If you're running a SaaS product, a paid newsletter, a course business, an ecommerce store, or a creator membership, the tax problem usually shows up after revenue starts working. Money comes in through card payments, maybe some bank transfers, maybe crypto or USDC, and suddenly your bookkeeping doesn't match your dashboard, your invoices don't match your bank account, and you aren't sure where tax applies.

That confusion is normal. Most advice on taxes for online businesses is either too general to use or too legalistic to act on. What matters in practice is simpler. You need to know which taxes exist, where you owe them, how your payment flows affect bookkeeping, and when the complexity is high enough that you should stop guessing.

Table of Contents

- Do I owe sales tax on digital products

- Do small side businesses still count

- What records should I keep for online revenue

The Three Main Taxes Online Businesses Pay

The starting point for taxes for online businesses is separating three different obligations. Founders often lump everything into “business taxes,” but that creates bad decisions because each tax has a different trigger, filing rhythm, and bookkeeping treatment.

Income tax is about profit

Income tax is the tax on what your business earns after expenses. If you sell subscriptions, courses, templates, consulting, or physical goods, income tax doesn't care which checkout button the customer used. It cares about your profit.

Clean books are essential for founders. Revenue, refunds, software spend, contractors, hosting, ad spend, banking fees, and payment fees all need to be categorized correctly. If they aren't, your tax return becomes guesswork.

Practical rule: Your dashboard shows sales activity. Your books need to show taxable profit.

For founders operating across borders, income tax gets more complicated because profits can be taxed in more than one jurisdiction unless the rules place them clearly. If you also need a non-U.S. perspective on entity basics and deadlines, this roundup of essential 2026 UK tax information is a useful companion read.

Sales tax is money you collect

Sales tax is different. In most cases, this is not your revenue. You collect it from the customer and pass it through to the relevant authority.

That distinction matters because founders often make one of two mistakes. They either ignore sales tax until a state or country contacts them, or they book sales tax collected as if it were business income. Both create cleanup work later.

A simple mental model helps:

| Tax type | What it applies to | Your role |

|---|---|---|

| Income tax | Net profit | Taxpayer |

| Sales tax | Taxable customer sale | Collector |

| Payroll tax | Wages and employment | Withholder and remitter |

Payroll tax starts when you hire

Payroll tax begins the moment you move from solo founder to employer. Once you hire employees, you take on withholding, employer-side remittance, and reporting obligations tied to compensation.

This catches early-stage companies because they think payroll is an HR issue. It isn't. It's a tax system with filing deadlines attached. The moment salaries start running, your controls need to improve.

A useful rule of thumb is this:

- If you pay yourself from profits, income tax is the first concern.

- If you collect tax from customers, sales tax control matters.

- If you pay a team, payroll tax becomes operational, not optional.

Most tax problems in online businesses don't come from obscure law. They come from mixing these three buckets together.

