Gaspard LEZIN

Fraud Payment Explained: A Merchant's Guide to Prevention

Learn to identify and stop fraud payment attempts. This guide covers common fraud types, detection signals, and prevention strategies for your online business.

Authorized Push Payment fraud isn't a niche banking problem anymore. Deloitte projects that US APP fraud losses could rise from $8.3 billion in 2024 to $14.9 billion by 2028 in a baseline scenario, with a higher scenario reaching $18.2 billion by 2028 (Deloitte Insights). That number should reset how any online merchant thinks about fraud payment.

A fraud payment is any transaction pushed through by deception, stolen credentials, account abuse, or manipulation of a person or system. Sometimes it's an obviously unauthorized purchase. Sometimes it's a customer who received the product and still disputes the charge. Sometimes it's a payment that looks clean at checkout and only turns toxic after fulfillment.

For a business owner, the damage isn't limited to the lost order value. Teams lose inventory, time, ad spend, support capacity, and trust. Good customers feel the friction from your controls, while bad actors test where your controls are weak. The real work is finding the line between protecting margin and protecting conversion.

Table of Contents

Why this hurts more than the order amount

The pressure on smaller teams

Where merchants usually get caught

How the attack pattern changes by payment rail

Transaction anomalies

User behavior and identity clues

How to connect weak signals into a decision

What each tool is good at stopping

Why layered controls beat one big rule engine

Build a review queue before you need one

Know when to fight and when to write it off

Why hybrid checkouts create blind spots

What a unified control model looks like

The merchant checklist

The Growing Threat of Fraudulent Payments

The headline risk isn't only card fraud anymore. The sharper problem is that fraud now moves across channels, and it often exploits speed. Deloitte's projection that APP fraud losses in the United States could increase from $8.3 billion in 2024 to $14.9 billion by 2028 shows how quickly social engineering and real-time payment manipulation are scaling (Deloitte Insights).

That matters because fraud payment rarely arrives wearing a sign that says "stolen." It often looks like a customer making a normal purchase, a finance employee paying an invoice, or a returning buyer using a familiar method. The difference is intent. Someone is abusing a process, a credential, an identity, or a trust signal to move money where it shouldn't go.

Why this hurts more than the order amount

Most new merchants focus on the visible loss first. That's natural, but incomplete. A bad payment can trigger a whole chain of avoidable costs:

Fulfillment loss: You ship goods, grant access, or deliver services before the issue is discovered.

Support drag: Your team spends time reviewing screenshots, shipping logs, account activity, and dispute evidence.

Policy distortion: After a fraud spike, many merchants overreact and tighten rules so much that good customers get blocked.

Trust damage: Legitimate buyers who get declined or delayed too often don't come back.

Practical rule: Fraud controls should reduce bad revenue, not good revenue. If your system catches fraud but scares off real buyers, it still failed.

The pressure on smaller teams

Large merchants can afford dedicated fraud analysts. Most growing businesses can't. They rely on a patchwork of gateway defaults, manual reviews, and support instincts. That setup works until volume grows, payment methods expand, or fraudsters notice an opening.

The challenge gets harder when you sell globally, accept multiple payment methods, or mix digital delivery with subscriptions and invoices. Different rails produce different failure modes. A card dispute behaves differently from a bank push payment scam, and both behave differently from abuse in a crypto-linked checkout flow.

