You launch card payments, revenue starts moving, and then someone on your team asks a simple question that usually lands with a thud: “Are we PCI compliant?”

That moment catches a lot of founders off guard. They assumed their payment provider handled the hard parts, or that PCI DSS was mostly paperwork for large enterprises. In practice, pci compliance requirements become a real issue the minute your business stores, processes, transmits cardholder data, or operates systems that could affect the security of that environment.

The mistake I see most often isn't ignorance of the 12 requirements. It's starting in the wrong place. Teams obsess over forms, scans, and policy templates before they answer the one question that drives almost everything else: what is in scope? If you get scope wrong, your audit gets harder, your controls get messier, and your engineering team wastes time securing systems that should never have touched card data in the first place.

Table of Contents

- Why PCI Compliance Matters More Than You Think

- The six objectives that organize PCI DSS

- What each requirement means in practice

Why PCI Compliance Matters More Than You Think

A common startup pattern looks like this. Product ships first, checkout works, customers pay, and only later does someone ask where card data goes, who can access payment logs, and whether support screenshots are exposing anything sensitive.

That is usually when PCI stops sounding abstract.

PCI DSS is a security baseline for any business handling card data, not a ceremonial annual form. The standard exists to protect payment data across the payment lifecycle, and the compliance burden can become painful if your architecture grew without clear boundaries. The operational risk is straightforward: once card data or systems affecting card data spread into your app, admin tools, support workflow, or internal network, cleanup gets expensive and slow.

The reason this matters so much is simple. Most organizations struggle to sustain compliance even after they know the rules. According to Verizon's Payment Security Report, as referenced by SecureTrust's PCI compliance requirements guide, only 14.3% of global organizations maintained full compliance at interim assessment, which means roughly 85.7% were non-compliant at that checkpoint.

Practical rule: PCI isn't hard because the standard is mysterious. It's hard because businesses change faster than their controls do.

Founders often expect a one-time setup. Auditors don't. If your payment flow changes, if a developer adds a new webhook consumer, if support tooling starts capturing payment metadata, your scope may change with it.

That's why the smartest PCI strategy usually starts with architecture, not paperwork. If you can keep raw cardholder data out of your systems, keep access narrow, and document clean boundaries, the rest of the program becomes manageable.

The 12 PCI Compliance Requirements Explained

The PCI DSS framework is built around 12 main requirements organized into six control objectives, creating a standard baseline for businesses that handle payment card data, as outlined by UCSF's walkthrough of PCI compliance requirements.

The six objectives that organize PCI DSS

PCI DSS is easier to understand when you stop reading it as a list and start reading it as a control model.

| Control objective | What it covers |

|---|---|

| Build and maintain a secure network and systems | Firewalls, secure configurations, and eliminating unsafe defaults |

| Protect account data | Securing stored data and protecting data in transit |

| Maintain a vulnerability management program | Malware defenses, patching, and secure software maintenance |

| Implement strong access control measures | Least privilege, unique identities, and physical access restrictions |

| Regularly monitor and test networks | Logging, monitoring, vulnerability scans, and control verification |

| Maintain an information security policy | Governance, documented responsibilities, and staff expectations |

Read that list closely and a pattern appears. PCI is trying to stop four common failures: data exposed unnecessarily, systems left weak by default, access granted too broadly, and control failures going unnoticed.

What each requirement means in practice

Here's the plain-English version of the 12 requirements.

Firewall and network security controls

You need a defined boundary between trusted systems and the public internet. In real environments, this means controlled pathways into the CDE, not flat internal networks where everything can talk to everything.No vendor-supplied defaults

Default passwords, stock configurations, and unused services are easy wins for attackers. They also signal weak operational discipline.Protect stored cardholder data

If you store payment data, that storage has to be tightly controlled. The better move for many teams is to avoid storing it directly at all.Encrypt cardholder data in transit

Data moving across open or public networks must be protected. This matters in browser-based flows, APIs, and any handoff between systems.

If card data passes through more places than necessary, your compliance problem isn't just security. It's architecture.

