Gaspard LEZIN

A Practical Chargeback Management Playbook for 2026

Master chargeback management with our step-by-step playbook. Learn to prevent, fight, and automate disputes to protect revenue and cut operational costs.

A lot of merchants still treat disputes like a back-office annoyance. That mindset is expensive. Global chargebacks caused an estimated $33.79 billion in losses for merchants in 2025, and Juniper projects that figure will rise by 23% by 2028 in its coverage of online payment fraud losses.

The part many teams miss is that a chargeback usually isn't just a reversed payment. If you are still fuzzy on what a chargeback is, it pulls in support, fraud review, finance, fulfillment, and whoever has to assemble evidence on a deadline. If you sell across cards, wallets, bank methods, and crypto rails, the problem isn't only dispute volume. It's fragmented visibility.

Table of Contents

Chargebacks are a process failure you can manage

What doesn't work

Prevention starts before checkout

The controls that actually reduce disputes

Build a fast intake process

Triage by reason code, not by panic

Match the evidence to the claim

Essential Evidence Checklist for Dispute Representment

A rebuttal letter should read like a timeline

Why manual workflows break first

A practical automation workflow

What to review every cycle

Why a Chargeback Management Playbook Is Non-Negotiable

Teams often look at the disputed amount and stop there. That's the wrong unit of analysis.

For every $30 in chargebacks processed, merchants incur an average loss of $32 in wasted labor, $27 in chargeback fees, and $32 in disputed labor costs, according to an Accertify summary of a Javelin Strategy study on improving win rates and reducing financial loss. Once you see that, a dispute stops looking like a payment problem and starts looking like an operations problem.

That distinction matters. If your team handles disputes ad hoc, support refunds one way, finance logs them another way, and fraud review happens only after the issuer notice arrives. You end up paying for the same chargeback multiple times, in lost revenue, staff time, and preventable mistakes.

Chargebacks are a process failure you can manage

Good chargeback management usually rests on four things:

Prevention: Stop customer confusion, merchant error, and avoidable fraud before they become issuer disputes.

Response: Route alerts fast, assign ownership, and work against the deadline immediately.

Automation: Pull evidence and transaction context from your systems without manual chasing.

Analysis: Review patterns so the same dispute type doesn't keep repeating.

Practical rule: If a dispute requires three teams to hunt for screenshots, email threads, and shipment proof manually, your process is already too expensive.

I've found that the most resilient teams don't treat disputes as isolated incidents. They treat them like recurring signals. One cluster might point to a misleading product page. Another might expose a weak refund handoff. Another might reveal a billing descriptor customers don't recognize.

That broader view is why chargeback management belongs inside the same discipline as fraud controls, refund policy, and operational monitoring. If you need a wider framework for that, this guide to understand business risk management is a useful companion because it puts payment disputes in the context of wider business exposure, not just payment processing.

What doesn't work

A few habits fail almost every time:

Treating every dispute as worth fighting: Some are unwinnable because the underlying transaction was flawed.

Using one evidence packet for every case: Banks don't reward generic submissions.

Reviewing disputes only at month end: By then, the operational fix is usually late.

Leaving ownership unclear: If nobody owns the queue, the queue owns you.

Fortifying Your First Line of Defense Against Disputes

The cheapest chargeback to handle is the one that never gets filed.

In card-not-present commerce, payment chargeback rates typically fall between 0.6% and 1%, which is higher than the 0.5% average fraud rate for general transactions, according to Chargebacks911's chargeback statistics. That gap tells you something important. Not every dispute is pure fraud. A lot of them come from confusion, poor communication, fulfillment issues, or weak internal controls.

Prevention starts before checkout

Prevention starts with what the customer sees, not what your fraud tool sees.

A recognizable billing descriptor is one of the simplest fixes. If your customer bought from "Northstar Fitness" but their statement says something vague, they may dispute first and ask questions later. Format it so the statement clearly points back to your brand, for example, a descriptor like SUBY.FI*YOURBRAND if that matches your payment setup and processor rules.

