Your sales dashboard says one thing. Your wallet balance says another. Refunds are trickling in, card payments clear on one timeline, crypto payments on another, and your finance sheet has started to look like a crime scene.

That's where payment reconciliation stops being an accounting chore and becomes an operating system for the business.

For an internet company that accepts cards and crypto but wants a single settlement asset, the key job isn't reconciling bank statements at month-end. It's proving that every customer payment, fee, refund, dispute, and payout can be traced into a clean USDC settlement record. When that logic is tight, cash visibility improves, support gets easier, and month-end stops turning into a hunt for missing money.

Table of Contents

Why Payment Reconciliation is Your Financial Control Panel

Most owners think payment reconciliation starts after the sale. In practice, it starts the moment you need to answer a simple question: did the money move the way you expected?

Payment reconciliation matches your internal transaction records against external records like processor files, bank statements, card-scheme reports, and invoices. That matching is what tells you whether revenue was recorded correctly, whether settlement happened on time, and whether something needs investigation before it becomes a bigger problem.

The real problem is visibility

A surprising number of payment teams still run this control in a fragile way. Kani Payments reports that 56% of payments firms still rely on spreadsheets for reconciliation, and 47% of firms in its sample were experiencing issues related to the process in its discussion of payment reconciliation challenges and controls.

That matters because reconciliation is not cleanup. It is the control that supports financial accuracy, audit readiness, and regulatory compliance. If your business accepts online payments across more than one rail, the question is never just “what did we sell?” It's “what settled, what is pending, what reversed, and what doesn't line up?”

Practical rule: If you can't explain the gap between booked revenue and settled funds quickly, you don't have cash visibility. You have a reporting delay.

What a good control panel tells you

For a modern online business, payment reconciliation should answer a short list of operational questions every day:

- What has been paid: Which customer payments were authorized or completed.

- What settled: Which transactions turned into merchant-side funds.

- What changed after the sale: Refunds, reversals, chargebacks, and fee deductions.

- What still needs attention: Transactions that are missing, delayed, duplicated, or mismatched.

A clean reconciliation process changes how you run the company.

| Question | Weak process | Strong process |

|---|---|---|

| Can you trust today's cash position? | Not really | Yes, with context |

| Can finance explain settlement gaps? | Slowly | Quickly |

| Can support answer payout questions? | Case by case | From records |

| Can you audit the full payment path? | Painfully | Reliably |

The businesses that handle this well don't treat reconciliation as a monthly accounting task. They use it as a live financial control panel. That becomes even more important when customer payments come in through cards and crypto, but the business wants one predictable settlement layer on the back end.