Protect systems against malware

Teams often treat this as an endpoint checkbox. Auditors look for whether protection is deployed, updated, and monitored where it matters.Develop and maintain secure systems and applications

Secure coding, patching, and disciplined change management all sit here. A vulnerable app connected to the payment environment is still a PCI issue.Restrict access by business need-to-know

Not every engineer, analyst, or support rep should be able to reach payment systems. Least privilege has to be designed, not assumed.Assign a unique ID to each person

Shared accounts undermine accountability. If an action happens in scope, you need to know exactly who did it.Restrict physical access

This applies to offices, devices, paper records, and any place sensitive payment data might be exposed physically.Track and monitor all access

Logs are not optional. You need visibility into who accessed what, when, and whether something abnormal happened.Regularly test security systems and processes

Controls that aren't tested drift over time. Testing proves they still work after changes, patches, and deployment cycles.Maintain a security policy for all personnel

PCI expects security to be institutional, not tribal knowledge held by one senior engineer.- Admin laptops that can log into payment infrastructure

- Identity systems that grant access into payment services

- Logging platforms that collect payment application events

- CI/CD pipelines that deploy code into in-scope systems

- Third-party support tools if they can expose card-related data or alter a payment workflow

Trace where card data first appears

Start at the customer input point. If your frontend collects card details directly, that matters immediately.List every system that touches payment events

Include web apps, APIs, queues, dashboards, support tools, and internal admin surfaces.Map who can affect those systems

Access paths matter as much as storage paths.- SAQ path means you attest to the controls relevant to your environment.

- RoC path means a qualified assessor performs a deeper review.

- Quarterly scanning and evidence collection may still apply depending on your setup.

Access control

Every person who can reach in-scope systems should have a unique identity, a defined role, and a reviewable access path. Shared admin accounts create immediate trouble.Encryption and data handling

Protect data at rest where storage exists, and protect data in transit across public networks. Just as important, remove unnecessary copies from logs, tickets, and exports.System hardening

Secure configurations, patching, and removal of unsafe defaults should be routine, not occasional cleanup after a failed assessment.Malware protection and endpoint discipline

This matters most on systems that can affect the CDE, including administrator workstations.Bad scoping

Teams exclude systems that can clearly affect the CDE, especially admin tools, identity providers, and deployment pipelines.Annual-checklist thinking

Controls get refreshed before validation and then decay. Access reviews stop, logging rules drift, and exceptions pile up.Policy without operations

A polished policy library won't save you if your engineers bypass the documented process every time production gets busy.Too much payment data in too many places

Logs, screenshots, exports, and support threads quietly expand your risk surface.- Their own website and app security

