A payment gateway is the tech that securely grabs a customer's payment details from your website and shoots them over to the payment network to get processed. Think of it as the digital doorman for your online store, connecting you to the financial world.

What Is a Payment Gateway and Why Does It Matter

When a customer hits that "Buy Now" button, a whole lot happens in the blink of an eye. Right in the middle of it all is the payment gateway, acting as a secure messenger to make sure sensitive financial data gets from point A to point B without a hitch.

Imagine your online store has a super-smart, multilingual cash register. This isn't just a simple till; it checks if the customer's card is real, sniffs out potential fraud, and talks to different banks to make sure there are enough funds for the purchase. That’s pretty much what a payment gateway does for every single online sale.

The Key Players in Every Transaction

To really get why this matters, you need to know who's involved when money changes hands online:

- The Customer: The person buying something from your site or app.

- The Merchant: That’s you! The business getting paid for a product or service.

- The Issuing Bank: The bank that gave the customer their credit or debit card.

- The Acquiring Bank: Your bank, which takes the payment on your business’s behalf.

The payment gateway is the secure go-between, making sure all these players can talk to each other in just a few seconds. It encrypts the customer's card info, sends it through the card networks to their bank for an okay, and then zips the approval or decline message right back to your website.

Security and Trust at the Core

This role as a secure messenger is its most important job. You can't overstate the importance of a payment gateway when you consider the strict PCI DSS compliance requirements and best practices that exist to protect payment data. By taking on this responsibility, the gateway lifts a massive security and compliance weight off your shoulders. You get to accept payments without having to store or handle sensitive cardholder details yourself.

A payment gateway is more than just a piece of technology; it's the foundation of trust in e-commerce. It assures customers that their financial details are safe while giving merchants the confidence that they will be paid securely and reliably.

The world runs on this technology. The global payment gateway market is expected to rocket to somewhere between USD 90.28 billion and USD 114.30 billion by 2030-2034. That number alone shows just how central it is to the entire digital economy.

For any online business—whether you're a solo creator selling digital art or a massive SaaS company—a solid payment gateway isn't just a nice-to-have, it's a must. It's the engine that drives your revenue, and picking the right one has a huge impact on your ability to sell internationally, manage your cash flow, and ultimately, build a thriving business.

How a Transaction Actually Flows Through a Payment Gateway

So, what really happens when a customer hits that "Buy Now" button? It feels instant, but behind the scenes, a lightning-fast sequence of events kicks off, all orchestrated by the payment gateway. This entire journey is broken down into two core stages: authorization (getting the thumbs-up) and settlement (moving the cash).

Let's walk through a single transaction to see how it all works. You'd be surprised at the complex dance that happens in just a couple of seconds.

The Authorization Stage: Getting the Green Light

First things first, we need to know if the customer actually has the money. This is the authorization stage, and it happens in a flash. The gateway is essentially asking the customer's bank, "Is this person good for the money?"

Here’s how it unfolds step-by-step:

- Encryption: The moment your customer enters their card details, the gateway springs into action, encrypting everything. Their card number, expiration date, and CVV are scrambled into a secure, unreadable code before it goes anywhere.

- Routing: The gateway shoots this encrypted bundle over to the payment processor. The processor then acts like a traffic cop, directing the request to the right card network—think Visa or Mastercard—which in turn passes it along to the bank that issued the customer's card.

- Approval or Decline: The issuing bank takes a look. It checks for sufficient funds, confirms the card details are right, and runs its own fraud detection scans. Based on this split-second analysis, it sends back a simple response: approved or declined.

- Confirmation: That response zips back along the same path: from the issuing bank, through the card network, to the processor, and finally back to the payment gateway. The gateway then tells your website the final verdict, and your customer sees either a confirmation message or an error.

This whole authorization handshake is a critical security step. It makes sure the payment is legit before you ship a product or grant access to a service.

The diagram below gives you a bird's-eye view of this flow, showing how the gateway sits right in the middle, connecting your business, your customer, and the banks.

As you can see, the gateway is the secure messenger making sure everyone is on the same page.

