A payment provider is a company that handles financial transactions between a customer and a business, acting as the intermediary that helps money move from one side to the other. If you're selling online, it's the system that enables “pay now,” while managing the messy parts behind the scenes.

If you're a founder selling across borders, this question usually comes up right after growth starts to feel real. Your checkout works in one market, then a customer in another country wants to pay with a method you don't support, your bank settlement feels slow, or your finance team starts asking why getting paid internationally is still so awkward. That's when “what is a payment provider” stops being a basic definition and becomes an operating question.

Table of Contents

What Is a Payment Provider Anyway

You launch in one country, then customers start arriving from everywhere. One wants to pay by card, another expects a wallet, another asks for a bank option, and a client on the other side of the world says they can pay today if you can invoice them in a way that works for them. Suddenly, taking payments isn't a checkout button problem. It's an infrastructure problem.

A payment provider is the business that helps you accept payments from customers and receive the funds as a merchant. In plain English, it sits between your customer, your checkout, and the financial systems that approve, route, and settle the payment.

That sounds simple because, at a high level, it is. The confusion starts when people use one term to describe several different jobs. Some tools focus on payment acceptance. Others focus on routing or fraud controls. Others are really about payout and settlement. For a modern internet business, especially one selling globally, all of those pieces affect cash flow and customer conversion.

Practical rule: Don't think only about how your customer pays. Think equally hard about how your business receives the money.

That second part matters more than many founders expect. A provider can let your customer pay in one format while your business settles in another. If you're trying to understand how payment systems fit into a wider product stack, this comprehensive fintech app guide is a useful companion because it shows how payment flows sit inside a bigger financial product experience.

Why founders get tripped up

When 'payment provider' is mentioned, a common association is a checkout form. But its function is broader:

- Accepting payment methods: cards, wallets, bank options, and sometimes crypto.

- Passing data securely: sending payment information through the right rails.

- Handling approvals and declines: checking whether the transaction can go through.

- Settling funds: making sure the business receives the money.

- Supporting operations: refunds, disputes, subscriptions, invoicing, and reporting.

If you only optimize the front end, you can end up with a nice checkout and a painful back office. That's why the modern definition of a payment provider has expanded. It's no longer just about collecting money. It's about giving a business control over how it gets paid in a global market.

