavior, or manual review? Teams can plan around a known timing model. They struggle when every payout needs interpretation.

The strongest evaluation questions are simple:

- When are funds considered settled

- What causes delay

- Who can see payment status

- How are exceptions reported

- What amount is guaranteed to arrive

A compliance review belongs in the same discussion. If you're serving regulated markets or larger clients, your vendor choices need to fit your resilience posture. In this context, a resource like the DORA compliance framework becomes useful, especially for teams that treat payments as critical infrastructure rather than a plugin.

Developer and operations fit decide the long-term outcome

A provider can look great in a sales demo and still be painful for engineers. Developer experience matters because payment edge cases don't disappear. They surface through retries, webhook handling, subscription states, refunds, and internal reconciliation.

Good infrastructure usually has these traits:

- Clear API primitives, so payments, customers, subscriptions, and payouts map cleanly to your product model.

- Useful webhooks, with event design that supports retries and idempotent processing.

- Readable documentation, because your team won't remember platform-specific quirks six months later.

- Operational visibility, including dashboards that help support and finance answer questions without engineering involvement.

A short walkthrough can also help teams align on what they're evaluating before integration starts.

A Detailed Comparison of Payment Models

Traditional banking and fintech aggregators are still the two most common starting points for global businesses. They solve different problems, and both come with trade-offs that matter once volume and support complexity increase.

Where traditional banking still works

If your company already operates with treasury staff, established banking relationships, and internal controls built around bank-led workflows, traditional banking can still fit. It's often accepted by enterprise counterparties, and legal or procurement teams may prefer it because they understand it.

The downside is the workflow around it. Payment initiation, status visibility, and exception handling often remain fragmented. You may get broad reach, but not always the kind of operational clarity a startup wants. For engineering teams, direct bank integrations can also be awkward, inconsistent, or too slow to adapt to product changes.

Where aggregators improve the picture

Fintech aggregators improve the front-end experience dramatically. You usually get cleaner APIs, hosted checkout options, support for more local payment methods, and a more usable dashboard. That can reduce time to launch and lower the amount of bank-specific logic your team has to own.

Still, the business should ask hard questions about the payout side. Some platforms abstract complexity well. Others move it into pricing tiers, reserve logic, payout holds, or delayed reconciliation. If your team has studied the trade-offs in building products with Stripe, you'll recognize the general pattern. A clean developer surface can still hide operational dependencies underneath.

| Criterion | Traditional Banking (SWIFT) | Fintech Aggregators |

|---|---|---|

| Integration effort | Usually higher, often relationship-driven | Usually lower, API-first or dashboard-first |

| Settlement visibility | Often limited and fragmented | Usually better, but varies by provider |

| Cost clarity | Can be opaque with intermediary and FX effects | Better upfront visibility, but pricing layers can add up |

| Speed consistency | Depends heavily on corridor and banks involved | Often improved, though not always independent of banking rails |

| Global access | Broad in institutional contexts | Broad for digital businesses, especially for checkout acceptance |

| Reconciliation | Often manual or split across systems | Better dashboards, but exports and payout logic still matter |

| Support burden | Higher when status is unclear | Lower than banks, but exceptions still require investigation |

If a provider claims simplicity, ask to see the actual payout lifecycle. That's where complexity usually reappears.

For many startups, aggregators are a sensible step up from banks. But they're still a compromise if the company wants wallet-native settlement, reduced dependence on cross-border bank movement, or tighter control over how revenue arrives.

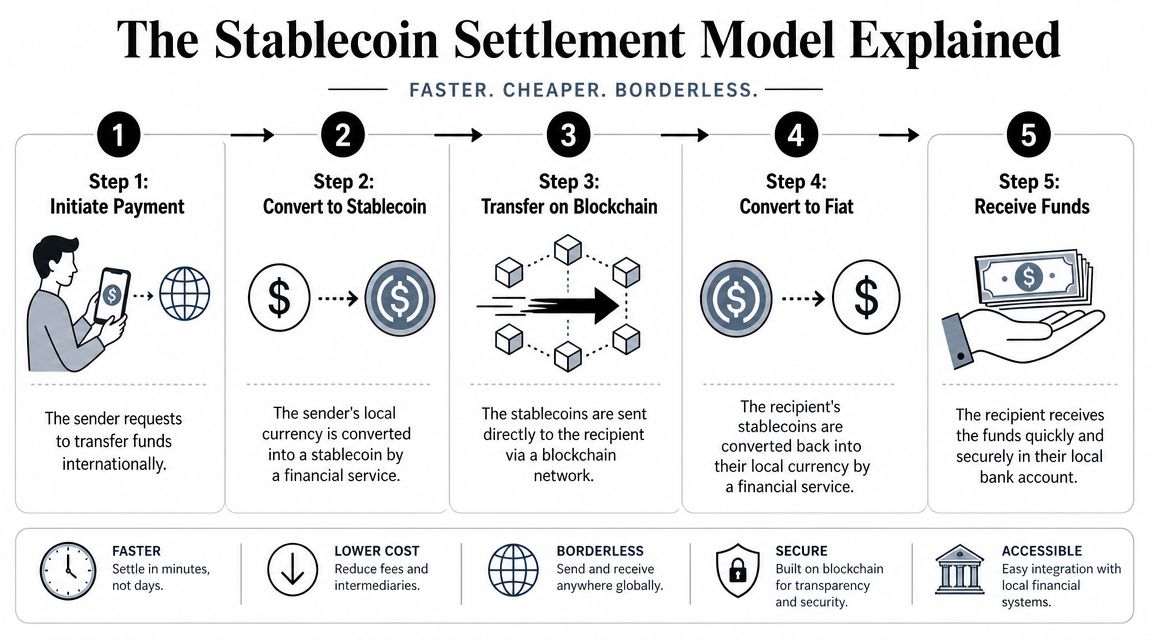

The Stablecoin Settlement Model Explained

Stablecoin settlement changes the shape of the stack. Instead of collecting money and then waiting for traditional cross-border payout mechanics to finish the job, the business can settle into a stablecoin balance or wallet-based treasury flow.

