Cross border e commerce is no longer a side channel for ambitious brands. It is becoming a core share of online retail. The market reached USD 551.23 billion in 2025 and is projected to reach USD 2,006.98 billion by 2034 at a 15.44% CAGR, and cross-border sales are projected to represent 33.7% of all global online retail in 2026 according to Precedence Research's cross-border e-commerce market outlook.

That changes the conversation. The question isn't whether customers will buy across borders. They already do. The question is whether your operation can support international demand without creating margin leaks, payment friction, support overhead, and settlement delays.

Most guides stop at localization, shipping, and currency display. Those matter. But the operational bottleneck I see most often sits deeper in the stack. Businesses can accept more payment methods than ever, yet many still can't manage a unified balance across fiat and crypto flows. That's where cross border e commerce gets hard in practice.

Table of Contents

- Regulatory compliance and logistics

- Payments, fraud, and FX volatility

- Support and fragmented ownership

The Unstoppable Rise of Global Online Shopping

By 2026, cross-border purchases are expected to account for roughly a third of online retail worldwide, as noted earlier. For an operating team, that does not just mean more international demand. It means the business starts behaving like a multi-market payments and treasury operation.

That shift is where many growth plans break. Demand can be global long before finance is ready to collect, convert, hold, and pay out across currencies and digital assets without creating delays, FX leakage, or reconciliation problems.

Cross-border demand is broad, not niche

Cross-border demand now reaches far beyond large marketplaces. SaaS companies, ecommerce brands, digital product sellers, creator businesses, and agencies all have buyers outside their home market. The opportunity is broad, but the operating model has to match it.

A company can win international orders and still lose margin in the payment flow. Card settlement may arrive in one currency, supplier payouts may leave in another, and some customers may prefer to pay in crypto while the finance team still reports in fiat. If those balances sit in separate systems, every transfer creates extra cost, extra delay, or both.

That is why payment architecture matters early. Teams reviewing expansion costs should also look at practical strategies to save on international transfers. Transfer fees affect pricing, payout timing, reserve planning, and market-level profitability.

Expansion starts with operational choices

Currency conversion and international shipping are only the surface layer.

A workable cross-border model usually includes:

- Localized payment acceptance: Customers need payment methods they already trust, whether that means cards, wallets, bank transfers, BNPL, or crypto.

- Unified balance management: Finance needs one view of funds held across fiat and digital assets, with clear rules for conversion, treasury movement, and payouts.

- Clear settlement logic: Each team should know what settles where, in which currency or asset, on what timeline, and with what fees.

- Margin visibility by market: Profit can change quickly once payment method mix, FX spreads, refunds, and payout rail costs are included.

- Shared operational control: Support, finance, and product teams need the same transaction record so disputes, exceptions, and reconciliation do not splinter across tools.

I have seen this repeatedly. International growth often stalls because the company added front-end localization before it built back-end money movement that finance could manage.

The stronger operators treat payments as part of market entry, not a checkout plugin. That usually leads them toward a more integrated electronic commerce payments infrastructure that supports local acceptance while keeping fiat and crypto balances usable inside one financial workflow.