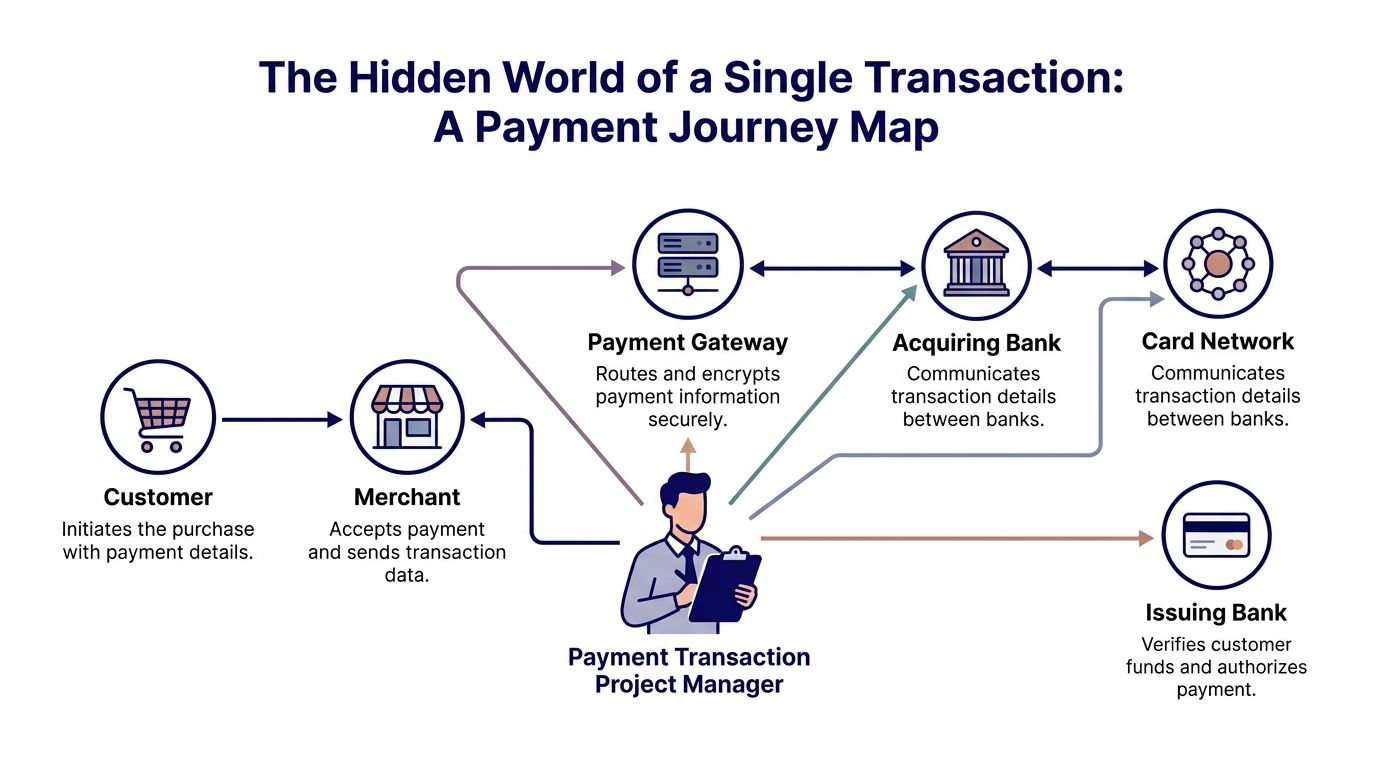

The Hidden World of a Single Transaction

A payment can feel instant to the customer. They tap “pay,” see a confirmation, and move on. Under the surface, several parties have to communicate in the right order, and they have to trust one another enough to approve the transaction.

A helpful way to think about it is this: the payment provider is like a project manager for money. Each participant has a different job, and the provider helps the whole process stay coordinated.

For a more focused look at the checkout-side role, Suby's overview of a payment gateway is useful because it clarifies one part of the broader stack.

Who's involved in one payment

Here's the cast of characters in a typical card transaction:

| Player | What they do |

|---|---|

| Customer | Starts the purchase and submits payment details |

| Merchant | Requests payment for the product or service |

| Payment gateway | Securely passes payment data to the right systems |

| Acquiring bank | Processes payments on the merchant side |

| Card network | Carries the message between institutions |

| Issuing bank | Decides whether to approve or decline based on the customer account |

A customer buying a subscription from your site doesn't see any of this. They just see success or failure. But each step affects conversion, reliability, and how quickly you can operate after the sale.

Why the provider matters so much

Let's walk through a simple example. A customer enters their card details at checkout. The gateway encrypts that information and routes it onward. The merchant-side bank and card network help deliver the request to the issuing bank. The issuing bank checks whether the payment looks valid and whether the customer can complete it. Then an approval or decline travels back through the chain.

That's only the authorization stage. Settlement comes later, and that's where founders often realize the payment story isn't finished when the customer sees “payment successful.”

A successful checkout isn't the end of the payment. It's the start of fulfillment, reconciliation, and payout.

This is why “payment provider” is a bigger idea than “money mover.” A good provider also helps with security requirements, recurring billing logic, dispute workflows, and the operational view your team needs after a payment happens.

Here's where people often get confused:

- Payment gateway vs payment provider: a gateway is often one component. The provider may include the gateway plus settlement, risk, reporting, and payouts.

- Approval vs settlement: an approved payment doesn't mean the funds are already in your hands.

- Collecting vs receiving: the customer's payment method and your payout method don't have to be the same thing.

