You run a SaaS product, a digital service, or a paid community. Customers are already coming from different countries, but your payments stack still behaves like you only sell locally. One customer pays by card in one currency, another asks to pay in crypto, your gateway settles later than expected, and finance has to untangle what arrived, in what form, and when.

That mismatch is becoming harder to ignore. The global digital payment market was valued at USD 94.34 billion in 2022 and is projected to reach USD 317.27 billion by 2030, with a CAGR of 20.6% from 2023 to 2030, according to Data Bridge Market Research on the global digital payment market. More businesses are selling internationally, but many still rely on payment infrastructure built around local bank rails and fragmented payout systems.

The painful part isn't usually checkout alone. It's settlement. You can accept a payment successfully and still deal with FX exposure, payout delays, multiple processors, and extra operational work after the sale.

A global payment api is meant to solve that. It gives you one way to accept payments across regions and payment methods, then routes the complexity behind the scenes. And when settlement happens in USDC, the business side gets something traditional cross-border stacks often struggle to deliver: a clean, predictable unit for revenue.

Table of Contents

- Accept the payment methods customers already use

- Settle revenue in one stable output

- Subscriptions and community access need native support

- Start with the least custom option

- Move to embedded checkout when checkout is part of the product

- Use direct api integration for full control over payment logic

- A SaaS team selling subscriptions globally

- A paid community on Discord or Telegram

- A freelancer sending simple global invoices

- Do customers need to understand crypto to pay by card

- Does a merchant need a bank account to receive payouts

- Is card dispute handling still relevant if settlement happens in USDC

- How does pricing compare with traditional providers

- Can this work for subscriptions and online communities

Introduction The Challenge of Global Online Sales

A lot of online businesses hit the same wall in stages.

At first, international demand feels like a win. A customer from Germany signs up. Then one from Brazil. Then a client in Singapore asks for an invoice. Revenue is growing, but the payment stack starts showing its seams. Card acceptance works in one place, payouts happen somewhere else, and settlement lands in ways that make reconciliation harder than it should be.

The problem usually isn't that any one tool is broken. It's that each tool solves a narrow part of the payment journey. One provider handles checkout. Another handles subscriptions. Another helps with crypto acceptance. Your bank handles settlement. Your team handles the glue.

Where teams usually get stuck

Three issues show up again and again:

- Currency mismatch: Customers want to pay in familiar ways, but the business wants predictable revenue.

- Payout uncertainty: You know a payment was approved, but you still don't know exactly when usable funds will arrive.

- Operational sprawl: Every new country or payment method seems to require another integration, another dashboard, or another support process.

Practical rule: A payment flow isn't finished when the buyer clicks pay. It's finished when your business can use the funds without extra manual work.

This is why a global payment api matters. It isn't just a developer convenience. It's a way to replace a patchwork of regional tools with one programmable layer that can handle acceptance, routing, and settlement more cleanly.

For global businesses, that's the fundamental shift. You stop designing around bank friction and start designing around how internet sales function.

