You open your dashboard, see payouts paused or your account under review, and your stomach drops. Orders are still coming in, customers still expect delivery, and support gives you a generic request for documents that doesn't tell you what really happened.

A stripe frozen account problem feels personal when you're in it, but in practice it's a risk workflow. Stripe processed $1.4 trillion in total payment volume in 2024, up 38% from the prior year, and it freezes merchant accounts when its systems detect patterns that look risky, such as dispute activity or unusual transaction shifts, according to Shuttle Global's Stripe freeze guide. The hard part isn't just the review. It's that Stripe typically holds remaining funds for 90-120 days to cover potential chargebacks, which can drain the working capital a small online business needs to keep operating, as noted in that same Shuttle Global analysis.

The businesses that recover fastest usually do three things well. They stop reacting emotionally, they diagnose the exact freeze type, and they send one clean evidence package that answers the risk question directly. The rest of this guide follows that same sequence.

Table of Contents

- First 24 hours, establish the facts

- Next 48 hours, assemble one review package

- Required Documents for Your Stripe Appeal

- Protect cash flow while the review is open

- What usually makes things worse

- Can a permanently closed account be reopened

- How long can funds stay held

- What's the best way to improve your chances

- Should you switch providers after recovery

- What should you look for in an alternative

What to Do When Stripe Freezes Your Account

You log in expecting to check payouts. Instead, transfers are paused, support has sent a generic risk notice, and payroll or ad spend is now tied to money you cannot touch.

Start by treating the freeze as an operating incident. Emotional reactions create extra work and usually weaken the review. Stripe often acts on automated risk signals before anyone has read the full context of your business, so the first job is to get organized fast.

A familiar pattern looks like this: a store launches a successful campaign, volume jumps, then payouts stop. The founder reads it as fraud or closure. In many cases, the account is stuck in review waiting for identity documents, invoices, fulfillment records, or a clear explanation for the change in transaction behavior. If you understand how payment fraud detection systems flag abnormal payment patterns, the logic is easier to see, even when the freeze hits a legitimate business.

Focus on control in the first few hours.

- Stop improvising: Don't send multiple tickets with different explanations and scattered files.

- Preserve records: Export transactions, customer communication, dispute data, order status, and shipping or delivery proof before anything changes.

- Classify the problem: A reserve, a payout pause, and an account freeze create different risks and require different responses.

- Protect the customer side: If orders, renewals, or access may be delayed, tell customers early so confusion does not turn into chargebacks.

Practical rule: A frozen account is both a payments issue and a cash flow issue. If the money is concentrated inside one payment facilitator, the freeze exposes a structural weakness, not just a support problem.

That is why the first decision is bigger than the appeal itself. Yes, you need to respond to Stripe in a disciplined way. You also need a settlement design that does not leave working capital trapped inside a platform account whenever a risk model changes its mind. For merchants with thin cash reserves, direct-to-wallet USDC settlement solves a problem that no support queue can solve. It reduces dependency on delayed fiat payouts and gives finance teams more predictable access to cleared funds.

Reviewing PayPal's Acceptable Use Policy helps frame the broader issue. Different platforms use different rules, but the underlying model is similar: the payment facilitator holds broad discretion, controls payout timing, and can restrict access when activity falls outside its risk tolerance.

The mindset that works

Handle the freeze like a compliance review. Clear, consistent documentation gets better results than angry arguments about fairness.

Use this sequence:

- Identify the likely trigger

- Match the right documents to that trigger

- Explain the business model in plain language

- Show what changed and why

- Follow up on a set schedule

That process will not reverse every freeze. It does give you the best chance of a serious review while you work on the larger fix, reducing reliance on a payment model that can interrupt cash flow without warning.

Why Stripe Freezes Accounts and What It Means

Stripe's risk systems don't only look for obvious fraud. They also react to patterns that fall outside what the model expects from your account history.

