You log in, see a dispute notification, and the first question is usually the same: was this fraud, a confused customer, or something your own checkout flow caused? The frustrating part is that the answer changes what you should do next. A refund might have solved it earlier. A chargeback means the bank is already involved, money is at risk, and your team now has work to do under a deadline.

That's why chargeback protection needs to be treated as an operating system, not a plugin. If you accept card payments, you need controls before the transaction, a response path when a customer disputes, and a process for recovering revenue when the claim is weak. That matters even more for internet businesses that want fast, predictable settlement. If customers pay by card and your business receives USDC, card risk doesn't disappear. It just needs to be managed with more discipline.

Table of Contents

- Why Chargeback Protection Is a Critical Business Strategy

- Refunds and chargebacks are not the same thing

- Who does what in the dispute flow

- Customer clarity prevents avoidable disputes

- Checkout controls catch risk before it settles

- Documentation starts before the dispute

- Three different products get sold as chargeback protection

- Where third-party coverage often falls short

Why Chargeback Protection Is a Critical Business Strategy

A chargeback is not just a reversed payment. It is a formal dispute process that pulls in the customer's bank, puts revenue at risk, and creates extra operational work for your team. If your business sells subscriptions, digital access, software, services, or cross-border goods, one dispute rarely stays isolated. The same root issue often shows up again in billing descriptors, customer support logs, refund handling, or fraud screening.

The scale alone should end any debate about whether this deserves attention. Chargeback volume is projected to reach 281.3 million transactions in 2026, and another benchmark cites $117 billion in global chargeback volume by the end of 2023. U.S. merchants also win only 54% of the chargebacks they fight through representment, according to chargeback statistics compiled by Chargeback.io. That means many merchants are losing disputed revenue even after doing the work to contest it.

Practical rule: If you only think about chargebacks after the alert arrives, you're already late.

The bigger operational mistake is treating chargeback protection like a single vendor feature. It isn't. Some tools try to stop fraud before approval. Some intercept disputes before they become chargebacks. Others help with representment after the fact. Merchants need all three layers working together, especially when margins are tight and card network monitoring thresholds are a real concern.

For teams that want customers to pay with cards while the business receives USDC, this becomes even more relevant. The payout model may be cleaner, but the card side still carries dispute risk. Fast settlement helps cash flow. It doesn't replace disciplined chargeback management.

Understanding the Chargeback Lifecycle

Most merchants fight chargebacks poorly because they don't map the process correctly. They treat it like a refund request that escalated. It's closer to a structured case review, led by banks and governed by card-network rules.

Refunds and chargebacks are not the same thing

A refund is a direct agreement between merchant and customer. You decide to return the money, usually because the customer contacted you and you accepted the request. That's operationally annoying, but manageable.

A chargeback begins when the customer goes to their bank instead. Once that happens, the dispute moves into a formal flow. Funds may be reversed while the claim is reviewed. You then have to decide whether to accept the loss or contest it through representment.

That difference matters because the evidence standard changes. A customer-service promise that would have resolved a refund may not be enough in a chargeback. Banks want documentation.