The Settlement Stage: Moving the Money

Okay, so the transaction was approved. But here's the kicker: no money has actually changed hands yet. That's what settlement is for.

Settlement is the process of actually collecting the authorized funds from the customer's account and dropping them into the merchant's account. Authorization is the promise; settlement is the delivery.

Instead of moving money for every single purchase, transactions are usually bundled up. At the end of the day, the payment gateway sends a batch of all your approved authorizations to your acquiring bank. From there, the acquiring bank collects the money from all the different customer banks and deposits it into your merchant account. This usually takes a few business days to complete.

Handling Refunds and Chargebacks

What about when money needs to flow the other way? The gateway handles that, too. When you need to issue a refund, the gateway initiates the process, pulling funds from your merchant account and sending them back to the customer's card.

It also plays a central role in managing chargebacks, which happen when a customer disputes a transaction with their bank. The gateway helps pass information back and forth between you and the bank to resolve the claim.

This is where modern solutions are changing the game. With Suby, our API lets businesses accept card payments just like any other gateway. Your customers get the same smooth checkout they're used to. The big difference? You receive your settlement funds directly as USDC, cutting through the complexities of traditional banking and giving you faster, more direct access to your revenue.

Choosing the Right Type of Payment Gateway

Not all payment gateways are built the same. Picking the right one really boils down to your technical know-how, the kind of checkout experience you want for your customers, and your overall business model. Figuring out the main integration styles is the first step to finding the perfect match.

There are really three main flavors of payment gateways: hosted gateways, API-driven gateways, and the more modern paylinks. Each one has its own give-and-take between brand control, how much work it is to set up, and how smooth the experience is for your customer. Let's dig into how each one works in the real world.

Hosted Gateways: The Simple Redirect

A hosted payment gateway is probably the most straightforward way to get up and running. When a customer hits the "buy" button, they're whisked away from your website to a secure payment page that lives on the gateway provider's servers. Once they've paid, they're sent right back to your site.

This method is super popular because it offloads the heavy lifting of security—especially PCI DSS compliance—onto the provider. Since you aren't touching or storing any sensitive card data on your own systems, your compliance headache gets a lot smaller.

But that simplicity does have a downside. Bouncing customers to another site can feel a bit jarring and might even cause some people to abandon their carts if the handoff isn't seamless. You also lose a ton of control over the branding and design of the checkout page, which can mess with your brand's consistent feel.

API-Driven Gateways for Full Control

If you're after a completely seamless, branded checkout experience, then an API-driven gateway is what you need. This approach, sometimes called an integrated or embedded gateway, lets you build the entire payment form right into your website or app using the provider's API.

The customer never leaves your site. It’s a clean, professional journey from start to finish. This gives you total command over the design and flow of your checkout, making it the go-to for serious e-commerce stores and SaaS companies who live and die by their user experience.

The trade-off for all that control is more technical responsibility. Your developers will have to build and maintain the integration, and your PCI compliance burden could be significantly larger depending on how you implement it.

Platforms like Suby, for instance, offer a powerful API that lets you build a custom flow for accepting both card and crypto payments. Developers can craft a unique experience, and the merchant gets settled in USDC.

No-Code Paylinks for Speed and Simplicity

The third option, which has become incredibly popular, is the no-code paylink. A paylink is just a simple, shareable URL that directs a customer to a ready-made checkout page. You can pop these links in an email, a social media post, or a direct message—no website required.

Paylinks are unbelievably flexible. Think about the possibilities:

- Invoicing: A freelancer can send a client a direct link to pay an invoice. Simple.

- Social Selling: A creator on Instagram can sell a digital product with a link in their bio.

- Paid Communities: Someone running a Discord server can sell access with a simple payment link.

This approach takes zero coding and gets you to market almost instantly. It doesn't have the deep, custom feel of an API, but for quick, direct sales, it’s a seriously powerful tool. If you want to dive deeper into the world of global payments, you can learn more about choosing the best international payment gateway in our guide.

