You’re probably dealing with this already. A customer in London pays instantly. Your team sees the sale right away. Then the money takes days to arrive, lands in the wrong currency, loses margin in conversion, and forces someone on your side to reconcile fees that weren’t obvious at checkout.

That gap between customer payment and merchant payout is where most payment pain lives.

Electronic commerce payments are often described as a checkout problem. For founders, they’re really an operations problem. The checkout is just the visible part. Underneath it, you have authorization, fraud checks, settlement timing, currency conversion, disputes, subscription retries, and payout logistics. If you sell globally, each one affects cash flow.

That matters because online payments are no longer a niche behavior. Global digital payments in electronic commerce reached £18.6 trillion in 2025, after digital methods grew from 34% of e-commerce transactions in 2014 to 66% by 2024, with 79% projected by 2028 according to The Payments Association’s 2025 trends report.

Table of Contents

- Cards still set the baseline

- Wallets reduce checkout friction

- Bank transfers and account-to-account methods

- Stablecoins solve a different payment problem

- What to support first

- The traditional flow

- Why founders feel friction later

- A cleaner payout model

- Where confusion usually happens

- The fee you see and the cost you absorb

- FX is often the margin leak

- Why payout timing matters so much

- What better looks like

- PCI DSS in plain language

- Strong customer authentication and 3DS

- Chargebacks and disputes

- What a good payment setup changes

- Payment links for fast deployment

- Embedded checkout for a cleaner customer experience

- API and webhooks for custom logic

- Matching the integration to the business model

- Failed payments are a revenue problem

- Dunning needs to be deliberate

- Subscription logic goes beyond charging a card

What Are Electronic Commerce Payments

A simple way to think about electronic commerce payments is this: they’re the system that lets a customer pay online and lets a business receive usable money.

For a founder, that system includes more than the checkout page. It includes the payment method the customer chooses, the companies that route and authorize the transaction, the fraud controls around it, and the way the final payout reaches your business.

The founder view

Say you run a SaaS product, a paid community, or a digital storefront. You can attract customers from many countries on day one. That’s the good part.

The harder part starts after the sale:

- A customer pays in one currency

- Your processor settles in another

- Your bank receives funds later than expected

- Your accounting team sees separate fees, reserves, and adjustments

Nothing about that feels like “just payments.” It feels like treasury, risk, support, and finance operations bundled into one workflow.

What sits inside the payment stack

Most electronic commerce payments involve a few core layers:

| Component | What it does | Why it matters |

|---|---|---|

| Checkout | Collects payment details | Shapes conversion and trust |

| Authorization | Requests approval for the charge | Determines whether the payment succeeds |

| Fraud controls | Filters risky transactions | Protects revenue without blocking good customers |

| Settlement | Moves funds through the network | Affects timing and predictability |

| Payout | Delivers money to the business | Impacts cash flow and operations |

Practical rule: A payment isn’t finished when the customer sees “success.” It’s finished when your business receives funds in a form you can use.

That’s why electronic commerce payments matter so much for internet businesses. They’re not just infrastructure. They shape your margins, your support workload, your expansion plans, and how quickly revenue turns into working capital.

Understanding Today's Digital Payment Methods

A founder launches in the US, gets customers in Germany, Brazil, and Singapore within the first month, and assumes the hard part is done once checkout accepts cards. Then the operational reality shows up. Approval rates vary by market, mobile buyers abandon clunky forms, some customers expect bank pay, and the business still gets settled through slow, fee-heavy cross-border rails.

Payment methods shape all of that. They influence whether a customer trusts the checkout, whether the charge gets approved, and how much friction your team inherits after the sale.

Cards still set the baseline

For many online businesses, credit and debit cards remain the default starting point because they are widely understood and broadly accepted. They work across one-time purchases, stored credentials, and recurring billing, which makes them the practical base layer for internet commerce.

Their role is still large at a global level. According to the Worldpay Global Payments Report 2024, cards accounted for 32% of global e-commerce transaction value in 2023. That matters for a simple reason. If card acceptance is weak, a business limits reach before it even gets to pricing, product, or growth.