That matters because legitimate businesses often look suspicious to a machine. High-volume creators, international subscription services, and cross-border B2B SaaS companies regularly trigger freezes because normal transaction patterns get misclassified as risk, especially when systems are tuned for domestic, low-frequency transactions, as described by Secure Global Pay's analysis of frozen and closed Stripe accounts.

If you've ever compared platform rules across payment providers, it's worth reading PayPal's Acceptable Use Policy explained by LA Law Group, APLC. Not because PayPal and Stripe are identical, but because it helps you see how broad platform discretion can be once a provider believes your activity falls outside its risk comfort zone.

The three patterns behind most freezes

Verification problems are the easiest to underestimate. A business name mismatch, old address, missing owner ID, or inconsistent bank details can trigger a review even if your sales are clean. Machines don't infer intent well. They see inconsistency and escalate.

Behavioral anomalies are the next bucket. Stripe's automated models commonly flag verification failures, high dispute rates, sudden spikes in transaction volume, mismatched IP geolocations, or inconsistent billing data, according to the resolution framework discussed in this YouTube breakdown of Stripe freeze recovery. If you want a practical look at how merchants monitor these signals earlier, this piece on payment fraud detection is useful background.

Growth without context catches a lot of otherwise healthy businesses. A successful ad campaign, a product launch, or a seasonal sales burst can look like fraud if the account history doesn't prepare the system for it.

Legitimate growth is still a pattern shift. Risk systems don't care whether the shift came from fraud or a successful campaign until someone adds context.

Later in the review, a human may see what happened. The freeze usually starts before that human context exists.

Not every hold is the same

Many merchants use "freeze" to describe several different situations. That's a problem because the response depends on the specific restriction.

- Payout hold: Payments may still process, but payouts are paused.

- Rolling reserve: Part of each payout is held back for a period.

- Full balance hold or account freeze: Access is restricted more broadly and the impact is usually much more severe.

A payout-specific hold can also come from banking-side issues, including ACH return codes or restricted bank statuses, which Stripe documents in its blocked bank account guidance for ACH Direct Debit. In those cases, the issue may be less about your product and more about the payout destination or bank verification trail.

This distinction matters because merchants waste time sending the wrong evidence. If the problem is entity mismatch, supplier invoices won't solve it. If the problem is a sales spike, generic ID documents won't be enough without context.

A good explainer can help if you're still sorting the categories in your head:

Your Immediate 72-Hour Action Plan

Monday starts with a healthy Stripe balance. By Tuesday afternoon, payouts are paused, support is vague, and payroll is due in three days. That is the moment to get structured. Fast action helps. Scattered action usually makes the review slower.

The first 72 hours are about two jobs. First, give Stripe a clean file they can review without chasing you for missing pieces. Second, protect cash flow outside the frozen rail, because the underlying problem is not only this hold. It is the payment facilitator model itself. When one platform sits between you and your money, your operating cash can disappear behind a risk review you do not control.

First 24 hours, establish the facts

Start with the account record, not assumptions.

Read the dashboard notice and every related email

Stripe often splits the story across different messages. The payout tab may show one restriction while email hints at the actual trigger.Write down the exact restriction

Note whether this is a payout pause, reserve, verification review, or full balance hold. That label determines what evidence belongs in your response.Export operating evidence immediately

Pull transactions, refunds, disputes, invoices, tracking data, customer communication, and support history. SaaS companies should also export subscription records, login activity, onboarding completion, and proof of service access.Build a dated timeline

Mark the day the issue started, then add anything that changed in the prior 30 to 60 days. Campaign launches, sudden volume jumps, new geographies, supplier changes, bank account updates, and product mix changes all matter.Freeze unnecessary edits on the account

Do not change entity details, payout bank information, or website language unless Stripe specifically asks for a correction. Random updates can make a simple review look like an identity mismatch.

A reviewer needs a consistent file. Give them one.