Why Traditional Gateways Struggle with Global Payments

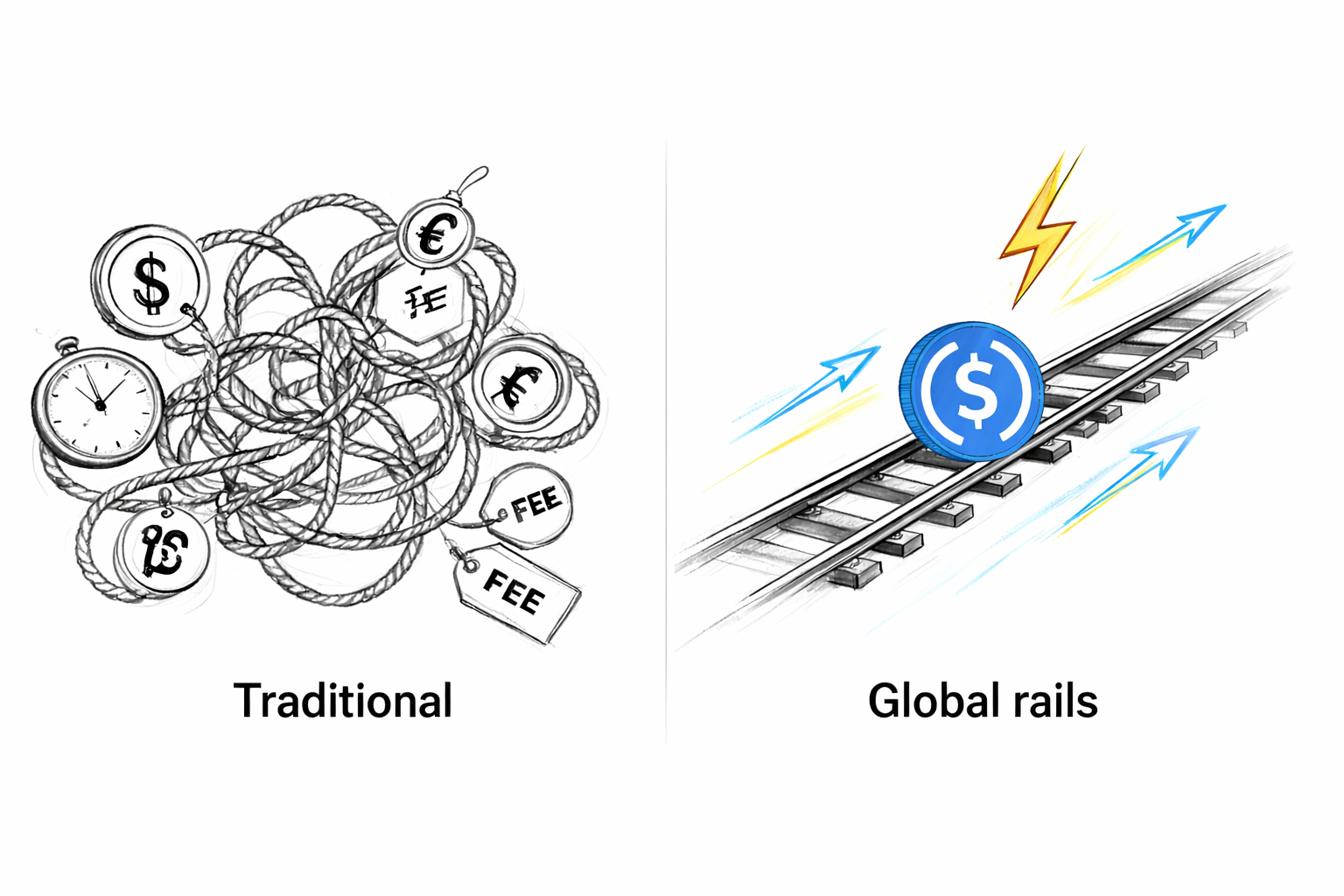

When you start selling to customers around the world, a payment gateway seems like the obvious first step. The problem is, most traditional gateways were designed for a different time—an era of domestic banking. This old-school architecture creates a lot of friction when you start operating on a global stage.