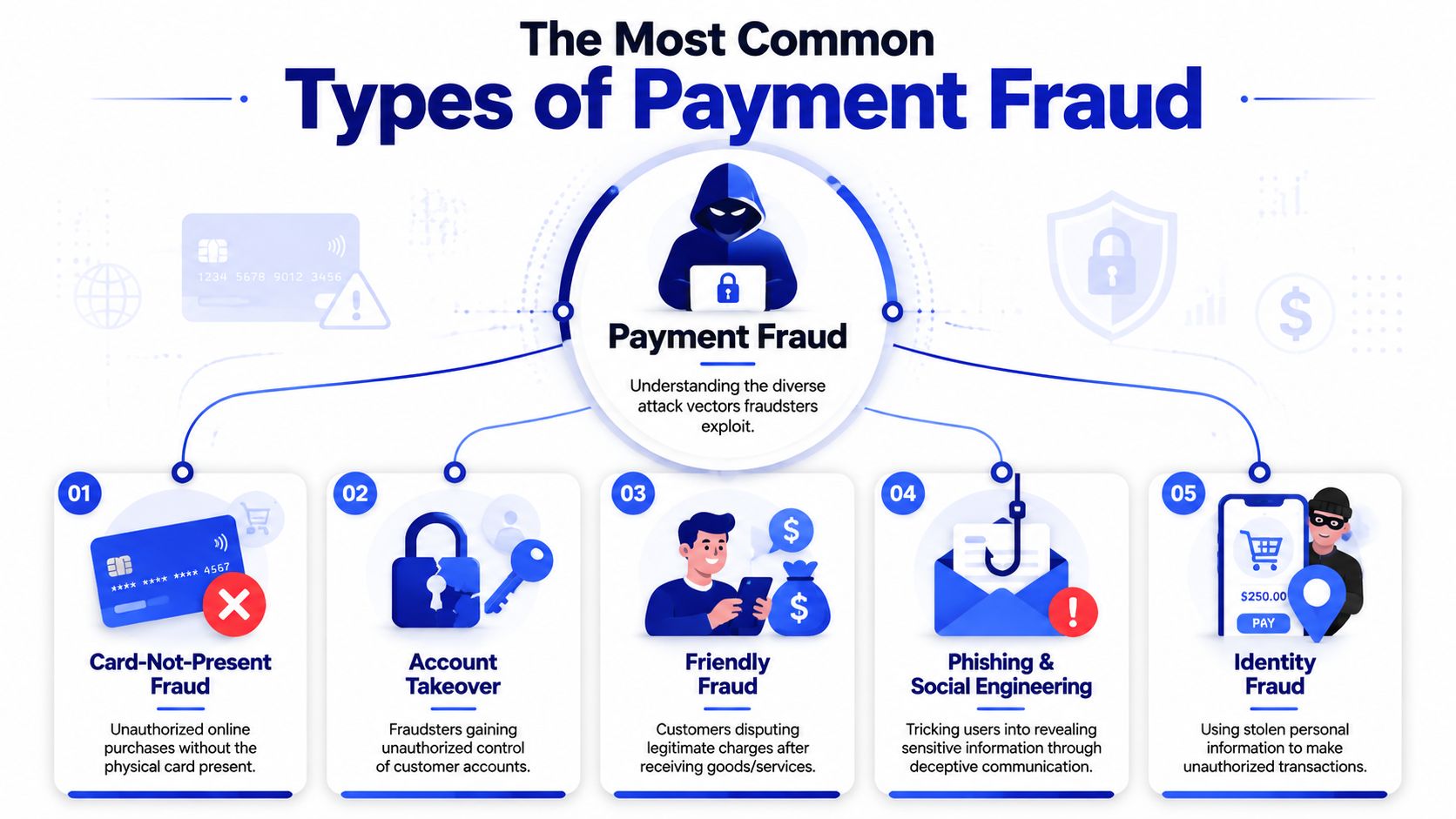

The Most Common Types of Payment Fraud

Fraud isn't one problem. It's a stack of attack patterns, each exploiting a different weakness in your checkout, account system, support flow, or payout process.

Where merchants usually get caught

Card-not-present fraud is the classic online retail problem. The fraudster doesn't need the physical card, only enough stolen data to pass checkout. For merchants, it feels like someone using a stolen wallet in a store where the cashier can't see their face.

Account takeover starts earlier in the funnel. A criminal gets into a real customer's account, changes details, uses saved payment methods, redeems credits, or places orders that look believable because the account history is real. These attacks are dangerous because they inherit trust from the victim's prior behavior.

Friendly fraud is less technical and often more irritating. A real customer buys something, receives it, then disputes the charge anyway. Sometimes it's confusion. Sometimes it's buyer's remorse. Sometimes it's deliberate chargeback abuse. Digital goods, subscriptions, coaching, and creator products deal with this constantly because delivery is real but harder to "see" than a shipped parcel.