Who does what in the dispute flow

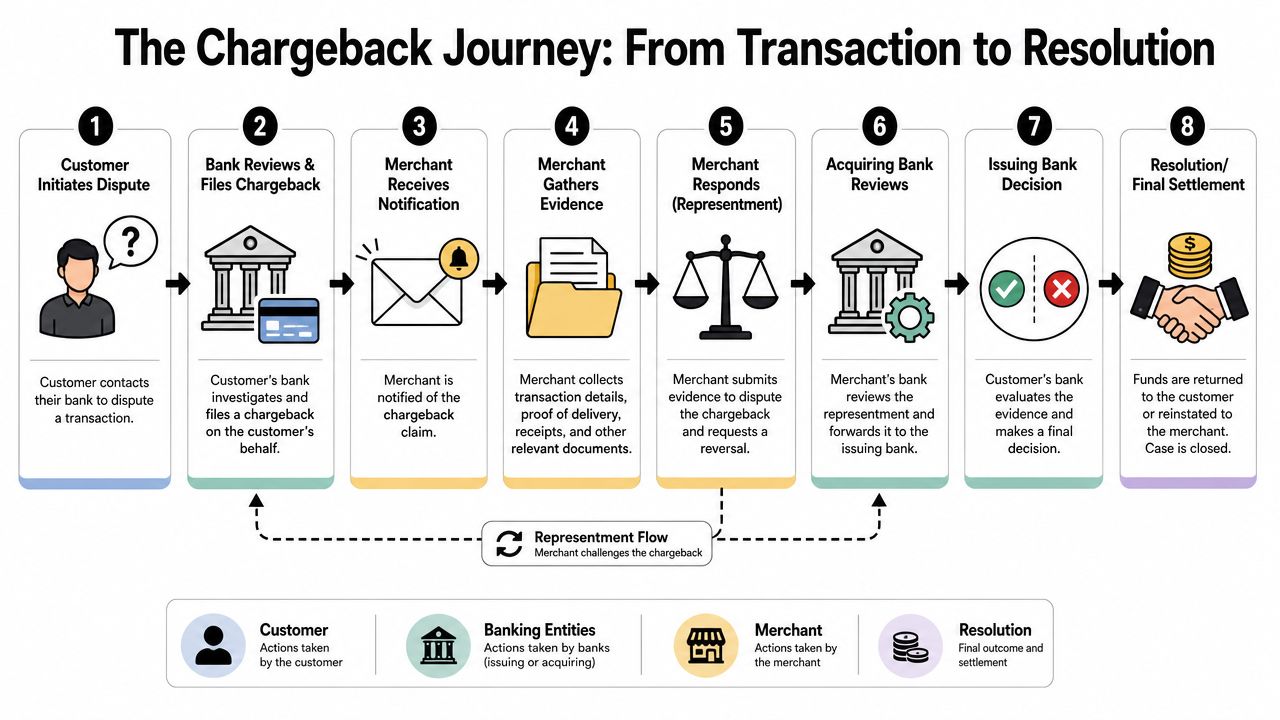

The chargeback lifecycle usually moves through a sequence like this:

The customer disputes the transaction

They contact the issuing bank and claim the charge was unauthorized, not received, not as described, or otherwise invalid.The issuing bank reviews and files the chargeback

If the bank accepts the complaint, it initiates the dispute through the card rails.The merchant gets notified

The notice usually includes a dispute reason and a response deadline. This often results in many teams losing time because the internal owner isn't clear.The merchant gathers evidence

You pull the order record, checkout details, delivery proof, usage logs, support history, refund policy, and any customer acknowledgement.The merchant submits representment

This is the formal response arguing that the transaction was valid or that the dispute reason doesn't fit the facts.The acquirer and issuer review the case

Your acquirer passes the package through the network. The issuer reviews the response and decides whether to uphold or reverse the chargeback.

When merchants lose disputes, it's often because the evidence was late, thin, or mismatched to the claim.

A useful way to think about it is simple: a chargeback is a documentation contest under time pressure. The customer has a story. The bank has a process. The merchant needs records that line up with the reason code and show why the transaction should stand.