Once you see a payment as a coordinated workflow rather than a single event, the overall system starts to make more sense.

Comparing Payout Models Cards vs Crypto

A lot of payment discussions get stuck in older categories like gateway, processor, aggregator, or merchant account provider. Those distinctions still matter, but for a global business, the more important question is often this: how do funds settle after the customer pays?

That's where traditional and newer models start to look very different.

If you want the crypto-native side of this picture in more detail, this explanation of a crypto payment processor helps connect checkout acceptance with settlement choices.

Old categories matter less than settlement design

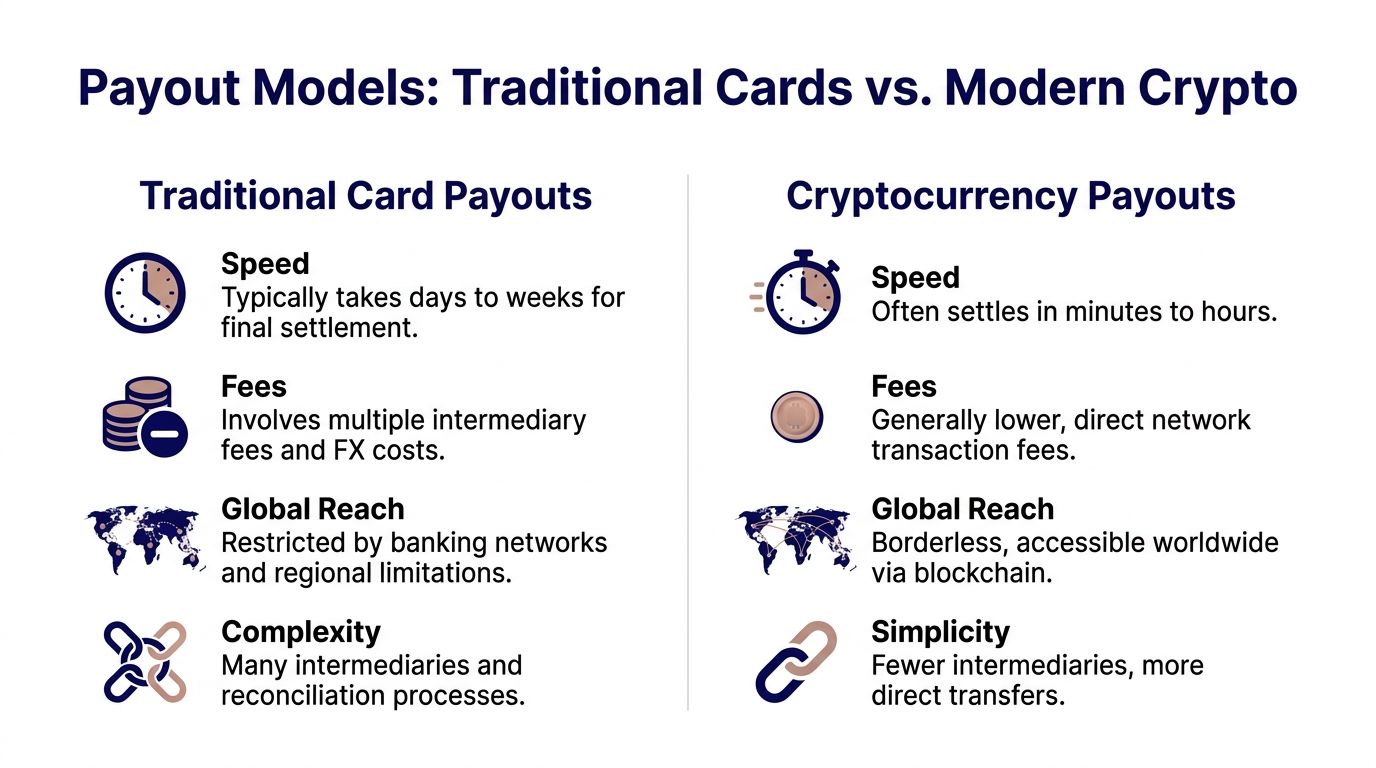

Traditionally, a customer pays by card and the merchant receives funds into a bank account through the banking system tied to card settlement. That model is familiar, and for many businesses it works fine.

