Monday starts with a message from your acquirer, and it's not subtle. Your card-not-present dispute performance is getting close to a threshold that now matters more than it used to. The old habit of treating fraud, customer disputes, and odd authorization noise as separate operational queues doesn't hold up anymore.

That's the core change behind the Visa Acquirer Monitoring Program. For payment teams, this isn't just a compliance rename. It changes what counts, how portfolio risk is judged, and how quickly a merchant issue can become an acquirer problem, then come back downstream as fees, remediation pressure, or account risk.

Organizations typically don't need another abstract compliance summary. They need a working view of what the Visa Acquirer Monitoring Program means inside the day-to-day stack, from monitoring and dispute ops to data capture and developer workflows. If you're also reviewing adjacent card controls, this overview of PCI DSS for UK IT providers is a useful companion because the operational discipline overlaps more than is commonly understood.

Table of Contents

- Introduction The New Rules of Payment Health

- Why Visa changed the model

- What VAMP means in day-to-day operations

- What payment teams should take from this definition

- The ratio your team has to watch

- What to monitor every week

- The threshold view that matters operationally

- Does enumeration fraud affect the ratio even if sales were declined

- How does the grace period actually reset

- What should a Head of Payments do first after a warning

Introduction The New Rules of Payment Health

A lot of merchants will meet VAMP in a very ordinary way. Not through a policy memo, but through a warning, an acquirer call, or a monthly review where one line suddenly starts getting executive attention.

The problem is that many teams still organize their work the old way. Fraud ops watches fraud. Chargeback ops watches disputes. Engineering watches auth performance. Customer support watches complaints. Under VAMP, those silos break down quickly because payment health is judged more holistically, and the cost of weak coordination shows up faster.

Practical rule: If your fraud team, dispute team, and developers aren't looking at the same operational signals each week, you're already behind the workflow VAMP expects.

That's why the right response isn't panic. It's instrumentation, shared ownership, and faster feedback loops between the acquirer-facing team and the people who control checkout, billing descriptors, fulfillment, and evidence collection.