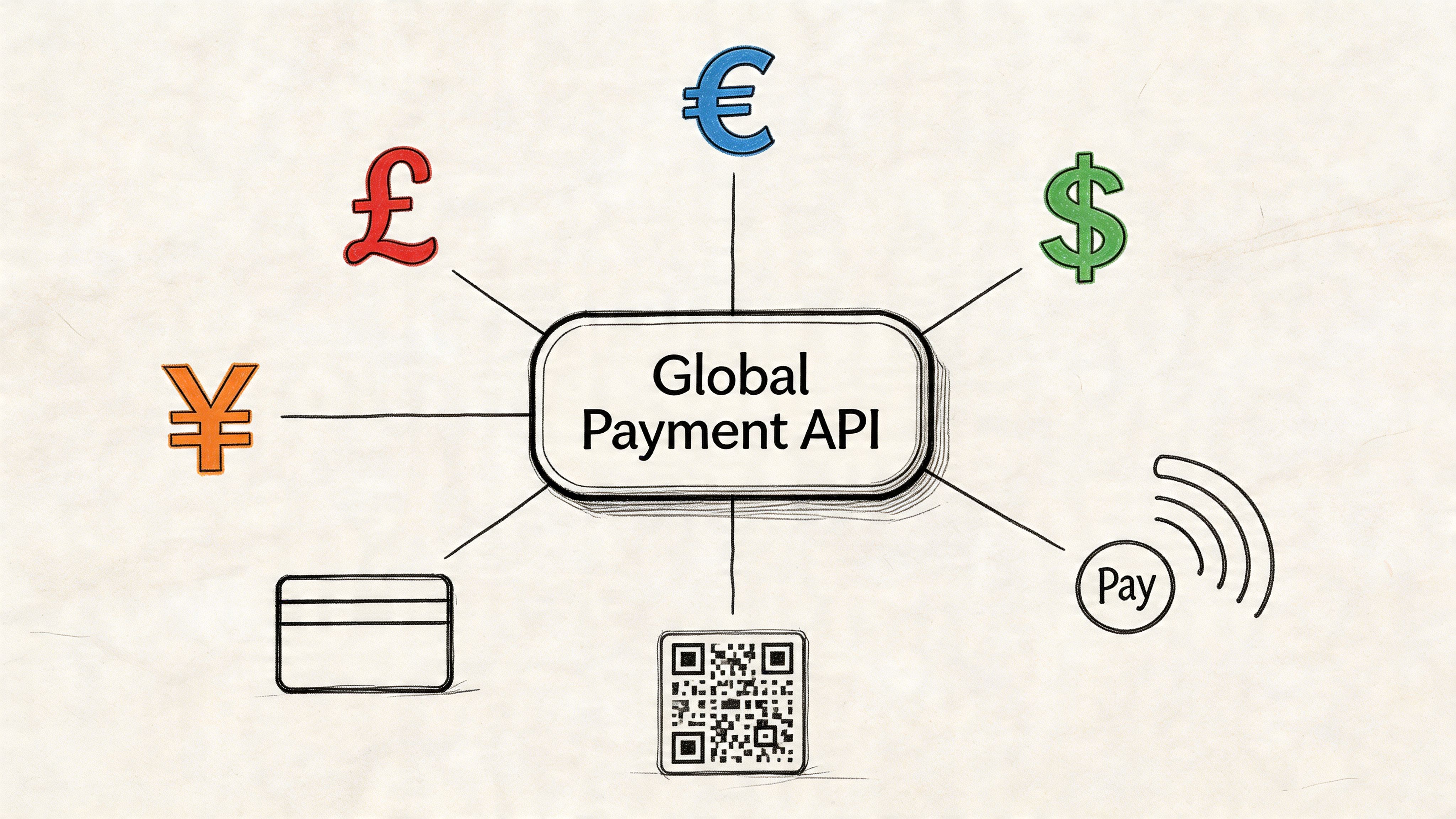

What Is a Global Payment API

A global payment api is a single integration layer that connects your business to multiple payment gateways, banks, and financial networks without forcing you to build separate integrations for each market. Stripe describes global payment APIs as unified platforms that consolidate access through one interface and abstract regional variation, so businesses don't need separate integrations for different countries, as explained in Stripe's overview of global payment APIs.

A simple way to think about it

Consider it a universal power adapter for money.

Your customer plugs in with the payment method they prefer. Your product doesn't need a different wall socket for every country. The api handles the translation layer so your system sees a consistent structure instead of dozens of country-specific rules and processor quirks.

That matters because payment systems vary in more ways than many realize. It's not just language or currency. It's also authorization rules, authentication flows, settlement expectations, and the shape of the underlying data.

A good global payment api gives your product a stable contract. Your team builds once against that contract, then expands by configuration instead of by rebuilding checkout logic each time.

If you're trying to understand the broader digital asset space customers may already be familiar with, Bitcoin market data on CoinStats is one example of the kind of resource product teams review when mapping user payment expectations across card and crypto experiences.

What sits behind the single integration

From a product perspective, the key benefit is abstraction. From an engineering perspective, the key benefit is interface design.

Instead of your team wiring up one processor for Europe, another for Asia, and another for creator subscriptions, the api becomes the layer your application talks to. That layer can expose predictable objects such as payments, customers, subscriptions, and webhooks.

Here’s the practical effect:

- Less custom regional logic: Your app doesn't need a different payment flow for every expansion market.

- Lower maintenance burden: When providers or regional rules change, you don't want that complexity pushed into your application code.

- Faster product iteration: Teams can focus on checkout UX, billing logic, and reconciliation instead of gateway plumbing.

A short explainer helps if you want to see the idea in motion:

The confusing part for many readers is this: a global payment api doesn't automatically solve every money movement problem by itself. It solves the integration problem first. Whether it also solves the settlement problem depends on the rails underneath it.

That distinction matters more than most generic guides admit.

The Two Worlds of Payment Settlement Rails

Two payment systems can look identical at checkout and behave very differently after the customer pays.

