You log in, see a dispute notification, and your first reaction is usually the wrong one. Most merchants look at the lost sale. However, the problem is more substantial. You lose the revenue, pay a fee, pull someone into evidence gathering, and take another step toward processor scrutiny if the pattern continues.

That’s why the phrase avoid dispute payment matters more than commonly understood. A dispute isn’t just a payment event. It’s an operations problem, a support problem, and for cross-border businesses, often a settlement problem too. If customers pay in one currency, you settle in another, and your billing trail is messy, confusion turns into disputes fast.

The operators who keep dispute rates under control usually do the same few things well. They make the charge recognizable. They communicate before a customer gets surprised. They tighten fraud checks without wrecking conversion. They make refunds easier than chargebacks. And when they sell globally, they simplify how money moves after checkout so there’s less room for FX confusion, payout delays, and reconciliation mistakes.

Table of Contents

- Make the checkout impossible to misunderstand

- Treat subscription communication as risk control

- Give customers a path back to you before they go to the bank

The True Cost of a Payment Dispute

The dispute email lands at the worst time. Your support inbox is already full, finance is reconciling payouts, and now someone has to pull order history, receipts, delivery logs, renewal notices, and customer messages just to decide whether this case is worth fighting.

The direct cost is painful enough. Globally, chargeback volume was projected to reach $117 billion by the end of 2023, each dispute costs merchants at least a $15 fee on top of lost revenue, and going over network thresholds such as Visa’s 0.9% dispute rate can put your processing account at risk, according to chargeback statistics compiled by Chargeback.io.

What merchants usually miss

A dispute rarely stays contained to one order. It drags in support, finance, and whoever owns billing. If the reason code points to fraud, your fraud rules get questioned. If it points to “service not received,” your fulfillment and messaging get examined. If it says “unrecognized charge,” your descriptor, receipt flow, and renewal reminders all go under the microscope.

For global businesses, there’s another layer. Customers may buy from one country, see a statement line they don’t recognize, compare it against a settlement amount that looks different because of currency effects, and decide the bank is the fastest place to complain. That’s where a lot of preventable disputes start.

Practical rule: If your first response to disputes is “fight harder,” you’re already late. The cheaper fix is usually earlier clarity.

Why this gets worse as you scale

At low volume, teams can survive on manual clean-up. Someone knows the customer, remembers the order, and can patch the issue with a quick refund or a support reply. At scale, that breaks. You need recognizable billing, clean logs, a simple refund path, and predictable settlement.

That’s one reason payment architecture matters. A system that lets customers pay with familiar methods while the business receives USDC can remove a lot of downstream friction in global operations. When settlement is predictable, finance has fewer reconciliation errors, support has fewer payout-related explanations to send, and dispute review is less cluttered by avoidable confusion.

Understanding Why Customers Dispute Payments

Most disputes come from a small set of recurring failures. If you don’t separate them clearly, you end up applying the wrong fix. A stolen card problem needs controls. A confused subscriber needs communication. A delivery problem needs service recovery.

Friendly fraud is the category many teams underestimate. In North America, about 60% of 2023 chargebacks were friendly fraud, and 75% of shoppers who file a dispute bypass the merchant and go straight to their bank, according to Chargeflow’s chargeback trends summary. That tells you two things. First, a lot of disputes are not classic criminal fraud. Second, customers often don’t even try to resolve the issue with you first.

The three causes that matter

True fraud

This is the cleanest category conceptually. Someone used a stolen card or unauthorized payment details. You’ll often see mismatched order signals, rushed checkout behavior, or delivery patterns that don’t fit the customer profile.

The mistake merchants make is treating every fraud dispute as winnable. It usually isn’t. The true work is preventing it before authorization, not building heroic evidence after the fact.

Friendly fraud

This is messier. The customer did make the purchase, but later disputes it. Sometimes they forgot the brand name on the statement. Sometimes they regret the purchase. Sometimes a family member bought it. Sometimes they panic at an auto-renewal and go directly to the bank because it feels easier than finding your support page.

This category is why “avoid dispute payment” isn’t just about security. It’s about memory cues, receipts, renewal reminders, and a billing experience that feels transparent enough that the customer doesn’t reach for the bank first.

Most avoidable disputes start as a customer confusion problem long before they become a bank process problem.

Merchant error

This is the category you own outright. Wrong item, missing fulfillment, unclear terms, duplicate billing, poor cancellation flow, or support that answers too slowly. These disputes are preventable, but only if you admit they’re process failures rather than “bad customers.”