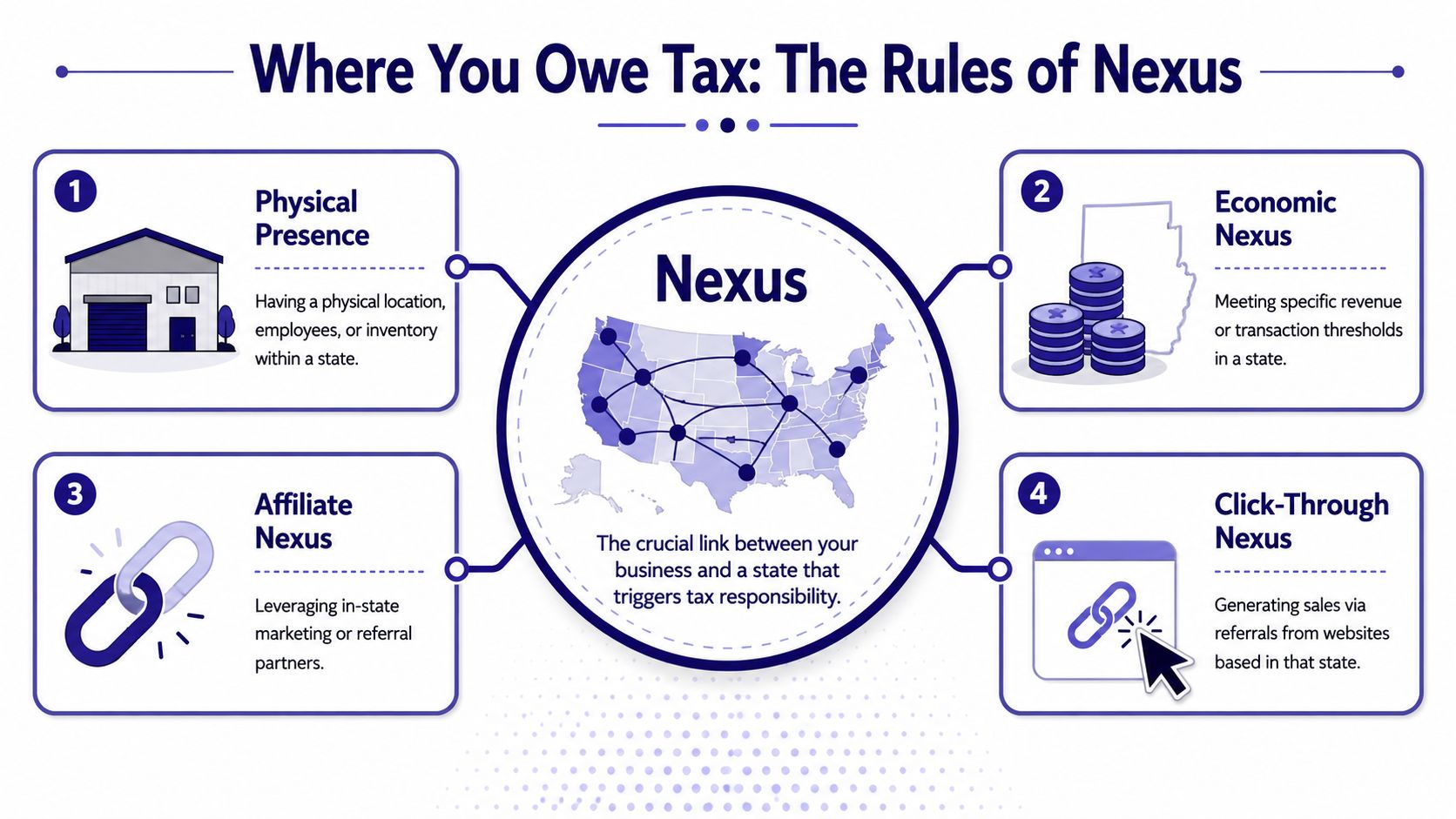

Where You Owe Tax The Rules of Nexus

The hardest part of U.S. sales tax isn't calculating it. It's knowing where you're obligated to collect it. That question turns on nexus, which is the legal connection between your business and a state.

What changed after Wayfair

The old mental model was physical presence. Founders assumed that if they had no office, warehouse, or employee in a state, they didn't owe sales tax there.

That isn't how it works now. For online businesses selling cross-border, the critical tax trigger is economic nexus, which no longer requires physical presence in the U.S. following the 2018 Supreme Court ruling in South Dakota v. Wayfair, with thresholds typically set at $100,000 in sales or 200 separate transactions within a 12-month period.

That one shift changed the operating burden for remote sellers, SaaS companies, and digital product businesses. You can become obligated in a state because of sales volume alone.

Nexus is not a planning concept. It's a trigger. Once you cross it, the state doesn't care that you never opened an office there.

There's a related international concept worth understanding too. If you're thinking beyond U.S. state taxes and into cross-border corporate exposure, this guide to the PE tax concept helps explain how taxable presence gets evaluated in other systems.

How founders should think about nexus

In practice, founders should treat nexus as a monitoring problem, not a once-a-year tax question. If your revenue is spread across many states, you need to know where sales are landing and whether the items sold are taxable in those states.

Start with these checks:

- Map your customer locations: Pull state-level sales reports from your payment and accounting stack.

- Separate taxable from non-taxable sales: Thresholds matter, but product taxability matters too.

- Watch threshold crossings in real time: Waiting until year-end is too late.

- Register before collecting: Once you have an obligation, your filing process needs to follow.

A lot of founders also miss that nexus can arise from more than economic activity. Physical presence, affiliates, and referral relationships can matter too. The practical point is not to memorize every category. It's to stop relying on “we're online only” as if that settles the issue.

If you want a direct overview of how this applies to remote selling, Suby has a useful explainer on internet sales tax obligations.