Building Your First Line of Defense

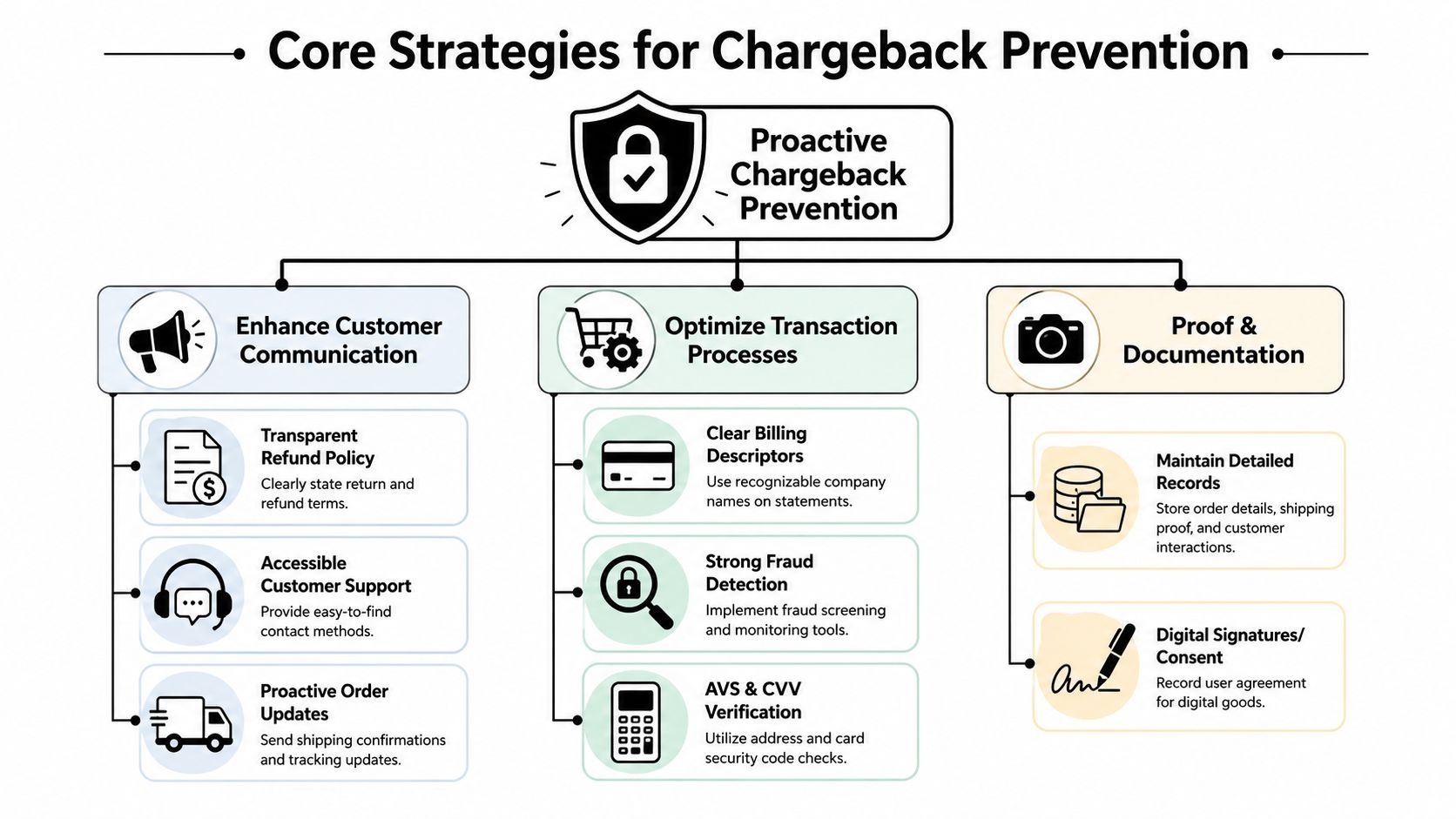

The cheapest chargeback to manage is the one that never gets filed. Prevention is mostly about reducing customer confusion, blocking obvious fraud, and keeping enough records to discourage weak claims later.

Customer clarity prevents avoidable disputes

Many disputes start long before the bank ever hears about them. The customer doesn't recognize the billing descriptor. They can't find support. They expected a refund path and hit silence instead.

Start with the parts you control:

- Use a recognizable billing descriptor: If your legal entity and brand name differ, make the descriptor as close to the customer-facing brand as possible.

- Publish refund and cancellation terms clearly: Don't bury them in a footer or write them like legal camouflage.

- Make support easy to reach: Email, chat, and account-level self-service all reduce the odds that a frustrated buyer goes straight to the bank.

- Send order and delivery confirmations: For physical goods, include tracking. For digital goods, confirm access, account creation, or entitlement changes.

