You launch in three countries on Friday. By Monday, sales are coming from places you never targeted, a few customers are emailing about failed checkouts, and your payments team is staring at a dashboard full of edge cases. Some transactions look great. Some look strange. A few are probably fraud, but if you block too aggressively, you'll reject real customers.

That's the point where real-time transaction monitoring stops sounding like bank jargon and starts sounding like basic survival.

For internet businesses, the problem is bigger than card fraud alone. Many teams now run a hybrid stack. Customers want to pay with cards or crypto, while the business wants clean operations, predictable settlement, and fewer manual reviews. If you also settle in stablecoins such as USDC, your payment flow moves across more rails, more systems, and more risk surfaces than a traditional single-processor setup. Users pay with cards, businesses receive USDC. That model is powerful, but it needs monitoring that can keep up.

Table of Contents

The Hidden Risks of Global Digital Payments

A familiar story goes like this. A SaaS founder opens access to global checkout, sees a burst of new subscriptions, then gets hit from three directions at once. One cluster of payments turns into disputes. Another cluster triggers compliance questions because the activity pattern looks unusual. A third group is made up of legitimate buyers who now can't get through because the fraud rules were tightened too fast.

That sequence happens because digital payments create overlapping risk, not one clean category. Fraud risk, chargeback risk, compliance risk, and operational risk all show up in the same queue. If your team reviews everything after the fact, you're always late. Money has already moved, customer frustration has already happened, and your ops team is already in cleanup mode.

For online businesses, especially those selling globally, payment risk often hides inside normal growth signals. A launch, a pricing experiment, a creator shoutout, or a new region can all create sudden volume changes. Those changes can look legitimate to marketing and suspicious to a payments system at the same time.

Real payment risk rarely arrives wearing a label. It usually looks like growth, until someone checks the details.

Security basics still matter here. If you handle card flows in any way, teams should understand foundational controls such as tokenization, access restriction, and audit readiness. A useful practical reference is Wonderment Apps on PCI DSS best practices, especially for founders who know they need payment security discipline but haven't mapped the operational checklist yet.

The deeper issue is timing. If your monitoring only tells you what went wrong later, it doesn't prevent loss. It documents it. That's why modern payment platforms increasingly treat real-time monitoring as part of the payment path itself, not as a separate reporting layer.