Common dispute triggers and their causes

| Dispute Reason Code | What the Customer Claims | Common Business Cause |

|---|---|---|

| Fraud or unauthorized | “I didn’t make this purchase” | Weak screening, stolen card use, insufficient verification |

| Unrecognized transaction | “I don’t know this merchant” | Poor billing descriptor, weak receipt branding, confusing company name |

| Product not received | “My order never arrived” | Shipping issue, weak tracking communication, digital delivery not documented |

| Service not provided | “I didn’t get what I paid for” | Access not provisioned, onboarding failure, unclear fulfillment steps |

| Recurring billing complaint | “I didn’t agree to this renewal” | Weak renewal notice, hidden subscription terms, cancellation friction |

| Not as described | “This wasn’t what was promised” | Misleading product page, expectation gap, support delay |

The fix starts by tagging every dispute to one of these buckets and then reviewing real examples. If your top cause is unrecognized charges, don’t spend the quarter only tuning fraud filters. If your top cause is renewals, don’t blame customers for not reading fine print. Clean up the recurring billing experience.

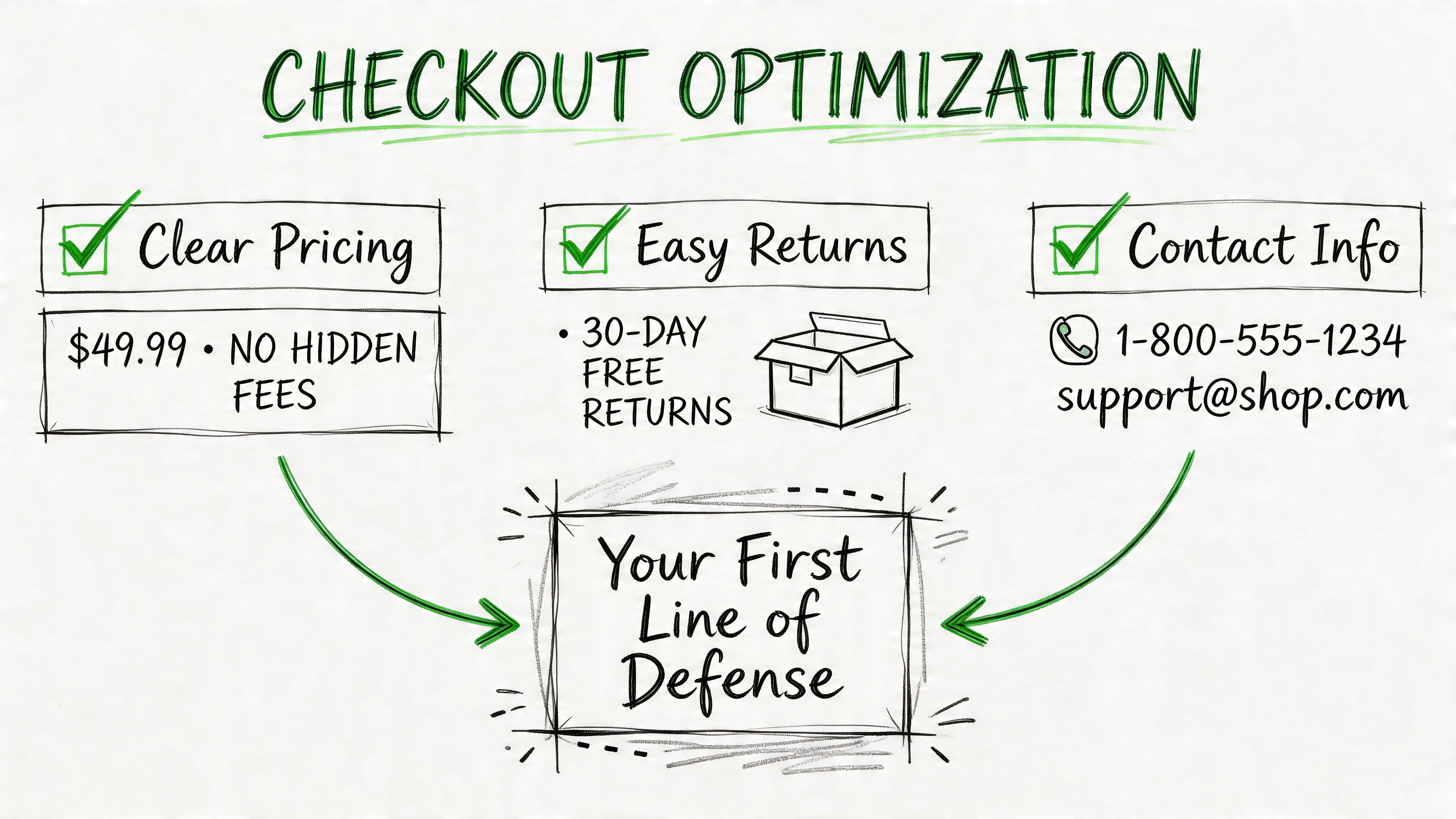

Your First Line of Defense Proactive Prevention

A large share of disputes is decided before the charge is ever submitted. The work here is operational. Remove surprise, make the merchant recognizable, and give the customer an obvious path to fix a problem without calling the bank.

Make the checkout impossible to misunderstand

Customers file disputes for two simple reasons. They did not expect the charge, or they do not recognize it later.

A checkout that prevents both is usually boring in the best way. It answers the practical questions before payment is approved:

- Show the full price upfront. Include taxes, shipping, fees, renewal timing, and what happens after a trial.

- Explain fulfillment clearly. If delivery is instant, manual, scheduled, or tied to onboarding, state that before the buyer pays.

- Place support access near the payment action. A visible email address, chat entry point, or help link catches issues early.

- Keep the merchant identity consistent. The brand on the checkout, receipt, confirmation email, and card statement should match closely enough that no customer has to guess.

The billing descriptor deserves extra attention. It is one of the cheapest fixes available, and it often gets ignored until dispute volume rises. Use a descriptor that matches the brand customers saw during checkout. If the legal entity differs from the storefront name, add the recognizable brand and support contact where the issuer allows it.

Treat subscription communication as risk control

Subscription disputes usually come from weak communication, not complicated fraud. A valid charge can still turn into a chargeback if the customer forgets the renewal, misses the cancellation path, or cannot connect the statement line to the service they bought.

The operators who keep this under control do the repetitive work every month:

- Send a confirmation immediately after purchase. Include the plan name, amount charged, renewal date, and cancellation steps.