- Access control for admin users

- Safe handling of payment-related metadata

- Vendor oversight and documentation

- Accurate scoping of connected systems

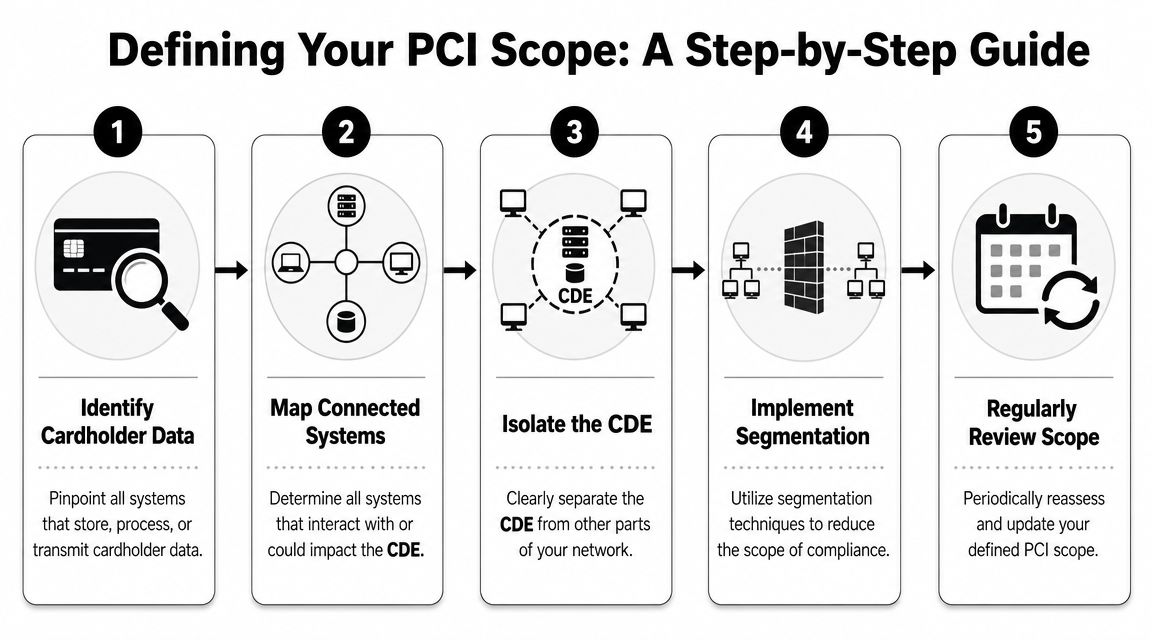

Defining Your Scope The Most Important Step

Teams often make PCI harder than it needs to be because they start with the controls before they define the boundary. The boundary is your Cardholder Data Environment, or CDE.

PCI DSS applies to systems, people, and processes that store, process, or transmit cardholder data, and also to anything that could impact the security of the CDE, according to the PCI Security Standards Council standards page. That second part is where founders usually get surprised.

What belongs in the CDE

The obvious in-scope systems are easy to spot. Payment pages that handle card entry, servers that process payment requests, vaulting systems, and tools that store payment-related records are clearly relevant.

The harder cases are adjacent systems. These often include:

That's why a scoping exercise has to be more than a network diagram. You need a data flow view and an access view. If a system can affect the confidentiality or security of the CDE, it deserves scrutiny.

For teams that are still deciding how to accept card payments online, this becomes much easier when the payment flow is designed to keep card entry and processing outside your own application footprint. This guide on how to accept credit card payments is useful background if you're comparing hosted versus direct card handling models.

A quick walkthrough helps many teams map the boundary more accurately:

Later in the scoping review, this explainer can help frame the process visually:

How teams actually reduce scope

Scope reduction is where the biggest operational wins happen. Two methods matter most: segmentation and tokenization.

Segmentation means separating the CDE from the rest of your environment so unrelated systems cannot freely connect to it. This reduces both risk and audit burden. Without segmentation, the practical answer to “what's in scope?” often becomes “far too much.”

Tokenization helps replace sensitive card data with a non-sensitive reference. That changes the architecture materially. Your app may still orchestrate payments, but it no longer needs to retain raw payment data.

A small, well-isolated CDE is easier to secure, easier to explain to an auditor, and easier to keep compliant when your product changes.

What doesn't work is “soft segmentation,” where teams claim systems are separate but still allow broad admin access, shared credentials, or uncontrolled internal connectivity. Auditors look for enforceable boundaries, not diagrams alone.

Navigating Merchant Levels and Validation Paths

Founders usually ask this next: “What exactly do we have to submit?” The answer depends on your merchant level, your acquiring bank, and how your payment flow is designed.

Why merchant level matters

Merchant levels are generally tied to annual transaction volume, and those levels affect how you validate compliance. In practice, smaller merchants often validate with a Self-Assessment Questionnaire, while larger merchants may face a formal Report on Compliance performed by a Qualified Security Assessor.

You should still confirm the exact requirement with your acquirer. Card brand rules and acquiring-bank expectations can vary, and your integration model matters as much as your size.

Here is the practical summary generally needed first:

| Merchant Level | Annual Transaction Volume | Validation Requirement |

|---|---|---|

| Level 1 | High transaction volume, threshold set by card brands and acquirers | Typically formal assessment, often a Report on Compliance by a QSA |

| Level 2 | Lower than Level 1 but still substantial | Commonly annual Self-Assessment Questionnaire, depending on acquirer |

| Level 3 | Lower-volume merchants, often including ecommerce bands | Usually Self-Assessment Questionnaire |

| Level 4 | Smaller merchants outside higher tiers | Usually Self-Assessment Questionnaire |

Validation paths in plain English

A founder-friendly way to think about validation is this:

Architecture affects paperwork: A merchant that keeps card data off its own systems usually has a much cleaner validation path than a merchant with a custom payment page and broad backend access to payment systems.