That difference lives in the settlement rail. One route ends in traditional banking infrastructure. The other ends in stablecoin settlement, such as USDC. If you're evaluating a global payment api, the important trade-offs become apparent.

Traditional settlement feels familiar but adds friction

Traditional cross-border settlement usually passes through multiple institutions. Even if the user experience looks modern, the backend often still depends on correspondent banking, regional processors, and currency conversion steps before funds become usable.

For a business, that creates several practical problems:

- Visibility gaps: A payment can be approved while finance still waits to see what settles.

- FX handling: Revenue may move through conversions at different points in the flow.

- Extra support work: When timing is unclear, customers and internal teams both ask the same question. Where's the money?

This is one reason cross-border operations get messy as you scale. More countries often means more exception handling, not just more sales. A useful companion read on this operational side is this guide to cross-border payment flows.

USDC settlement changes the last mile

Stablecoin settlement changes the backend logic. The customer can still pay with a familiar method, including cards, but the business receives settlement in USDC. That removes a lot of the ambiguity that usually accumulates after payment acceptance.

Instead of thinking in terms of "which bank account receives what, after which conversion, after which delay," the business can think in terms of a single settlement output.

When settlement is stable and uniform, finance work gets simpler. Your team spends less time translating revenue from one form into another.

This is the part many teams miss. They focus on acceptance because it's visible to customers. But settlement defines how your operations run.

Here is the difference in plain terms:

| Feature | Traditional Bank Rails (SWIFT) | Stablecoin Rails (USDC) |

|---|---|---|

| Settlement path | Moves through banking intermediaries | Moves on stablecoin rails to a wallet |

| Currency handling | Often involves multiple conversion points | Revenue settles in one stable unit |

| Payout timing | Can feel variable and bank-dependent | More predictable from an operational view |

| Reconciliation | Often split across bank and processor records | Easier to track against one settlement asset |

| Expansion overhead | More country-specific banking setup | Less dependence on local banking structure |

| Risk surface | Banking delays and opaque routing | Wallet and onchain operations become central |

A few readers get nervous at this point because "stablecoin" sounds like a customer-facing requirement. It doesn't have to be. The cleanest model is often this: users pay with cards, businesses receive USDC.

That separation is powerful. It preserves a familiar checkout for buyers while giving the merchant a more consistent settlement outcome.

Key Features for Modern Global Commerce

Once you understand settlement, the feature set of a modern global payment api makes more sense. The goal isn't to pile on payment options for their own sake. The goal is to reduce friction for the buyer while keeping the merchant side operationally simple.

Accept the payment methods customers already use

Most businesses shouldn't force a customer to learn a new behavior just to complete a purchase. If your customer wants to pay by Visa or Mastercard, checkout should support that. If another customer prefers crypto, that path should also exist when it fits the business.

The value of one api is that your product team can support both without building two unrelated systems.

A practical stack usually includes:

- Card acceptance: Useful for mainstream checkout and recurring billing.

- Crypto acceptance: Useful for customers who already hold digital assets and want to pay that way.

- Unified payment objects: So your backend doesn't have to branch into separate accounting logic every time the payment method changes.

For teams comparing approaches, this article on accepting crypto payments for business is helpful because it frames crypto acceptance as part of a broader commercial workflow, not a standalone novelty.

Settle revenue in one stable output

This is the merchant-side feature that matters most in practice. A flexible checkout is useful. A single settlement format is what keeps ops manageable.

If customers can pay by card or crypto, but your business still receives a fragmented mix of currencies and delayed bank transfers, you've only solved the front half of the problem. A cleaner model is one where payment methods vary on the customer side while merchant settlement stays consistent in USDC.

That gives product, finance, and support teams a simpler operating model:

- Product can design one billing experience.

- Finance can track revenue in one stable settlement asset.

- Support doesn't need to explain multiple payout paths to every merchant or creator.

Subscriptions and community access need native support

Online businesses rarely process only one-off payments. They need recurring subscriptions, renewals, failed payment handling, and access control.

That becomes even more important for creators and community operators. A payment system isn't very useful if someone pays successfully but still has to wait for a manual role update in Discord or Telegram.

A strong global payment api should support use cases like:

- Recurring subscriptions for SaaS plans, memberships, and retainers

- Shareable paylinks for invoices, simple checkout pages, or direct sales

- Native Discord and Telegram integrations for paid access and membership lifecycle handling

The best payment feature is often the one that removes an operational task your team used to do by hand.

This is also where the article's core positioning matters most: users pay with cards, businesses receive USDC. That model works well because it aligns a familiar buying experience with a simpler settlement workflow on the business side.