Mapping Your Payment Flow to USDC Settlements

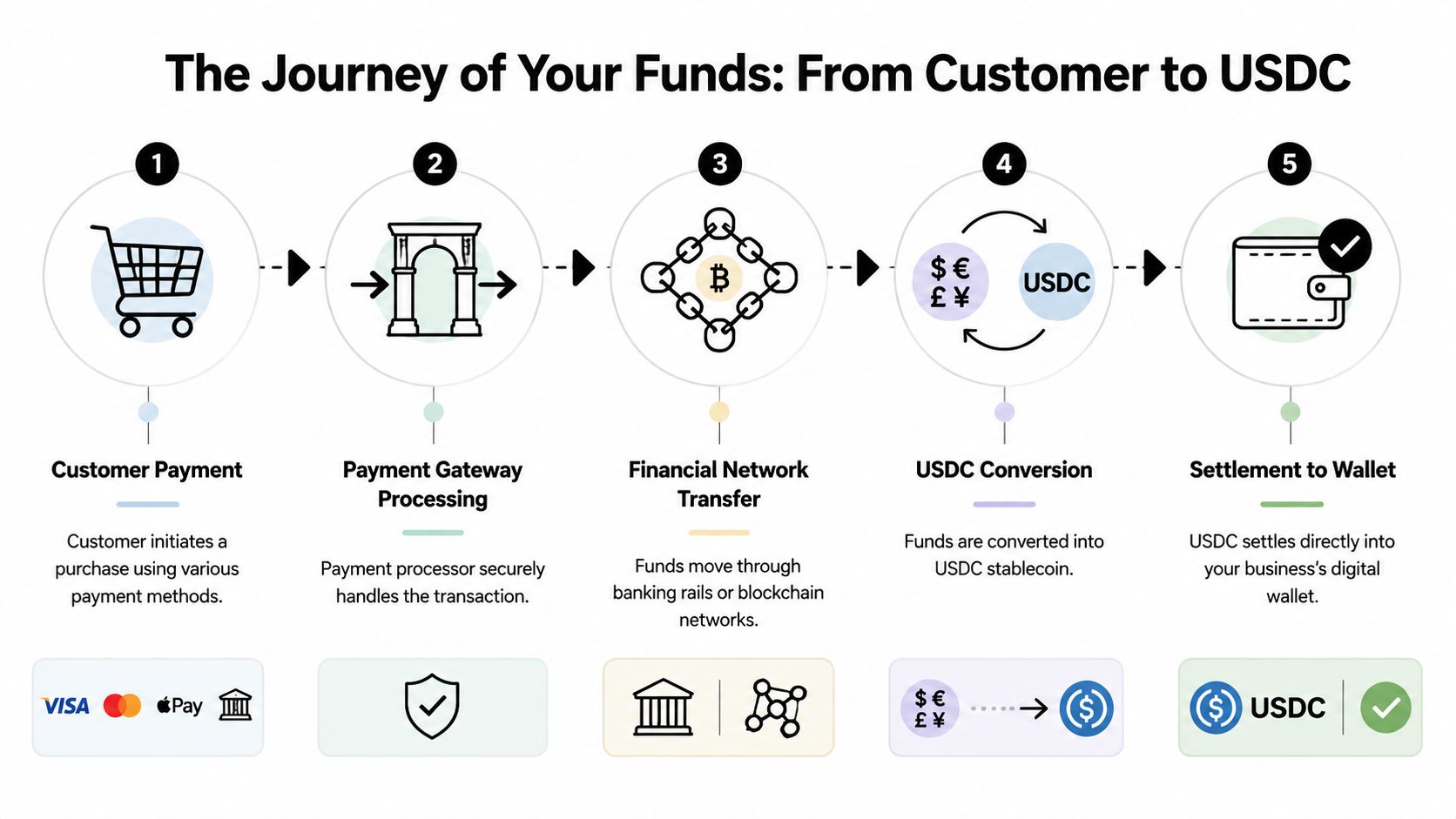

Traditional reconciliation often starts from the bank account and works backward. That's the wrong mental model for an internet business that wants settlement clarity. Start from the customer payment event, then trace each system record until it lands as USDC in your wallet.

Follow the records, not just the money

A typical multi-rail flow looks simple from the customer side. They pay with a card or a supported crypto asset. Behind the scenes, the payment stack creates several records that need to line up if you want reliable reconciliation.

Think about the lifecycle as a chain of evidence:

Customer action

An order, invoice, subscription renewal, or access payment is initiated.Payment confirmation record

Your checkout or application logs the payment event, usually with an internal order ID, customer ID, and amount.Processor or gateway record

The payment system returns its own transaction reference and status.Settlement record

Funds are grouped, netted, and prepared for merchant settlement.Wallet receipt

The final USDC transfer appears in your wallet history with its own transaction hash or equivalent settlement reference.

If you skip one of these records, reconciliation gets messy fast. You end up matching totals instead of transactions, and totals can hide problems for a long time.

Reconciliation works best when every payment event has one durable internal identifier that survives all the way through settlement.