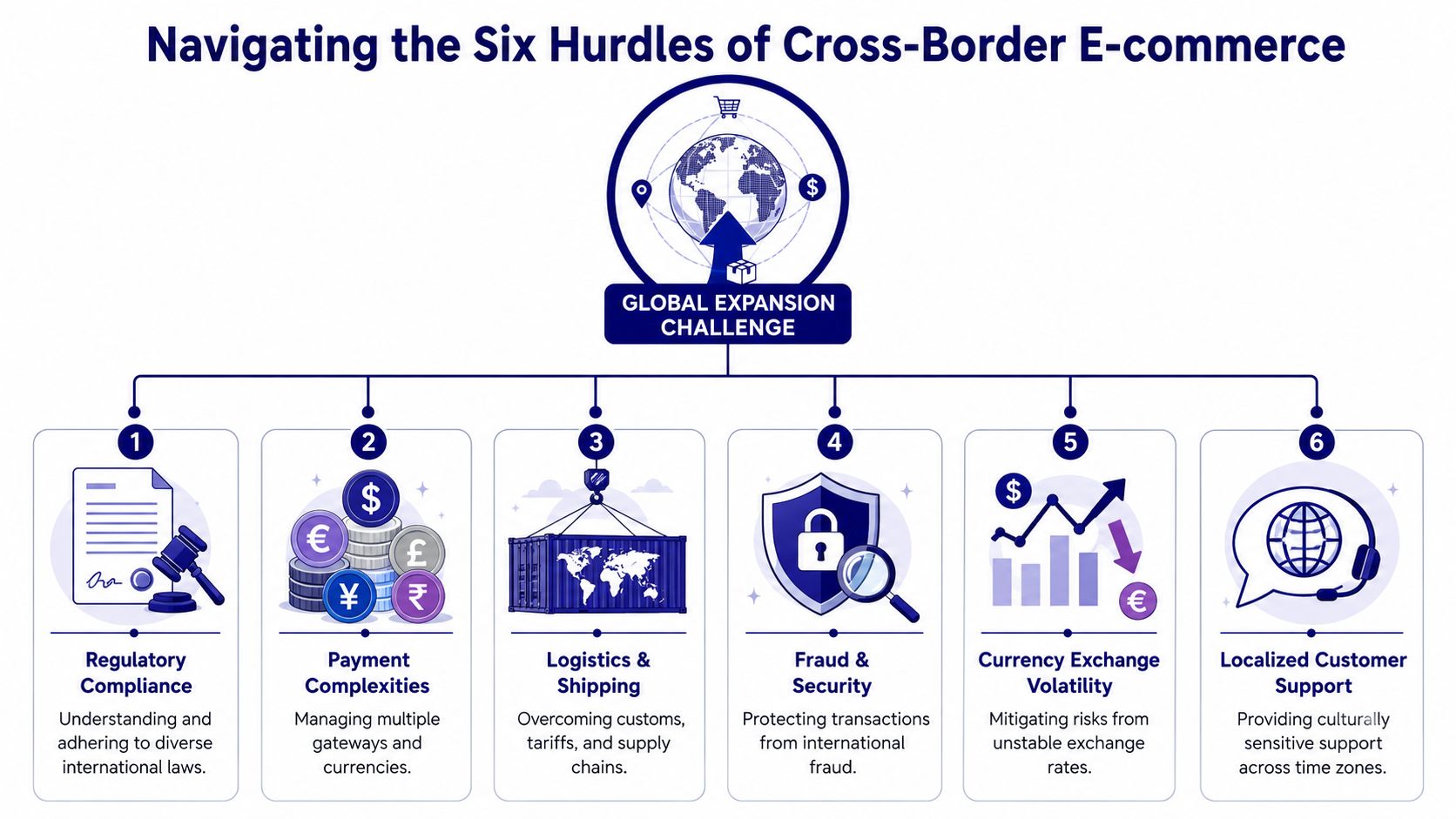

Navigating the Six Hurdles of Cross-Border E-commerce

Global demand is attractive. Global operations are where the work starts.

Regulatory compliance and logistics

The first hurdle is compliance. Every market has its own rules around tax collection, consumer protection, refunds, restricted goods, and data handling. A team can win traffic and still create expensive cleanup if legal review happens after launch.

The second is logistics. Delivery promises, customs handling, duties, returns, and carrier reliability all shape conversion. If checkout says one thing and delivery reality says another, support tickets climb and repeat purchase intent falls.

A simple rule helps here.

Practical rule: Don't enter a new market until finance, legal, operations, and support agree on the same order lifecycle.

Payments, fraud, and FX volatility

The third hurdle is payments. Many international plans become fragile at this point. Cross-border payment infrastructure now needs a provider-agnostic abstraction layer and cloud-native, horizontally scalable processing to handle 300+ global payment methods without code rework as volume grows, as outlined in Corefy's payment infrastructure analysis. In plain terms, hard-coded regional gateways age badly.

The fourth hurdle is fraud and security. International orders carry more variables, more edge cases, and more room for false positives. If your fraud rules are too strict, good customers get blocked. If they're too loose, disputes and losses rise.