How to Integrate a Global Payment API

A practical integration starts with one question: what are you trying to control?

If your business sells across borders, the checkout form is only the visible layer. The harder part sits underneath. You need to collect payment from a buyer using familiar methods, confirm the result inside your product, and settle funds in a way that does not create extra FX risk or reconciliation work for finance. That is why many teams now design the integration around a simple goal: customers can pay in familiar ways, while the business settles in USDC.

Start with the least custom option

For early sales, invoices, and demand validation, paylinks are often the right first step. A paylink works like a ready-made checkout counter. Your team creates the payment page, sends it to the buyer, and starts accepting payments without building a full billing interface first.

This option is useful when engineering time is limited or when the product is still proving demand. It also reduces maintenance because your team is not responsible for every checkout screen, edge case, and device layout from day one.

Paylinks fit well when:

- You need to launch quickly: sales can start before a custom billing flow exists.

- Your payment flow is simple: one-time charges and basic subscriptions often do not need custom UX.

- You want a smaller implementation scope: hosted checkout reduces the amount of payment UI your team has to support.

Move to embedded checkout when checkout is part of the product

Embedded checkout is the next step for teams that care about conversion, branding, or in-app continuity. Instead of sending users to a separate hosted page, you place prebuilt payment components inside your own product.

A good comparison is buying versus assembling furniture. Paylinks are the finished table. Embedded checkout is a strong tabletop with prebuilt legs. You still choose where it goes and how it fits the room, but you are not cutting raw lumber yourself.

That tradeoff matters in global commerce. You keep more control over the buying experience while avoiding the work of rebuilding every payment state, validation rule, and error flow. If you are comparing these implementation choices, this guide to payment gateway API integration gives a helpful reference for how teams move from hosted flows to more embedded setups.

Use direct api integration for full control over payment logic

A direct api integration makes sense when payments are closely tied to your product logic. That usually includes custom billing rules, internal ledger updates, subscription lifecycle handling, marketplace flows, or automated access control after payment.

In this model, your application creates payment objects, stores the business context, and reacts to status changes from the payment provider.

Webhooks are the part that often trips people up. A webhook is a message sent from the payment system to your backend when an event happens. It works like a signed delivery notification. Your system does not need to keep asking, "did the payment succeed yet?" The provider sends the answer when the status changes.

A common flow looks like this:

- Your app creates a payment request

- The customer completes checkout

- The payment platform processes the transaction

- A webhook notifies your backend

- Your app updates access, billing status, or internal records

Here is a simple example of what a payment creation payload might look like conceptually:

{"amount": "49.00","currency": "USD","customer_email": "buyer@example.com","payment_method_types": ["card", "crypto"],"mode": "subscription","settlement_currency": "USDC"}The exact schema varies by provider, but the integration pattern stays consistent. Your backend sends clear intent. The payment system returns clear status events. Your application decides what to do next, such as granting access, retrying a failed renewal, or flagging the transaction for review.

The most important design choice for a global business is often the settlement model, not the front-end widget. If your buyers are spread across regions, card acceptance may still be the best way to maximize conversion. But settling the merchant side in USDC changes the back-office equation. It reduces exposure to currency swings, shortens the distance between payment and usable funds, and gives finance one settlement asset to reconcile instead of a patchwork of local outcomes.

That is the part many generic API guides skip.

Teams also need to protect account access around payment actions, especially for subscriptions, account changes, and admin approvals. Background reading on robust OTP verification methods can help when you are designing those surrounding security flows.

One provider in this category is Suby, which offers paylinks, embedded checkout, direct API access, subscriptions, card and crypto acceptance, and native Discord and Telegram integrations, with merchant settlement in USDC.

Security Compliance and Operational Realities

Payments live or die on trust. A product can have a clean API and still fail a real buyer if authentication breaks, refund handling is clumsy, or finance can't see what happened after the transaction.

Card security and authentication

For card payments, businesses need to know that sensitive card handling is managed through the right processing setup. In practical terms, that means the payment layer should rely on a PCI-DSS Level 1 certified processing partner when handling card flows, and it should support Strong Customer Authentication where required.

That matters for two reasons. First, it reduces direct exposure to card data. Second, it helps the business fit into payment environments where additional buyer authentication is part of normal checkout.

Security also extends beyond payment credentials. Many teams reviewing operational security also look at account access, user verification flows, and login protection. If you're comparing options around account confirmation and onboarding, this overview of robust OTP verification methods is a useful background resource.