Cards do have tradeoffs. Cross-border card payments often carry higher interchange, scheme fees, FX spreads, and more declines than domestic transactions. A payment method that feels familiar to the buyer can still create hidden cost for the merchant.

Wallets reduce checkout friction

Digital wallets such as Apple Pay, Google Pay, and PayPal speed up checkout by reducing typing and reusing stored credentials. On mobile, that difference can be the gap between a completed order and an abandoned cart.

Wallets also help with trust. The customer recognizes the brand, the device can supply authentication signals, and the issuer often gets better data than it would from a manually entered card form. That can improve approval rates in the right context.

Wallets are already a major part of online commerce. According to the Worldpay Global Payments Report 2024, digital wallets made up 50% of global e-commerce transaction value in 2023.

The catch is operational. Many wallets still settle through traditional acquiring and banking infrastructure. So the customer experience may improve while the merchant still deals with delayed payouts, FX conversion, and fragmented reconciliation on the back end.

Bank transfers and account-to-account methods

Bank-based methods are common in markets where customers prefer direct account payments, especially for larger purchases or local payment habits that developed outside the card system. In practice, these methods can lower acceptance friction in specific regions and reduce reliance on card rails.

They are not a universal replacement for cards. Coverage varies by country, refund flows can be more complex, and user experience depends heavily on the local scheme. A founder selling globally usually needs them as part of a mix, not as the only option.

Stablecoins solve a different payment problem

Stablecoins matter for a different reason. They do not replace every customer-facing payment method. They improve how a business receives and moves money after the sale.

That distinction clears up a common point of confusion. Checkout and settlement are separate jobs. Cards and wallets are strong tools for customer acceptance. Stablecoins such as USDC are increasingly useful for settlement because they can reduce banking delays, cut out repeated currency conversions, and give internet businesses a more predictable way to hold or move funds across borders.

A good comparison is retail versus wholesale transport. Cards help the customer get through the front door. Stablecoin settlement helps the business move value between markets without waiting on several banks, correspondent fees, and batch-based payout schedules.

For a global software company, marketplace, or creator platform, that difference is practical, not theoretical. The buyer can still pay with a familiar method, while the merchant receives settlement in a digital dollar format that is easier to route, reconcile, and use for international payouts.

Strong global payment setups often separate the best method for customer checkout from the best method for merchant settlement.

What to support first

Choosing payment methods starts with two questions. How does your customer prefer to pay, and how does your business prefer to receive funds?

- For broad consumer reach: cards are usually the base layer.

- For mobile-heavy checkout: wallets often improve completion.

- For region-specific preferences or larger purchases: bank-based methods can improve local fit.

- For global internet businesses managing FX, payout timing, and treasury complexity: settlement options such as stablecoins deserve as much attention as checkout options.

- For subscriptions and repeat purchases: choose methods that support stored credentials and reliable recurring billing.

The useful mindset is broader than “what should we turn on at checkout?” A better question is “which payment methods create the least friction from purchase to usable cash?” That is where many traditional cross-border setups start to break down, and where modern settlement options begin to earn their place.

The Journey of a Payment from Click to Payout

A card payment looks instant from the outside. It usually isn’t.

When a customer clicks “Pay,” several companies and systems have to agree before your business sees a successful charge. Then a separate process starts to settle and pay out the funds.