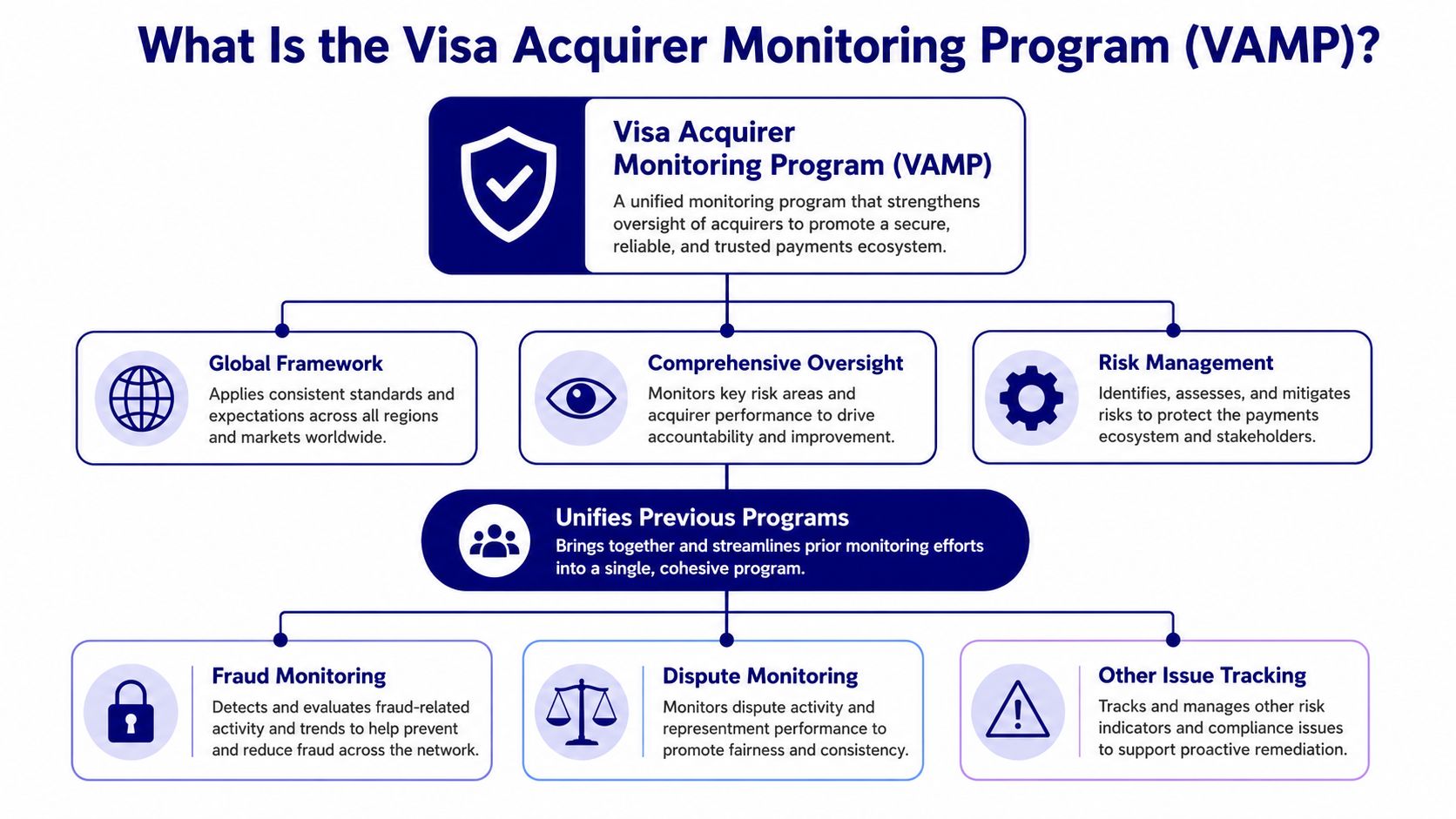

What Is the Visa Acquirer Monitoring Program

A payment team usually realizes what VAMP is when routine work starts to change. The fraud analyst asks for dispute reason code detail earlier in the month. The developer gets a ticket to tighten descriptor formatting. The acquirer contact wants one remediation plan instead of separate updates from fraud, chargebacks, and support.

That shift is the point of the Visa Acquirer Monitoring Program. VAMP is Visa's combined monitoring framework for portfolio risk. It pulls fraud and certain dispute signals into one program so acquirers can judge merchant risk in one operating model instead of across several disconnected ones.

Why Visa changed the model

Under the older setup, a merchant could look acceptable in one monitoring lane and weak in another. That created slow diagnosis and messy ownership. One team would treat fraud as the main problem, another would focus on service disputes, and engineering would often hear about both too late to fix the root cause in the same cycle.

VAMP changes the workflow. Acquirers now need a clearer view of risk across the merchant portfolio, and merchants need tighter coordination across fraud controls, customer experience, fulfillment, and dispute operations.

For Heads of Payments, the trade-off is straightforward. A single framework gives less room to explain away one bad metric as someone else's problem. It also gives teams a better chance to catch linked issues early, before they turn into acquirer escalation.

What VAMP means in day-to-day operations

At the merchant level, VAMP matters because it changes how work gets prioritized.

Fraud-related disputes and eligible non-fraud disputes are no longer treated as separate management conversations. They affect the same monitoring picture. If a billing descriptor is unclear, customer support is slow, or cancellation flows are hard to find, those are no longer “just CX issues.” They can increase the same risk pressure your acquirer is already watching.

That forces a more disciplined weekly operating rhythm:

- Fraud ops needs to review fraud signals alongside incoming dispute trends, not in isolation.

- Chargeback teams need faster tagging of preventable disputes so patterns reach product and engineering before month-end.

- Developers need event-level visibility into checkout failures, recurring billing logic, refunds, and descriptor behavior.

- Customer support and fulfillment need clear escalation paths because shipping delays, unclear renewals, and slow refunds often become payment risk issues.

Teams that already run a shared review across fraud, disputes, and checkout data adapt faster. If your team does not have that cadence yet, start with a payment fraud prevention workflow that ties risk signals to operational owners.

What payment teams should take from this definition

VAMP is not just a Visa policy label. It is an operating constraint.

It tells acquirers to judge merchant risk in one connected way, and it pushes merchants to do the same internally. The practical question is no longer, “Which team owns this issue?” The better question is, “Could this issue raise fraud counts, increase disputes, or weaken our acquirer standing if we leave it alone for another billing cycle?”

