You open your inbox and see a dispute notice for a payment you already counted as revenue. The customer got access, your team delivered what was promised, and now the funds are in question anyway. That moment catches a lot of online businesses off guard, especially if you sell subscriptions, digital access, or community memberships where there’s no box, tracking label, or signed delivery slip to point to.

Chargebacks are part of card payments, whether you sell software, paid Discord access, Telegram memberships, consulting, or digital goods. They’re also more confusing in a card-to-USDC flow, because the customer pays by card while your business receives USDC. That doesn’t remove chargeback risk. It changes how you should document transactions, handle customer communication, and organize evidence.

Table of Contents

- What a merchant actually loses

- Why this hits online businesses harder

- Why card-to-USDC businesses need a different mindset

- Who is involved

- The two-cycle flow in plain English

- What representment actually means

- Why timing changes the outcome

- Start with the customer confusion layer

- Build checkout copy for disputes, not just conversions

- Use refunds strategically

- Prevention checklist for digital merchants

- Step one, classify the dispute before you react

- Step two, gather evidence that matches the reason code

- Step three, write a rebuttal letter that sounds factual

- Step four, make the accept-or-fight decision like an operator

- Step five, improve the next case while closing the current one

- What to automate first

- Why hybrid card-to-USDC systems need evidence-aware workflows

- Connect dispute events to the rest of your stack

What a Chargeback Is and Why It Matters

A chargeback is not a refund. A refund is something you choose to issue. A chargeback is a forced reversal started by the cardholder through their bank.

That difference matters because a refund usually ends the issue. A chargeback starts a formal dispute process and puts your payment operations under scrutiny. If you ignore it, or respond badly, you can lose the transaction, absorb extra costs, and damage your standing with your payment partners.

What a merchant actually loses

The obvious loss is the disputed sale. The less obvious damage is operational.

You lose staff time. You lose focus. You often lose the chance to resolve the issue directly with the customer. If chargebacks keep piling up, your processor or acquiring partners can decide your business is too risky.

The scale of the problem is already large and still growing. Global chargeback volumes are projected to rise from 238 million in 2023 to 337 million by 2026, a 41% increase. In 2023 alone, disputes totaled over $65.2 billion worldwide, and card-not-present eCommerce chargeback rates averaged between 0.6% and 1%, close to the 1% level that can trigger account termination, according to chargeback statistics compiled by Chargebacks911.

Practical rule: Treat every chargeback as both a lost-revenue event and a process failure signal. Even when the customer is wrong, something in the payment, descriptor, checkout, or post-sale experience may have made the dispute easier to file.

Why this hits online businesses harder

Card-not-present merchants operate in an environment where customers can dispute with a few taps. That’s especially true for businesses selling digital access, subscriptions, one-click paylinks, and international services.

Common patterns I see in disputes are simple. The customer didn’t recognize the descriptor. They forgot they subscribed. They expected instant support. They paid for access and later claimed they never received anything because there was no physical shipment. Those are prevention problems before they become dispute problems.

If you’re still tightening up checkout language, billing clarity, or access delivery, start with the basics of accepting credit card payments clearly and cleanly. Most avoidable chargebacks begin there.

Why card-to-USDC businesses need a different mindset

When a customer pays by card and your business receives USDC, the card side still follows card-network dispute rules. The settlement side is different, but the chargeback risk still begins with the card payment.

That means your operating model needs two things at once:

- Customer-facing clarity so fewer buyers feel confused enough to dispute

- Merchant-side evidence discipline so you can prove what was purchased, when access was granted, and what happened after payment

Businesses that understand that early usually handle chargebacks far better than businesses that assume digital delivery is too hard to defend.

The Chargeback Process Explained

Most merchants first encounter chargebacks as a notification. By then, the process is already moving. The customer has contacted their bank, the issuer has opened a dispute, and the case is no longer a simple support ticket.

The legal roots of this system go back decades. The Fair Credit Billing Act of 1974 created the framework for modern chargebacks, giving consumers 60 days to dispute charges and requiring issuers to investigate within 90 days, as outlined in this history of chargebacks.

Who is involved

A chargeback has several moving parties:

| Party | Role in the dispute |

|---|---|

| Cardholder | Questions or challenges the payment |

| Issuing bank | Reviews the customer claim and initiates the dispute |

| Card network | Applies network rules and may handle escalation |

| Acquiring bank | Receives the dispute on the merchant side |

| Merchant | Accepts the loss or submits evidence to fight it |

If you think of chargebacks like a structured review process, the issuer is hearing the complaint first, and your side only gets heard once the case reaches you through the acquirer.