Global card fraud losses reached about $34 billion in 2023 and are projected to keep rising, while common prevention levers still include AVS/CVV, 3-D Secure, and strong customer service policies, according to Chargeback Gurus on protecting businesses from chargebacks. That's a useful reminder. The basics still matter.

A practical addition is tighter traffic hygiene. If you're seeing repeated suspicious attempts from the same sources, this guide to mastering IP security is worth reviewing as part of your wider abuse-prevention setup.

Checkout controls catch risk before it settles

Fraud tools don't eliminate chargebacks, but they improve your odds before the order is accepted.

Use the controls that fit your checkout flow:

| Control | What it helps with | Where teams go wrong |

|---|---|---|

| AVS | Compares billing address details | Letting mismatches through with no review logic |

| CVV | Verifies the card security code | Treating a pass as proof the buyer is legitimate |

| 3-D Secure | Adds issuer-side authentication | Turning it on blindly without reviewing conversion impact |

| Velocity checks | Detects repeated attempts or unusual purchase bursts | Setting rules too loosely or never revisiting them |

Video walkthroughs can help teams align product, risk, and support around the same prevention model:

If you're tuning checkout risk rules, it also helps to review your broader payment fraud detection approach. The goal isn't to block everything risky. It's to route different risk patterns to the right action, approve, step up, review, or decline.

Documentation starts before the dispute

Teams often think evidence collection begins when the chargeback arrives. It should begin when the order is created.

Keep records that help in a dispute:

- Transaction details: Timestamp, order value, SKU or plan name, billing details, and device or session markers if your stack stores them.

- Customer consent: Accepted terms, recurring billing agreement, cancellation flow, or acknowledgement for digital access.

- Fulfillment proof: Shipment confirmation, delivery confirmation, access logs, download records, or membership activation.

- Support history: Emails, chat logs, refund discussions, and any resolution the customer accepted.

Good prevention looks boring from the outside. Clear descriptors, working support, clean logs, and sensible fraud rules don't feel sophisticated. They win anyway.

How to Respond When a Chargeback Occurs

Once a chargeback lands, the job changes. You're no longer trying to stop a bad order. You're trying to prove a disputed transaction was valid, or at least show the dispute reason doesn't match what happened.

Industry guidance consistently points to a three-stage control system, prevention before authorization, intervention before the chargeback posts, and post-dispute recovery through representment, because each stage attacks a different failure mode, as explained in Solidgate's guide to chargeback protection. This is the recovery stage, and the difference between winning and losing usually comes down to speed and evidence quality.

Speed matters more than most teams think

A slow response kills otherwise winnable cases. Notifications get buried. Support has one part of the record, finance has another, and whoever owns disputes is waiting on screenshots from three systems.

Treat dispute handling like an operations process, not an inbox task. Good teams usually do three things fast:

- Assign an owner immediately: One person should own the case, even if several teams contribute evidence.

- Use a standard evidence checklist: Don't rebuild the package from scratch each time.

- Triage by dispute type: Unauthorized use, item not received, recurring billing confusion, and service dissatisfaction all require different proof.

If your team hasn't formalized that workflow yet, these incident response best practices are a useful model. The same discipline applies. Clear ownership, fast escalation, and documented steps beat ad hoc reactions.

Match evidence to the claim

The most common mistake in representment is sending accurate evidence that doesn't answer the actual allegation.

A better approach looks like this:

Unauthorized transaction claim

Show AVS and CVV results if you have them, any successful customer authentication step, the order record, prior account history, and evidence the cardholder used the service or received the product.Item not received claim

Lead with shipment and delivery proof, tracking history, delivery confirmation, and customer messages acknowledging shipment or receipt.Recurring billing dispute

Provide the sign-up record, accepted recurring terms, billing reminders if applicable, account access history, and cancellation policy acknowledgement.Friendly fraud pattern

Use support logs, login activity, usage evidence, download or access history, and prior non-fraud complaints from the same customer if relevant to the case.

Don't argue emotionally. Build a file that makes the bank's decision easy.