Phishing and invoice deception hit teams as much as customers. A fraudster imitates your brand, your vendor, or your finance contact and tricks someone into authorizing a payment or changing banking details. That's why fraud payment prevention isn't just a checkout topic. It's an operations topic.

Synthetic identity abuse sits in between fake and real. The attacker builds an identity using mixed information, enough to look plausible across forms and checks. Merchants often miss this because each individual data point looks ordinary, but the bundle doesn't hold together under closer review.

The safest-looking order can still be the worst order if the fraudster borrowed a real account and behaves patiently.

How the attack pattern changes by payment rail

Merchants still underestimate how much older payment methods remain exposed. Checks remain the payment method most frequently impacted by fraud globally, and 58% of organizations reported experiencing check fraud in 2025 according to the AFP survey (AFP Payments Fraud and Control Survey). That's a useful reminder that fraud follows weak controls, not fashion.

Hybrid businesses have an extra problem. They may accept cards, wallets, bank transfers, invoiced payments, and crypto in the same commercial flow. Fraudsters don't care which department owns each method. They test the easiest seam. A checkout may be well protected, while manual invoice approval is loose. Or a bank payout change process may be weaker than card screening.

A practical way to study this is to review real breach reporting, not just merchant advice. InsecureWeb's Quickpay1688 breach analysis is worth reading because it shows how exposed payment information can become part of later fraud attempts, even when the eventual attack happens far away from the original breach.