Use this short checklist to confirm your team understands VAMP in practical terms:

- One owner: Assign a single person to consolidate fraud, dispute, and acquirer reporting.

- One weekly review: Put fraud ops, disputes, support, and engineering in the same meeting with the same numbers.

- One issue log: Track descriptor problems, refund delays, fulfillment failures, and recurring billing complaints in the same queue as payment risk items.

- One escalation rule: Define when a negative trend triggers developer work, acquirer communication, or executive review.

That is the working definition that matters. VAMP changes what your acquirer measures, but the bigger impact is how your internal teams have to operate every week.

Understanding VAMP Triggers and Thresholds

A common failure pattern looks like this. The risk team watches fraud alerts, the disputes team watches chargebacks, engineering watches authorization and settlement logs, and nobody recalculates VAMP exposure until the acquirer asks questions. By then, the fix is slower and more expensive because the underlying issue usually started weeks earlier in checkout, billing, fulfillment, or support.

The practical job is to convert VAMP into a short set of operating metrics your team reviews every week. If your reporting only arrives through acquirer notices, you are already late.

The ratio your team has to watch

At a high level, VAMP ties together fraud cases, eligible disputes, and settled transaction volume into one monitored ratio. Your team does not need to memorize policy language. Your team does need a reliable internal version of that calculation, built from the same source systems your acquirer will expect you to explain.

That changes day-to-day work for both payments teams and developers. Fraud prevention alone will not keep the number down if preventable non-fraud disputes keep rising because of weak descriptors, delayed refunds, unclear trial terms, duplicate billing, or poor delivery communication.

For many online merchants, volume is high enough that this becomes relevant quickly rather than staying a theoretical program rule.

If your current setup still treats fraud and disputes as separate queues, fix that first with a payment fraud prevention workflow that connects fraud signals, dispute drivers, and team ownership.

What to monitor every week

The teams that stay out of trouble usually review the same five inputs every week, in the same order:

- Settled Visa transaction count: Use settled volume, not just authorized volume, and make sure partial captures and late captures are handled consistently.

- Fraud case inflow: Pull card-not-present fraud signals into the same dashboard as disputes so the trend is visible before it hits monthly reporting.

- Eligible dispute count: Break this down by root cause, not only by reason code. “Product not received” and “credit not processed” need different owners.

- Refund timing: Track time from customer request to refund submission. Slow refunds often become avoidable disputes.

- Descriptor and billing-change defects: Any release that affects statement descriptors, recurring billing logic, trial conversion, or invoice timing should be tagged as VAMP-relevant.

Weak reporting proves detrimental. A team can have acceptable fraud controls and still lose ground because its dispute data is late, incomplete, or impossible to reconcile across PSP, CRM, and support systems. The operational cost of that problem is well described by digna on data quality in finance.

The threshold view that matters operationally

Thresholds matter because they change how much scrutiny a merchant creates for the acquirer and how quickly patience runs out. The exact policy details should come from your acquirer and current Visa documentation, but the working model is straightforward. There is a warning band where performance is already poor enough to trigger concern, and there is a higher-risk point where a merchant can become a direct portfolio problem.

Keep a table like this in your weekly review pack.

| Operating view | What your team should assume | Internal response |

|---|---|---|

| Early warning range | Your dispute and fraud mix is trending in the wrong direction, even if revenue still looks healthy | Freeze risky checkout or billing tests, review top dispute drivers, and confirm refund SLAs are being met |

| Acquirer concern range | Your merchant profile can start affecting acquirer confidence and underwriting posture | Prepare a written remediation plan, tighten release approvals for billing and descriptor changes, and increase weekly reporting cadence |

| Merchant-level excessive risk | The account may face formal remediation pressure and, if unresolved, a path toward termination | Assign an executive owner, move engineering fixes to the current sprint, and send your acquirer dated progress updates |

Two trade-offs matter in practice.

Approval rate versus downstream dispute quality

A retry rule, softer risk policy, or more aggressive subscription recovery flow can raise short-term captured volume. It can also create more customer confusion, more “I did not recognize this” claims, and more refunds requested after settlement. Teams should test approval changes together with dispute-rate impact, not in isolation.