If you're comparing hosted processors and trying to understand the security questions buyers ask, this breakdown of whether Stripe is safe is a useful example of the kind of due diligence merchants apply to payment providers generally.

Key Technical and Organizational Controls in Practice

Most failed PCI programs don't fail because nobody installed a control. They fail because the control exists on paper but not in a way that produces usable evidence.

Controls that auditors expect to see working

Start with the basics that often expose weak implementations:

A lot of teams also underestimate test design. If you're planning annual or change-driven testing, this guide to scoping PCI penetration tests is a useful reference because the value of a pen test depends heavily on what was placed in scope.

Evidence matters as much as implementation

A key operational control in PCI is continuous evidence generation. Requirement 10 requires logging actions involving cardholder data, and PCI guidance also expects regular testing, including quarterly external and internal vulnerability scans, as described in ControlCase's breakdown of the 12 PCI DSS requirements.

That changes how you should build your stack. Logging should be centralized. Authentication events should correlate with system actions. Scan results should lead to tracked remediation, followed by proof that the fix worked.

One useful test: if an assessor asks who accessed a payment-related system last week, what changed, and how you know the change was reviewed, your team should be able to answer without reconstructing the story by hand.

For engineering teams building payment capabilities into products, a clean payment gateway API integration matters here because integration choices decide whether you inherit broad PCI responsibility or keep the card flow more isolated.

Common Compliance Pitfalls and How to Avoid Them

The most common PCI mistake is treating the audit as the project. It isn't. The project is keeping your environment stable, explainable, and controlled between assessments.

Where teams usually fail

A few patterns show up repeatedly:

One operational truth is worth keeping in view. Compliance often fails in the handoffs: engineering to DevOps, support to finance, vendor to merchant. If nobody owns the whole payment data flow, gaps appear.

What PCI DSS 40 changes operationally

PCI DSS 4.0 pushes teams away from static checkbox compliance and toward a more continuous, risk-based model. It also strengthens authentication expectations, including MFA for all access into the cardholder data environment, not just remote access, as noted in Optro's overview of PCI DSS requirements.

That matters in everyday operations. Internal administrators, developers with production access, and support users with advanced privileges all come into focus. Old assumptions like “it's only internal” no longer hold up well.

Compliance that depends on one security lead reminding everyone what to do will break the first time the team scales or the architecture changes.

The practical fix is boring but effective: tighten ownership, review access regularly, document exceptions, and treat infrastructure changes as potential scope changes.

How a Certified Partner Simplifies Your Compliance

The easiest PCI burden to manage is the one you never create in your own environment.

What outsourcing actually removes

If a certified payment partner handles card capture and processing in a hosted or tokenized flow, raw cardholder data doesn't need to pass through your servers. That changes your PCI obligations materially. You still have responsibility, but your scope can become much narrower.

This is the main reason experienced teams lean toward payment architectures that keep sensitive card handling off the merchant stack. The fewer systems that store, process, or transmit card data directly, the easier the assessment, the cleaner the evidence trail, and the lower the chance that an unrelated internal system gets pulled into scope.

One option in that category is Suby. It provides an API that lets businesses accept payments by card or crypto, while businesses receive USDC. It also offers native Discord and Telegram integrations for subscriptions, paid access, and online communities. In the PCI context, the relevant point is architectural: users pay with cards, businesses receive USDC, and keeping raw card handling with a compliant processing partner helps reduce what the merchant has to secure directly.

What still stays with the merchant

Using a partner doesn't eliminate PCI obligations entirely. Merchants still need to think about:

That distinction matters. Outsourcing payment processing is not the same as outsourcing security judgment. You still need to know where payment data goes, what your staff can access, and which systems could affect the payment environment.

The good news is that this model usually aligns with how startups should build anyway. Keep sensitive card handling out of your stack, keep the boundary narrow, and make your audit about a small, well-defined environment instead of your whole company.

If you're building a global checkout or subscription flow and want to reduce payment complexity from the start, Suby is worth evaluating. It lets customers pay with cards, while businesses receive USDC, and it also supports card and crypto payments through an API plus native Discord and Telegram integrations for memberships, paid access, and online communities.