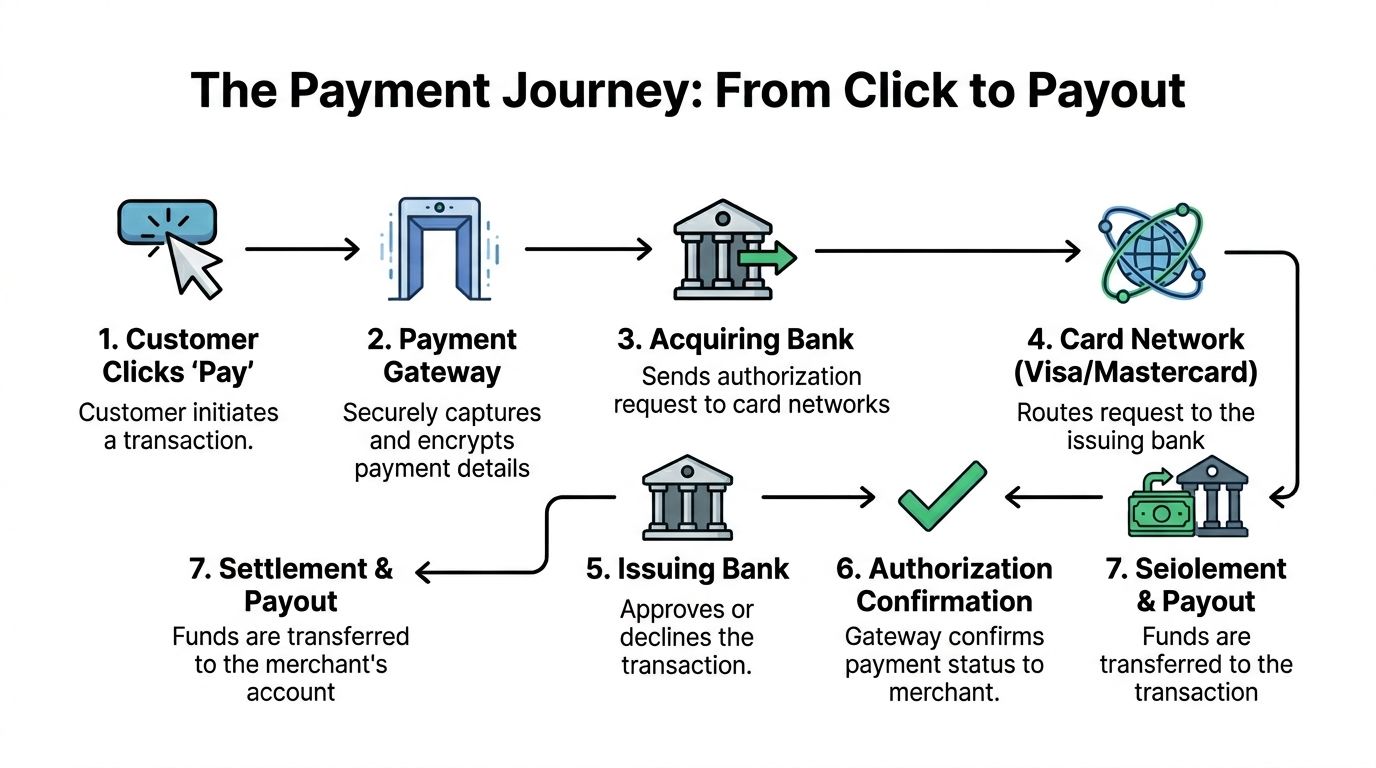

The traditional flow

Here’s the usual path for an online card transaction:

The customer enters payment details

Your checkout collects card or wallet data and sends it securely.The payment gateway packages the request

The gateway encrypts the data and prepares it for the processor.The processor passes it to the acquirer

This is the merchant-side banking relationship that handles the request.The card network routes the transaction

Networks such as Visa and Mastercard carry the authorization request.The issuing bank decides

The customer’s bank approves or declines based on available funds, fraud checks, and policy rules.The authorization response returns

Your checkout shows success or failure.Settlement happens later

Even after approval, funds still need to move through clearing and settlement before payout reaches the merchant.

That’s a lot of handoffs for something customers expect to feel simple.

Why founders feel friction later

The payment can be approved immediately, but operations teams often run into problems afterward.

A few examples:

- Authorization succeeded, payout is delayed

- Settlement arrives net of fees that weren’t obvious

- Cross-border sales create FX exposure

- Reconciliation requires matching multiple reports

- A support team needs to explain declines that happened upstream

The size of this infrastructure is one reason the industry is changing. The payment processing industry is projected to reach $139.90 billion by 2030, growing at a 14.5% CAGR, according to PayCompass payment processing industry stats. That growth reflects how much machinery sits behind a single online payment, and why real-time settlement matters more now.