But global commerce exposes its weak spots quickly:

- Cross-border delays: money can take time to move through banking rails.

- Extra conversion steps: if the customer pays in one currency and you operate in another, you may face conversion somewhere in the flow.

- More reconciliation work: different markets, methods, and payout cycles can make finance operations messy.

A newer model separates the customer's payment experience from the business's settlement preference. That means a customer can still pay with a familiar method like a card, while the business chooses to receive funds differently, including in stablecoins like USDC.

A simple side by side view

Here's the practical comparison founders usually care about:

| Question | Traditional card to bank settlement | Card or crypto to stablecoin settlement |

|---|---|---|

| Customer experience | Familiar card checkout | Can still be familiar card checkout, or crypto if offered |

| Merchant payout destination | Bank account | Stablecoin balance or wallet, depending on provider |

| Cross-border handling | Often tied to banking rails and conversions | Can reduce dependence on traditional cross-border banking steps |

| Treasury flexibility | Lower if you want digital dollar liquidity | Higher if you want to hold or move stablecoin value |

| Operational fit | Good for local banking-first operations | Useful for internet-native and international operations |

This is the key idea behind hybrid models. The customer doesn't need to care how you settle. They just pay in the way they prefer. You choose what happens next on the merchant side.

One example is Suby, which provides an API that lets businesses accept payments by card or crypto, and also offers native Discord and Telegram integrations for subscriptions, paid access, and online communities. It's a single product with four ways to use it: Suby Payments for API-first card and crypto checkout, Suby Crypto as a crypto payment gateway that handles the swap, sponsors the gas, and settles to a non-custodial wallet or Suby balance, Suby Gating for paid access to Discord, Telegram, downloads, and courses, and Suby Invoicing so clients can pay how they want while the business receives what it wants. In practice, that means customers can pay by card, wallet, bank, or crypto, while the business chooses to settle to a bank account or in stablecoins like USDC, including the card-to-USDC flow many global businesses now want. Pricing depends on the payment method used, so it's worth checking the Suby pricing page for the current per-method details.

Founder takeaway: The checkout method your customer sees and the payout method your business needs are now separate design choices. That changes how you should evaluate providers.

Key Features for a Global Business in 2026

If you're evaluating providers for a business that sells internationally, the feature list should be practical, not abstract. You're not buying a badge. You're choosing a system that affects conversion, support load, treasury operations, and product flexibility.

The practical checklist

A global-ready provider should cover more than basic payment acceptance.

Broad pay-in options: Customers don't all want to pay the same way. Look for support across cards, wallets, bank methods, and, if relevant to your market, crypto. This matters because payment friction often shows up as abandonment, not explicit feedback.

Flexible settlement: This is the feature many teams underweight at the start. You may want bank payouts in one market and stablecoin settlement in another. The best setup lets your customer pay in their preferred method while your business receives funds in the format that matches your operations.

Strong API and webhooks: If you're building a SaaS product, marketplace, app, or custom checkout, API quality matters. Clean documentation, reliable webhooks, and predictable event handling reduce engineering drag.

Operational tooling: Dashboards, refund workflows, dispute handling, subscriptions, invoicing, and payment links are not “nice to have” once volume starts growing. They're what your finance and support teams use every day.

What to confirm before you sign

Security and compliance should be plain, documented, and easy to verify.

- PCI-aligned processing support: If card payments are involved, your provider should clearly state how card security is handled and what your responsibilities are.

- Authentication support: For regions and use cases that require stronger customer checks, support for SCA matters.

- Refund and dispute workflows: Problems happen. You need to know what the process looks like before you face your first one.

- Integration options: Some businesses need a direct API. Others need payment links, embedded checkout, or native community integrations.