The sources of truth that matter

For this model, you don't need dozens of files. You need the right ones, in the right order.

| Layer | What it proves | Typical record to keep |

|---|---|---|

| Internal sales system | The customer intended to pay | Order or invoice record |

| Checkout or payment layer | The payment was initiated or confirmed | Transaction event log |

| Settlement reporting | The platform prepared merchant funds | Settlement report |

| Wallet activity | USDC arrived at the destination | Wallet transaction history |

A USDC-centered settlement model becomes easier to reason about than a traditional bank-based payout setup. Instead of tracking multiple payout currencies, FX conversions, and delayed bank deposits across regions, you can design your reconciliation around one merchant settlement asset.

That doesn't remove complexity entirely. Fees may post on one schedule, refunds on another, and settlement can still batch multiple customer payments together. But your target state is clearer: every valid payment should be traceable to a final USDC outcome.

For online businesses, that clean endpoint changes the accounting conversation. You're no longer asking which local bank account received which payout. You're asking whether the payment event and the wallet settlement record agree, and if not, whether the difference is timing, fees, or an exception that needs action.

A Practical Guide to Matching and Investigating

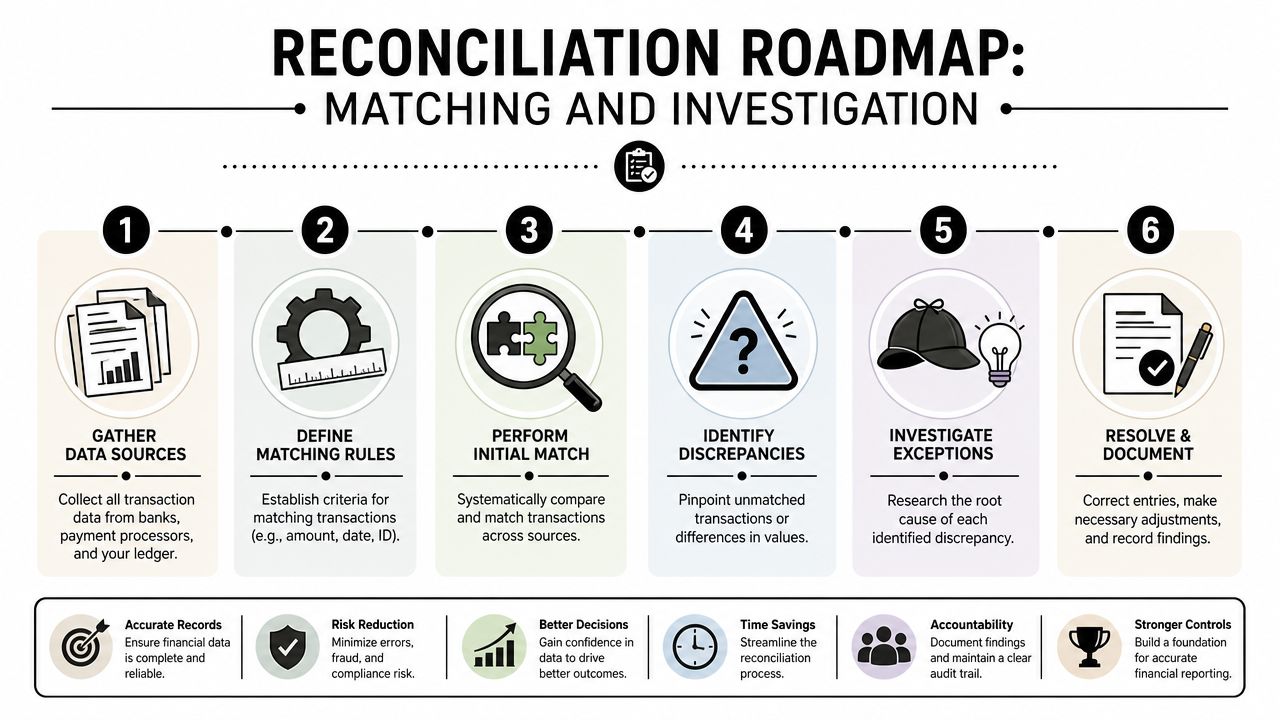

Once your payment flow is mapped, the work becomes mechanical. Good payment reconciliation is a repeatable routine, not a heroic effort at month-end.