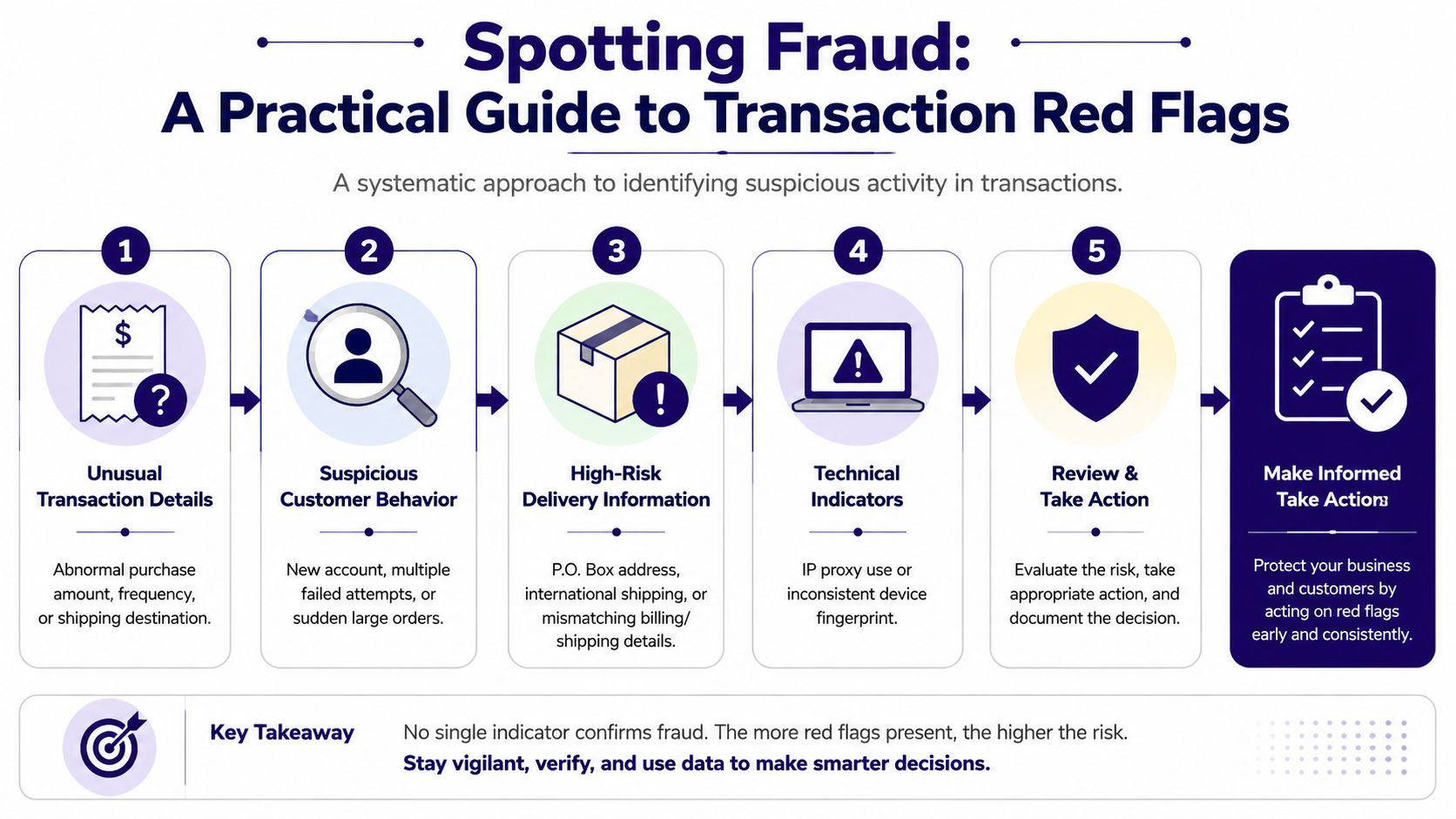

How to Spot a Fraudulent Transaction

Most fraudulent transactions don't look outrageous on their own. They look slightly off. The skill is learning which signals matter, which ones can be ignored, and which combinations justify holding an order.

A useful mental model is to stop looking for a single smoking gun. Strong fraud teams combine small signals into a decision. That's how payment fraud intelligence systems work. They correlate multiple data points, and industry benchmarks show that using precise data such as phone numbers and physical addresses can drive true positive detection rates to over 90%, with phone number matches at 95.21% accuracy (Recorded Future payment fraud intelligence).

Start with this visual checklist.

Transaction anomalies

Some orders are suspicious because of what was purchased and how fast it happened.

Unusual order size: A first-time customer buying your highest-value package is not automatically fraudulent, but it deserves scrutiny.

Rapid retries: Multiple failed payment attempts followed by one success often mean someone is testing stolen credentials or cycling through cards.

Rush behavior: Fraudsters like urgency. Fast shipping, instant delivery, last-minute account changes, and pressure on support are common tells.

Mismatch between product and buyer profile: A new account with no prior activity suddenly purchasing bulk access, giftable goods, or easily resold items should go to review.

User behavior and identity clues

The next layer is behavior around the transaction. At this stage, new merchants often trust their gut too much and their logs too little.

A normal customer usually behaves consistently. They browse, compare, maybe fail once, then complete checkout. A bad actor often jumps straight to the valuable action, avoids profile completion, and gives minimal verifiable context.

Useful red flags include:

Disposable or low-trust contact details

Billing and shipping details that don't make sense together

Name, email, and phone combinations that feel assembled rather than lived-in

Support messages that push for manual approval instead of normal verification

Repeated use of "clean" looking but barely established accounts

If you're building your review flow, Suby's guide to payment fraud detection is a practical reference for how merchants can think about these patterns in a live payment environment.

A short explainer helps frame the logic behind these checks.

How to connect weak signals into a decision

Single-point rules create noise. Combined signals create confidence. A new customer with a large order isn't enough. A new customer with a large order, mismatched address details, unusual retry behavior, and account changes right after payment is another story.

A simple review table keeps teams consistent:

Signal type | Low concern | Higher concern |

|---|---|---|

Order pattern | Normal basket, normal timing | High-value first order, repeated retries |

Identity quality | Stable contact details | Inconsistent name, phone, address bundle |

Account behavior | Normal browsing and checkout | Fast path to purchase, post-payment changes |

Delivery risk | Expected destination | Hard-to-verify delivery or access request |

Review the pattern, not the event. Fraud payment is usually a cluster of small contradictions.

Your Toolkit for Fraud Payment Prevention

Fraud prevention works best as a layered system. Merchants get into trouble when they expect one control to do everything. Address checks won't stop account takeover. Two-factor authentication won't solve friendly fraud. Manual review won't scale if your checkout starts seeing volume across regions and payment methods.