Next 48 hours, assemble one review package

I have seen legitimate businesses lose days because they answered in fragments. ID in one upload. Bank statement in another. Sales explanation in a third email. Reviews move faster when the file reads like it was prepared by operations, not improvised under stress.

Create one PDF with a short cover note at the front. Keep the order logical. Use clear filenames. If your legal name, trading name, or address changed at any point, explain the difference directly instead of hoping it goes unnoticed.

Include these items:

- Identity and entity records: Government ID, business registration, tax documentation, and beneficial ownership details if relevant

- Payout proof: Bank statement or bank letter showing that the payout account belongs to the same business or owner listed in Stripe

- Sales evidence: Customer invoices, order confirmations, product pages, refund policy, and terms that were live during the flagged period

- Fulfillment evidence: Tracking, delivery confirmation, onboarding records, usage logs, account activation records, or signed service confirmations

- Context memo: A concise explanation of what changed and why the pattern is legitimate

For physical goods, delivery proof usually carries the most weight. For software, digital access logs are stronger than polished screenshots. For services, dated client approvals and work records beat a generic proposal deck.

If the restriction starts to look less like a routine review and more like a likely closure, this guide on a Stripe banned account and what that usually means can help you separate recoverable cases from permanent ones.

Required Documents for Your Stripe Appeal

| Document Type | What It Proves | Pro Tip |

|---|---|---|

| Government-issued ID | The account owner is a real person tied to the business | Use a current document and make sure the name matches the Stripe profile exactly |

| Business registration document | The company legally exists | Highlight the registered name and address if the document is long |

| Tax or EIN proof | The business entity matches tax records | Include the most recent version you have |

| Bank statement | The payout account belongs to the same entity | Use statements that clearly show the business name and account details |

| Supplier invoices | You have a legitimate source of goods or services | Include recent invoices that line up with the products sold |

| Customer invoices or receipts | Transactions reflect real sales activity | Pick examples tied to the flagged period |

| Proof of delivery or service fulfillment | Customers received what they paid for | For SaaS, use access logs or onboarding records, not just screenshots |

| Refund policy and terms of service | Buyers were informed about core commercial terms | Submit the exact version visible during the flagged transactions |

| Explanation letter | You understand the trigger and can explain it clearly | Address the anomaly directly, such as a promotion, launch, or geography change |

Protect cash flow while the review is open

Do not wait for the appeal outcome before dealing with liquidity risk.