Some disputes should not be fought. If your team shipped the wrong item, failed to process an agreed refund, or made a billing error, accept the loss, fix the process, and move on. Representment is for disputable claims, not for defending avoidable mistakes.

Evaluating Third-Party Protection and Insurance

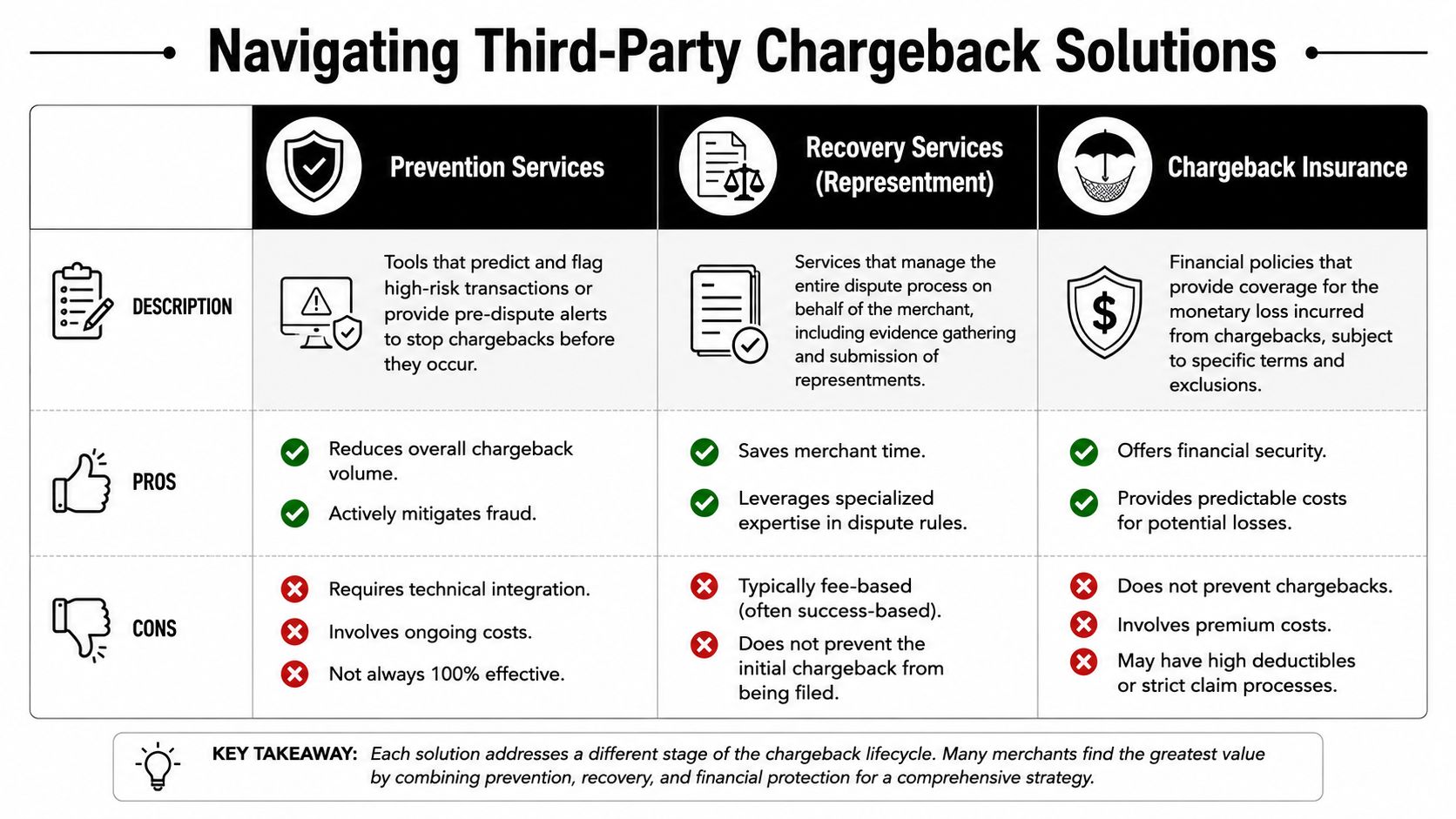

The market uses the phrase chargeback protection too loosely. Merchants hear it and assume someone else will absorb the loss. In practice, different vendors solve very different problems.