A cleaner payout model

A more modern approach keeps the customer experience familiar while simplifying what happens after authorization.

Instead of forcing the merchant to wait for bank-driven payout cycles in local fiat, the system can accept a customer’s card payment and settle the merchant side in USDC.

That changes the part founders usually hate most:

| Traditional setup | Modern settlement setup |

|---|---|

| Customer pays by card | Customer pays by card |

| Merchant waits for payout cycle | Merchant receives settlement in USDC |

| FX can affect the received value | Payout is more predictable |

| Bank accounts and regions shape access | Wallet-based settlement reduces banking dependence |

This isn’t magic. It’s just a cleaner separation between front-end payment acceptance and back-end payout delivery.

If your users want a normal checkout, give them one. If your finance team wants faster, more predictable settlement, design for that separately.

Where confusion usually happens

Founders often mix up three different moments:

- Authorization means the bank approved the transaction.

- Settlement means the money is moving through the payment system.

- Payout means your business receives the funds.

Those are related, but they are not the same thing. A checkout can look healthy while the payout side stays slow, fragmented, or expensive.

That’s why evaluating electronic commerce payments only by checkout design misses the full operating cost. The important question is not just “Can the customer pay?” It’s “How many systems stand between the sale and usable revenue?”

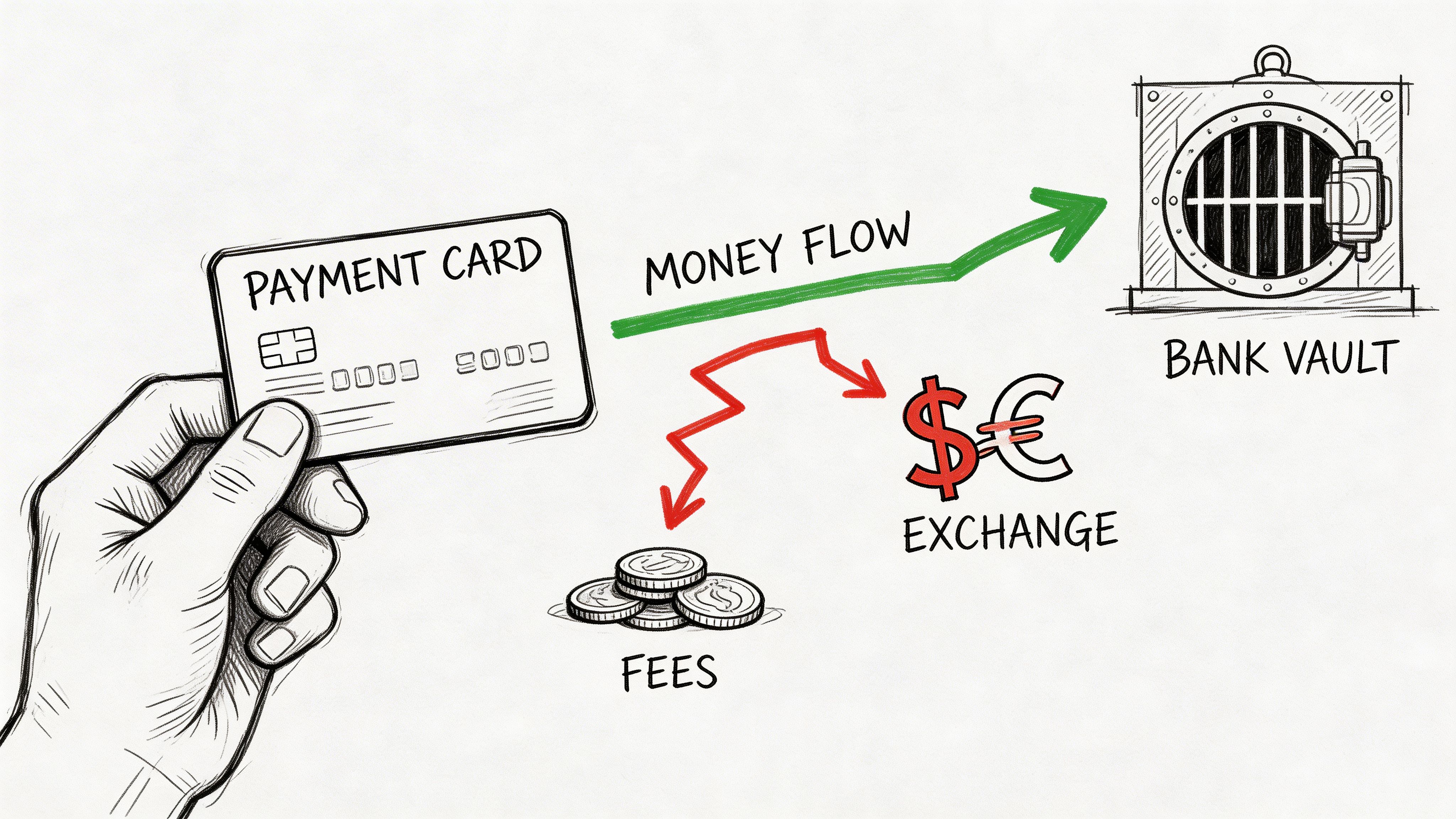

Navigating Fees, Currency Exchange, and Payouts

Most businesses start by comparing headline processing rates. That’s understandable, but it’s rarely enough.

The bigger cost usually hides in the layers around the charge. Cross-border fees, currency conversion, delayed settlement, reserves, and reconciliation overhead can reshape your margins.

The fee you see and the cost you absorb

A checkout rate may look clear at first. Then the finance reality shows up later.

That gap appears when a business sells across borders, settles into a bank account in a different currency, or gets paid on a timeline controlled by the processor rather than by the business.

A founder often ends up paying in three ways at once:

- Direct processing fees

- Foreign exchange spread

- Operational cost from waiting and reconciling

FX is often the margin leak