How the operating model changes

The European Central Bank notes that where stablecoin-based settlement is used, transfer finality is typically measured in seconds to minutes, and the main performance variable becomes the cost of conversion rather than wire latency, as discussed in the ECB analysis on payment integration and settlement.

That point is more important than it may sound. In bank-led cross-border systems, delay often comes from the path money takes through institutions. In stablecoin-led settlement, the key questions become different:

- How does the payer enter the system

- How is conversion handled

- Where does settlement land

- How does finance reconcile wallet receipts with order data

- What compliance controls sit around the flow

This is why stablecoin settlement isn't just “faster payments.” It's a different operating model for treasury, reconciliation, and payout planning.

What this looks like in a product flow

One practical example is Suby's cross-border payment flow. The model is straightforward: a business can accept payments by card or crypto, and the business receives USDC. That means the checkout can stay familiar for the buyer while the payout side becomes more predictable for the merchant. Suby also offers an API for integration and native Discord and Telegram integrations for subscriptions, paid access, and online communities.

That combination matters for internet-native businesses. Users pay with cards, businesses receive USDC. Finance no longer has to wait on a bank payout chain to know what treasury received, and engineering doesn't have to stitch together separate tools for checkout, recurring billing, and access control.

The strongest stablecoin payment setups don't ask customers to change behavior. They change the settlement layer behind the scenes.

This model still has real design choices. Teams need to decide who controls wallets, how refunds and disputes are handled, how accounting maps wallet receipts into revenue reporting, and whether the business wants to hold USDC or convert further downstream. But those are explicit decisions, which is usually preferable to inheriting hidden timing and fee behavior from a bank chain you can't inspect.

Choosing the Right Solution for Your Business

The right architecture depends less on industry labels and more on how your revenue moves. Three business profiles show the difference clearly.

Global SaaS companies

A SaaS company usually cares about recurring billing, reliable card acceptance, and predictable settlement for subscription revenue. If the team is global from day one, it also needs clean event handling for upgrades, renewals, failed payments, and access state changes.

For this profile, fintech aggregators can work if the main goal is fast launch with a familiar dashboard. Stablecoin-settled flows fit better when the company wants clearer payout logic and wallet-based treasury. If your finance team spends too much time chasing FX effects or reconciling delayed receipts, that's a sign to look beyond standard aggregator setups.

For founders comparing options, this overview of fintech platforms for cross-border payments without a bank is useful because it frames selection around operating model, not just feature lists.

International ecommerce merchants

Ecommerce merchants usually prioritize conversion first and operations second, until operations become painful. The issue is that international selling creates constant mismatch between the buyer's payment experience and the merchant's settlement experience.

A practical fit here is often a provider that keeps checkout simple while reducing payout uncertainty. Merchants also benefit from tooling around invoice and payout data, especially when cross-border records need cleanup before accounting import. Something like DigiParser for invoice automation can help teams standardize messy invoice inputs before they hit reconciliation workflows.

Creators and community businesses

Creators, membership businesses, and community operators don't just need payment acceptance. They need payment-triggered access control. That changes the buying criteria completely.

The best fit here is usually a system that combines:

- Card acceptance, because the audience wants a familiar way to pay

- Recurring subscriptions, so access renews automatically

- USDC settlement, when the operator wants predictable cross-border revenue receipt

- Access automation, especially for Discord or Telegram communities

Traditional banking is rarely a good fit for this profile. Aggregators can work for checkout, but they often leave community access and payout design to other tools. A stablecoin-settled, access-aware product is often cleaner.

Your Implementation Checklist and Next Steps

The fastest way to make a bad payment decision is to evaluate providers only from the checkout demo. The better approach is to audit the full flow from customer payment to final reconciliation.

Use this checklist before you commit:

- Map your incoming payment methods. List where customers pay by card, where they expect local methods, and where crypto acceptance is relevant.

- Document settlement expectations. Decide how fast funds need to arrive and how much timing variance your business can tolerate.

- Break down total cost. Include processing, conversion, payout, support overhead, and reconciliation effort.

- Review developer workload. Look at API quality, webhook behavior, documentation, and how easily your team can test failure cases.

- Check compliance responsibilities. Clarify which controls belong to your provider and which still sit with your business.

- Test finance operations. Make sure accounting can understand what was paid, what settled, and what arrived.

- Run a corridor-based pilot. Start with a few real markets, then inspect settlement behavior before broader rollout.

Choose the model your support, finance, and engineering teams can all explain the same way. If each team tells a different story about how money moves, the architecture is too opaque.

If you want an API-first option, start with the basics. Confirm your checkout requirements, define your settlement preference, test webhooks, and make sure the payout format matches how your finance team books revenue. For teams that want to accept payments by card or crypto while receiving USDC, a wallet-settled model is often the cleanest way to remove cross-border banking friction without forcing a new checkout habit on customers.

If you want to see that model in practice, take a look at Suby. It gives businesses a way to accept payments by card or crypto, while settling revenue in USDC, and it also supports API-based integration plus native Discord and Telegram flows for subscriptions and paid access.