You log into your payment dashboard, see a dispute notification, and your first reaction is usually the same. Confusion first, then annoyance, then a more serious question: did the customer have a problem, or did the bank just pull money out of your account with almost no warning?

That reaction is normal. Chargebacks feel personal when they first happen, especially if you shipped the order, delivered the service, or have clean transaction records. But this isn't a rare edge case. In 2023, the global payment industry recorded over 238 million chargebacks, with projections of 261 million in 2025 and 324 million by 2028, and merchants won only an average of 45% of them, according to PayCompass citing Mastercard and Datos Insights.

For online businesses, chargebacks sit in the awkward zone between fraud prevention, customer support, fulfillment, and payment operations. If you treat them as only a fraud problem, you'll miss half the causes. If you treat them as random noise, they'll keep eating margin and creating processor risk.

A practical understanding helps. The search query "chargeback what is" sounds basic, but the real answer isn't just a definition. It's how chargebacks start, why they happen, what they cost, and what you can do before the next one lands.

Table of Contents

- That Sinking Feeling When You Get Your First Chargeback

- The simple definition that actually matters

- Chargeback vs refund at a glance

That Sinking Feeling When You Get Your First Chargeback

The first chargeback usually arrives without context. You don't get a clean narrative. You get a dispute alert, a reason code that may not be obvious, and a debit against funds you thought were settled.

For a merchant, it feels backward. The customer didn't email support. They didn't ask for a refund. They went to the bank, and now you have a deadline, a shrinking window to respond, and a case file to build.

That moment causes two mistakes.

First, some businesses panic and contest every dispute, including the ones they shouldn't fight. Second, others give up immediately and accept every chargeback as a cost of selling online. Both approaches are expensive. One burns time on weak cases. The other trains your team to absorb avoidable losses.

Most merchants don't need a heroic chargeback strategy. They need a disciplined one.

A better response starts with separating emotion from diagnosis. Ask four questions right away:

- Was the transaction authorized: Does your record show a normal customer journey, expected checkout behavior, and a legitimate purchase pattern?

- Was the product or service delivered: Can you prove shipping, access, usage, or fulfillment?

- Did the customer have a support path: Was it easy for them to contact you before going to the bank?

- Is the billing line recognizable: Would the buyer know your business name when they scanned their statement?

Those questions matter because chargebacks don't come from one place. Some are real fraud. Some are misunderstandings. Some happen because your own billing, delivery, or post-purchase communication created enough friction for the customer to dispute first and ask questions never.

That last category gets ignored in most basic guides, but it's where many international merchants get hit. Cross-border payments introduce extra confusion around pricing, descriptors, delivery expectations, and settlement visibility. When the payment experience feels unclear, disputes rise even if the order itself was valid.

What Is a Chargeback and How Is It Different from a Refund

The simple definition that actually matters

A chargeback is a payment reversal initiated through the cardholder's bank after the customer disputes a transaction. The shortest useful definition is this: it's a forced refund through the banking system, not through your support team.

That distinction matters because you don't control the opening move. In a normal refund, the customer contacts you, you review the issue, and you decide whether to return the money. In a chargeback, the issuer steps in first, removes funds provisionally, and asks questions inside a formal dispute process.

Chargebacks weren't invented to make merchants miserable. They started as consumer protection. The Fair Credit Billing Act of 1974 formally established chargebacks in the United States and gave cardholders the right to dispute fraudulent transactions, billing errors, or undelivered goods and services within a 60-day window, as described in this history of chargebacks and the FCBA.

So if you're searching "chargeback what is," the full answer is both legal and operational. It's a consumer protection mechanism that became a merchant operations problem.

Chargeback vs refund at a glance

| Aspect | Refund | Chargeback |

|---|---|---|

| Who starts it | The merchant, usually after the customer contacts support | The cardholder's bank after a dispute |

| Where it happens | Inside your support and payment workflow | Inside the card network dispute process |

| Merchant control | High | Limited and reactive |

| Customer relationship impact | Often preserves goodwill | Often signals the relationship has already broken down |

| Evidence needed | Usually minimal | Often requires transaction, delivery, and communication records |

| Operational burden | Lower | Higher |

| Risk to payment account | Low | Can affect your chargeback ratio and processor standing |

A refund is almost always the cleaner path when a customer has a valid issue and reaches out early. That's why refund operations matter more than most merchants think. If you sell on Shopify, a practical resource on handling that side well is Master Refunds on Shopify, especially if your team still treats refunds and disputes as unrelated workflows.