If you sell globally, foreign exchange matters even when payment volume looks healthy.

Traditional processors can impose 2-5 day settlement windows and 1-3% FX fees, while 40% of small merchants in emerging markets cite payout uncertainty as a top barrier, according to the World Bank blog on why digital payments still stop at the small shop.

That’s why two businesses with the same sales volume can feel very different financially. One receives predictable value quickly. The other waits, converts, and loses margin in steps that are hard to explain to customers and hard to model internally.

Why payout timing matters so much

Delayed payouts aren’t just annoying. They change how a company operates.

A few examples:

- A SaaS team delays ad spend because cash hasn’t landed yet

- A creator can’t pay collaborators on time

- An agency invoices globally but keeps juggling bank accounts

- Support staff spend time answering “where is my payout?”

A slow payout cycle turns revenue into a planning problem.

Founder check: If your payment setup works only after you add manual finance workarounds, it doesn’t really work.

A short explainer can help if you want a visual view of how fees and movement of funds interact in practice.

What better looks like

A practical alternative is to preserve familiar customer payment methods while changing the payout rail used on the merchant side.

For a global business, receiving settlement in USDC can reduce uncertainty around when funds arrive and what value they hold when they do. That doesn’t remove every operational task, but it removes a large chunk of traditional cross-border friction.

The important shift is conceptual. Don’t judge electronic commerce payments only by acceptance. Judge them by net usable revenue, settlement predictability, and how much manual finance work the system creates.

Keeping Payments Secure and Compliant

Security is where many founders either overcomplicate the topic or avoid it entirely. Neither helps.

You don’t need to become a payment compliance specialist, but you do need to understand the moving parts well enough to choose tools and workflows that don’t create unnecessary risk.

PCI DSS in plain language

PCI DSS is the security standard for handling card data. If your business accepts cards online, this matters because card details are sensitive and tightly regulated.

The practical question is simple: are you directly handling card data, or is your payment provider handling it in a way that reduces your exposure?