Secure payments aren't only about preventing card theft. They're also about making sure the right user completes the right action at the right time.

Refunds disputes and internal controls

A modern payment system also has to handle the less glamorous parts well.

That includes:

- Refunds: Teams need a defined way to return funds without manual workarounds.

- Disputes: Card payments still exist inside card network rules, so dispute processes remain relevant even if merchant settlement happens differently.

- Two-factor authentication: Admin access should be protected, especially where payment settings or payout details can be changed.

- Dashboard visibility: Operators need real-time views into payments, subscriptions, churn, and payouts.

The biggest misconception here is that newer settlement rails remove operational discipline. They don't. They change where the complexity sits. You may remove bank delay uncertainty, but you still need clear controls for disputes, access changes, and transaction review.

Teams that plan for that early usually have fewer support problems later.

Real-World Examples with Suby

Theory helps, but payment architecture becomes clearer when you attach it to day-to-day use.

A SaaS team selling subscriptions globally

A SaaS company with customers in multiple regions wants one checkout for everyone. Some buyers are comfortable paying by card. Others prefer crypto. The product team doesn't want to build and maintain separate billing systems for each preference.

In this setup, the company uses embedded checkout for recurring plans. Customers pay in the way that's most convenient to them, while the business settles revenue in USDC. That makes the finance side cleaner because the team isn't juggling multiple payout outputs just because the customer base is global.

A paid community on Discord or Telegram

A creator or community operator has a more specific problem. Payment isn't the whole product. Access is.

They need users to pay, get added to the right community tier, keep access while the subscription is active, and lose access when it ends. If those steps happen in separate tools, someone ends up doing manual cleanup.

A global payment layer with native community integrations solves that by tying payment status to access control. For teams thinking carefully about user communication and delivery channels around these flows, it also helps to understand the safety and encryption of communication channels because support messages, alerts, and membership notifications are part of the overall trust model.

A freelancer sending simple global invoices

A freelance designer in Asia invoices a client in the US. Traditional wires often create the same pattern of uncertainty. The client asks whether the invoice was received. The freelancer waits. The bank records arrive later than the actual business conversation.

A paylink changes the flow. The client gets a direct checkout link, pays with a familiar method, and the freelancer receives settlement in USDC without waiting on a long chain of banking intermediaries. The result isn't just faster feeling. It's easier to reason about.

These examples look different on the surface, but the underlying model is the same. Checkout should be flexible for the customer. Settlement should be simple for the business.

Conclusion The Future of Internet-Native Commerce

Internet-native businesses don't sell into one market anymore, even when they start small. Their payment systems need to reflect that reality.

A strong global payment api helps by reducing integration sprawl, supporting familiar customer payment methods, and making global checkout easier to operate. The bigger shift comes from settlement. When businesses receive USDC, they avoid much of the FX confusion, payout uncertainty, and operational drag built into older cross-border setups.

That's why this model fits modern commerce so well. Users can pay with cards or crypto. Businesses can receive revenue in one stable output. Teams spend less time managing payment edge cases and more time building the product.

The companies that adapt fastest won't just accept international payments. They'll run on infrastructure designed for international business from the start.

Frequently Asked Questions

Do customers need to understand crypto to pay by card

No. A customer paying by card can complete checkout in a familiar way without managing a wallet or understanding onchain mechanics. The stablecoin part can stay on the settlement side for the business.

Does a merchant need a bank account to receive payouts

Not necessarily. In a USDC-settlement model, the merchant receives revenue to a wallet rather than relying on traditional bank payout rails. That changes the operating model from bank-account settlement to wallet-based settlement.

Is card dispute handling still relevant if settlement happens in USDC

Yes. If the customer pays by card, card-network dispute processes still matter. Settlement format and checkout method are related, but they aren't the same thing. Businesses still need a clear workflow for chargebacks and evidence handling.

How does pricing compare with traditional providers

The key difference is transparency. Some modern providers use an all-inclusive fee model, while traditional stacks often distribute costs across processing fees, FX spreads, payout friction, and operational overhead. The right comparison isn't only the posted fee. It's the total cost of getting usable revenue into the form your business prefers.

Can this work for subscriptions and online communities

Yes. A global payment api can support recurring subscriptions and, in some products, direct integrations with platforms like Discord and Telegram for paid access and membership management.

If you want to see a practical implementation of this model, Suby is worth reviewing. It provides an API for businesses to accept payments by card or crypto, supports paylinks, embedded checkout, subscriptions, and native Discord and Telegram integrations, and follows the model discussed throughout this article: users pay with cards, businesses receive USDC.