Don't choose based on the homepage promise. Choose based on whether the provider can support your exact payment flow, payout preference, and internal workflow.

There's also a product strategy angle here. A creator monetizing a Telegram community, a SaaS company billing globally, and a freelancer invoicing overseas clients may all need “a payment provider,” but they don't need the same implementation. The right feature set depends on how you sell, where your buyers are, and how you want funds to land after collection.

How Stablecoin Rails Eliminate Cross-Border Friction

Cross-border payments often feel harder than they should. Not because the customer experience is always broken, but because the money path after payment can still be slow, layered, and hard to control.

The reason stablecoin rails matter isn't novelty. It's that they can simplify the settlement leg of international commerce.

A deeper discussion of cross-border payments solutions helps frame why businesses are looking beyond old banking-only flows.

The old path across borders

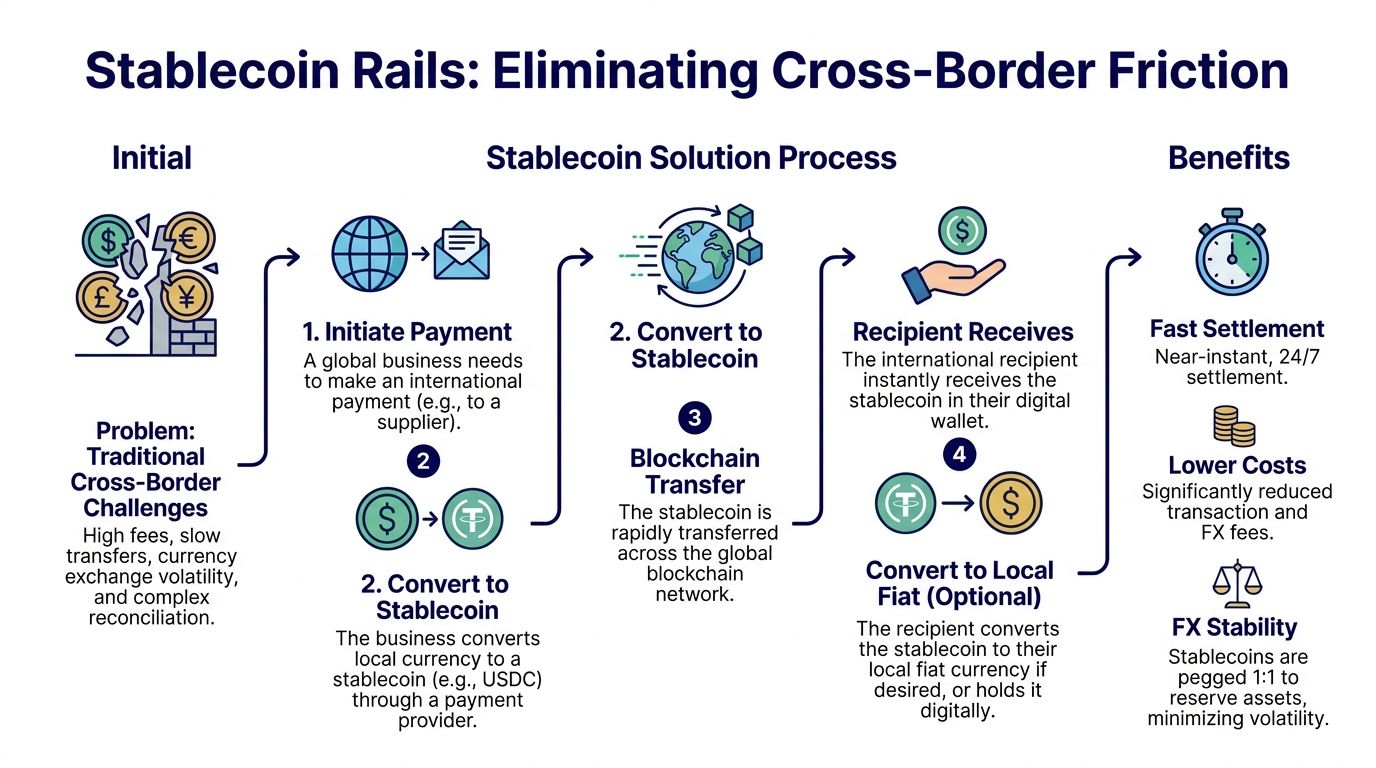

Start with a common situation. A customer in one country buys from your company. They pay using a familiar method, and from their point of view the transaction is done.