If you want a straightforward outside explanation, this guide on what is PCI DSS compliance is useful. For a payment-focused overview from the merchant side, this resource also helps: https://www.suby.fi/post/what-is-pci-dss-compliance

Strong customer authentication and 3DS

Customers sometimes see extra verification steps and assume they’re just friction. Done well, they’re part of what keeps online payments workable at scale.

Modern mobile e-commerce payments use expanded data in EMV 3-D Secure, and that can reduce fraud by 40-60% compared to legacy transactions. Issuers using that richer data can also approve 85% more low-risk payments, which can cut cart abandonment by 10-15%, according to ETA expert insights on how consumers are making payments.

That’s an important tradeoff to understand. Better authentication doesn’t always mean more visible friction. In many cases, it means the system has enough context to let a legitimate payment pass without visible friction.

Security should remove bad transactions without making good customers prove too much.

Chargebacks and disputes

Every online business needs a working process for disputes.

A few habits make a big difference:

- Use clear descriptors: customers should recognize the charge.

- Keep renewal messaging visible: recurring billing should never feel surprising.

- Store fulfillment evidence: access logs, invoice records, and usage data matter.

- Respond consistently: dispute handling works better when it follows a repeatable workflow.

The goal isn’t to eliminate every dispute. It’s to avoid preventable ones and handle the rest without chaos.

What a good payment setup changes

When a payment platform handles card security controls, authentication flows, and dispute tooling well, your team spends less time treating payments as a separate compliance project.

That is the ultimate win. Security stops being an obstacle course and becomes part of the operating system of your business.

How to Integrate Payments into Your Business

Integration choice usually comes down to one thing. How much control do you need, and how fast do you need to launch?

Some businesses just need a link they can send today. Others want a branded checkout in their app. Developer-heavy teams usually want direct control through APIs and webhooks.

Payment links for fast deployment

Payment links are the fastest way to start accepting money online.

They work well for:

- Freelancers sending invoices

- Agencies charging clients across borders

- Creators selling access to a product or service

- Small teams testing a new offer without engineering work

The main advantage is speed. You don’t need a custom front end to validate demand.

Embedded checkout for a cleaner customer experience

An embedded checkout keeps the payment flow inside your site or product experience.

That usually makes sense when:

- your brand matters at the point of payment

- you want fewer redirects

- your product delivers access immediately after purchase

- you need a more consistent handoff between app state and payment state

This model gives you more control without requiring a full custom payments build from scratch.

API and webhooks for custom logic

If payments are central to your product, API-based integration is usually the right path.

That setup is better when you need to:

- trigger access after successful payment

- listen for subscription renewals, failures, and cancellations

- sync payment events into your own app logic

- manage custom billing states or internal entitlements

For many software teams, that’s where payment infrastructure starts to feel like product infrastructure.

Matching the integration to the business model

Here’s a practical way to decide:

| Business type | Best starting point | Why |

|---|---|---|

| Freelancer or consultant | Payment link | Fast setup, low complexity |

| SaaS or web app | Embedded checkout or API | Better control over user flows |

| Community or membership business | API or native community integration | Access control matters as much as payment |

Suby provides an API that allows any business to accept payments by card or crypto, and it also offers paylinks, an embeddable checkout, and native integrations with Discord and Telegram for subscriptions, paid access, and online communities. In that model, users pay with cards or supported crypto, and businesses receive USDC. If you want a broader walkthrough of card acceptance options, this guide is relevant: https://www.suby.fi/post/how-to-accept-credit-card-payments

The right integration is the one your team can operate reliably after launch, not the one that looked most flexible in a product demo.

The Nuances of Subscription and Recurring Payments

Recurring revenue businesses don’t just process payments. They manage a continuing relationship between billing, product access, and retention.

That changes the payment conversation completely. A one-time purchase can survive a little friction. A subscription business can’t.

Failed payments are a revenue problem

In electronic commerce payments, failed payment rates often range from 6-10% globally, creating $30-50 billion in annual revenue leakage. Intelligent retry logic can improve recovery by 20-30%, according to Antom’s guide to e-commerce KPIs and metrics that help reduce failed payments.

That’s why payment operations belong in the revenue stack, not only in finance.