Growth experiments versus evidence quality

Faster checkout often removes fields and friction. That can help conversion, but it can also reduce order clarity, weaken proof of customer consent, or make support history harder to assemble. If developers ship a checkout update, they should also confirm what evidence will still be available if disputes rise next month.

Use this release checklist for any change that touches payments, recurring billing, or post-purchase communication:

- Confirm the statement descriptor is unchanged, or document the change and customer communication plan.

- Verify trial terms, renewal dates, and cancellation steps are visible in the checkout and customer emails.

- Check that refund webhooks, support tickets, and order events can be tied to the same transaction ID.

- Confirm dispute and fraud exports still map correctly after any schema or API version change.

- Require sign-off from payments ops before releasing retry logic, account updater rules, or billing scheduler changes.

One simple decision rule helps. If a change can raise conversion while making customer recognition, refund handling, or evidence collection worse, treat it as a VAMP risk review item before it ships.

The Consequences of VAMP Enrollment

Monday starts with a ratio review. By Friday, the issue has spread into finance, support, engineering, and the acquirer call queue. That is what VAMP enrollment does in practice. It turns a payment metric into an operating problem with daily deadlines and real revenue risk.

Why the financial hit arrives fast

The direct cost is only the first layer. Card network assessments and acquirer pressure can show up quickly, but the bigger hit usually comes from lower approval quality, higher support workload, more refunds, and slower growth decisions while the team is under review.

For lower-margin businesses, that hurts immediately. A subscription merchant may still be growing top-line volume while losing contribution margin on the same transactions that created the dispute problem. A marketplace may find that one seller cohort is driving the issue, but the reporting is too weak to isolate it fast enough. By the time leadership sees the full picture, VAMP has already become a pricing, reserve, and underwriting discussion.

Data quality decides how expensive this gets. If the dispute team cannot match order events, refund timestamps, customer messages, and payment IDs without manual work, every remediation step takes longer and every acquirer update looks less credible. This piece from digna on data quality in finance is worth reading because weak data hygiene becomes a direct cost center under VAMP.

The day-to-day workload changes fast

Enrollment changes the operating rhythm for both payments ops and developers. Teams stop working from monthly summaries and start running a tighter weekly, sometimes daily, control cycle.

In practice, that usually means:

- A named owner for acquirer communication: One person needs to coordinate updates, evidence requests, timelines, and internal follow-up.

- A transaction-level root-cause review: Pull samples by product, BIN country, issuer response, billing model, and support outcome. Broad explanations are not enough.

- An evidence assembly workflow: Payment ID, order ID, refund status, shipment or service-delivery proof, customer communication, and descriptor data should be easy to retrieve in one place.

- Developer support for reporting fixes: If your PSP, CRM, support desk, and subscription system do not share stable identifiers, engineering usually has to patch the gaps before the next review cycle.

- A fallback processing plan: If the acquirer loses confidence, leadership needs a realistic backup path for card acceptance and cash-flow continuity.

The developer piece is often missed. VAMP remediation is rarely just policy work. It often requires API and data-pipeline changes, such as storing more complete authorization responses, preserving webhook event history, versioning dispute reason mappings, or fixing how refunds and cancellations are written back to the ledger. If those details are messy, the payments team spends its time reconciling exports instead of reducing disputes.

I have seen teams lose two weeks just figuring out which system held the final truth for a canceled subscription. That delay matters. Acquirers expect a plan, but they also expect proof that the merchant can measure whether the plan is working.

A short operating checklist helps here:

- Confirm who sends acquirer updates and how often.

- Build one exception report that ties disputes, fraud signals, refunds, and support contacts to the same transaction reference.

- Require engineering review for any missing fields that block evidence production.

- Separate merchant, product, or geography cohorts so the team can isolate the source of deterioration.

- Document a processor contingency path, including account contacts, reserve exposure, and migration dependencies.

If performance stays weak, the commercial risk gets bigger than program fees. Acquirers can tighten terms, hold more funds, restrict volume growth, or decide the account is no longer worth the oversight burden. For a practical view of that downside, Suby's article on what happens when a payments account gets restricted or shut down is useful background.

Once that trust breaks, the question is no longer whether the team understands its ratio. The question is whether the business can keep stable access to card acceptance.