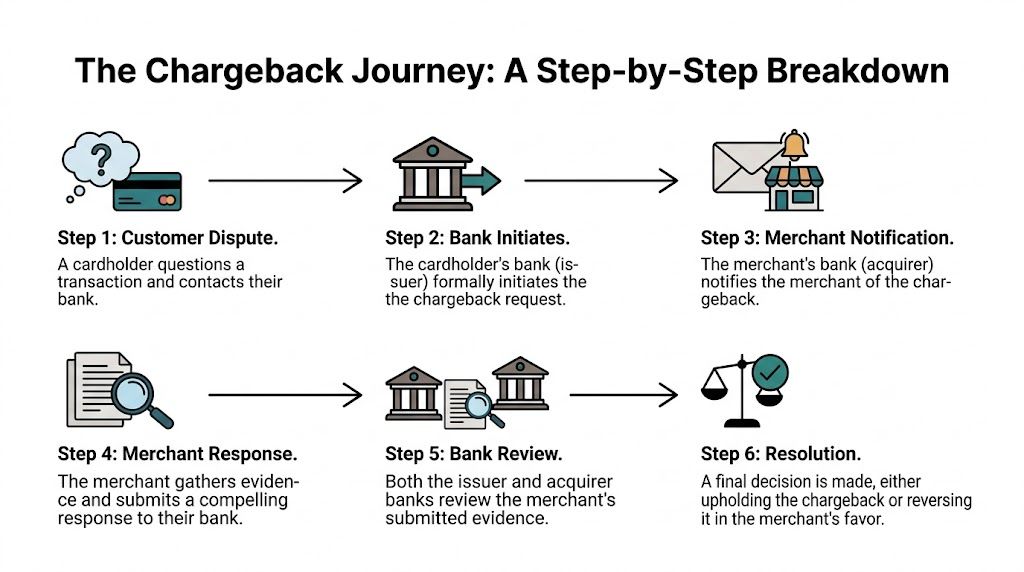

The two-cycle flow in plain English

A lot of merchants assume a chargeback is one event. In practice, it works more like a staged process.

First, the disputed funds are pulled back through the banking chain. Then you decide whether to accept that outcome or challenge it with evidence. In Mastercard’s structure, this operates as a two-cycle process, where the first chargeback opens the case and the second presentment is your formal response. Stripe gives a useful overview of that two-cycle chargeback flow.

Here’s the merchant-side sequence that matters most:

- The customer disputes the payment with their bank.

- The issuer initiates the chargeback if the claim fits a dispute category.

- Your acquirer notifies you that funds are being challenged.

- You choose a path. Accept the chargeback, or fight it.

- If you fight it, you submit representment, which means you present the transaction again with evidence.

- The issuer makes a decision after reviewing your package.

- In some cases, the dispute can escalate further through network procedures.

Accepting a chargeback is not a neutral administrative choice. Operationally, it’s close to letting the customer keep the refund and the dispute count.

What representment actually means

Representment is your formal rebuttal. You’re saying the original transaction was valid, the customer received what was sold, and the dispute should be reversed.

A strong package usually includes a rebuttal letter plus records that fit the reason for the dispute. For digital businesses, that might mean checkout confirmation, access logs, customer messages, proof of account creation, support history, and evidence that the buyer used the service after purchase.

Weak representment usually fails for one of three reasons:

- The evidence doesn’t match the dispute reason

- The timeline is incomplete

- The merchant submits too late

Why timing changes the outcome

Chargeback evidence has a shelf life. If you wait while your team debates what happened, the deadline can pass before you even organize the file.

That’s why mature payment ops teams don’t treat chargebacks like ad hoc support tickets. They treat them like timed cases. The businesses that win more often are usually not the businesses with the best story. They’re the ones with the cleanest records and the fastest response motion.

Proactive Chargeback Prevention Strategies

Most chargeback reduction work happens before any dispute is filed. Once the issuer opens the case, your options narrow fast. Prevention is cheaper, cleaner, and usually more effective than trying to rescue a weak transaction after the fact.

Start with the customer confusion layer

For internet-native businesses selling subscriptions or digital access through Discord and Telegram, customer confusion is a rising cause of chargebacks, and these friendly-fraud disputes can be reduced with clear service terms at checkout and strong customer authentication, according to Chargebacks911’s review of chargeback risk factors.

That tracks with what operators see every day. People dispute recurring charges they forgot about. They dispute digital access they expected to work differently. They dispute community payments because they don’t understand whether they bought a one-time product, a recurring membership, or gated access.

The easiest prevention wins usually look boring:

- Use a recognizable billing identity so customers know who charged them

- State exactly what the buyer gets at checkout, not after payment

- Show renewal terms before purchase for recurring plans

- Send immediate confirmation messages with access details and support contact info

If your business is already seeing avoidable disputes, this guide on how to avoid payment disputes is a useful practical companion.