Three different products get sold as chargeback protection

Here's the cleaner way to separate them:

| Category | What it does | Best use case | Main limitation |

|---|---|---|---|

| Prevention services | Scores or blocks risky orders, sometimes adds pre-dispute alerts | Merchants with fraud pressure before approval | Doesn't recover losses from disputes already filed |

| Recovery services | Manages representment and evidence workflows | Teams with weak internal dispute operations | Helps after the event, not before it |

| Insurance or indemnification | Reimburses certain covered losses | Merchants wanting cost predictability for specific dispute types | Coverage is usually narrower than expected |

That distinction matters when comparing vendors, but it also matters when deciding whether you even need one. Some merchants don't need outsourced representment first. They need better descriptors, clearer support, and a less messy cancellation flow.

If you're reviewing who should hold payment responsibility across markets, business models, and support flows, this overview of the best merchant of record options can help frame the operational trade-offs.

Where third-party coverage often falls short

Coverage limits are where expectations usually break.

Industry analysis notes that chargeback protection is not a single product category, and one expert estimate says only 20-30% of all chargebacks typically qualify for reimbursement under insurance-style products. It also notes that many reimbursement programs cover approved orders for unauthorized use rather than the full range of dispute types, in AlphaComm's review of chargeback protection. That means common problems like friendly fraud, product dissatisfaction, or service-quality disputes may still land on your desk.

A concrete example is useful here. PayPal's Chargeback Protection applies only to eligible merchants and only to specific dispute types such as unauthorized transactions and item not received, with eligibility tied to terms including proof of shipment or delivery and a monthly loss cap structure, according to PayPal's Chargeback Protection help documentation. It does not cover every reason a customer might dispute a payment.

So when a vendor says “we cover chargebacks,” ask sharper questions:

- Which dispute reasons are covered

- What proof is required from the merchant

- Whether friendly fraud is excluded

- Whether reimbursement applies only to approved transactions

- Who handles representment and who just pays after the loss

- What happens when documentation is incomplete

If the contract says reimbursement is conditional, assume your operations still determine the outcome.

The right third-party tool can absolutely help. It just won't rescue a merchant with weak support, messy records, or poor fraud controls.

Managing Disputes with Suby

For merchants using Suby, the chargeback playbook stays the same on the card side. Prevention, intervention, and recovery still matter. What changes is how the payment flow and settlement model fit into your operations.

Suby provides an API that lets businesses accept payments by card or crypto, and it also offers native integrations with Discord and Telegram for subscriptions, paid access, and online communities. Customers can pay with cards, and businesses receive USDC. That model is useful for internet businesses that want a familiar checkout experience on the buyer side with predictable settlement on the merchant side.

What changes when cards fund USDC settlement

Dispute handling still depends on merchant evidence. If a customer challenges a card payment, your team still needs the same fundamentals: clear order records, proof of delivery or access, billing transparency, and support history. No payout model changes that.

What does improve is financial clarity. When your business operates around USDC settlement, it's easier to reason about the commercial effect of a lost dispute than in setups where money moves through multiple bank rails, payout windows, and currency conversions. For global businesses, that cleaner settlement path can make reconciliation simpler.

Suby is also built for practical implementation. Merchants can use paylinks, embedded checkout, or direct API integration, and the platform supports one-time payments and recurring subscriptions. That matters because the strongest dispute operations rely on good system records. The easier it is to connect payment events, subscription status, and access history, the easier it is to prepare a defensible response when a dispute appears.