- Send renewal reminders before billing. Keep the subject line and sender name recognizable.

- Confirm cancellations in writing. Remove ambiguity. Customers should know the subscription is off.

- Review support-risk accounts before renewal. If a customer reported failed login, missing access, or account confusion, do not let the next charge hit without context.

Teams that want a stronger view of upstream risk should also review fraud signals alongside dispute signals. Suby’s guide to payment fraud patterns and prevention is useful for that, because the same checkout weaknesses often create both problems.

Give customers a path back to you before they go to the bank

If support is hard to find, the issuer becomes your customer service department. That is expensive.

Receipts should link to help. Account pages should show billing history and active plans. Renewal emails should explain cancellation in plain language. Refund rules should be easy to read before and after purchase.

I have seen merchants spend heavily on fraud tooling while keeping a vague receipt template and a buried cancellation page. They still lose preventable disputes because the customer cannot answer a basic question fast enough: what was this charge, and who do I contact?

For global sellers, payment architecture also affects prevention. A hybrid card-and-crypto model can reduce operational mess if it is set up well. When card acceptance, subscription logic, and settlement are handled in one system, finance and support teams are working from the same record instead of reconciling separate processors, wallets, and internal spreadsheets.

That is where guaranteed USDC settlement is useful. The customer still pays with familiar rails when needed, but the business settles revenue in a stable digital asset with cleaner treasury handling across borders. Fewer handoffs means fewer billing mismatches, fewer reconciliation errors, and faster answers when a customer questions a charge.

Suby is one example of that model. It supports card and crypto payments through one API and settles revenue in USDC, with native Discord and Telegram integrations for subscriptions, paid access, and community monetization. Operational clarity reduces preventable disputes, especially for cross-border businesses that need support, billing, and settlement records to line up.

On the back office side, good records still matter. Teams handling invoices, KYC files, support logs, fulfillment proofs, and cancellation confirmations can use intelligent document processing to keep evidence organized and searchable before a dispute ever needs a response.

Technical Fortifications for Your Payment System

Good communication prevents confusion. Technical controls prevent a different class of problems. You still need both. If your backend accepts avoidable fraud, your support team will spend weeks arguing over charges that should never have gone through.

Use the basic controls properly

Three controls matter in almost every card setup.

AVS checks whether the billing address matches the issuer’s records. It won’t solve every fraud case, but it helps catch obvious mismatch patterns.