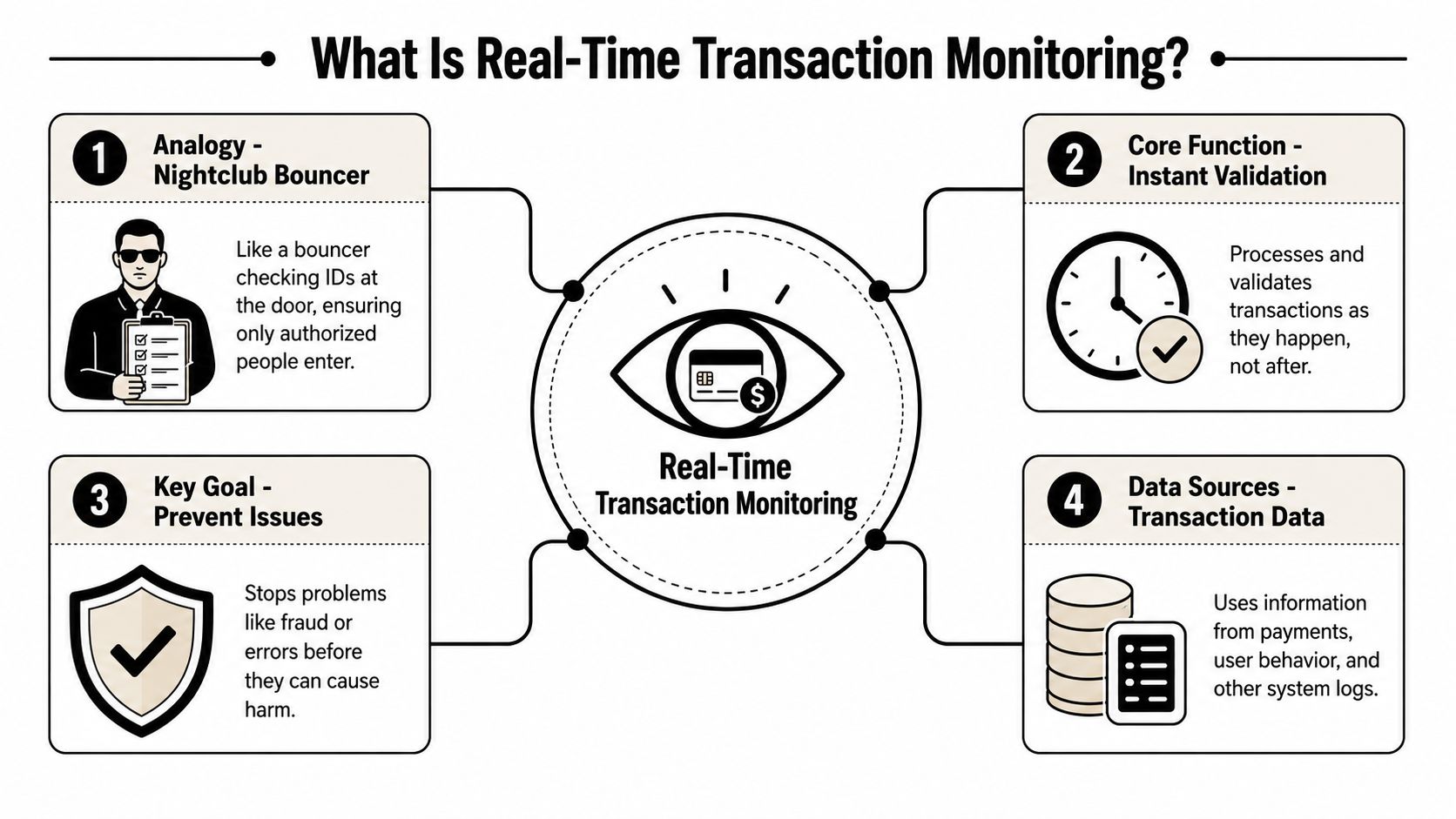

What Is Real-Time Transaction Monitoring

Real-time transaction monitoring means evaluating a payment while it is happening, not hours later in a batch job. The system looks at the transaction, compares it to risk rules and behavior patterns, then decides whether to allow it, hold it, or block it before settlement.

A simple way to think about it

Think about a building entrance.

A live guard at the door checks who's coming in, notices odd behavior, and can stop a problem before it enters the building. A security team reviewing footage the next day may understand what happened, but they can't prevent it. That's the difference between real-time monitoring and batch review.

In payments, that timing difference matters even more because many modern rails settle quickly. According to Tookitaki's explanation of real-time transaction monitoring, these systems analyze payments as they occur rather than in end-of-day batches, so suspicious transfers can be flagged, held, or blocked before settlement. The same source describes this as operating within milliseconds in high-risk environments, which makes latency part of the control itself.

That last point confuses many non-specialists. Monitoring speed is not just a nice engineering metric. It affects the actual outcome. If your risk decision comes too late, you may detect fraud correctly and still fail operationally.

Why milliseconds matter

Real-time systems usually inspect a set of signals in a very short window:

- Transaction context, such as amount, currency, merchant, and payment type

- Customer context, such as whether this is a first-time buyer or a known user

- Behavior context, such as unusual bursts of activity or inconsistent location patterns

- Technical context, such as device or session signals

A good monitoring system doesn't treat every payment the same. It asks, “Is this normal for this user, this channel, and this moment?”

Practical rule: If a transaction can settle before your team can review it, your monitoring logic has to run before or during authorization.

That's why real-time transaction monitoring has become essential for instant payments, card flows with high fraud exposure, and hybrid stacks where card and crypto coexist. When customers pay in familiar ways and the business settles in USDC, the monitoring layer has to interpret activity across different behaviors without adding visible friction to every legitimate purchase.

Why Your Business Needs Real-Time Monitoring

Real-time monitoring is easy to frame as a fraud tool. That's true, but it's incomplete. For most businesses, it's also a revenue tool, a customer experience tool, and a control system for expansion.

It protects revenue, not just compliance

A blocked fraudulent payment saves money. A blocked legitimate payment loses money. Good monitoring has to care about both outcomes.

One industry analysis summarized by Flagright on real-time transaction monitoring ROI says a smarter real-time monitoring system can move approval rates from 95% to 98%–99% on the first pass, leaving only 1%–2% of clearly suspicious transactions to be stopped. The business meaning is simple. Better precision doesn't just reduce bad transactions. It also reduces unnecessary friction for good customers.