Practical rule: If a customer is reachable and the complaint is legitimate, a refund is usually cheaper than letting the dispute become a chargeback.

The merchants who keep chargebacks under control usually do one thing well. They make it easier to resolve a problem with them than with the bank.

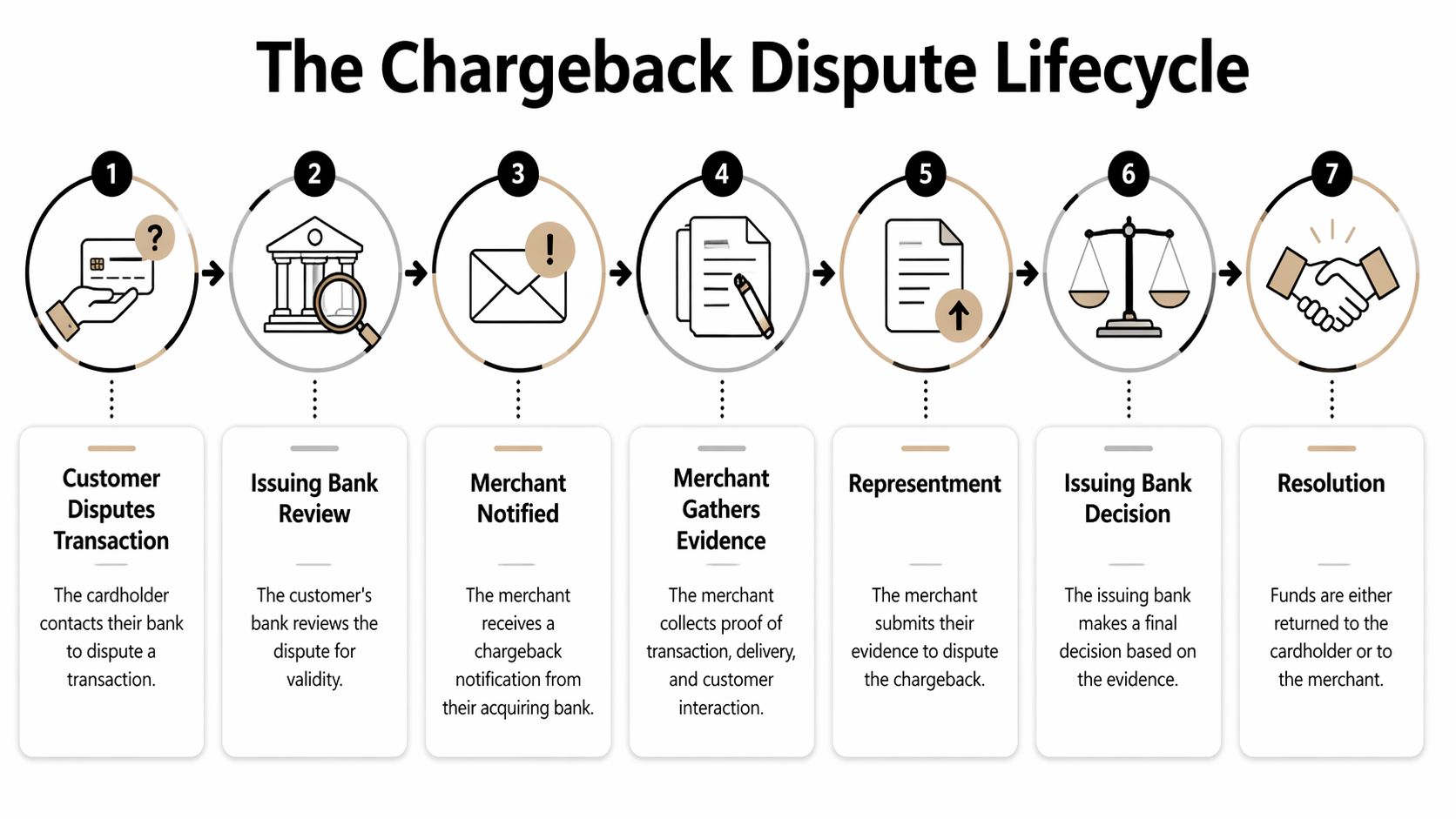

The Chargeback Dispute Lifecycle Step by Step

What happens after the customer calls the bank

The process is structured, even if it doesn't feel that way when you're in it.