What each tool is good at stopping

Real-time risk scoring is one of the most useful controls because it works during the transaction, not after it. It evaluates risk using live signals such as SIM swap detection, and this approach can push true positive detection rates to over 90% by identifying risky patterns before the transaction completes (Vonage on risk scoring in payments).

Strong Customer Authentication and 2FA are best for reducing abuse around identity and account access. They add friction, but it's productive friction when someone tries to log in from a new environment, change payout details, or trigger a sensitive action.

Manual review queues are best reserved for edge cases. Use people where judgment matters. Don't waste analyst time re-checking obviously safe recurring subscriptions or obviously bad bot traffic.

Webhooks and real-time alerts help operations react before fulfillment. If a payment event, account change, or verification failure happens, the right team should know immediately. Delay turns a reversible risk into a shipped loss.

Device and behavioral signals are good at stopping fraudsters who pass surface-level checks. A clean card and a plausible address don't mean much if the underlying behavior looks automated, inconsistent, or evasive.

For a wider strategy lens, Logical Commander Software Ltd. on fraud has a useful breakdown of how merchants can structure controls without turning the customer journey into a maze.

Why layered controls beat one big rule engine

Merchants often build fraud stacks in the wrong order. They start with rigid decline rules, then add exceptions, then add manual reviews, and eventually nobody understands why orders are approved or blocked.

A better sequence looks like this:

Filter obvious abuse early. Block clearly invalid inputs, repeated high-risk attempts, and known bad behaviors.

Score what remains. Let the system weigh transaction, identity, and behavioral signals together.

Step up verification selectively. Ask for stronger proof only when the risk justifies it.

Route edge cases to humans. Keep the queue small and focused.

Feed outcomes back into the rules. Every confirmed fraud case and every false decline should improve the model.

That last step is where many teams fail. They collect losses but don't collect lessons. A chargeback reason, an account recovery event, a failed payout change, or a support transcript often tells you exactly which control broke.

A strong fraud stack doesn't try to make every transaction safe. It tries to make risky transactions expensive and inconvenient for the attacker.

An Operational Playbook for Managing Fraud

Fraud prevention matters, but response discipline matters just as much. Every merchant eventually has a transaction that slips through. When that happens, improvisation creates more loss than the original fraud.

Build a review queue before you need one

Set a clear threshold for orders that require review before fulfillment. Don't leave this to whoever happens to be online. The team should know which signals trigger a hold, who reviews it, what evidence they check, and how fast they need to decide.

A simple operational queue should capture:

Order context: What was purchased, for how much, and by whom

Risk notes: Why the order was held

Verification status: Whether the customer responded and what they provided

Fulfillment state: Not started, partially delivered, or fully delivered

Decision owner: Who approved, rejected, or escalated it

This is also where refunds, reversals, and disputes need a standard path. If you don't already have one, Suby's overview of chargeback management is a useful operational reference because it focuses on what merchants need to document when a payment turns into a formal dispute.

Know when to fight and when to write it off

Not every chargeback deserves representment. New business owners often react emotionally and try to contest everything. That's expensive. You need a decision rule, and building reliable chargeback protection into your workflow makes those calls far easier.

Fight when you have strong evidence. That usually means clear delivery records, accepted terms, account usage logs, customer communication, and proof that the transaction came from the genuine customer journey rather than a hijacked path.

Accept the loss when the evidence is thin, the amount is low, or the internal cost of fighting is higher than the likely recovery. Operations leaders learn this fast. Winning every dispute is impossible. Preserving team time is part of fraud control.

A solid playbook also includes post-incident review:

Which signal was missed

Whether fulfillment happened too early

Whether support bypassed verification

Whether a policy change is needed

The point isn't blame. The point is closing the gap before the next attempt.

Unified Fraud Protection for Modern Payments

Most fraud advice was built for merchants with one checkout rail and one settlement path. That's not how many internet businesses operate now. They might accept cards, bank methods, wallets, and crypto in one commercial flow, while settling to a bank account or stablecoins like USDC depending on treasury needs.

That creates a practical problem. Fraud controls are often split by payment method, team, and tool. Card checks live in one system. Bank payment review lives in another. Crypto monitoring sits somewhere else, if it exists at all. The result is a fragmented risk picture.