A failed renewal might happen because of an expired card, insufficient funds, fraud controls, or a temporary issuer issue. The customer may still want the product. If your system gives up too early, you lose revenue that was recoverable.

Dunning needs to be deliberate

Dunning is the process of retrying failed subscription charges and communicating with the customer in a structured way.

Good dunning usually includes:

- Retry timing: don’t hammer the same card repeatedly without a plan.

- Customer messaging: tell the user what happened and what to do next.

- Access rules: decide whether to pause access immediately or after a grace period.

- Recovery visibility: track which failures are being saved.

If you’re comparing platform approaches, this overview of recurring payment systems is a helpful reference point for thinking through the operational side.

Subscription logic goes beyond charging a card

Recurring billing also has to handle all the awkward real-life moments:

- an upgrade in the middle of a billing cycle

- a downgrade at renewal

- a pause for a seasonal user

- a failed renewal followed by successful recovery

- access revocation when billing finally stops

Each one is a product event and a payment event at the same time.

A subscription system should answer two questions clearly: did the payment succeed, and what should happen to access now?

That’s why recurring payments need more than a basic checkout. They need lifecycle logic that protects revenue without creating support chaos.

Building a Modern Global Payment Infrastructure

A founder in Berlin sells to customers in Brazil, Nigeria, and the US. Checkout works. Revenue shows up on the dashboard. Then the harder part starts. Funds arrive days later, conversion fees chip away at margin, finance has to reconcile mismatched amounts, and support gets questions about missing payouts.

That is the fundamental design problem in global electronic commerce payments. Accepting money is only the front door. The back office determines how much operational drag your team carries after every sale.

What to optimize for now

Legacy cross-border payment flows were built around correspondent banking, batch settlement, and multiple intermediaries. That structure creates three common headaches for internet businesses: slow access to funds, limited visibility into FX costs, and payout paths that vary by country.

For a global company, those are not edge cases. They affect cash planning, pricing, support workload, and how confidently you can enter new markets.

A better model keeps the customer side familiar and modernizes the settlement side.

That usually means customers still pay with methods they already trust, such as cards, while the merchant receives a faster, more predictable digital settlement outcome. If you want a practical overview of that model, this guide on how to accept international payments for online businesses explains the tradeoffs clearly.

Stablecoin settlement matters here for a simple reason. It removes several pieces of the old chain. Instead of waiting for funds to move through banking layers in different currencies, the business can receive value in USDC with clearer timing and less ambiguity around what will arrive.

A simple provider checklist

A good global payment stack should reduce manual finance work, not hide it behind a clean checkout.

When you evaluate providers, ask:

- Checkout fit: Can buyers use payment methods they already recognize and trust?

- Settlement model: What asset or currency does the business receive, and how long does that take?

- FX handling: Where does conversion happen, and who absorbs the spread and fees?

- Cross-border coverage: Does the payout model stay consistent as you add countries?

- Recurring revenue support: Can the system support subscriptions, retries, renewals, and entitlement changes?

- Reconciliation workload: Will your finance team get clear records that match orders, fees, taxes, and payouts?

- Compliance and controls: Are KYC, AML, fraud checks, and audit trails built into the operating model?

The easiest way to judge this is to follow one transaction all the way to your bank or treasury account. If the path is hard to explain, it will be hard to operate at scale.

The practical conclusion

Many global internet businesses are moving toward a hybrid structure. The customer experience stays familiar. The merchant settlement layer gets rebuilt for speed, predictability, and simpler cross-border operations.

That is why card acceptance on the front end plus USDC settlement on the back end is getting attention. It solves an old problem in a practical way. Sales can remain local to the customer, while treasury operations become more consistent for the business.

If your company sells internationally, this approach can reduce payout delays, lower reconciliation effort, and make margins easier to understand.

If your business sells globally and wants a simpler payout model, Suby is one option to evaluate. It provides an API for accepting card and crypto payments, supports subscriptions and community access flows for Discord and Telegram, and is built around the core model that users pay with cards while businesses receive USDC.