That matters if you sell subscriptions, software seats, community access, or digital products. Every extra failed payment can mean a lost renewal, a support ticket, or a customer who never comes back. In fast-moving online businesses, payment failure is often misread as a conversion problem when it's really a risk-decision problem.

A second reason this category matters is scale. The Fact.MR transaction monitoring market report estimates the global transaction monitoring market at US$17.59 billion in 2024, with a projection of US$43.2 billion by 2034 and a 9.4% CAGR. The same report says North America accounted for 33% of global revenue in 2024. That tells you this isn't niche infrastructure. It's a core layer in modern payment operations.

It helps you expand with fewer surprises

When businesses enter new markets, risk patterns change before internal processes do. A region that looks promising from a sales perspective may produce more verification mismatches, more unfamiliar purchasing behavior, or more manual review load.

Real-time monitoring helps because it gives you a controlled way to say yes. Instead of imposing one blunt rule on every transaction, you can evaluate risk based on context and route only the uncertain cases for deeper review.

A quick visual overview helps if you want a non-technical explanation for internal teams:

For operators, the practical benefits usually show up in four places:

- Approval quality improves, because more legitimate customers clear on the first try

- Manual review pressure drops, because analysts focus on the smaller set of ambiguous cases

- Compliance response gets faster, because suspicious activity is identified closer to the transaction event

- Customer trust increases, because the checkout feels smooth without feeling unprotected

The best payment experience is often invisible. The customer only notices it when a legitimate purchase gets blocked, or a fraudulent one gets through.

Core Components and Key Signals to Track

A real-time monitoring system is not one magic model. It's a stack of decision tools working together. In practice, such systems typically combine deterministic rules, pattern analysis, and extra context from surrounding systems.

What a modern monitoring stack actually does

A common design pattern is to calculate risk scores before or during authorization, then pay more attention to scenarios such as cross-border transfers, new accounts, and unusual spikes in activity. AML RightSource's guidance for transaction monitoring in real-time payments also recommends combining threshold-based rules with behavioral analytics, device fingerprinting, and strong authentication to reduce false positives.

That stack usually has three working parts:

Rules engine

This handles direct logic. For example, it can flag repeated attempts from the same account, sudden jumps in order value, or impossible changes in geography.Behavior layer

This asks whether the action fits the user's normal pattern. A purchase may look fine in isolation but become suspicious when compared with recent activity.Enrichment layer

This adds context from outside the raw payment request, such as device reputation, account history, or risk indicators from earlier sessions.

If you want a deeper look at the fraud side of this problem, Suby's guide to payment fraud detection is a useful companion read.

Key transaction monitoring signals

Below is a practical table you can use when reviewing what your current system does and doesn't inspect.

| Signal | What It Indicates | Example |

|---|---|---|

| Transaction velocity | Whether activity is happening too quickly to be normal | The same customer attempts several purchases in a short period |

| First-time customer behavior | Lack of historical trust signals | A brand-new user tries a high-value purchase immediately |

| Cross-border activity | Higher uncertainty due to location, issuer, or settlement differences | A customer account normally active in one region suddenly pays from another |

| Location mismatch | Inconsistency between expected and observed geography | Billing details, device location, and purchasing pattern don't line up |

| Device change | A session that differs from normal user access patterns | An established customer appears on an unfamiliar device during checkout |

| Unusual spike in amount | A transaction value that sits outside the user's normal range | A low-ticket buyer suddenly attempts a much larger payment |

| Payment method shift | Behavioral change that may deserve extra scrutiny | A customer who usually pays one way suddenly switches rails |

| Account age | Whether the user has enough history for low-friction approval | A new account attempts sensitive actions right after signup |

| Repeated decline and retry behavior | Possible testing or evasion attempts | Multiple failed transactions are followed by slightly altered retries |

A common mistake is tracking these signals separately without combining them into a single decision. One unusual trait may mean nothing. Several in the same event usually mean something worth checking.

You don't want more alerts. You want fewer, better alerts with enough context to make a fast decision.