CVV verifies that the payer has the physical card details, not just a number pulled from a breach or a bad list.

3D Secure adds another layer of authentication. It can increase friction in some cases, but for higher-risk transactions it gives you a much stronger basis for screening and recordkeeping.

What doesn’t work is switching these on blindly and never reviewing results. Teams often create false declines, hurt conversion, and still miss the fraud patterns that matter because nobody looks at exceptions by product, region, or customer segment.

For businesses dealing with invoices, KYC files, support records, and fulfillment proofs during dispute review, strong internal documentation matters too. That’s why tools and workflows around intelligent document processing can be useful. Clean, searchable records make it easier to trace what happened when a transaction, subscription change, or access grant gets questioned later.

Why USDC settlement changes the dispute picture

Most legacy advice treats disputes as a pure card problem. That’s incomplete for international businesses. A lot of operational friction comes after the payment, when merchants reconcile currencies, wait on bank timelines, and explain FX differences to customers or finance teams.

That’s where hybrid models matter. According to the verified data provided for this article, hybrid card-crypto gateways like Suby can reduce effective disputes by up to 40% by using native USDC rails, which helps avoid FX disputes entirely, as described in the referenced Square dispute prevention page. The practical point is straightforward. Customers can still pay with familiar methods, while the business receives USDC with more predictable settlement.

This setup doesn’t remove the need for card controls. It removes a layer of cross-border mess that often sits around the payment and makes disputes harder to interpret.

If you’re evaluating payment security architecture, it also helps to understand what PCI compliance covers in the stack. Suby’s overview of PCI-DSS compliance and why it matters is a useful technical reference when you’re deciding what your team should own directly and what your payment provider should handle.

Building a Smart Response and Refund Workflow

A lot of disputes are still recoverable before they become chargebacks. The window is small, but it exists. If a customer is upset, confused, or worried about a renewal, you want them talking to support, not opening a banking app.