This isn't just a small annoyance; it's something that can directly hit your revenue and make operations a nightmare. The fundamental issue is that these systems simply weren't built for the borderless nature of the internet. They depend on a tangled web of correspondent banks, currency conversions, and regional rules that slow everything down and pile on unexpected costs.

The Hidden Costs of Currency Conversion

For any international merchant, the most immediate pain point is currency conversion. Imagine a customer in Japan pays in Yen, but your business account is in Euros. A traditional gateway has to handle that exchange, and believe me, it’s rarely free or transparent.

Gateways typically tack on a foreign exchange (FX) fee, which is a percentage markup on top of the daily market rate. This fee can run anywhere from 1% to 3%, sometimes more, and it comes directly out of your profit margin. Over thousands of transactions, that really starts to add up.

Beyond the obvious fees, the exchange rates they give you can be less than ideal. Gateways often use their own internal rates, which might not be the best available on the market, creating another hidden cost. If you're running on tight margins, this constant financial leak makes it incredibly difficult to price your products competitively in different countries.

Unpredictable Settlement Times and Cash Flow

Another huge headache is just how unpredictable settlement can be. With a domestic sale, you might see the money in your account in a couple of days. But for international payments? That timeline can stretch out dramatically.

The money has to hop between multiple banking systems, each with its own processing times, holidays, and cutoff periods. A payment from a customer in Australia to a business in Germany could easily take five to seven business days or even longer to finally land. This creates a serious cash flow problem.

You've made the sale, your customer has the product, but your money is stuck in transit somewhere in the global banking network. This delay ties up working capital and makes financial planning a constant guessing game.

This uncertainty means businesses have to keep more cash on hand just to cover day-to-day expenses while they wait for their revenue to arrive. It’s a frustrating and inefficient way to manage a global business.

Introducing the Global Payment Layer

To solve these exact problems, a new model has emerged: the Global Payment Layer. Instead of depending on the slow, expensive legacy banking rails for settlement, this approach uses modern, stable currency rails like USDC.

This changes everything. A global payment layer lets your customers pay in their local currency with their card, just like they always do. But on the back end, the settlement happens almost instantly, without the usual cross-border friction.

Here's why this new approach is a game-changer:

- Instant Settlement: Your revenue is settled in USDC, often within minutes, not days. This gives you immediate access to your funds and dramatically improves your cash flow.

- No Currency Risk: By getting paid in USDC, you're holding a stable digital dollar. You're no longer at the mercy of daily fluctuations in various foreign currencies, which simplifies your accounting and protects your profits.

- Simplified Treasury: Forget about juggling multiple currency balances in different bank accounts. You can have a single, unified treasury in USDC, making it far easier to manage global revenue.

This is exactly what we built at Suby. We provide a powerful API and simple integrations that let any business accept payments by card or crypto. Your customers get the smooth checkout they expect, while your business gets fast, predictable USDC payouts. It’s designed to take the headaches out of global payments for good.

Feature Comparison Traditional Gateway vs Global Payment Layer (Suby)

.tbl-scroll{contain:inline-size;overflow-x:auto;-webkit-overflow-scrolling:touch}.tbl-scroll table{min-width:600px;width:100%;border-collapse:collapse;margin-bottom:20px}.tbl-scroll th{border:1px solid #ddd;padding:8px;text-align:left;background-color:#f2f2f2;white-space:nowrap}.tbl-scroll td{border:1px solid #ddd;padding:8px;text-align:left}FeatureTraditional Payment GatewayGlobal Payment Layer (Suby)Settlement Speed5-7+ business days for international transactionsNear-instant settlement in USDC (minutes)Currency ConversionMandatory FX conversion with fees of 1-3% or moreNo forced FX conversion; receive stable USDCCurrency RiskExposed to volatile exchange rate fluctuationsEliminated; hold a stable asset pegged to the US dollarCross-Border FeesMultiple hidden fees from correspondent banks and networksMinimal network fees, transparent and predictableCash FlowUnpredictable, ties up working capital for days or weeksGreatly improved; immediate access to fundsTreasury ManagementComplex; requires managing multiple currency accounts and balancesSimplified; a single, unified treasury in USDC

As you can see, the choice directly affects your bottom line and operational agility. A global payment layer is fundamentally designed to remove the borders and delays that are built into the traditional financial system, giving you a much more efficient way to operate internationally.