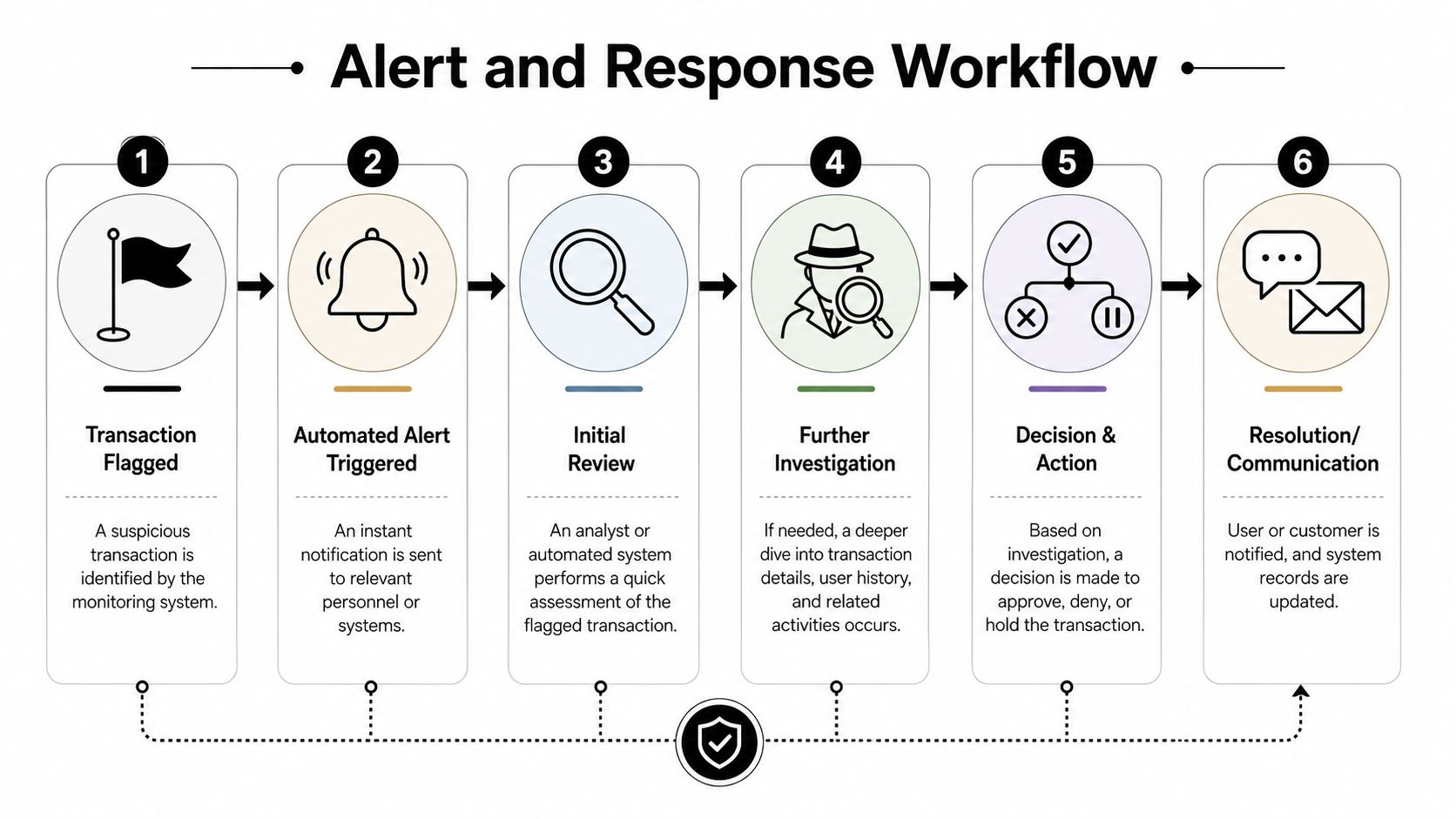

Understanding Alert and Response Workflows

Detection is only half the job. Once a transaction is flagged, your system needs a response path that fits the level of risk. Otherwise, every alert becomes an operational burden.

What happens after a transaction gets flagged

A typical workflow looks like this:

The monitoring layer detects a risk pattern

This may be a rules hit, an anomaly score, or a combination of signals.The system assigns a severity level

Low-confidence issues may get tagged for review. High-confidence issues may trigger an immediate action.Context is attached to the alert

Analysts need more than a red flag. They need evidence, such as account history, prior attempts, device changes, or related transactions.A decision is made

The transaction is approved, declined, or temporarily held.The outcome feeds future tuning

If analysts keep clearing a certain alert type, the rules probably need adjustment.