Then fix the pages customers read when something goes wrong. Refund policy, delivery timing, subscription terms, renewal language, and cancellation steps should be easy to find before payment and inside the receipt email. Hidden terms create avoidable disputes.

A merchant can survive some fraud. A merchant usually struggles more with preventable customer confusion because it keeps repeating until the customer experience changes.

If you're mapping broader exposure beyond disputes, this breakdown of the five main business fraud risks is worth reading. It helps frame chargebacks as one part of a wider control environment.

The controls that actually reduce disputes

The technical side matters too, especially for digital goods, subscriptions, and cross-border sales. Suby provides an API that lets businesses accept payments by card or crypto, and it also offers native integrations with Discord and Telegram for use cases like subscriptions, paid access, and online communities. As a single product, it can be used four ways: Suby Payments for accepting cards, bank transfers, Apple Pay, Google Pay, Klarna, and more, plus crypto through one checkout, Suby Crypto for crypto payments with swap handling and gas sponsorship, Suby Gating for paid access to Discord, Telegram, downloads, and courses, and Suby Invoicing for letting the client pay how they want while the business receives what it wants. That matters in dispute prevention because customers can pay by card, wallet, bank, or crypto, while the business can receive funds to a bank account or in stablecoins like USDC, including the common flow where a customer pays by card and the business receives USDC. Pricing depends on the payment method used, so check Suby's pricing page for exact figures.

What should be in your prevention stack:

Strong authentication: Use SCA and 2FA where available. Friction at the right moment is cheaper than a dispute later.

Transparent fulfillment updates: Send confirmation, shipment, access, or delivery messages automatically. Silence creates suspicion.

Fast refund handling: A clean refund often prevents a formal dispute. Slow refunds often trigger one.

Accurate product language: Match your product page to what the customer receives.

Support escalation paths: Train support to recognize "I don't recognize this charge" and "I didn't get what I expected" as dispute-risk signals.

A good operating rule is simple. If a customer has to work to understand the transaction, the issuer will eventually do that work for them. Layering in dedicated chargeback protection on top of these controls gives you a merchant-side safety net when prevention alone falls short.

For a practical companion on prevention mechanics, this post on how to avoid payment disputes is a useful reference.

Swift Detection and Initial Response Protocols

Once a dispute is opened, speed matters more than perfect formatting.

The teams that lose recoverable disputes usually don't lose because they had no evidence. They lose because the evidence was scattered, ownership was unclear, or the submission started too late. Your first job is to turn a dispute notice into an internal incident with a clock on it.

Build a fast intake process

Start with a standard intake sequence the moment the alert lands:

Confirm the deadline. Banks and processors don't care that somebody was on leave.

Freeze the case data. Pull the order record, payment metadata, support history, refund status, and fulfillment proof immediately.

Assign one owner. Support can help, finance can help, fraud can help, but one person should drive the case.

Flag related activity. Check whether the same customer, cardholder, account, device, or order pattern shows up elsewhere.

Decide whether to accept or fight. Not every case deserves representment.

A real-time monitoring layer helps because the lag between transaction, complaint, and dispute is where teams get blindsided. This article on real-time transaction monitoring is useful if you're tightening that part of the workflow.

Triage by reason code, not by panic

Not all disputes are asking the same question. Your intake should classify the case before anyone starts assembling documents.

Use broad buckets first:

Fraud or unauthorized use: Focus on authentication, transaction logs, prior customer behavior, and access evidence.

Product or service not received: Focus on shipping records, access logs, fulfillment milestones, and customer communications.

Not as described or canceled: Focus on product page language, terms acceptance, renewal notices, and usage history.

Processing or merchant error: Focus on whether you made the mistake. If you did, accept it and fix the root cause.

The first hour should answer one question: "What exactly is the issuer being told happened here?"