The customer disputes the transaction

They contact their issuing bank and claim something was wrong. That could mean fraud, a billing error, non-delivery, or a service complaint.The issuer reviews the claim

If the bank accepts the complaint as valid enough to proceed, it opens the dispute and pushes the case into the card network flow.Your acquirer or processor notifies you

This is often the first point where the merchant sees the issue clearly. By then, funds may already be debited provisionally.You decide whether to accept or fight it

Some chargebacks should be accepted. Others should be contested. The mistake is treating every case the same.You build a representment package

This is your response. It usually includes order details, delivery confirmation, usage logs, customer communication, billing records, and anything else that directly addresses the dispute reason.The issuer reviews your evidence

The bank then decides whether to reverse the chargeback or uphold it.The case closes, or escalates

Some disputes end there. Others move into further review depending on network rules and the facts of the case.

Where merchants usually lose

Speed matters more than many teams expect. Once a cardholder files a dispute, the merchant typically has only 7 to 45 days to submit evidence, depending on the card network, and Visa allows 20 days for a representment response, according to PayPal's explanation of the chargeback process.

That means the operational challenge isn't just "prove you were right." It's "prove it quickly, in the right format, and with evidence that matches the reason code."

Common failure points look like this:

- Slow internal handoff: Support has the emails, ops has the delivery record, finance has the transaction detail, and nobody assembles the file in time.

- Too much irrelevant evidence: Merchants often send everything instead of sending the few records that directly answer the claim.

- Weak documentation: A vague tracking update or generic invoice rarely wins a dispute on its own.

- Fighting bad cases: If the order was mishandled, representment won't rescue it.

Good dispute handling is mostly records discipline under deadline pressure.

The best teams build the evidence trail before any dispute happens. They don't start searching for proof after the bank notice arrives.

Common Reasons Merchants Receive Chargebacks

Reason codes tell you where to look

Chargebacks don't arrive as open-ended complaints. They come with reason codes, and those codes matter because they tell you what kind of evidence the bank expects. Across networks like Visa and Mastercard, there are roughly 150 of these codes, and they shape how merchants fight disputes, as outlined by Chargeback Gurus in its overview of merchant chargebacks.