The fifth hurdle is currency exchange volatility. Even when customers convert well, FX exposure can subtly eat margin. That matters even more when a business accepts in one currency, stores in another, and pays out in a third.

Here's a quick operating view of the trade-offs:

| Hurdle | What breaks first | What usually works better |

|---|---|---|

| Compliance | Launching before local review | Country-by-country controls |

| Shipping | Generic delivery promises | Market-specific service levels |

| Payments | Multiple disconnected gateways | Unified orchestration layer |

| Fraud | One global risk rule | Market-aware review logic |

| FX | Manual conversions | Predefined settlement policies |

Support and fragmented ownership

The sixth hurdle is localized customer support. Buyers don't only need answers in their language. They need answers in their commercial context. A refund expectation, payment failure explanation, or delivery update often needs local nuance.

Operationally, one more issue sits beneath all six hurdles. Ownership gets fragmented. Marketing owns traffic, product owns checkout, finance owns settlement, and support owns complaints. Nobody owns the full transaction journey.

That's why teams often run into the same processor mistakes repeatedly. If you're auditing your current setup, this breakdown of common pitfalls with global payment processors is useful because most failures come from architecture decisions that looked efficient at the start.

Actionable Strategies for International Growth

You don't need a perfect international operation before expanding. You do need a disciplined one. The businesses that grow cleanly in cross border e commerce adapt their offer, checkout, and payout model to each market instead of forcing one domestic setup everywhere.

Build around local payment behavior

A one-size-fits-all checkout leaves money on the table. Globally, 59% of shoppers buy from retailers outside their home country. About 60% of European consumers use e-wallets for international purchases, and BNPL-assisted cross-border transactions grew by 38% in markets like Brazil and Nigeria, according to this cross-border e-commerce statistics roundup.

That should shape your launch plan immediately.

- Match method to market: If a region leans toward wallets, surface wallets early in the checkout flow. If BNPL is part of buyer behavior, treat it as conversion infrastructure, not an optional add-on.

- Reduce method clutter: More options don't always mean better checkout. Show the methods buyers are most likely to trust in that specific market.

- Align payout logic with payin reality: If your customers pay through a fragmented mix of cards, wallets, and alternative methods, your finance team needs a settlement model that doesn't create balance sprawl.

The checkout that performs best in one country can underperform badly in another, even when the product is identical.

Sequence expansion instead of launching everywhere

International growth gets easier when you stage it. Start with a small set of markets where you can support local expectations well. Learn from payment failures, refund patterns, and support volume, then expand.

A practical sequencing model looks like this:

- Choose markets with operational fit: Don't only chase demand. Pick places where you can support shipping, compliance, and payments cleanly.

- Localize the buying path first: Language, pricing display, payment methods, and support expectations usually matter before brand storytelling does.

- Instrument margin by payment method: Flat assumptions hide real costs. You need to know which payin mix supports profitable scale.

- Review settlement workflows early: Treasury friction becomes visible only after volume arrives, and by then it is harder to rework.

If you're comparing launch frameworks, this guide for international business expansion is worth reading because it pushes teams to think in terms of market readiness, not just market size.