Paystand notes that finance teams often reconcile on a daily, weekly, or monthly basis and recommends automation to reduce human error and speed matching in its guide to payment reconciliation workflows. For internet businesses with steady transaction volume, waiting too long creates backlog and blurs context.

Start with a repeatable matching key

The best match key is usually your own. An internal order ID, invoice ID, or subscription event ID should appear as early as possible in the payment flow and stay attached to downstream records.

A practical daily workflow looks like this:

Pull your internal sales records

Export or query the orders, invoices, renewals, or access charges created during the reconciliation window.Pull your payment and settlement records

Collect the processor-side transaction list and the merchant settlement output.Pull wallet activity

Confirm the incoming USDC settlement records for the same period. If you need a clean reference point for this step, a dedicated view of transaction history and payout records makes investigations much easier.Match in layers

First match internal records to payment confirmations. Then match payment confirmations to settlement records. Finally match settlement records to wallet receipts.Flag exceptions, don't bury them

Unmatched records should go into an exception queue with status, owner, and next action.

A lot of teams make one avoidable mistake here. They try to reconcile net deposits first because that feels closer to cash. That often hides fee deductions, partial refunds, and timing issues. Match gross transaction logic first. Then explain the net result.

How to work exceptions without drowning in them

Not every break is a real loss. Many are timing differences. But you still need a disciplined process to prove that.

Common exception types include:

- Timing differences: A payment is confirmed, but settlement lands later.

- Bundled settlements: One wallet settlement represents many customer payments.

- Refunds or reversals: The original sale matched, but the later reversal changes the net position.

- Fee differences: The transaction is real, but the net amount doesn't match expectation.

- Missing references: The money moved, but the record chain is incomplete.

Here's a simple investigation grid:

| Exception type | First question | Typical resolution |

|---|---|---|

| Payment missing from settlement | Is it still within expected timing? | Hold open, review next cycle |

| Settlement without clear source payments | Is this a batch payout? | Expand settlement to child transactions |

| Net amount lower than expected | Were fees or refunds applied? | Record fee or refund detail |

| Wallet receipt missing | Was payout actually sent yet? | Check settlement status and retry logic |

| Duplicate record | Is this a replay or true duplicate? | Void duplicate entry, document reason |

When you document these steps well, your ledger stays clean. If you want a broader accounting lens on documenting adjustments and approvals, CEF ledger reconciliation best practices is a useful companion resource.

The strongest reconciliation teams spend less time matching clean transactions and more time shortening exception resolution.

Automating Reconciliation with Webhooks and APIs

Manual reconciliation breaks first in the handoff points. Someone exports a CSV late. A refund posts after the weekly check. A payout arrives, but nobody updates the ledger until tomorrow. The records are all there, but they arrive at different times and in different formats.

That is why the hardest modern problem is timing, not arithmetic. Industry commentary on payment reconciliation bottlenecks points to fragmented data and manual review as core issues, with automation needed to answer not only whether records balance, but when they should balance.

What automation changes in practice

A useful automation setup does three jobs at once:

- Collects events automatically from the payment layer instead of relying on manual exports

- Applies matching rules continuously as new records arrive

- Routes exceptions early so your team only touches the transactions that need judgment

That's where APIs and webhooks help. An API lets your system request transaction and settlement data on demand. A webhook pushes a notification the moment something happens, such as a payment confirmation, subscription event, refund, or payout update.

For a business that accepts cards and crypto but wants a single merchant settlement asset, this architecture is a much better fit than spreadsheet-based reconciliation. You can ingest events as they occur, update internal records immediately, and build a ledger that reflects real operational state instead of last week's exports.

One option in this category is Suby, which provides an API that allows businesses to accept payments by card or crypto, with merchants receiving USDC, and also offers native Discord and Telegram integrations for paid access, subscriptions, and online communities. If you're evaluating implementation detail, this overview of payment gateway API integration is a practical starting point.