How Suby Delivers Modern Global Payments

If you’re running a modern online business, you’re likely operating on a global scale. The problem is, most payment systems were built for a single country, leaving you stuck with legacy infrastructure that holds you back. Suby offers a completely new way of thinking about this—a global payment layer built from the ground up to solve the cross-border headaches that plague so many merchants.

The idea is refreshingly simple: your customers pay with their card, just like they always do, and your business receives stable, predictable USDC.

This model completely sidesteps the slow, expensive, and frankly outdated network of correspondent banks that traditional gateways depend on. Instead of waiting days for funds to clear while losing a chunk of your revenue to hidden currency conversion fees, you get fast, transparent settlements. It’s a game-changer for businesses expanding into new markets where local banking can be a tangled, unpredictable mess.

This shift couldn't be more timely. The global center of commerce is changing. The Asia-Pacific region, for example, is now the world’s dominant and fastest-growing payment gateway market, driven by massive e-commerce adoption across an area with more than half the world's population. For any business trying to capture a piece of that growth, a payment solution that isn’t tied to Western banking systems offers a serious competitive edge. You can dig deeper into how regional trends are shaping payment infrastructure on Mordor Intelligence.

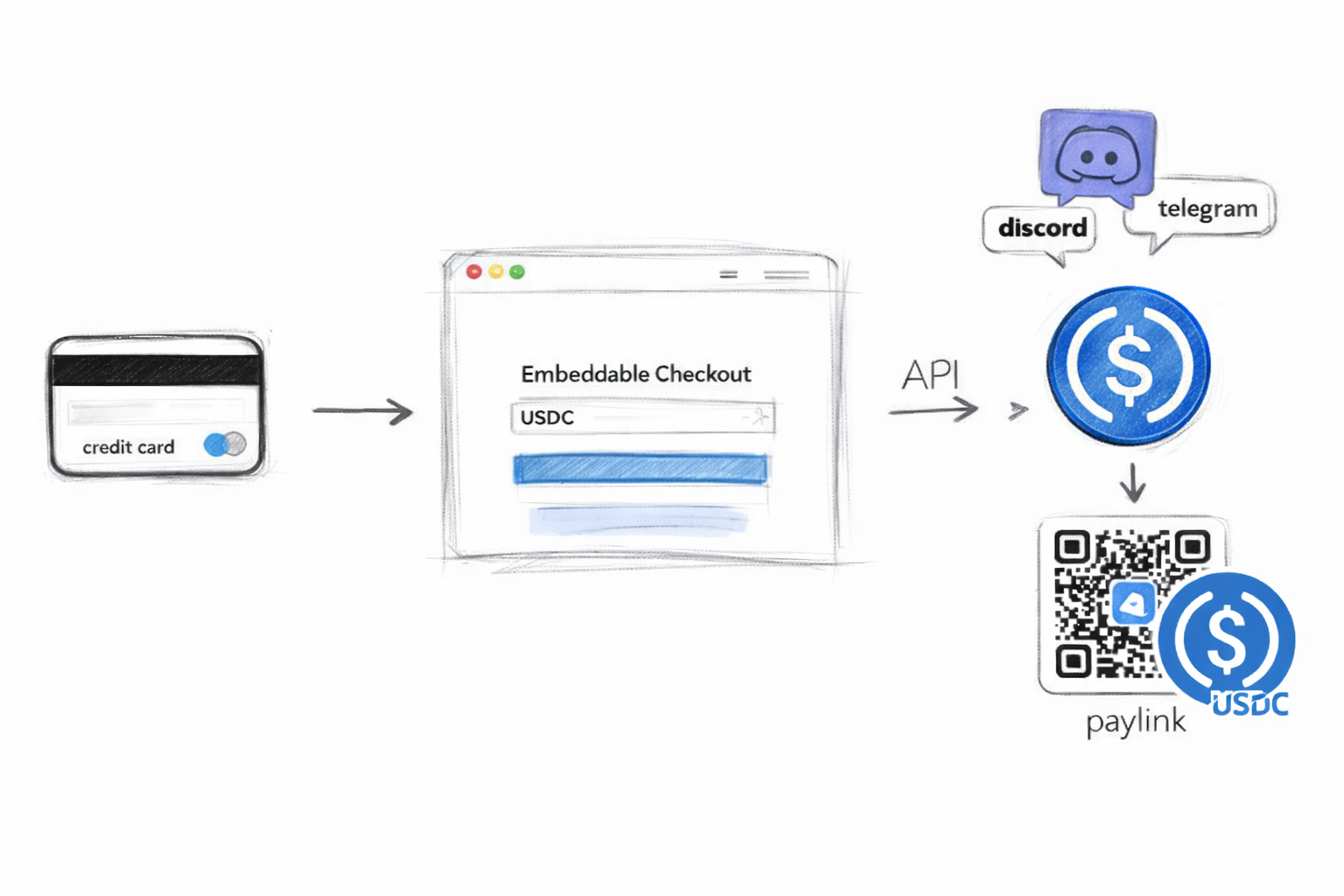

Flexible Integration for Any Business Model

Suby gives you several ways to get started, so you can pick the one that fits your technical comfort level and business model. This flexibility means that whether you’re a developer, a creator, or an e-commerce owner, you can plug into a global payment gateway without all the usual friction.

Here’s a look at the main integration options:

- A Powerful API for Developers: For businesses that need total control, Suby provides a clean, straightforward API. It lets your developers build custom payment flows directly into websites, web apps, or mobile applications for a completely seamless checkout experience.

- Embeddable Checkout: Don't have a dev team on standby? You can drop a conversion-optimized checkout widget directly onto your website with just a few lines of code. It gives customers a clean, on-site payment experience without needing a big development project.

- No-Code Paylinks: For the quickest setup imaginable, you can create and share simple payment links. They’re perfect for invoicing clients, selling on social media, or taking one-off payments when you don’t even have a website.