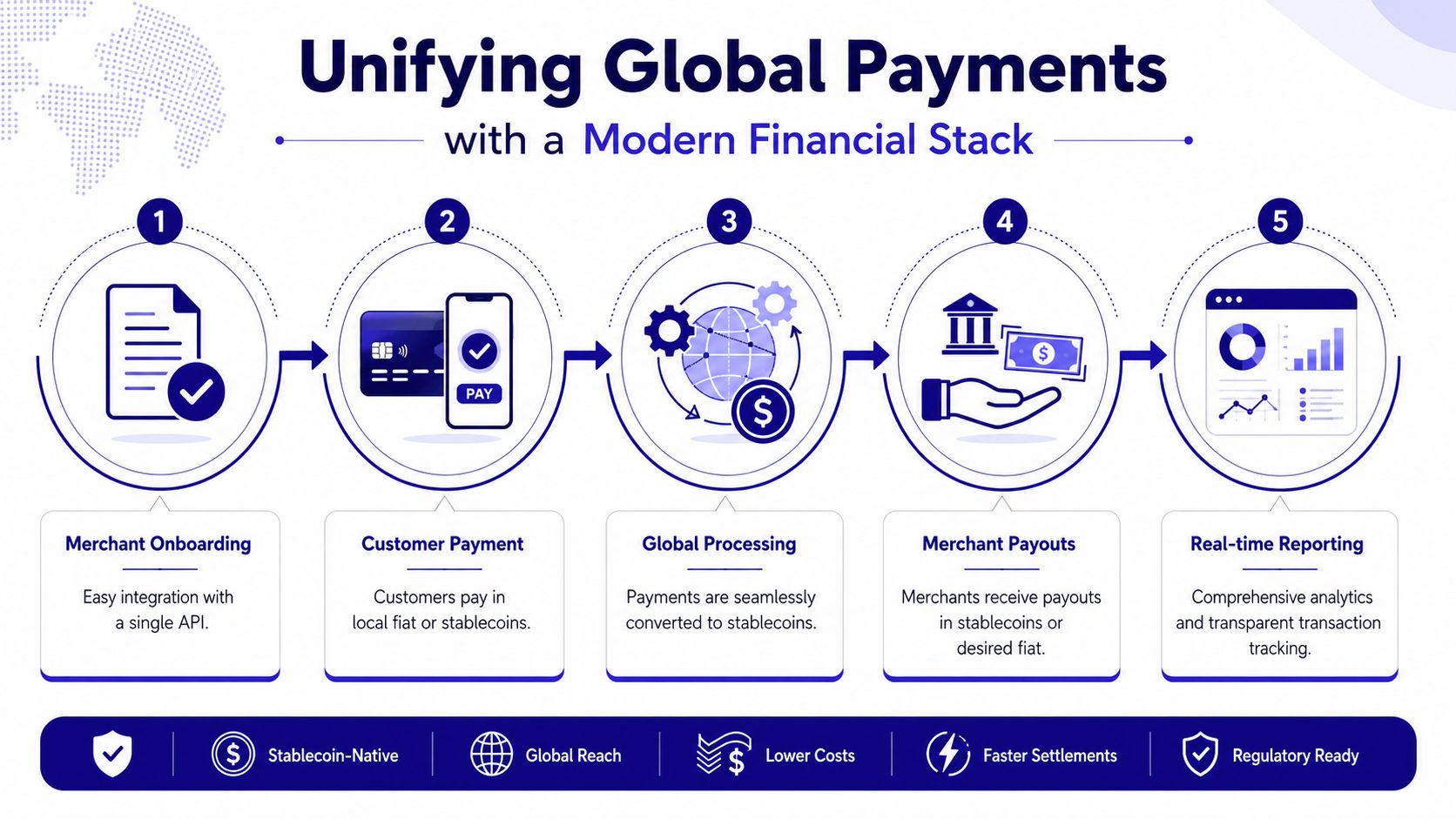

Unifying Global Payments with a Modern Financial Stack

Cross border e commerce usually breaks in finance before it breaks in demand. A business can localize checkout, add the right payment methods, and still lose time and margin once funds start landing in different processor balances, bank accounts, and wallets.

A modern financial stack fixes that by connecting acceptance, conversion, treasury, and payout in one operating layer. A key advantage is not only taking more payment types. It is keeping those payins usable once they arrive.

To make the model concrete, this flow shows what that system should look like in practice.

Why balance fluidity matters

In my experience, the biggest operational gap in cross border e commerce is balance fluidity. Many companies can accept both fiat and crypto. Far fewer can route those payins into one operational balance that supports conversion and payout without manual transfers between systems.

That gap creates extra work fast. Card revenue may sit with one processor, crypto receipts in a separate wallet, and local bank-based methods inside another provider's ledger. Finance then has to reconcile three sources of truth before it can decide what is available to pay suppliers, settle refunds, or move cash into the next market.

The cost is not only accounting effort. Treasury slows down, payout timing becomes harder to control, and conversion fees stack up when funds have to bounce through multiple intermediaries. For marketplace operators and Amazon sellers, Clickstera's advice on Amazon profit margins is a useful reminder that small FX and settlement costs can erode margin once they repeat across countries and payment flows.