A Guide to International Taxes VAT GST and DSTs

Once you sell outside your home country, the tax question shifts. Instead of asking only where your company is based, authorities look at where your customer is located and what type of sale you're making.

Consumption taxes follow the customer

VAT and GST are consumption taxes. For many online businesses, that means the sale can create a collection obligation in the customer's jurisdiction, not just in yours.

This matters most for software subscriptions, downloadable products, paid communities, online education, and other digital services. A founder may have a clean domestic setup and still create foreign compliance work by selling to customers abroad.

Your operating model should reflect that reality:

- Invoice clearly: Show the tax treatment and customer location logic in your records.

- Store evidence of location: Billing address, country data, and transaction records need to line up.

- Separate tax collected from revenue: The same discipline that matters for U.S. sales tax matters here too.

If your revenue includes pre-sales, memberships, or campaign-style launches, this guide on VAT and tax for crowdfunding campaigns is worth reading because those models often create tax treatment questions earlier than founders expect.

Why digital taxes became a global issue

Digital business moved faster than international tax rules. Countries responded in different ways, including Digital Services Taxes, or DSTs, which several jurisdictions imposed on gross revenues from certain digital services, typically ranging between 2% and 7% according to the Hinrich Foundation overview of trade and tax in a digital world.

The OECD then pushed for a broader framework. In October 2021, 136 countries agreed to a reform allowing multinationals to be taxed where they generate profit, and it introduced a global minimum corporate tax rate of 15% for companies with revenue over 750 million euros, as outlined in the OECD announcement summary.

For most founders, that OECD deal doesn't change day-to-day filing in the same way sales tax or VAT does. But it explains why tax authorities now focus much more aggressively on digital revenue, customer location, and cross-border profit allocation.

Selling globally means your bookkeeping has to become location-aware, even if your product is entirely digital.

Handling Modern Payments from Cards to Crypto

Tax reporting breaks when payment operations get messy. That's common in internet businesses because revenue no longer arrives through one clean merchant account.

Why reconciliation breaks first

A modern online company might accept cards for subscriptions, bank payments for invoices, and stablecoins for international clients. The tax treatment starts with the same principle, but the bookkeeping gets harder because settlement timing, payout currency, fees, and transaction records don't always line up neatly.

The core discipline is straightforward. You need to record what the customer paid, when they paid, what fee was deducted, what currency reached you, and whether any conversion happened before settlement.

What doesn't work is trying to reconstruct all of that from bank statements alone. Bank data usually shows settlement. Tax and accounting records need the original commercial event.

A cleaner operating setup

One practical option is to reduce the number of disconnected systems touching revenue. Suby provides an API that lets any business accept payments by card or crypto, and it also offers native integrations with Discord and Telegram for use cases like subscriptions, paid access, and online communities. As a single product, it can be used in four ways: Suby Payments for accepting cards and crypto through one checkout, Suby Crypto for handling token swaps, gas sponsorship, and settlement to a non-custodial wallet or the Suby balance, Suby Gating for paid access to Discord, Telegram, downloads, and courses, and Suby Invoicing so the client pays how they want while the business receives what it wants. The platform also unifies over 300 payment methods into a single balance view, supports switching between USD and EUR, and allows payout in any currency or stablecoin according to the official product description.

That matters for tax operations because customers can pay any way they want, and the business gets paid the way it chooses. A useful example is the flow where a customer pays by card and the business receives USDC. That's operationally convenient, but only if your books preserve both sides of the transaction clearly.

A few controls make this manageable:

- Record gross customer payment first: Don't start from net settlement.

- Log conversion details: If funds move from card intake to stablecoin payout, preserve that trail.

- Keep transaction-level IDs: They matter when reconciling disputes, refunds, and audit questions.

- Check pricing by method: Payment costs vary by payin method, so don't assume a flat rate. Use the official pricing page before booking assumptions.

If you're adding digital asset acceptance, it helps to think less about novelty and more about ledger hygiene.

Your Step-by-Step Compliance and Bookkeeping Checklist

Founders don't need a perfect tax department on day one. They do need a repeatable operating routine. That's what keeps taxes for online businesses from turning into a cleanup project.