Build checkout copy for disputes, not just conversions

A checkout that converts but creates confusion later is expensive. This is common with paylinks, creator products, digital memberships, and subscription plans sold in chat-based communities.

Write for the future dispute reviewer as well as the buyer. A clean product label and a plain-English service description do more defensive work than most merchants realize.

For example, these details help:

- Access terms instead of vague benefit language

- Renewal wording placed before payment confirmation

- Delivery method explained as account access, role assignment, invite, or subscription activation

- Support route visible before and after payment

A customer who understands the purchase is more likely to request help. A customer who feels surprised is more likely to go to the bank.

A broader operational playbook for managing high chargeback rates is worth reviewing if your disputes are not isolated and are starting to reflect process issues across support, billing, and fraud controls.

Use refunds strategically

Some merchants treat refunds as failure. In payment operations, a timely refund is often a cheaper outcome than a chargeback.

If a customer is unhappy but reachable, resolve it directly. Waiting for the dispute often turns a manageable support issue into a formal payment problem. That is especially true when the complaint is based on misunderstanding rather than true fraud.

A useful mindset is simple:

- Refund valid complaints fast

- Challenge invalid disputes with evidence

- Don’t let indecision push cases into the wrong bucket

This is a good point to review the mechanics visually:

Prevention checklist for digital merchants

Here’s the prevention stack I’d want in place for any business selling access, subscriptions, or online services:

- Descriptor clarity: Make sure the card statement name matches what customers know.

- Access logs: Keep records of login, activation, role assignment, or service usage.

- Support visibility: Put a real contact path in receipts, portals, and onboarding emails.

- Policy alignment: Match refund terms, cancellation terms, and delivery wording across checkout and support.

- Authentication controls: Use strong customer authentication where available.

- Internal tagging: Flag first-payment disputes, recurring disputes, and duplicate complaint patterns separately.

Merchants that skip this groundwork usually end up trying to win disputes with screenshots and guesswork. That rarely holds up.

How to Respond to a Chargeback in Suby

When a chargeback lands, speed matters more than most merchants expect. You typically have a 10 to 45 day representment window from notification, depending on the card network, and missing that deadline means an automatic loss no matter how strong your evidence is, as explained in Chargeflow’s chargeback life cycle overview.

That’s why the first rule is simple. Don’t start by arguing about whether the customer is right. Start by securing the timeline, the records, and the deadline.

Step one, classify the dispute before you react

Not every chargeback should be fought.

If the transaction was true fraud, accepting the dispute is usually the right call. If the customer clearly received the service and your records are strong, representment may be worth the effort. The mistake merchants make is treating all disputes as moral arguments. The banks don’t care who feels offended. They care whether the evidence answers the claim.

Ask these questions first:

- Was the cardholder the buyer?

- Did the customer receive access, service, or delivery?

- Do we have records that directly answer the dispute reason?

- Is the value worth the response effort if evidence is weak?

Step two, gather evidence that matches the reason code

Many responses fall apart because merchants dump every screenshot they can find into a folder and hope volume equals credibility. It doesn’t.

A good evidence file is selective and ordered. Include only documents that make the dispute reviewer’s job easier.

Useful evidence often includes:

- Transaction records showing date, amount, and purchase details

- Checkout records that show what the buyer agreed to

- AVS or CVV records if available through your payment stack

- Proof of delivery or access such as activation, login, role assignment, or usage history

- Customer communication including support emails, chat logs, or confirmation messages

- Refund or cancellation history if the customer contacted you before disputing

For digital access businesses, I’d also include a short event sequence. Payment completed, receipt sent, account activated, user logged in, support conversation opened, cancellation requested, and so on. That sequence often matters more than any single screenshot.

Operator note: If your evidence requires a long spoken explanation, it probably isn’t organized well enough yet.

Step three, write a rebuttal letter that sounds factual

Your rebuttal letter should be short, specific, and unemotional. Don’t accuse the customer of lying unless the evidence makes the point on its own. State what was purchased, when it was delivered, and why the dispute claim is inconsistent with the record.

A simple template works:

To the dispute review team,

We are challenging this chargeback because the transaction was valid and the purchased service was provided as agreed. The customer completed payment on [date], received confirmation immediately, and was granted access to the purchased service thereafter.

Our attached records include the transaction confirmation, service terms presented at checkout, proof of access or usage, and relevant communication with the customer. These documents show that the service was delivered and that the transaction was authorized.

Based on the attached evidence, we request reversal of the chargeback.

Step four, make the accept-or-fight decision like an operator

Discipline matters. A weak case with weak records should not consume hours of team time just because the dispute feels unfair.

Use a simple decision table:

| Situation | Better move |

|---|---|

| True fraud | Accept |

| Merchant mistake | Accept and fix root cause |

| Clear service delivery, strong evidence | Fight |

| Ambiguous facts, poor records | Usually accept, then tighten process |

| Repeat customer abuse pattern with proof | Fight if documentation is clean |

Step five, improve the next case while closing the current one

Every dispute should produce an operational note. Not a vague note, a usable one.