The real beauty of this is that the customer's experience never changes. They use their Visa or Mastercard like normal, completely unaware of the sophisticated mechanics happening on the backend that give your business the efficiency of USDC settlement.

Built for Creators and Online Communities

Suby isn’t just for standard e-commerce. It also has native integrations designed specifically for the creator economy. Anyone who has tried to manage a paid community knows it often means duct-taping multiple tools together. Suby cleans up that entire workflow.

The platform includes direct integrations with Discord and Telegram—two of the biggest platforms for building online communities. This lets creators and community managers easily monetize their groups with subscriptions or one-time access fees. The system automatically handles payment processing, access control, and subscription events, so you can stop doing all that manual work.

Whether you're selling access to an exclusive Discord channel or a premium Telegram group, the payment gateway and community management are handled in one unified system. For more on this, check out our guide on how to accept crypto payments for your business.

Security and Transparency First

Of course, none of this matters without rock-solid security. Suby ensures all card transactions are processed through a PCI-DSS Level 1 certified partner, which is the highest security standard in the payment card industry. This means sensitive cardholder data is handled with top-tier protection, taking a huge compliance burden off your shoulders.

On the business side, the pricing is designed to be completely transparent. It starts at a clear percentage per transaction, with no hidden setup costs, monthly minimums, or convoluted fee structures that make it impossible to forecast your expenses. That clarity, combined with the real-world benefits of USDC settlement, makes Suby a predictable and efficient partner for any business ready to operate on a global scale.

Common Questions About Payment Gateways

Jumping into online payments brings up a ton of questions. Whether you're a business owner launching your first store or a developer trying to plug in a new payment system, getting the basics right is crucial. This section cuts through the noise to give you clear, straightforward answers to the most common questions we hear.

Think of this as your practical cheat sheet. We'll break down the jargon and explain the key differences between all the moving parts, so you can move forward with confidence.

What Is the Difference Between a Payment Gateway and a Payment Processor?