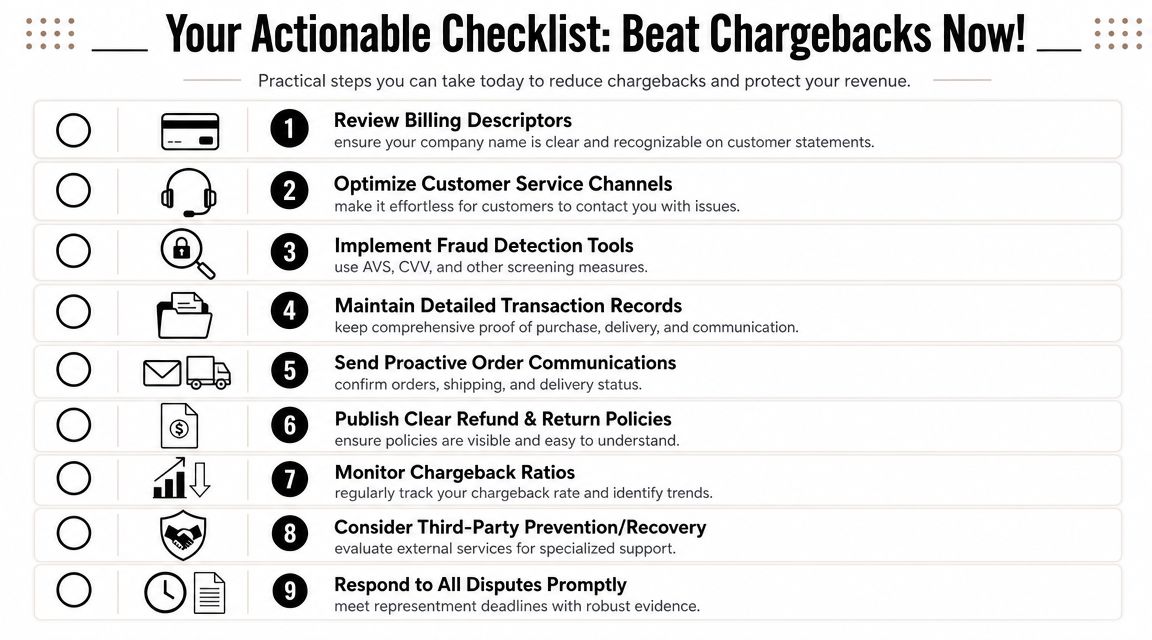

A Practical Checklist for Reducing Chargebacks

Most chargeback problems aren't solved by one big change. They improve when merchants tighten the small operational points that disputes tend to expose.

Run through this checklist against your current setup:

- Review billing descriptors: Is the name on the card statement immediately recognizable to the customer?

- Check support paths: Can a customer find help faster than they can find the number for their bank?

- Require core fraud controls: Are AVS, CVV, and any appropriate authentication steps configured sensibly for your checkout?

- Confirm order messaging: Do customers receive payment confirmation, fulfillment updates, and recurring billing context where relevant?

- Store usable records: Can you quickly pull proof of purchase, proof of delivery or access, customer consent, and support history?

- Audit refund handling: Are promised refunds processed cleanly and documented?

- Prepare dispute templates: Do you already have response templates for item not received, unauthorized use, recurring billing, and service-access claims?

- Review specialist support: If internal operations are stretched, have you evaluated where external prevention or representment help fits?

- Respond promptly every time: Even weak disputes need a decision and a workflow, not silence.

Customer communication deserves special attention. Many disputes are downstream of unclear billing, confusing cancellation, or support friction. Teams working on subscription or product support flows may get useful ideas from this piece on solving SaaS customer service challenges.

If you want a practical next step, review your current dispute flow against this checklist and compare it with your existing approach to avoiding payment disputes. The goal is simple. Fewer preventable disputes, better evidence when they happen, and faster decisions across the whole payment stack.

If you want customers to pay with cards while your business receives USDC, Suby gives you a practical way to do it through a single API, paylinks, embedded checkout, and native Discord and Telegram integrations. It's built for subscriptions, paid access, and global online sales, with card and crypto acceptance on the front end and USDC settlement for the business on the back end.