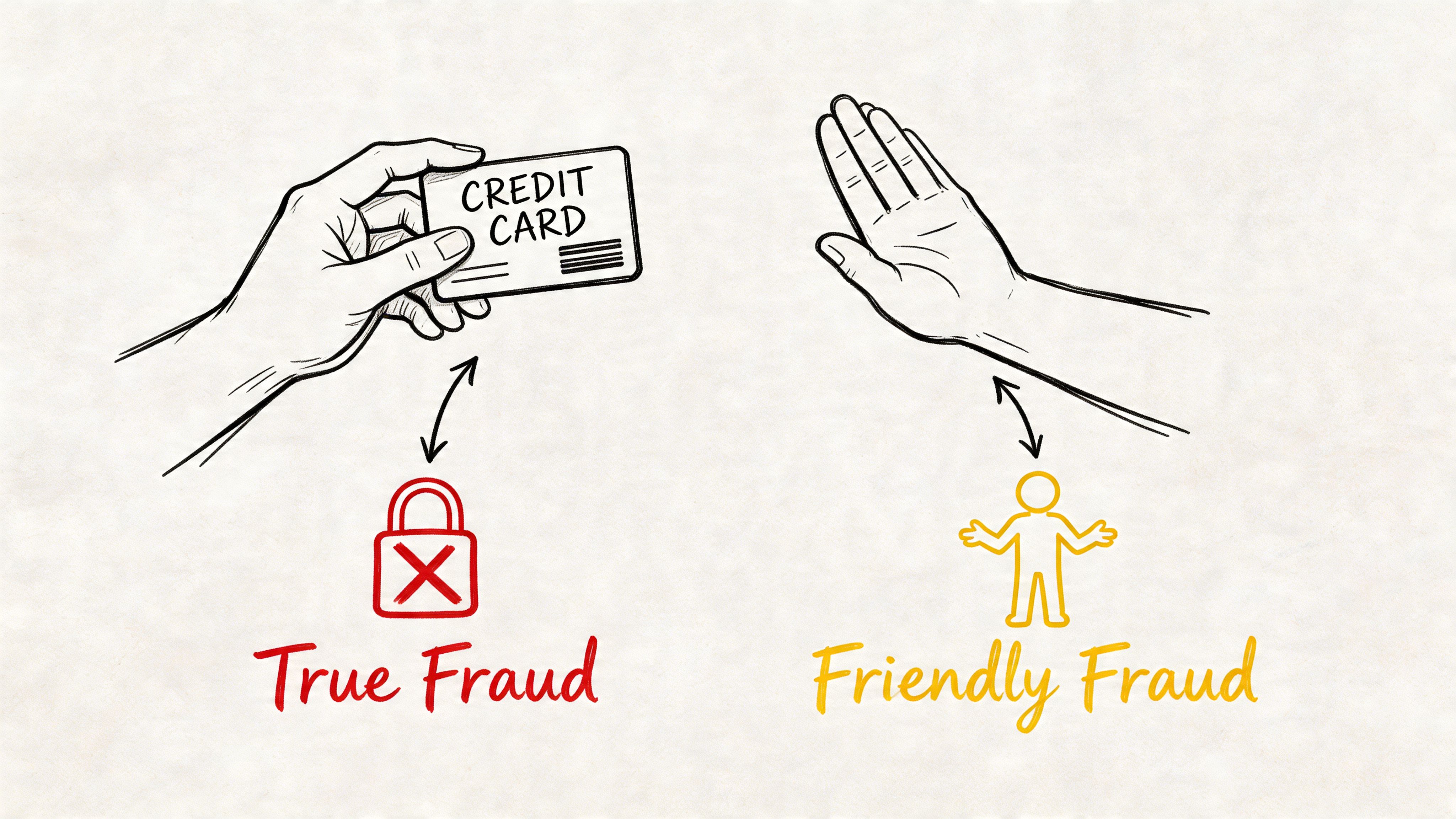

The same source notes that friendly fraud can make up up to 70% of all chargeback volume. That's why many merchants feel blindsided. They assume disputes mostly come from stolen cards. In reality, a large share comes from legitimate customers disputing legitimate transactions.

If you're trying to reduce that category, it helps to understand the broader context of payment fraud patterns businesses deal with, because not every disputed transaction is criminal fraud and not every "fraud" claim reflects what happened.

The three buckets that matter in practice

True fraud is the easiest category to understand and often the hardest to win. The cardholder says they never authorized the transaction. Sometimes that's accurate. Stolen credentials, unauthorized card use, and account takeover fall here.

Friendly fraud is more slippery. A customer may recognize neither your billing descriptor nor the purchase, may forget a subscription renewal, or may dispute a valid charge instead of asking for a refund. Some cases are careless. Some are deliberate.

Merchant error is the category businesses most want to ignore. Duplicate billing, poor fulfillment, vague delivery timelines, unclear pricing, confusing renewal terms, and support that responds too late all create chargebacks that look like fraud on the surface.

A few examples show how this plays out:

- Transaction not recognized: Often tied to confusing billing descriptors or a buyer forgetting a purchase.

- Item not received: Sometimes a real delivery problem, sometimes a fulfillment communication problem, sometimes abuse.

- Not as described: Can come from inaccurate product pages, mismatched expectations, or a customer bypassing your return policy.

- Duplicate processing: Often a systems or checkout issue, especially in complex international flows.

If you only ask "was this fraud," you'll miss the operational cause and the next dispute will happen the same way.

For cross-border merchants, payment friction often sits underneath these reason codes. A customer sees one price at checkout, another figure after conversion, or a statement entry they don't recognize in a foreign buying context. The bank then receives a dispute that looks like billing error or duplicate charge. The underlying problem was payment architecture, not product quality.