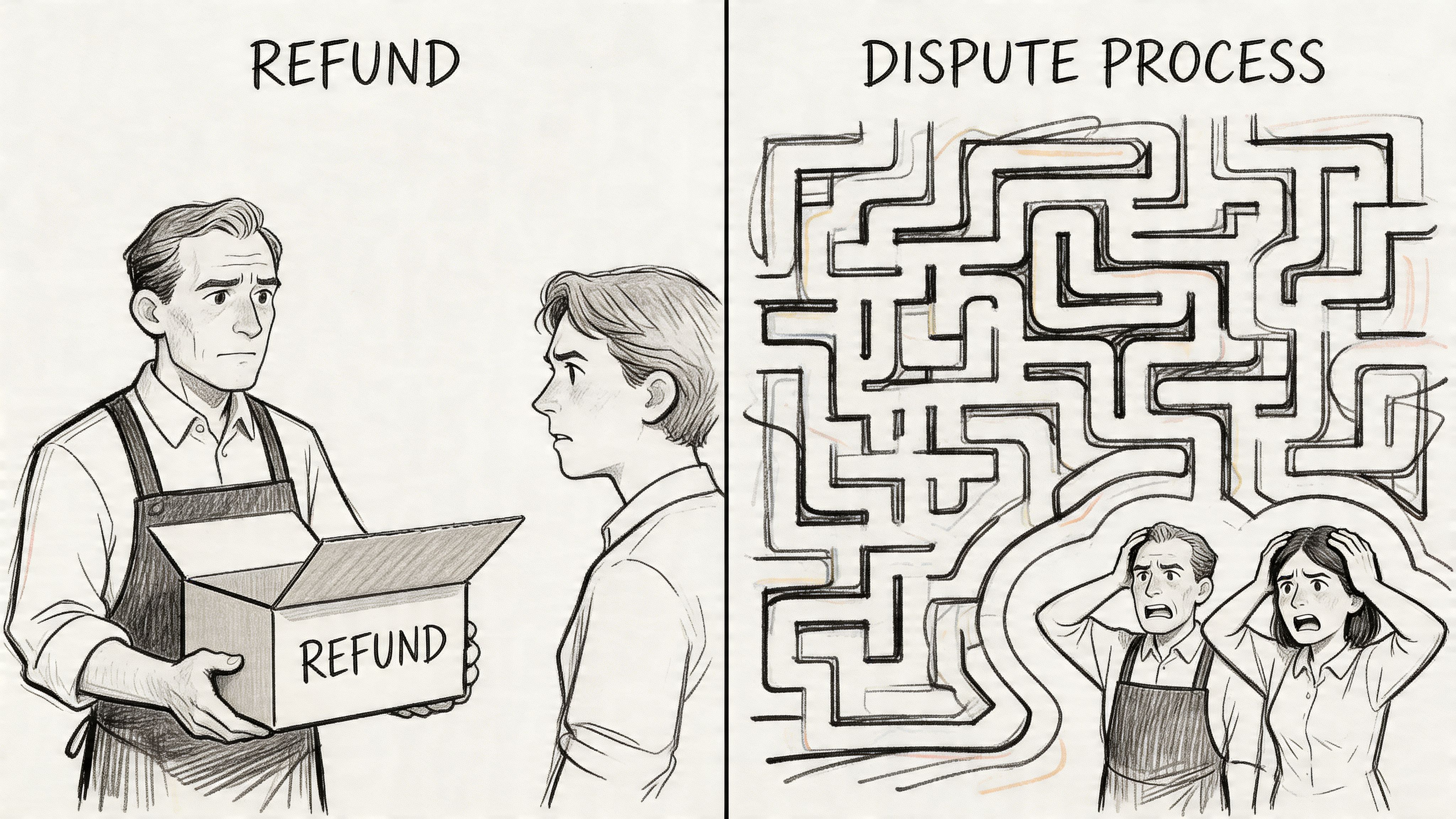

Refund speed beats representment theatre

Merchants often overestimate the value of fighting. They treat representment like revenue recovery when it’s usually cost control at best. If the customer is likely to win, or if the evidence is messy, the cheapest move is often to refund early and close the issue cleanly.

The logic is simple. A refund costs the sale. A chargeback can cost the sale, a fee, internal labor, and more account-level risk. For recurring businesses, this gets even sharper when cross-border billing is involved. The verified data for this article states that FX confusion and renewal surprises drive 35% of disputes in multi-currency subscription setups, and using a real-time dashboard with proactive alerts can reduce these disputes by 50%, as noted in the referenced Stripe resource on chargeback types.

Operator mindset: Refunding the right unhappy customer quickly is not weakness. It’s dispute prevention.

Set up the workflow before the complaint arrives

A workable response system has to be boring and fast. If agents need manager approval, engineering help, and finance intervention just to issue a small refund, customers will escalate before you act.

A practical workflow looks like this:

- Route billing complaints first. These should skip generic queues and land with whoever can verify orders and issue refunds fast.

- Define refund authority. Support should know exactly when they can resolve a case without waiting.

- Watch event triggers. Failed renewals, access complaints, duplicate orders, and unusual cancellation spikes should produce alerts.

- Keep account history in one place. The agent handling the complaint should see payment date, plan, invoices, support messages, and access status together.

For teams that need to tighten the human side of escalation handling, this guide on handling an upset customer is a useful operational read because tone and speed often decide whether someone asks for a refund or files a dispute.

If you run subscriptions, your dunning process is part of dispute control too. Weak retry messaging and unclear failed-payment handling create confusion that later looks like unauthorized billing. Suby’s article on what a dunning process should cover is relevant here because recovery flows and dispute prevention overlap more than most billing teams think.

A good dashboard helps, but the policy matters more. Customers should know how to reach you, agents should know when to refund, and finance should prefer a controlled refund over a messy chargeback.

Conclusion From Defense to a Smarter Payment Stack

Merchants that consistently avoid dispute payment problems don’t rely on one trick. They combine clear checkout language, recognizable billing, strong renewal messaging, solid fraud controls, and an easy path to refund before a complaint hardens into a chargeback.

That matters because fighting is never the whole answer. The verified data for this article notes that even elite representment strategies only win 60% to 75% of fought disputes, while prevention can eliminate 40% to 70% before they happen, according to the referenced Xcaliber guide to merchant dispute win rates. In other words, the upside is usually upstream.

For global businesses, the payment stack itself also shapes dispute risk. If customers can pay with cards or crypto, while the business receives USDC in a predictable way, operations get simpler. Reconciliation gets cleaner. Cross-border friction falls. Support has fewer settlement mysteries to untangle. That doesn’t eliminate disputes, but it removes some of the confusion that feeds them.

The practical takeaway is straightforward. Don’t build a dispute program around evidence packs alone. Build it around recognition, communication, refunds, and cleaner settlement.

If you want a payment setup built for that model, Suby provides an API that lets businesses accept card and crypto payments while receiving USDC, plus native Discord and Telegram integrations for subscriptions, paid access, and online communities.