This workflow sounds obvious, but many teams struggle because they don't separate urgent cases from noisy ones. That's where tuning matters. The same Flagright analysis cited earlier says a well-tuned system can raise approval rates from 95% to 98%–99%, leaving only 1%–2% for review, which is what makes the analyst queue manageable in practice.

If disputes are part of your operating pain, this guide on how to avoid payment disputes pairs well with alert workflow design because better upstream decisions often reduce downstream support and chargeback work.

Hard block or soft flag

Not every suspicious event deserves the same response.

A hard block is appropriate when the risk is clear and immediate. Think stolen credentials, impossible behavior, or a transaction pattern strongly associated with fraud. The goal is prevention.

A soft flag is better when the signal is uncertain. Maybe the customer is new, traveling, or making an unusually large but legitimate purchase. In those cases, forcing manual review or extra verification can protect revenue without rejecting the customer outright.

Use this decision split as a practical rule of thumb:

- Hard block when settlement speed makes recovery unlikely and confidence is high

- Soft flag when more context could rescue a legitimate transaction

- Post-event review when the channel is lower risk or operationally better suited to follow-up analysis

The strongest workflows are boring in the best way. Alerts arrive with context. Analysts know what to do. Customers only feel friction when there's a real reason.

Implementing Monitoring with Suby's API and Dashboard

For developers, the question isn't whether monitoring matters. It's how much of it you want to build yourself.

What implementation looks like in practice

In a hybrid payment stack, the hard part isn't just detection speed. It's deciding which events deserve in-flight action and which can be reviewed later. Industry commentary collected by CSI on AML transaction monitoring trends notes that teams are struggling to tune monitoring for mixed payment environments without creating a false-positive spiral. The practical takeaway is that the best systems choose carefully between in-flight blocking and post-settlement review.

That matters for businesses where customers pay with cards or crypto while the business settles in USDC. Card activity, wallet-based payments, subscriptions, renewals, and one-off purchases don't all behave the same way. A single blunt policy will either miss risk or block too much legitimate business.

A practical implementation usually includes:

- Event-driven alerts through webhooks, so your app can react immediately when a payment state changes or a risk condition requires follow-up

- A review surface in a dashboard, where operators can inspect payment activity, subscriptions, and payout visibility without digging through logs

- Channel-aware policies, so one payment type doesn't inherit rules that only make sense for another

- Feedback loops, where reviewed outcomes inform future rule tuning

For businesses that want one payment layer rather than stitching together separate tools, Suby's global payment API is relevant here. Suby provides an API that lets businesses accept payments by card or crypto, with users paying by card and businesses receiving USDC. It also offers native integrations with Discord and Telegram for subscriptions, paid access, and online communities.

How to think about hybrid payment stacks

If you're designing your own monitoring logic, avoid the temptation to make every risky-looking event a block. That approach feels safe at first, then insidiously harms approval rates and support load.

Instead, define response by payment context:

- Card checkout events often need stricter real-time decisions because user friction, dispute exposure, and authorization timing are tightly coupled

- Recurring payments need continuity logic, because a loyal subscriber with one unusual renewal signal isn't the same as a brand-new user

- Crypto-originating flows may need different evidence, especially around wallet behavior and payment finality

- Access-based products such as communities or digital memberships benefit from monitoring tied to subscription state, not just one payment event

The dashboard matters more than many teams expect. Engineers often focus on the scoring engine, but operators need a clear place to see what happened, why it was flagged, and what action is available. Without that, even a good model creates bad operations.

Build a Resilient Global Payment System

A global checkout stack is only as strong as its decision speed. If your team can't evaluate risk while money is moving, you're left choosing between two bad options. Let more fraud through, or block too many real customers.

That's why real-time transaction monitoring belongs in the foundation of a modern payment system. It helps teams protect revenue, keep approval quality high, and respond to suspicious behavior before settlement turns a warning into a loss. For internet-native businesses, that matters even more when payment methods vary and settlement happens in USDC.

The practical standard is clear. Customers want low-friction checkout. Operators want visibility. Developers want reliable hooks into payment events. Finance wants predictable settlement. A monitoring layer has to support all four.

If your business accepts payments globally, especially across card and crypto rails, the goal isn't perfect certainty. It's fast, well-governed decisions with as little customer friction as possible.

If you're building a payment flow where users pay with cards and your business receives USDC, Suby is worth a look. It provides an API for card and crypto acceptance, supports subscriptions and paylinks, and includes native Discord and Telegram integrations for paid access and online communities.