The Hidden Costs of Chargebacks for Your Business

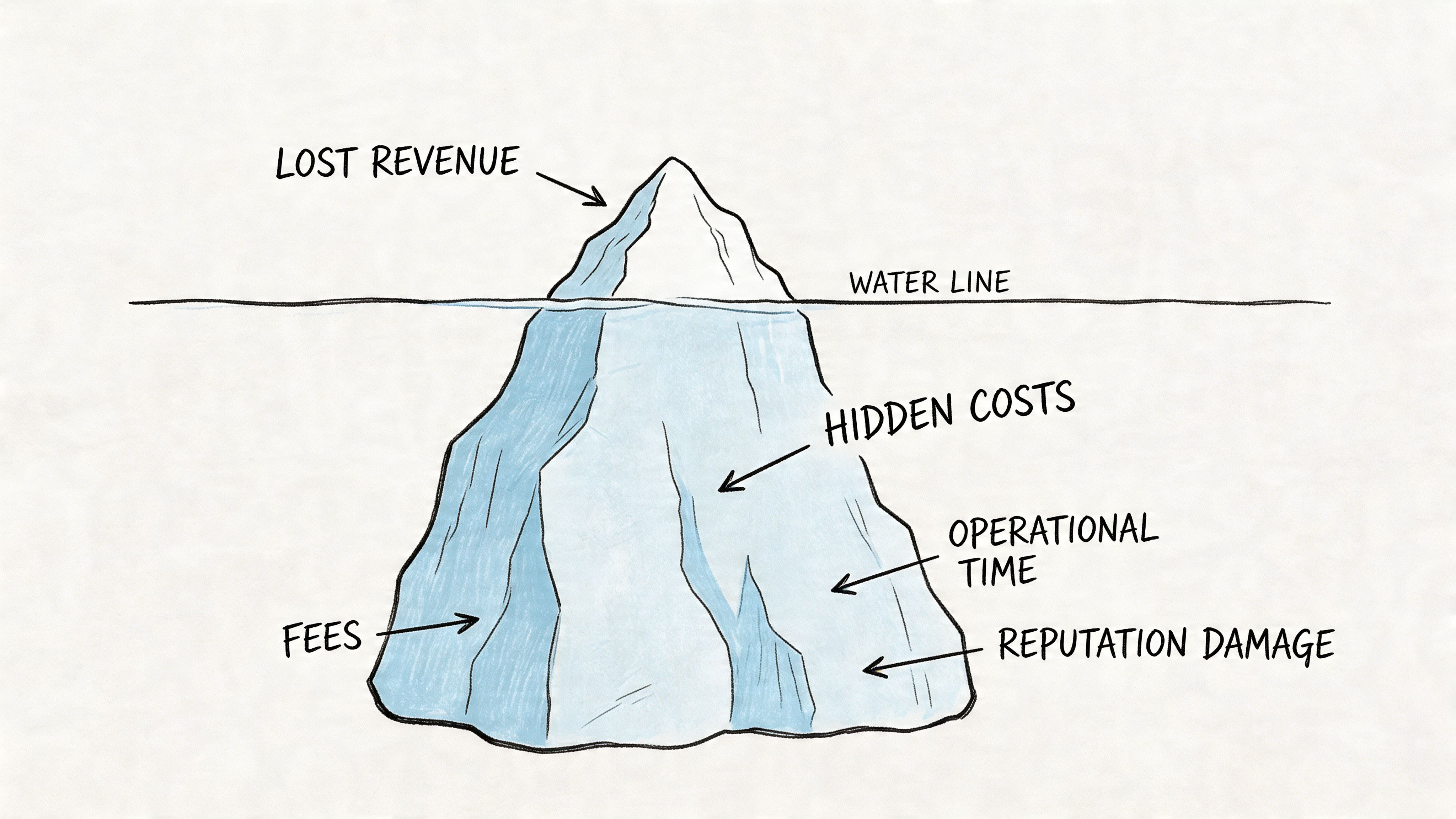

The direct loss is obvious. You lose the sale, the product or service may already be gone, and the processor may attach a fee. That's the part every merchant notices first.

The larger problem sits below the surface. Chargebacks pull support, finance, operations, and risk teams into manual work. They distort revenue reporting. They create friction with processors. They also force you to spend time proving things that should have been obvious from the original transaction trail.

The visible loss is only the start

According to Chargeback Help's guide to lowering chargebacks, merchants can face an initial fee of $20–$100 per dispute, and if their chargeback ratio exceeds thresholds, often as low as 0.56%, they can end up in mandatory monitoring programs that cost thousands per month or even have accounts frozen or terminated.

That changes the conversation. A chargeback isn't just one unhappy customer. It can become a processor-level risk signal.

Here are the hidden costs merchants feel fastest:

- Staff time: Someone has to locate records, write responses, and manage deadlines.

- Lost inventory or delivered service: Physical goods don't come back automatically. Digital access may already have been consumed.

- Support pressure: Chargeback-heavy businesses often see support volume rise because the same clarity problems that create disputes also create tickets.

- Decision fatigue: Teams start making bad refund and risk choices when every dispute feels urgent.

Why processor risk matters more than one lost order

A business can survive a few disputes. What hurts is the pattern. Once processors start seeing increased chargeback activity, they may respond with tighter controls, reserves, extra reviews, or a harder path to growth.