This is also the point where many teams overreact and over-collect. Don't ask five people for everything. Ask for the exact records that align with the dispute claim. Broad evidence dumps waste time and often bury the strongest proof.

How to Build and Submit a Winning Dispute Case

Representment is where discipline shows up on paper.

The global average chargeback win rate for merchants is around 20% to 30%, but that can rise to over 42% for organizations that use customized, data-driven representment strategies instead of generic responses, according to Forbes Advisor's chargeback statistics overview. That tracks with what operators see in practice. Banks don't reward volume. They reward relevance.

Match the evidence to the claim

A winning dispute file doesn't try to prove everything. It proves the specific point that matters for that reason code.

For an "unauthorized transaction" claim, AVS, CVV, 3D Secure results, login history, device or IP consistency, and evidence of account access usually matter. For a "product not received" claim, shipment confirmation, delivery proof, tracking events, access timestamps, or service activation logs matter more.

Don't send a fulfillment packet to answer a fraud claim. Don't send authentication logs to answer a cancellation dispute. Tailoring the evidence is the work.

Here is the evidence set I want available for every case, even if I don't submit all of it.

Essential Evidence Checklist for Dispute Representment

Evidence Type | What It Proves | Applicable To |

|---|---|---|

Order confirmation | The customer completed a purchase and received the transaction summary | Most dispute types |

Sales receipt or invoice | The amount, item, date, and transaction details match your records | Most dispute types |

AVS, CVV, or authentication result | The transaction passed verification checks tied to the payment attempt | Fraud or unauthorized claims |

Authorization code | The issuer approved the transaction at the time of sale | Fraud or processing claims |

IP or device log | The purchase or account access came from a consistent environment | Fraud, digital goods, subscriptions |

Delivery confirmation | The goods were shipped and reached the stated destination | Product not received |

Access or usage logs | The customer accessed the digital product, service, or membership | Digital goods, SaaS, subscriptions |

Customer communications | The buyer acknowledged the order, asked for help, or discussed the purchase | Most dispute types |

Refund or cancellation record | You followed your stated refund or cancellation process | Canceled recurring transactions, service issues |

Terms acceptance record | The customer agreed to billing, renewal, or delivery terms | Subscriptions, memberships, digital services |

Product description snapshot | The item or service was described accurately at time of purchase | Not as described claims |

A rebuttal letter should read like a timeline

The letter itself should be short. The documents do the proving. The letter tells the bank how to read them.

Use this structure:

Opening statement: Identify the transaction and state clearly that you are contesting the dispute.

Reason-code response: Name the claim being made and answer only that claim.

Timeline: Show purchase, authentication, fulfillment, communication, and any post-purchase activity in order.

Evidence map: Refer to the attached records by name so the reviewer can follow the packet.

Closing request: Ask for reversal based on the evidence submitted.

A plain example of the narrative style:

The cardholder completed the purchase using a successfully authenticated transaction. The order confirmation was sent to the customer immediately. The service was then accessed from the same account environment. The attached records show the purchase, verification results, and subsequent usage.

That reads better than a defensive essay. Keep emotion out of it. Don't accuse the customer of fraud unless your processor requires that language for a specific workflow. Stick to observable facts.

Three habits improve case quality fast:

Build one packet per reason code. Reuse your process, not the exact contents.

Name files clearly. "Delivery-confirmation-order-1842" is better than "screenshot-final-new."

Submit complete packets. Partial evidence followed by late follow-ups rarely helps.

If the transaction was flawed, accept the chargeback. Good chargeback management includes knowing when not to fight.