Examples:

- Billing descriptor caused confusion

- Customer support reply took too long

- Access proof existed but was hard to export

- Cancellation terms were visible, but not prominent enough

- Staff saved screenshots but not timestamps

That loop matters because winning one chargeback doesn’t fix the system. It just resolves one file.

Using Suby's API and Webhooks for Automation

Manual dispute handling breaks down once volume grows. Even a small increase in transactions can create enough operational noise that deadlines get missed, evidence gets scattered, and customer access isn’t updated consistently after a dispute appears.

That’s where automation starts paying off. Suby provides an API that lets businesses accept payments by card or crypto, with merchants receiving USDC, and it also offers native Discord and Telegram integrations for subscriptions, paid access, and online communities. For teams building custom workflows, the payment gateway API integration guide is the right starting point.

What to automate first

The first goal is not full dispute intelligence. The first goal is removing human lag.

Good first automations include:

- Create an internal ticket when a dispute event appears

- Tag the customer account so support sees the payment issue immediately

- Pause access review for recurring digital services where your policy requires it

- Request evidence automatically from support, billing, and product logs

- Push the deadline into your operations queue with reminders

That kind of workflow prevents the common failure mode where a chargeback notice sits in one inbox until the deadline is gone.

Why hybrid card-to-USDC systems need evidence-aware workflows

In hybrid card-crypto systems, card disputes still run through PCI-DSS certified partners, but blockchain records tied to USDC settlement can provide an immutable layer of proof for some disputes, as noted in Payscout’s discussion of chargebacks in hybrid payment flows.

That doesn’t mean every chargeback becomes easy to win. It means your dispute workflows can combine card-side records with settlement-side records in a way traditional merchants often don’t. If the dispute concerns whether value moved through the system, immutable settlement records can support the timeline.

Automation works best when it gathers evidence before a human asks for it. The more your system captures by default, the less you depend on memory during a dispute.

Connect dispute events to the rest of your stack

A practical setup usually links dispute alerts to support, access control, and your internal finance records.

For example, if your business also uses external billing or ops tools, it can help to review how those systems exchange payment context. If your broader stack includes card-processing tools elsewhere, a technical reference like Spur’s Stripe integration overview can be useful for thinking through how event-driven payment integrations are structured, even if your chargeback workflow lives elsewhere.

The main principle is simple. Don’t let dispute handling live in a silo. Connect it to support, access, and recordkeeping so every team sees the same payment reality.

Tracking Your Metrics and Final Takeaways

Most merchants focus on winning the latest chargeback. That’s understandable, but it’s not how payment risk is controlled. What matters more is whether your overall dispute pattern is stable, improving, or getting worse.

The metric to watch is your chargeback ratio. At a practical level, that means disputes relative to your transaction volume. If that number rises, your processing risk rises with it. Earlier in this guide, the industry benchmark we cited showed how close many card-not-present businesses already operate to the 1% risk line.

Use a simple operating loop

The healthiest chargeback programs run on three actions:

- Prevent: Reduce confusion, tighten checkout language, improve support, and document service delivery better.

- Respond: Handle valid cases fast, fight defensible cases with focused evidence, and never miss representment deadlines.

- Analyze: Review every dispute for root cause, then change the underlying process.

This sounds basic because it is basic. Most chargeback problems come from inconsistency, not complexity.

What to track every month

You don’t need a huge analytics project to get useful control. Start with a short operating list:

| Metric | Why it matters |

|---|---|

| Chargeback count | Shows raw dispute pressure |

| Chargeback ratio | Shows whether disputes are becoming a processor risk |

| Top dispute reasons | Reveals whether confusion, fraud, or service issues drive losses |

| Response time | Tells you if your team can act inside representment windows |

| Win versus accept pattern | Helps you see where evidence is strong and where it is not |

A lot of merchants make the mistake of treating all disputes as “fraud.” That obscures the underlying problem. Sometimes the root cause is billing recognition. Sometimes it’s subscription communication. Sometimes it’s a weak delivery record for digital access.

Final view from an operator’s seat

Chargebacks are not just a payments problem. They sit at the intersection of checkout design, customer support, fraud controls, subscription management, and evidence collection.

If you sell online and users pay with cards while your business receives USDC, the right question isn’t whether chargebacks apply to you. They do. The useful question is whether your operation is built to prevent the avoidable ones and respond correctly to the rest.

If you want a payment setup where customers can pay by card or crypto while your business receives USDC, Suby provides an API, paylinks, embedded checkout, webhooks, and native Discord and Telegram integrations for subscriptions, paid access, and online communities.