Where webhooks fit

Webhooks are especially valuable when reconciliation needs to stay aligned with user access or service delivery.

Consider a subscription business with a private community. A customer pays, access is granted, a renewal fails later, access changes, and eventually a refund may be issued. If finance is reconciling from delayed exports while operations are managing access in real time, the business creates two different truths. Webhooks close that gap by feeding the same payment events into both systems.

A simple webhook-driven flow usually looks like this:

- Payment event arrives.

- Internal system updates order or subscription status.

- Reconciliation engine attempts an automatic match.

- Unmatched events move into review.

- Later settlement event closes the loop against wallet receipt.

Here's a short product walkthrough that helps make this model more concrete:

Automation does not remove the need for controls. It changes where people spend time. Instead of copying rows between files, your team reviews the outliers, verifies rule logic, and keeps the exception queue honest.

Testing and Monitoring Your Reconciliation System

A reconciliation setup is only trustworthy if you can break it on purpose and still understand what happened. That's why testing matters as much as automation.

Test the full path

Run a small set of controlled transactions through your full flow. Include more than one scenario. A straightforward payment is the baseline, but it isn't enough on its own.

Test cases worth running include:

- A standard successful payment: Confirm the order record, payment record, settlement record, and wallet receipt all connect.

- A delayed settlement scenario: Verify your system marks it as timing-related instead of unresolved loss.

- A refund case: Make sure the original payment and later reversal tie back to the same commercial event.

- A failed or incomplete path: Confirm that alerts fire and that the transaction lands in an exception queue.

Document what “good” looks like for each test. If a record is expected to remain open temporarily, say so clearly. That prevents teams from chasing normal timing differences as if they were incidents.

Checkpoint: If an operator can't tell the difference between a normal pending item and a real discrepancy, the system needs clearer status logic.

Monitor the exceptions, not just the totals

Most businesses watch total revenue and total settled funds. That's useful, but it won't tell you where the process is weakening.

A better monitoring routine tracks operational signals such as:

- Age of open exceptions: Old breaks usually point to ownership or data quality issues.

- Reason codes by type: Timing issue, refund, duplicate, missing reference, fee mismatch.

- Manual touchpoints: Which transactions still require spreadsheet work or ad hoc review.

- Rule failures after changes: Any increase after a product update, provider change, or new payment path.

For ongoing visibility, a dedicated view of real-time transaction monitoring helps teams catch drift before it turns into a month-end cleanup project.

A good monitoring habit is simple. Review open exceptions on a fixed cadence, tune your matching rules when patterns repeat, and keep an audit trail for every adjustment. Reconciliation systems fail unnoticed when nobody owns the queue.

Conclusion Gaining Clarity in a Complex World

Payment reconciliation matters because online payment flows are no longer linear. A customer pays with one method, a platform processes the transaction, fees and refunds follow their own timelines, and the business still needs one clean answer to the question, “What settled?”

For internet-native companies, a USDC-centered model is easier to control than a patchwork of bank payouts, currency conversions, and delayed settlement reports. The key is building reconciliation around the full chain of records, not around one end-of-month deposit.

That means using durable identifiers, matching transactions in layers, and treating exceptions as an operating workflow instead of an afterthought. It also means moving away from spreadsheet habits that can't keep up with multi-rail payments.

APIs and webhooks are the practical upgrade. They let systems collect payment events as they happen, push changes into your internal records, and keep finance, support, and operations aligned around the same source of truth. When customer payments come in through cards or crypto and merchant settlements land in USDC, that automation gives you a cleaner ledger and fewer surprises.

The payoff is straightforward. You spend less time asking where money went, and more time using accurate cash data to run the business.

If your business wants a simpler way to accept card and crypto payments while receiving USDC, Suby is built for that model. Users pay with cards, businesses receive USDC, and teams can connect payments to subscriptions, paid access, and online communities through API, Discord, and Telegram integrations.