Your Action Plan for VAMP Prevention and Remediation

Monday morning, the Head of Payments sees dispute counts rising, support says refund complaints are up, and engineering is already tied up with release work. That is how VAMP problems usually show up in practice. Not as a policy issue, but as an operating issue with real financial exposure and too many teams touching the same transaction from different systems.

The teams that stay out of trouble treat VAMP as a workflow problem. Payment ops needs one review rhythm. Support needs clean escalation rules. Developers need to know which fields must be captured at authorization, at checkout, and after fulfillment so the dispute team is not rebuilding evidence by hand later.

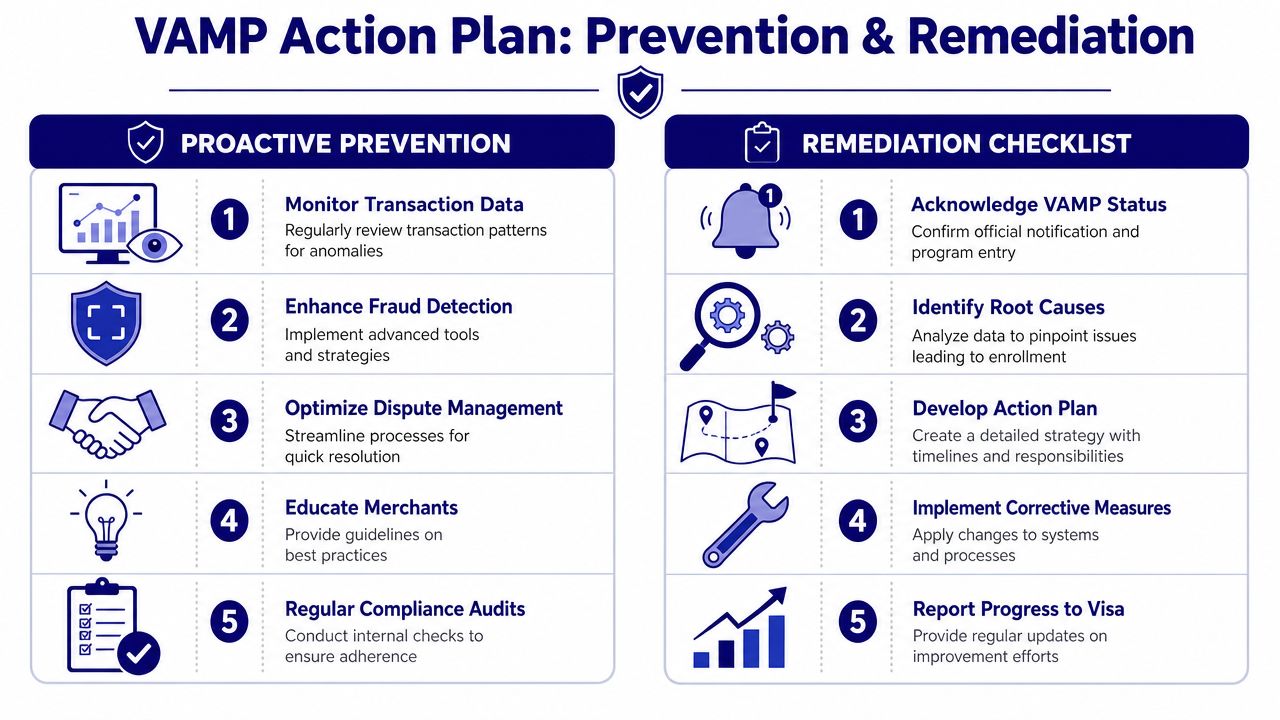

Prevention workflow for payment teams

Prevention starts with one rule. Review payment health as a connected system, not as separate fraud, chargeback, and support queues.

Use this operating checklist:

- Monitor one shared ratio view: Put fraud disputes, non-fraud disputes, refund patterns, and authorization performance into the same report. If different managers own each stream, payment ops still needs one source of truth.

- Flag early transaction anomalies: Watch for approval-rate swings, bursts of soft declines, unusual retries, card testing patterns, and sudden changes in issuer response codes. Those signals often appear before disputes accumulate.