Why hybrid checkouts create blind spots

This is the part most guides miss. The impact of fraud on crypto-native SaaS and cross-border agencies using stablecoin settlements is rarely addressed with data. Traditional card fraud gets plenty of attention, but the crypto-fiat hybrid model remains a black hole in compliance literature, which leaves merchants unsure whether ordinary KYC and AML controls are enough for USDC payouts and mixed payment flows.

That gap matters because hybrid businesses don't experience fraud in neat silos. A customer can enter through a card flow, trigger support through email, ask to change settlement details, and later interact with a crypto payout path. If each step is reviewed separately, nobody sees the whole pattern.

What a unified control model looks like

A better model starts with a shared risk layer across all payment methods. The business doesn't need identical rules for every rail, but it does need consistent logic. The same customer identity, account history, device context, payout preference changes, and behavioral pattern should inform every decision.

This is where payment infrastructure matters. Suby is payment infrastructure for the global internet economy, and it provides an API that lets businesses accept payments by card or crypto while supporting broader pay-ins across cards, wallets, bank methods, BNPL, and crypto. Customers can pay any way they want, and businesses can receive funds the way they choose, either to a bank account or in stablecoins like USDC. One practical flow is that a customer pays by card and the business receives USDC, but that's only one option among several.

Suby is one product with four ways to use it:

Suby Payments for API-first checkout across card, bank transfer, Apple Pay, Google Pay, Klarna, and more, or crypto

Suby Crypto as a crypto payment gateway that handles the swap, sponsors gas, and lets the business keep funds in a self-custody wallet or a unified Suby balance, receiving the same assets the customer paid or auto-converting everything to USDC on Base

Suby Gating for paid access to Discord, Telegram, downloads, and courses

Suby Invoicing so clients can pay how they want while the business receives what it wants

For businesses running subscriptions, paid communities, or online access products, Suby also offers native integrations with Discord and Telegram. That's useful because fraud control doesn't stop at payment acceptance. It also affects who gets access, when access is revoked, and how quickly your team can respond to failed or reversed payments.

The operational advantage is simple. When the payment stack, balance, and payout choices sit in one system, teams have a better chance of applying unified checks instead of method-by-method guesswork. Pricing is method-dependent, so merchants should review exact figures on the pricing page rather than assume a flat rate.

Staying Ahead of Legal and Compliance Rules

Fraud prevention and compliance overlap, but they aren't the same thing. A merchant can have decent fraud instincts and still create legal or audit problems by handling card data badly, skipping required customer authentication, or keeping poor records.

The merchant checklist

PCI DSS responsibilities apply if you accept card payments. In practice, merchants should minimize direct exposure to card data and rely on compliant infrastructure where possible. If you want a practical external checklist, the audit-ready PCI DSS 4.0 guide is a solid starting point for understanding what teams need to document and control.

Strong Customer Authentication matters in markets where it's required, but it's also a useful risk control beyond formal compliance. It helps prove that a sensitive action had stronger verification behind it.

Data privacy and retention need boring discipline. Keep what you need for fraud review and dispute handling, but don't collect random sensitive data just because it might be useful later.

Provider due diligence matters too. If you're evaluating infrastructure, check what parts of compliance the provider helps you offload. Suby works with a PCI-DSS Level 1 certified processing partner and supports SCA, 2FA, dispute handling, and zero-fee refunds. Merchants that want a deeper look at the card-side obligations can review Suby's guide to PCI compliance requirements.

Compliance won't stop fraud on its own. It does something just as important. It keeps your payment operation defensible, auditable, and less fragile when something goes wrong.

Suby is a payment gateway and Merchant of Record. Your customers pay with card, bank transfer, Apple Pay, Google Pay, Klarna, and more, or stablecoins, and you get paid out to your bank account, or directly in stablecoins (USDC, EURC) to your wallet, anywhere in the world, no bank account required. It runs on one API, with native Discord and Telegram integrations for subscriptions and paid access. For fraud payment operations, that unified stack puts card, bank, wallet, and crypto activity under one risk layer, so hybrid checkouts stop creating the blind spots that let fraudulent transactions slip between separate tools.