This is easily the biggest point of confusion out there. People use the terms interchangeably all the time, but a payment gateway and a payment processor have two very different jobs in a transaction.

The easiest way to think about it is this: the gateway is like the secure credit card terminal on a physical countertop. Its only job is to safely grab the customer's payment details from your website, encrypt them, and pass them along for approval. It’s the front door to the whole process.

The payment processor is the one working behind the scenes to actually move the money. It takes the info from the gateway and does the heavy lifting, communicating with the banks and card networks (like Visa or Mastercard) to shift the funds from the customer’s account to yours. In short, the gateway starts the conversation, and the processor handles the money transfer.

To put it simply: The gateway securely collects and sends the payment data. The processor actually executes the financial transaction. Some companies bundle these services, but they are still separate functions.

Knowing the difference helps you troubleshoot problems and understand what to look for in a provider. A great gateway delivers a smooth, secure checkout experience for your customer, while a great processor ensures the money lands in your account reliably and efficiently.

How Can I Ensure My Payment Gateway Is Secure?

Security isn't a feature, it's the absolute bedrock of any payment system. Your number one priority should be choosing a provider that is PCI DSS (Payment Card Industry Data Security Standard) compliant. This is the global security standard that anyone handling card data must follow.

Being PCI DSS compliant means a provider adheres to a long list of strict security rules designed to protect sensitive cardholder information. This drastically cuts down the risk of data breaches and fraud. You can get a deeper look into what this involves in our guide on what is PCI DSS compliance.

Another must-have security feature is tokenization. This process swaps a customer's real card number for a unique, non-sensitive "token." If that token is ever exposed, it's useless to a fraudster. The best part? The actual sensitive data never even touches your servers, which massively reduces your security and compliance headaches.

The simplest, most effective strategy is to just use a solution that handles all of this for you. For example, Suby processes all card payments through a PCI-DSS Level 1 certified partner, giving your business and your customers the highest level of security available.

Can Any Payment Gateway Handle International Payments?

Technically, yes, most gateways can process a card from another country. But how they do it is what really matters, and this is where traditional gateways often fall flat for global businesses.

The problems usually boil down to a few key things:

- High Currency Conversion Fees: When a customer pays in their currency and you get paid in yours, old-school systems often skim 1-3% off the top in hidden fees and give you a terrible exchange rate.

- Multi-Day Settlement Delays: It's not uncommon for international payments to take five to seven business days—or even longer—to actually show up in your bank account. That can be a real killer for cash flow.

- Increased Chargeback Risk: Different banking systems and confusing transaction descriptions on customer statements often lead to more disputes and chargebacks.

This is exactly the problem that modern, global-native payment layers are built to solve. With a solution like Suby, your customer pays with their card just like normal. But on your end, you get the funds quickly and predictably as USDC. This completely sidesteps the currency conversion mess and cross-border settlement delays.

How Do I Integrate a Payment Gateway into My Website?

The good news is that you don't have to be a hardcore developer to get started. Integration options are designed for a range of technical skills, so you can pick what works for you.

The three most common ways to integrate are:

- No-Code Paylinks: These are just simple, shareable links that take customers to a ready-made checkout page. It’s the easiest method by far—zero programming required. Perfect for sending invoices, selling on social media, or taking one-off payments.

- Embeddable Checkout: This lets you drop a payment form right onto your website by pasting in a small snippet of code. It gives customers a more seamless, on-site experience without you needing to build it all from scratch.

- Full API Integration: For total control and a completely custom experience, developers can use a provider's API (Application Programming Interface). This allows you to build the entire payment flow directly into your app, making it feel perfectly branded and seamless.

Suby offers all three of these options. This flexibility means that any business, from a solo creator to a big SaaS company, can tap into a modern global payment system. You can start with a simple paylink and graduate to a full API integration as your business scales—all while getting fast, reliable USDC settlements. Your customers get the familiar card payment experience they expect, and your business gets paid without the usual cross-border friction.

Ready to take the friction out of global payments? With Suby, your customers pay by card, and you receive fast, predictable USDC. Start accepting payments today.