- Apply frontline controls consistently: AVS, CVV checks, velocity rules, and device fingerprinting only help if teams enforce them by segment and review override logic regularly.

- Set internal alert bands before acquirer escalation: A practical trigger is an internal warning when a merchant, product, or geography starts getting close to the limit. Waiting for the formal notice wastes time you could have used to cut exposure.

- Segment performance aggressively: Break out results by MID, traffic source, subscription plan, geography, product line, and descriptor. Blended reporting hides the cohort that is driving deterioration.

- Define field ownership in the API flow: Payment, fraud, and dispute teams should know who owns device data, IP capture, customer identifiers, retry metadata, refund timestamps, and delivery confirmation events.

For teams building their own oversight stack, Suby's guide to real-time transaction monitoring workflows for payments teams is a useful reference for alert design and review queues.

One practical mistake shows up often. Ops teams ask for better monitoring after ratios move, but developers never got a clear schema for the data needed to investigate the problem. If the event model does not reliably connect auth attempts, customer actions, support contacts, and dispute outcomes, the review process becomes slow and subjective.

Remediation workflow when ratios start moving the wrong way

Once performance starts slipping, shorten the decision cycle. Daily review beats weekly summary reports here.

A workable response sequence looks like this:

Pause avoidable risk

Stop experiments that can distort payment behavior. That includes checkout copy tests, aggressive retry logic, new affiliate traffic, fulfillment promise changes, or billing rule changes that make root-cause analysis harder.

Build a dispute driver map

Group cases by product, issuer, descriptor, customer complaint, support contact timing, refund timing, and fulfillment status. Reason codes matter, but they rarely tell the full story on their own.

Fix customer-facing confusion first

Clear descriptors, better receipts, visible cancellation paths, accurate delivery windows, and well-timed subscription reminders can reduce non-fraud disputes faster than many fraud-rule changes.

Audit evidence inputs at the data layer

As noted earlier from Inovio's VAMP guidance, merchants should use proactive fraud controls, set internal alerts before formal escalation, and prepare CE3.0 support by reliably capturing data such as device identifiers, IP information, and enough transaction history to support representment. The operational point is simple. If those fields are optional in your checkout or payment API flow, evidence quality will be inconsistent.

Assign one owner for corrective actions

Someone needs authority to coordinate payment ops, support, fraud, and engineering. Shared accountability usually turns into delayed action.

Log every rule change and result

Record when controls changed, which cohort was affected, what hypothesis the team was testing, and what happened to disputes, refunds, approvals, and support contacts afterward. Acquirers care about whether the merchant can show a controlled response, not just whether the team held a meeting.

For developers, the remediation checklist is usually more specific than the policy memo suggests:

- Confirm device, IP, account, and order identifiers are stored in a retrievable format.

- Make sure retry attempts share a transaction lineage the dispute team can follow.

- Write refund, cancellation, shipment, and access events back to the same record.

- Preserve descriptor, MCC, merchant entity, and processor response data.

- Test whether evidence can be exported without manual spreadsheet joins.

What fails in practice is predictable:

- Vague statements that fraud rules were tightened

- Separate narratives from support, risk, and payment ops

- No cohort-level analysis

- Evidence fields that exist in theory but are missing in production

- Waiting for the next monthly acquirer update before checking whether changes worked

The better model is operationally boring, which is exactly the point. One dashboard. One incident owner. One evidence standard. One weekly review with engineering until the trend stabilizes.

How a Modern Payment Partner Simplifies VAMP Compliance

Manual VAMP operations break down in predictable places. Teams lose time reconciling data across gateways, support tools, subscription systems, and dispute platforms. Developers then get pulled into evidence requests long after the original event, when logs are harder to trust and context is missing.

That's why infrastructure choice matters more than many merchants assume.

Where infrastructure reduces manual work

A modern setup should give payment teams one operational place to review transactions, disputes, subscriptions, and payout behavior. That doesn't remove VAMP obligations, but it does reduce the friction that causes missed signals.

Suby is payment infrastructure for the global internet economy. It provides an API that lets businesses accept payments by card or crypto, and it also offers native integrations with Discord and Telegram for use cases like subscriptions, paid access, and online communities. Customers can pay any way they want, and businesses get paid the way they choose.