This short explainer is useful if your team still sees chargebacks as a simple fee line item:

A chargeback problem is rarely just a finance problem. It usually means checkout clarity, customer communication, or fulfillment discipline is weaker than it should be.

For international businesses, the hidden cost gets worse because payment friction creates disputes that look avoidable in hindsight. Confusing foreign charges, statement mismatch, delayed settlement visibility, and uneven post-purchase communication all increase operational drag. You don't just lose the disputed transaction. You create support work and processor scrutiny you didn't need.

A Practical Guide to Managing Chargebacks

How to respond when a chargeback hits

The first move is triage, not defense. Read the reason code, pull the order timeline, and decide whether the dispute is valid. If the customer was truly defrauded or your team made a clear fulfillment mistake, accept the chargeback and fix the process that caused it.

If the case is worth fighting, build your response around the claim, not around your frustration.

A practical workflow looks like this:

Match the evidence to the dispute

For a non-delivery claim, focus on shipment, delivery, access logs, or service completion. For a "not recognized" claim, focus on billing details, prior purchase history, and customer identity signals.Create one clean chronology

Show the order date, payment confirmation, delivery or access event, and any customer communication. Banks respond better to a coherent timeline than to a pile of screenshots.Use primary records

Order confirmation, invoice, signed delivery proof, usage logs, support exchanges, cancellation records, and checkout acceptance records usually matter more than internal notes.Submit before the deadline

A strong case submitted late is still a lost case.Track outcomes by reason category

Don't just record "won" or "lost." Record why the dispute happened and whether your evidence was fit for that code.

Contest fewer cases, but contest the right ones with cleaner evidence.

If your team doesn't have a standard operating procedure yet, start one immediately. A simple checklist beats an improvised response every time. This guide on how to avoid payment disputes before they escalate is a useful companion for operational teams working on that checklist.

How to prevent the next one

Prevention isn't one tool. It's a stack of small decisions that remove ambiguity for the customer and produce better records for the merchant.

- Use a recognizable billing descriptor: If the customer doesn't recognize your statement name, they may dispute a valid charge.

- Make delivery and access visible: Send clear confirmations, shipping updates, or service-access emails right after purchase.

- Keep cancellation simple: Subscription disputes spike when customers can't find the cancellation path or don't trust that it worked.

- Write a refund policy humans can understand: A vague policy protects nobody. A clear one often prevents escalation.

- Store proof automatically: Don't rely on staff memory. Save order events, support messages, fulfillment data, and customer acknowledgments in one place.

- Review payment friction points: If cross-border buyers face confusing pricing, currency surprises, duplicate-looking entries, or failed retries, you'll see that confusion later as disputes.

One more practical note. Not all prevention sits inside fraud tooling. Many chargebacks start after payment approval, in the messy space where communication, fulfillment, and billing meet. That's why payment operations and customer operations need to work from the same playbook.

How Your Payment Solution Can Be Your Best Defense

Most businesses evaluate payment providers on approval rates, checkout design, and fees. They should also evaluate them on dispute visibility, refund flexibility, billing clarity, and how much cross-border confusion the payment flow introduces.

That's where modern payment architecture changes the conversation. Traditional setups often add friction for international buyers through currency conversion confusion, unfamiliar billing lines, payout delays, and fragmented support records. That friction doesn't always show up as a failed checkout. It often shows up later as a chargeback.

A better stack reduces ambiguity before the customer ever contacts their bank. If you're comparing various payment tools, look beyond front-end checkout features and inspect the full payment lifecycle. How clear is the customer experience? How easy is it to issue refunds? How complete is the dispute evidence trail? How clean is the handoff between payment data and support data?

For businesses that want a simpler cross-border setup, it's worth reviewing options that let users pay by card while the business receives USDC, because that can remove some of the FX and settlement friction that often creates disputes in the first place. If you're exploring that model, this guide on how to accept credit card payments is a practical starting point.

The right payment partner doesn't eliminate chargebacks. Nothing does. But it can remove the avoidable ones, speed up your response to the valid ones, and lower the operational mess around the rest.

Suby helps online businesses accept payments by card or crypto while receiving USDC. It provides an API, webhooks, paylinks, embedded checkout, and native integrations for Discord and Telegram use cases like subscriptions, paid access, and online communities. If you want a payment setup where users pay with cards and your business receives USDC, see Suby.