A better setup gives the business one place where incoming funds land, regardless of whether the customer paid by card, wallet, bank method, or crypto. From that balance, the finance team decides how to settle based on working capital needs, supplier obligations, and corridor speed.

What a unified stack changes operationally

Teams feel the difference in daily operations, not in architecture diagrams.

With a unified stack, the customer still pays with the method they trust. The internal result changes. Finance works from one operating balance instead of chasing funds across processors and wallets. Treasury can convert or hold value based on timing, currency exposure, and payout destination rather than being constrained by the original payin rail. Reconciliation becomes a controlled system process with fewer spreadsheet patches and fewer end-of-month surprises.

That is why a single API approach tends to outperform a stack of regional fixes once volume grows. One integration can support card and crypto acceptance while keeping settlement flexible across bank rails and stablecoins. It also gives product teams room to support subscription flows, community access, and invoicing without rebuilding the money movement layer each time. The global payment API architecture for cross-border settlement is worth reviewing if you are evaluating how to keep payins, balances, and payouts connected in one system.

The principle is straightforward. Customers should pay with the method that converts best in their market. The business should receive and deploy funds from one balance that it controls.

Four Ways to Go Global with a Unified Payment API

The abstract idea only matters if it maps to real business use cases. One product can cover several international payment workflows when the payin side, balance layer, and payout side are connected.

One product, four practical uses

Suby Payments is the API-first payment stack for teams that want cards and crypto in one checkout. This suits SaaS platforms, ecommerce operators, and developers building subscription or one-time purchase flows.

Suby Crypto is the crypto payment gateway layer for businesses that want a cleaner customer experience. It handles the swap, sponsors the gas, and settles either to a non-custodial wallet or to the Suby balance.

Suby Gating fits creators and community operators. It provides paid access for Discord, Telegram, downloads, and courses. That matters for global audiences because the monetization layer and access control sit together instead of being stitched across multiple tools.

Suby Invoicing works for agencies, freelancers, and service businesses billing clients internationally. The client chooses how to pay, while the business chooses how to receive funds.

For teams evaluating implementation detail, the global payment API overview is the clearest place to understand how a single integration supports these use cases.

How the payout choice changes the model

The payout side is where this becomes operationally different from a basic checkout tool.

According to Suby's pricing page, stablecoin settlement rails like USDC eliminate reliance on fragile banking corridors and reduce FX fees. It also states that for card payments, fees are deducted at payout time, while crypto transactions settle immediately after blockchain confirmation, with no fixed fees. Pricing depends on the payment method used, so there isn't a single flat rate to cite.

That creates a flexible model for cross border e commerce. A customer can pay by card, wallet, bank, or crypto, and the business chooses whether to receive the money in a bank account or in stablecoins like USDC, in the currency it wants. One especially practical flow is card payin with USDC settlement, but that is just one option among several.

There is also a broader infrastructure advantage behind this. Suby provides an API that lets businesses accept payments by card or crypto, and it also offers native Discord and Telegram integrations for subscriptions, paid access, and online communities. That means the same product can serve a merchant checkout, a SaaS subscription flow, a paid community, and an international invoice.

Your Next Step in Cross-Border Commerce

Cross border e commerce is growing because customers already behave globally. What holds companies back isn't demand. It's the operational complexity behind checkout, compliance, support, settlement, and reconciliation.

The businesses that handle this well don't overcomplicate the strategy. They localize what the customer sees, standardize what the finance team manages, and choose infrastructure that doesn't force separate systems for every market or payment rail.

The biggest blind spot is still the same one. Many teams can accept international payments, but they can't manage fiat and crypto payins inside one usable balance. Once that gap is closed, global selling becomes easier to control, easier to reconcile, and easier to scale.

If you're building for international customers, Suby is one practical option to evaluate. It is payment infrastructure for the global internet economy. Businesses can accept card, wallet, bank, or crypto payments, then choose to settle to a bank account or in stablecoins like USDC. The core model is simple and useful for cross-border operations: customers pay any way they want, businesses get paid the way they choose.