Suby is one product with four ways to use it:

- Suby Payments is an API-first payment stack to accept cards and crypto through one checkout.

- Suby Crypto is a crypto payment gateway that handles the swap, sponsors the gas, and settles to a non-custodial wallet or to the Suby balance.

- Suby Gating provides paid access for Discord, Telegram, downloads, and courses.

- Suby Invoicing lets the client pay how they want while the business receives what it wants.

For VAMP-sensitive merchants, the useful point is operational consistency. Fewer disconnected systems generally means cleaner reporting, faster issue isolation, and better evidence handling.

What developers should expect from the API layer

Suby.fi's Merchant API is designed to accept both credit and debit card payments and cryptocurrency payments in a single flow, enabling support for 300+ payment methods including Visa, Mastercard, Apple Pay, Cash App, SEPA, USDC, USDT, ETH, and SOL, according to the Suby Merchant API introduction.

That matters because many businesses need optionality at the acceptance layer while still keeping one internal payment workflow. One common pattern is that the customer pays by card and the business receives USDC. That's not the only setup, but it's a practical one for teams managing global settlement preferences.

Pricing depends on the payment method used, so it's better to check Suby pricing for current method-specific details rather than assume one flat rate.

For a closer look at the product flow, this overview is useful:

For developers, the key VAMP question isn't “Does the platform process payments?” It's “Can we get the transaction and event data we need, quickly, in a form our risk and dispute workflows can use?”

Frequently Asked Questions About VAMP

The tricky parts of the Visa Acquirer Monitoring Program usually aren't the headline rules. They're the edge cases that inflate risk without detection while teams think they're still under control.

Does enumeration fraud affect the ratio even if sales were declined

Yes, and this is one of the most misunderstood parts of the program.

Visa counts all enumerated authorization transactions, approved and declined, divided by total CNP authorized transactions, with a monthly minimum of 300,000 enumerated events to trigger the program, according to Visa's explanation of enumeration treatment under VAMP.

That means a merchant can't treat declined card testing or signature-guessing traffic as harmless background noise. For high-volume ecommerce, the operational problem is that authorization abuse can now affect the broader performance picture even if those attempts never become valid sales.

The practical fix is to monitor abnormal authorization patterns with the same seriousness as confirmed fraud. If your fraud tooling focuses only on post-settlement fraud loss, it's incomplete for VAMP.

How does the grace period actually reset

The rollout includes a three-month advisory grace period from April 1 through June 30, 2025, during which acquirers and merchants are tracked without fines so they can understand their VAMP ratio before enforcement begins, according to Visa's VAMP launch webinar summary.

Operationally, teams also need to pay attention to rolling grace mechanics for later identifications. Guidance covered in Merchant Risk Council's discussion of VAMP impact assessment highlights the rolling 12-month logic for first-time offenders and the importance of complete resolution before a later grace window can be treated as a fresh case.

In plain terms, don't assume “we had our warning already” is the same as “we closed the issue properly.” Acquirers and Visa will care whether remediation was completed, not just whether the merchant survived the first notice period.

A grace period is time to fix the operating model. It is not proof that the operating model was fixed.

What should a Head of Payments do first after a warning

Start with ownership and evidence, not debate.

Use a short response list:

- Name one internal owner: VAMP deteriorates when risk, support, finance, and engineering all think someone else is coordinating.

- Pull the last dispute cohorts: Segment by product, channel, fulfillment status, and billing experience.

- Review auth behavior immediately: Enumeration, retries, and unusual decline patterns can distort the picture faster than many teams expect.

- Talk to the acquirer early: Don't wait until you have a perfect remediation pack. Share what you've found, what you're changing, and what timeline is realistic.

- Check data capture before fighting disputes: If device, IP, and transaction history fields are inconsistent, fix the collection process first.

If you do those things quickly, you usually get a clearer answer to the only question that matters in the first few days: is this a localized operating issue, or a sign that your payments stack needs stronger controls across the board?

Suby helps businesses accept payments by card or crypto through one API, with native Discord and Telegram integrations for subscriptions, paid access, and online communities. Customers can pay by card, wallet, bank, or crypto, and the business can choose how to receive funds, whether to a bank account or in stablecoins like USDC. If you want a setup where customers pay any way they want and your business gets paid the way you choose, see Suby.