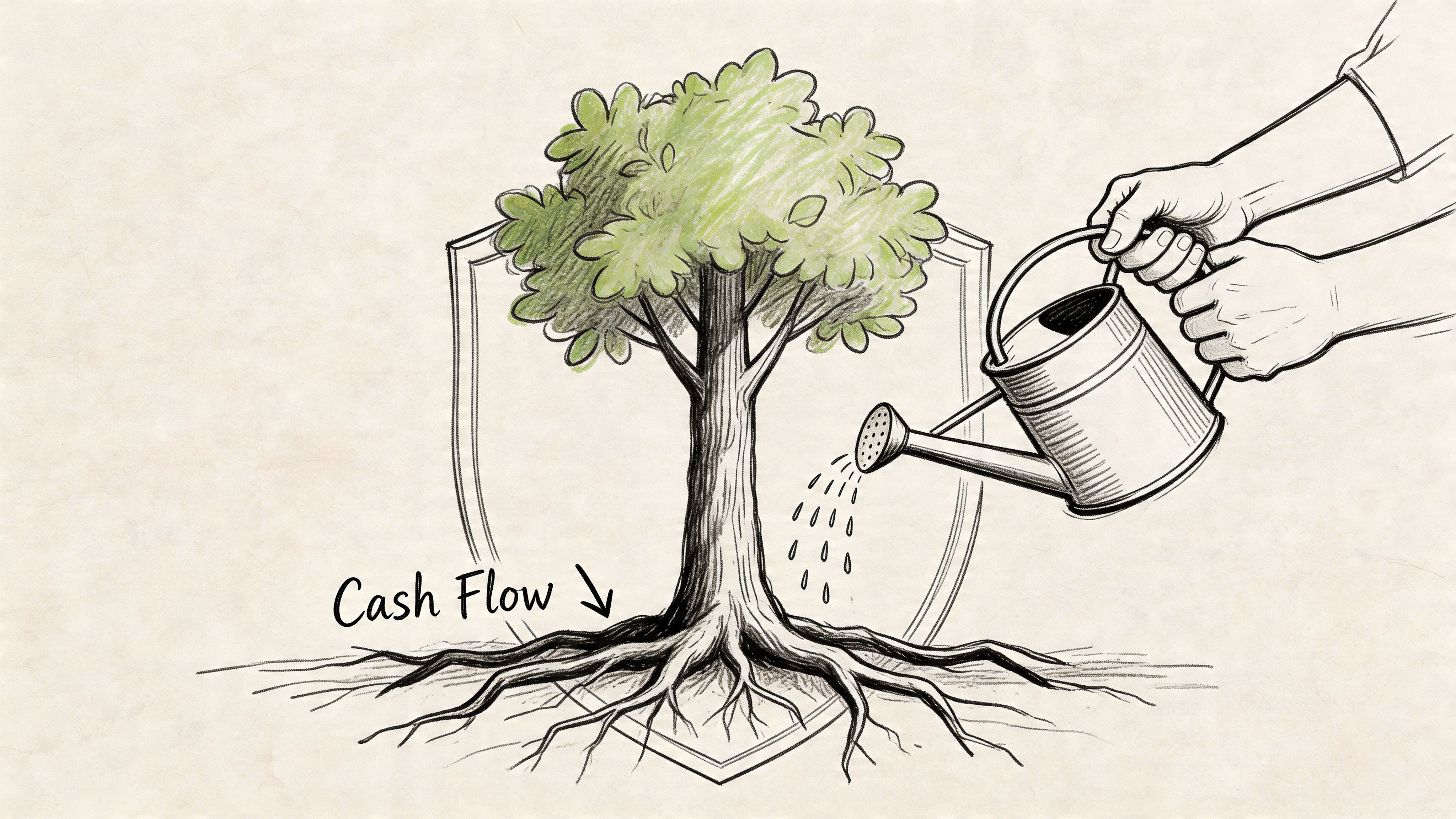

If Stripe is your only processor, the freeze has already exposed a structural weakness in your payment stack. A second acquirer can reduce concentration risk, but it does not solve the basic issue if that provider also controls settlement and can hold funds inside its own system. Businesses that need predictable access to revenue should start evaluating payment flows where settlement goes directly to their own wallet, with USDC received under their control rather than parked inside a facilitator balance.

That is a different operating model. It changes treasury, reconciliation, and sometimes customer checkout expectations. It also removes one of the biggest sources of cash flow uncertainty. If your business has already been burned by a freeze, that trade-off is worth serious attention.

What usually makes things worse

A few mistakes come up in almost every failed recovery attempt.

- Emotional emails: Frustration is understandable, but it does not answer the risk question under review.

- Evidence sent in pieces: Multiple uploads across different threads increase the chance that the reviewer misses something or waits for a cleaner package.

- Weak explanations: “Sales went up” is not enough. State which campaign ran, when it started, which countries it reached, and how fulfillment kept pace.

- Silence on complaints or disputes: If refunds, chargebacks, or fulfillment delays are part of the pattern, address them directly and show the correction.

- Assuming reinstatement solves the whole problem: Even if the account comes back, the underlying concentration risk remains.

The practical goal for these 72 hours is simple. Build a file Stripe can review quickly, and start reducing dependence on any single processor that can interrupt your operating cash overnight.