The operating checklist

Register the business properly

Form the entity you plan to operate through, get the necessary tax IDs, and make sure the legal name on invoices, banking, and payment processors matches.Separate personal and business money

Use a dedicated business bank account from the start. If personal spending runs through the same account, your tax prep gets slower and less reliable.Choose accounting software early

Don't wait until revenue is material. Start with a system that can handle recurring revenue, refunds, and payment fee mapping before your chart of accounts gets messy.

Operator note: Good bookkeeping is less about software choice and more about whether someone reviews the records every month.

Track nexus thresholds continuously

All 45 U.S. states with sales tax now enforce economic nexus rules, and Washington requires collection once $100,000 in sales or 200 transactions are reached, with the obligation beginning instantly and no grace period, according to Klasing Associates' explanation of online business tax obligations. That means your reporting has to identify where taxable sales are building before a filing problem appears.Maintain document evidence digitally

Save invoices, contracts, receipts, payout reports, and customer tax records in one system. Searchability matters when questions come up months later.Build a reconciliation habit

Payment processor balances, bank deposits, refunds, and accounting entries should match regularly, not only at year-end. A helpful starting point is this guide to payment reconciliation for online businesses.- You have multi-state exposure: If you're tracking obligations in several states, filing risk goes up fast.

- You sell internationally: VAT, GST, and local invoicing rules usually need country-specific review.

- You accept crypto or stablecoin payments regularly: The bookkeeping needs someone who understands how to document those flows.

- You're hiring across jurisdictions: Payroll tax gets complicated quickly.

- You've received a notice or audit inquiry: That's not the moment to experiment.

What to review every month

Use a short monthly review instead of a heroic annual catch-up:

| Review item | What to check |

|---|---|

| Revenue | Gross sales, refunds, and failed payments |

| Tax collected | Amounts held for remittance, not booked as income |

| Expenses | Correct categorization and supporting documents |

| Jurisdiction exposure | New states or countries where obligations may be forming |

| Payouts | Whether settlement records match source transactions |

The businesses that stay calm during tax season usually aren't smarter. They just close the books consistently.

Common Tax Mistakes and When to Hire a Professional

The expensive mistakes are usually boring. They happen when founders move fast operationally and assume tax can be fixed later.

Mistakes that create avoidable problems

One common error is commingling funds. If the same card pays for software subscriptions, ad spend, groceries, and founder travel, your records stop being reliable. You can still clean it up, but you pay for that cleanup in time or accounting fees.

Another mistake is assuming all online sales are taxable in the same way. They aren't. Product type, customer location, and local rules all matter. Founders who skip that nuance often over-collect, under-collect, or register in places where they didn't need to.

A third problem is ignoring payment complexity. If you accept subscriptions, invoices, and digital asset payments without a clear ledger trail, refund handling and revenue recognition become much harder than they should be.

Bad tax outcomes usually start as weak operating habits, not aggressive tax positions.

When DIY stops making sense

You should bring in a CPA or tax advisor when the business crosses from simple to layered. The signal isn't only revenue growth. It's structural complexity.

Hire help when:

A founder can own the workflow. That doesn't mean the founder should interpret every edge case alone.

Frequently Asked Questions About Online Business Taxes

Do I owe sales tax on digital products

Sometimes, yes. Sometimes, no. It depends on the jurisdiction and the nature of the product.

In California, electronic data products like software, digital books, and mobile apps are generally not taxable when transmitted over the internet unless they include physical materials, as explained in Numeral's summary of California sales tax rules for online sellers. That's a good example of why generic tax advice can mislead digital sellers.

Do small side businesses still count

Yes. A side business is still a business for tax purposes. Small scale doesn't remove the need to track income, expenses, and any collection obligations that apply to your sales model.

The practical difference is volume, not responsibility. If the activity is real and recurring, keep books from the start.

What records should I keep for online revenue

Keep the original invoice, proof of payment, refund records, fee detail, customer location data where relevant, and the settlement record showing what reached your bank or wallet.

For subscription businesses, also keep plan terms, renewal history, and cancellation evidence. For digital asset payments, keep transaction IDs and any conversion records tied to settlement.

If you want a cleaner way to manage global payment flows while keeping tax and bookkeeping records easier to reconcile, Suby is one option to look at. It gives businesses an API to accept card or crypto payments, supports native Discord and Telegram monetization flows, and lets customers pay how they want while the business receives funds the way it chooses, including bank payout or stablecoins like USDC.