For your business, though, the money may still need to move through several institutions before it reaches your operating account. If currencies differ, another conversion step may appear. If your team works with contractors, suppliers, or treasury accounts in multiple regions, that complexity multiplies in the back office.

Common friction points look like this:

- Banking delays: your sale is complete, but usable funds may not be immediately available.

- Opaque conversion: you know money was converted, but not always with much clarity.

- Reconciliation burden: different currencies and payout systems create accounting work.

- Limited control: your payout path is often determined by legacy rails, not by what best fits your business.

The newer path with stablecoin settlement

Now take the same commercial moment and change only the settlement rail. The customer can still pay with a method they recognize, such as a card. On the merchant side, the provider converts and settles value into a stablecoin such as USDC, rather than forcing a traditional bank-only payout path.

That changes the business experience in a few important ways.

- Faster access to funds: you're not waiting on every cross-border banking step before the value becomes usable.

- More treasury control: you can hold digital dollar value, move it when needed, or convert on your own timeline.

- Cleaner international operations: for internet businesses with global suppliers, contractors, or retained earnings across markets, this can be much easier to work with.

Here's a short visual explainer that complements the flow above:

Stablecoin settlement isn't about using new rails for their own sake. It's about reducing the friction that old rails add to global business.

This is why the hybrid fiat-to-stablecoin model matters. A customer pays the way they already understand. The business receives the form of value that better matches global operations. That's a meaningful shift from the older assumption that customer payment method and merchant payout rail must mirror each other.

Choosing the Right Provider for Your Business Model

The right provider depends less on abstract feature lists and more on how your business earns money. Two founders can sell online, process the same broad categories of payments, and still need very different setups.

Match the provider to how you sell

A few examples make this easier to sort out.

If you're a developer-led SaaS company, you'll probably care most about API quality, webhooks, recurring billing support, and the ability to control checkout and payout logic inside your product. The provider has to fit your stack, not force your product to work around its limitations.

If you run a paid community or creator business, native integrations can matter more than raw API flexibility. A provider that works cleanly with Discord or Telegram may remove a lot of manual admin work around access control, renewals, and member payments.

If you're a freelancer, consultant, or agency, invoicing flexibility may be the deciding factor. Clients often want to pay in the method they already use internally. You may prefer to receive the funds in a different form that's easier for your own operations.

The questions worth asking

Before you choose, ask these:

How do my customers want to pay?

Don't answer from assumption. Look at your current buyers, geography, and sales process.How do I want to receive funds?

Bank account, stablecoin settlement, or a mix depending on market.Do I need infrastructure or a simple workflow?

Some teams need deep API control. Others need payment links, invoicing, or community gating.Who on my team will live in this system?

Engineering, finance, support, and operations may all rely on it for different reasons.What happens after the payment succeeds?

Access control, subscription management, reconciliation, refunds, and reporting matter as much as the transaction itself.

A lot of founders compare providers only on visible checkout experience or headline fees. That's usually too narrow. Pricing matters, of course, but since pricing often depends on payment method and flow, it rarely tells the whole story by itself. The better lens is operational fit.

Choose the provider that lets your customers pay with the least friction and lets your business receive funds in the form that best supports growth. For a global company, that combination is often more important than shaving a tiny amount off a single transaction path.

If you want a payment setup that supports card and crypto acceptance through one API, plus native Discord and Telegram flows for subscriptions, paid access, and communities, take a look at Suby. The core idea is simple: customers can pay the way they want, and your business can receive the money the way you choose.