Communicating with Stripe and Escalating Your Case

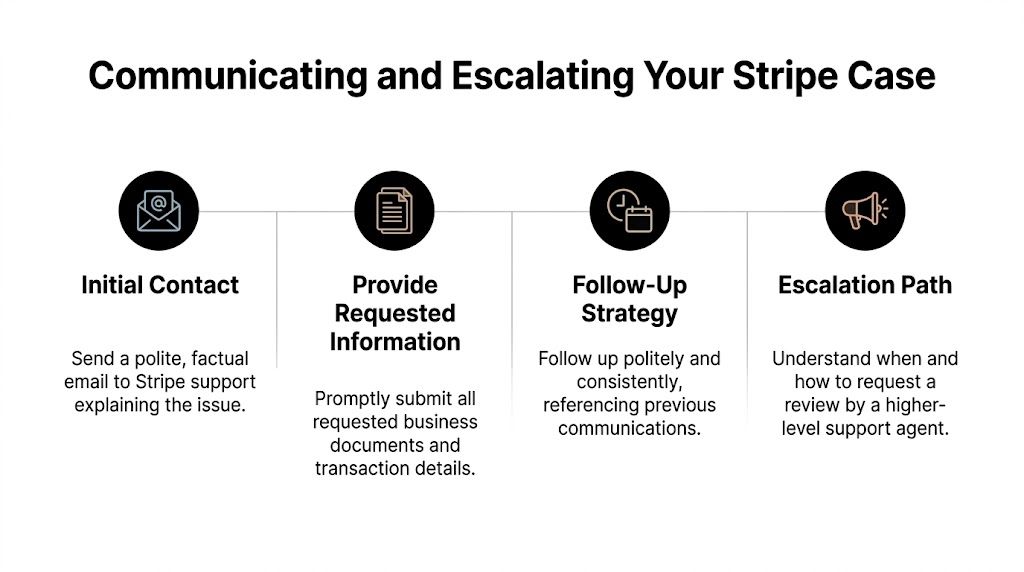

The tone of your communication affects the outcome more than most merchants think. Support won't reward anger, and long emotional emails often bury the evidence that matters.

A good message sounds like it came from an operations lead, not a panicked founder at midnight. Short paragraphs. Clear subject line. Direct response to the likely trigger. Attachments organized once, not scattered across a thread.

If your issue has moved from temporary hold toward a more severe restriction, this guide on a Stripe banned account helps frame the difference between a recoverable review and a likely closure.

How to write the first message

Use an opening paragraph like this:

Hello Stripe team, our account is currently under review and we want to provide a complete response to support your assessment. Based on the notification, we believe the trigger may relate to recent transaction pattern changes and verification review. We have attached a single document set containing identity records, business registration, bank verification, invoices, fulfillment evidence, and a summary of the volume change with supporting context.

That works because it does three jobs at once. It signals cooperation, shows that you understood the issue, and tells the reviewer the package is organized.

After that opening, keep the body tight:

- State the trigger you believe applies

- Explain the business activity behind it

- List the attachments in order

- Describe any corrective actions already taken

- Ask for confirmation that the case is with the right review team

When to follow up and when to escalate

Follow up politely every 48-72 hours if you haven't received a substantive response. That cadence is part of the commonly recommended resolution process in the same recovery framework discussed earlier, but the exact words still matter. Don't open fresh tickets unless the original thread is clearly dead. Multiple tickets create fragmentation.

A useful follow-up is simple:

I'm following up on ticket [number]. We submitted the requested documentation and would appreciate confirmation that the package is complete and under review. If any additional item is needed, please let us know and we'll provide it promptly.

Escalation makes sense when support repeats canned responses, asks for documents you've already sent, or goes silent after your package was delivered. At that point, ask for review by a higher-level risk or account specialist. Stay factual. Mention the operational impact, but don't turn the message into a rant.

Communication rule: Persistence helps. Pressure without structure doesn't.

Keep a log of every reply, attachment, and timestamp. If the case drags on, that record becomes your map. It also prevents you from re-sending conflicting versions of the same documents.