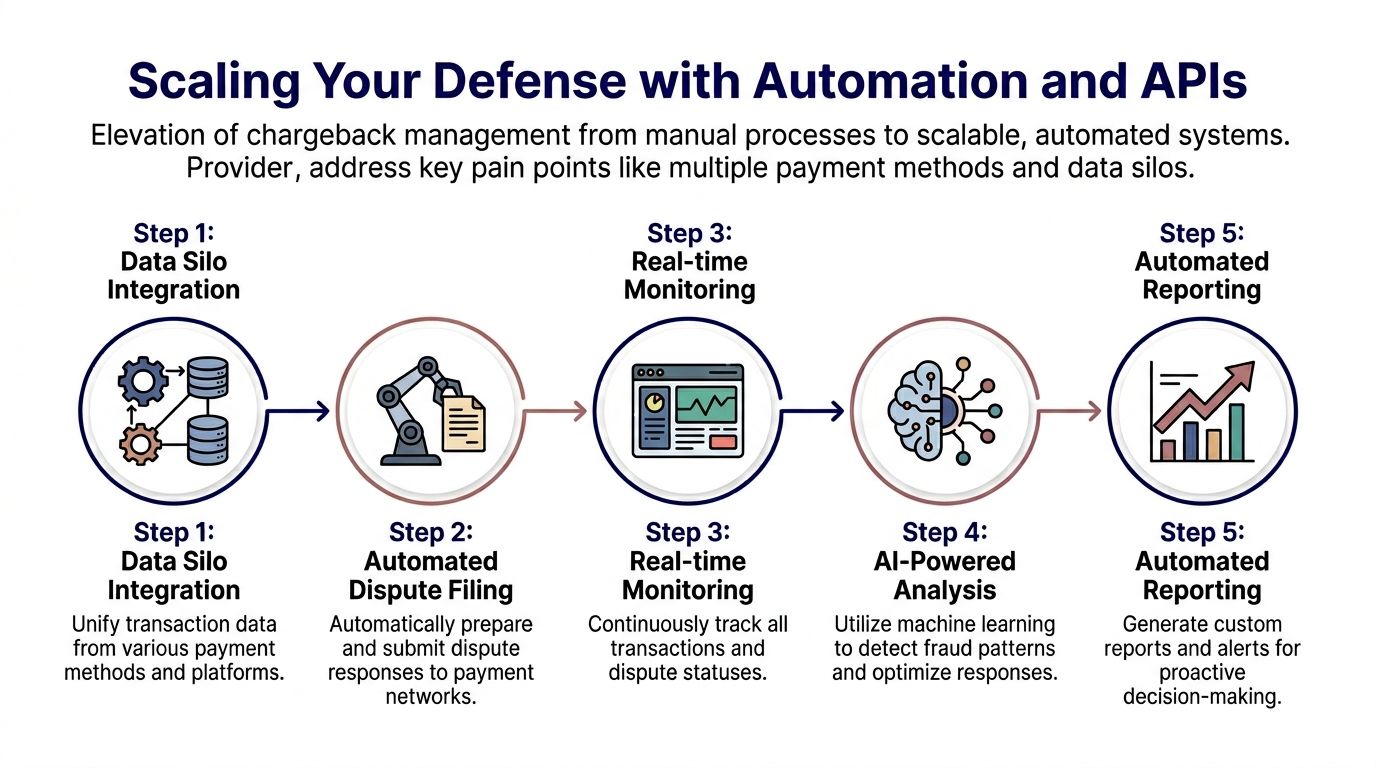

Scaling Your Defense with Automation and APIs

Manual dispute handling works for a while. Then volume, geography, and payment diversity expose every weakness in the process.

A 2025 report from McKinsey says that 42% of cross-border merchants identify data silos from fragmented payment systems as their primary barrier to reducing high chargeback ratios, as cited in McKinsey's global payments report insights. That's exactly what operations teams run into when card disputes live in one portal, wallet issues in another, and crypto transaction context somewhere else entirely.

Why manual workflows break first

The problem isn't only the dispute itself. It's the disconnected evidence trail.

A support agent has the ticket history. Finance has settlement records. Ops has shipment data. Product has access logs. If payments span cards, wallets, bank methods, and crypto rails, nobody gets the full picture without asking three or four teams to reconstruct it.