Preventing Future Account Freezes and Securing Your Cash Flow

The hidden cost of a frozen account isn't only the review itself. It's the uncertainty around payroll, supplier payments, ad spend, and customer delivery while someone else controls your settlement timing.

That burden is often missing from generic "contact support" advice. The operational and psychological stress of recovery timelines is real, and for creators and SaaS companies on thin margins, even a 2-week freeze can mean missed payroll, as highlighted in Chargeflow's discussion of Stripe payout holds.

What reduces risk inside the old model

If you're staying on a traditional payment facilitator, basic discipline still matters.

- Keep entity data current: Names, addresses, directors, and payout details should match across your documents.

- Prepare for spikes: If you know a launch or promotion is coming, assemble campaign context and fulfillment plans before the spike happens.

- Reduce avoidable disputes: Clear billing descriptors, visible refund terms, and reliable fulfillment records lower the chance that a normal complaint turns into a risk signal.

- Maintain backups: A second payment route can keep parts of the business alive if one provider freezes activity.

Those steps help, but they don't remove the core issue. You're still operating inside a model where an intermediary can pause payouts based on its own risk logic.

Why payout design matters more than support quality

This is the part many merchants only realize after their second or third freeze. The problem isn't that support was slow. It's that the payout architecture gave the platform the power to hold your operating capital in the first place.

For global internet businesses, a different settlement model is often more important than a different brand name. Some merchants now choose systems that let customers pay by card while the business receives revenue directly in USDC, because that removes bank payout delays and the hold-based settlement pattern common in payment facilitator setups. If you're comparing models rather than logos, this article on an alternative to Stripe is a practical starting point.

One example is Suby, which provides an API that lets businesses accept payments by card or crypto, with merchants receiving USDC. It also offers native integrations with Discord and Telegram for subscriptions, paid access, and online communities. The relevant distinction here isn't marketing language. It's the settlement model: users pay with cards, businesses receive USDC.

That won't fit every company. Some businesses still need a conventional bank-settlement stack for internal reasons. But if payout predictability matters more than maintaining a familiar processor relationship, direct-to-wallet settlement changes the risk profile in a fundamental way.

A better support experience is helpful. A payment flow that doesn't leave your operating cash exposed is better.

Frequently Asked Questions About Stripe Account Issues

Can a permanently closed account be reopened

Sometimes, but the odds depend on why it was closed. Verification problems can often be corrected when the record is clean and complete. Repeated high-risk patterns are much harder to reverse. If the closure came from a core policy or risk determination rather than missing documents, focus on fund recovery and continuity planning instead of assuming reinstatement is likely.

How long can funds stay held

A common hold window is 90-120 days for remaining funds in frozen accounts, based on the frozen-account reporting cited earlier from Shuttle Global. In extreme cases, merchants have reported longer holds tied to prolonged reviews and account closures. The practical takeaway is simple: plan as if the money won't arrive soon, then build operations around that assumption.

What's the best way to improve your chances

Send one organized package, not a stream of attachments. Match every document to the likely trigger. Keep names and addresses consistent. Follow up on a schedule, and keep the tone professional even if you're getting canned responses.

Should you switch providers after recovery

Usually, yes, or at least diversify. A business that has already triggered one serious review should assume it can happen again. The deeper question isn't which logo to replace Stripe with. It's whether you want to stay in a model where a facilitator can interrupt payouts, or move to a setup built for direct, predictable settlement.

What should you look for in an alternative

Look at settlement mechanics first. If your business can't tolerate payout uncertainty, choose a system based on how and when you receive funds. Also check whether it supports your real workflow, such as subscriptions, paylinks, API integrations, or community access if you monetize Discord or Telegram.

If payout uncertainty is hurting your business planning, take a look at Suby. Suby gives online businesses an API to accept payments by card or crypto, while merchants receive USDC. It also includes native Discord and Telegram integrations for subscriptions, paid access, and online communities. The core model is simple: users pay with cards, businesses receive USDC.