That is why chargeback management gets expensive as a company grows internationally. Not because the rules become impossible, but because the data gets fragmented.

A practical automation workflow

The fix is straightforward. Use APIs and webhooks to move the first layer of dispute work out of inboxes and into systems.

A workable setup looks like this:

Webhook intake: A dispute event triggers an internal workflow the moment it appears.

Automatic case creation: Your system opens a ticket in a support desk or posts to a private operations channel.

Data enrichment: The workflow pulls order details, transaction status, customer profile, previous refunds, and fulfillment state into one case view.

Owner assignment: Rules route the case by reason code, product type, region, or risk profile.

Submission support: The team reviews a preassembled evidence set instead of starting from zero.

Automation doesn't replace judgment. It removes the repetitive collection work so judgment can focus on whether the case is worth fighting and what evidence actually matters.

A unified payment stack is useful. When one API handles acceptance across card and crypto, and funds land in one balance with payout flexibility to a bank account or in stablecoins like USDC, the dispute workflow gets cleaner because transaction context is less fragmented. That matters even more if you also use native integrations with Discord or Telegram for subscriptions and gated access, where access logs and billing context often need to sit close together.

The practical test is simple. If a dispute arrives, can your system gather what happened without asking three teams to export spreadsheets? If the answer is no, automation will pay for itself in saved time alone.

Turning Chargeback Data into Actionable Insights

Chargeback data should change operating decisions, not just fill a monthly report.

Teams that review disputes case by case usually miss the pattern that caused them. The useful question is not only whether you can win this dispute. It is whether the same failure is about to create 20 more across cards, wallets, and crypto-linked orders.

That matters in a mixed payment stack. Card disputes have formal chargeback workflows. Wallet claims often surface through a different console or support channel. Crypto payments may not reverse the same way, but they still create refund conflicts, access complaints, and fraud signals that belong in the same review. If each method is managed in its own tool, the business sees fragments instead of causes.

What to review every cycle

Review disputes in clusters your operations team can act on:

By product or offer: Repeated disputes on one SKU, subscription tier, or gated community plan usually point to a promise, billing, or delivery problem.

By payment method: Cards may show friendly fraud or descriptor confusion. Wallets may expose authentication or account-mismatch issues. Crypto orders often reveal refund-policy friction or fulfillment disputes.

By region: Cross-border sales often surface support-hour gaps, language issues, and tax or pricing confusion.

By reason code or claim type: Unauthorized use, duplicate billing, and "not as described" each need a different fix.

By support history: Cases with slow replies, no refund decision, or unclear cancellation handling are more likely to escalate.

Counts are only the start. Pull a sample from each cluster and read the full order path, payment event, support thread, and fulfillment record. That is usually where the operational mistake shows up.

A single reporting view helps because dispute analysis falls apart when payments, settlements, refunds, and support outcomes live in separate systems. Teams need to compare what the customer paid, what the processor settled, what the business refunded, and what access or fulfillment the customer received. That gets harder when cards, wallets, bank payments, and crypto all feed the same revenue line.

If your records still need manual matching before anyone trusts the numbers, fix that first. This guide to payment reconciliation for mixed payment flows covers the foundation.

The review cadence can stay simple. Pull the latest dispute batch, group it by payment method and root cause, then assign one fix per pattern. Change the descriptor. Tighten refund rules. Rewrite the offer page. Add wallet-specific support macros. Adjust how crypto purchases are documented and fulfilled.

Suby is a payment gateway and Merchant of Record. Your customers pay with card, bank transfer, Apple Pay, Google Pay, Klarna, and more, or stablecoins, and you get paid out to your bank account, or directly in stablecoins (USDC, EURC) to your wallet, anywhere in the world, no bank account required. Because card and crypto activity sits under one payment layer with native Discord and Telegram access, chargeback management gets easier: transaction context, settlement behavior, and customer access history all live in one place instead of scattered across disconnected tools.