You know the feeling. Orders start coming in from outside your home market, and what looked like growth suddenly turns into operations work.

A customer in Germany wants a clean invoice. Another in Australia gets a card decline that your domestic setup rarely sees. Finance wants to know why payouts land late, support gets refund questions you cannot answer quickly, and tax becomes a weekly source of background stress. At that point, choosing the best merchant of record for e-commerce stops being a checkout decision. It becomes a cash flow decision.

The mistake I see most often is evaluating Merchant of Record providers like shopping cart plugins. Teams compare checkout design, payment methods, and headline fees, then ignore the one question that matters most in daily operations. How do you get paid, when do you get paid, and in what currency do you keep your margin? That settlement layer changes everything from forecasting to treasury to how painful expansion feels.

Table of Contents

- What an MoR takes off your plate

- MoR versus a standard payment processor

- Why this model matters beyond digital products

- 1. Legal liability

- 2. Tax and VAT handling

- 3. Payment rails and customer payment options

- 4. Settlement speed

- 5. FX exposure and fee structure

- 6. Chargeback and dispute handling

- 7. Integration model

- 8. Geographic coverage

- 9. Developer and operator experience

- A simple scorecard to use internally

- Merchant of Record Provider Comparison

- All-in-one platforms

- Digital goods specialists

- Stablecoin settlement layers

- What works best by business type

- The flow that changes the finance experience

- What is useful in practice

- Pricing and operational details

- If you run a traditional e-commerce store

- If you sell software, subscriptions, or digital products

- If settlement friction is the primary problem

- A short decision filter

- Is an MoR the same as a payment processor

- Are MoRs only for digital businesses

- When does handling compliance in-house make sense

- Can an MoR help with chargebacks and fraud

- Does the settlement currency matter that much

Why Selling Globally Is Harder Than It Looks

The first few international sales usually feel easy. Your store is live, customers can enter a card, and revenue appears. Then the hidden work shows up.

The problems do not arrive one at a time

A software founder might think the hard part is translation. A physical goods seller might assume shipping is the main challenge. In practice, global selling breaks in several places at once.

One market wants tax shown a certain way. Another has local payment expectations. Your processor approves one customer and declines another for reasons your team cannot diagnose. Then your payout lands later than expected, with fees and conversion losses that make reconciliation messy.

If you sell on marketplaces as well as your own site, the picture gets even more fragmented. Teams planning marketplace expansion often run into a second layer of complexity around logistics and account setup, which is why practical guides on selling globally on Amazon are useful long before you launch a new region.

A similar issue shows up in direct checkout operations. The sale looks complete on the customer side, but the back office still has to handle taxes, disputes, reporting, and cross-border payout friction. That is where a good explanation of cross-border payment mechanics becomes more relevant than another generic growth checklist.

Where operators usually feel the pain first

The early warning signs are usually operational, not strategic:

- Payout timing gets unreliable: Revenue exists on paper, but finance cannot rely on when funds will be usable.

- Support workload rises: Customers ask about charges, invoices, refunds, and currencies.

- Tax risk becomes unclear: Someone on the team starts asking who is responsible for filing and remittance.

- Margins get softer: FX conversion and payment frictions eat into net revenue.

- Expansion slows down: Every new market adds another set of payment and compliance questions.

If your team is spending more time explaining transactions than selling products, your payment stack is already limiting growth.

This is why Merchant of Record adoption keeps growing. The issue is not only accepting payment. The issue is turning global demand into revenue you can settle, account for, and trust.

Understanding the Merchant of Record Model

A customer in Germany places an order on your storefront, pays in euros, and expects a local-looking receipt, a clean refund flow, and no tax surprises. Your team, meanwhile, needs that same order to settle cleanly, show up correctly in reporting, and reach your bank without avoidable FX loss or payout delays. That gap between a successful checkout and usable revenue is the reason the Merchant of Record model matters.

A Merchant of Record, or MoR, is the legal entity responsible for the transaction. In practice, that means the MoR does not just authorize a payment. It takes on the seller-side obligations tied to that sale.

What an MoR takes off your plate

A real MoR sits at the transaction layer. It usually handles:

- Tax handling: Calculating, collecting, and remitting sales tax, VAT, or GST where applicable.

- Transaction liability: Acting as the seller of record for the payment event.

- Fraud and disputes: Managing chargebacks and fraud screening under its checkout structure.

- Compliance work: Covering the rules tied to selling into different jurisdictions.

- Receipts and billing records: Issuing transaction documentation under the MoR entity.

That structure changes more than legal wording. It changes who owns the messy parts of cross-border commerce, and that has direct effects on finance, support, and operations.

It also affects settlement. Many teams evaluate MoR providers by looking at tax coverage, payment methods, and checkout UX. Those matter, but the harder operational question is simpler: how, when, and in what currency do you keep your margin? If the provider creates delays, forces extra conversions, or makes reconciliation hard, the “global payments solution” still creates back-office drag.

MoR versus a standard payment processor

A standard payment processor helps you accept payment. Your business usually remains responsible for tax logic, transaction liability, and much of the compliance burden around the sale.

An MoR changes that allocation of responsibility.

| Model | What it mainly does | Who carries more transaction responsibility |

|---|---|---|

| Standard PSP | Processes payment | Your business |

| Merchant of Record | Processes payment and assumes transaction-related liability | The MoR |

The settlement layer is where the distinction becomes commercially important. Two providers can both advertise broad payment method support, but produce very different outcomes once funds leave checkout. One may settle on long bank payout cycles, convert into a base currency you do not want, and make multi-entity reconciliation painful. Another may give clearer payout timing, better currency handling, or alternative rails that reduce dependence on traditional banking delays.

If you want a concise commercial overview, this explanation of the merchant of record model for online businesses covers the core setup well.

Why this model matters beyond digital products

MoR is common in SaaS, software, and other digital businesses because tax and compliance complexity shows up early there. The model is also relevant in e-commerce more broadly, especially when a brand is selling internationally without building local entities in every market.

For physical goods, you should also understand the separate function of an Importer of Record (IOR). The MoR handles transaction responsibility. The IOR handles customs-related responsibility. Those are different jobs, and mixing them up creates avoidable risk during expansion.

An MoR is a risk allocation and settlement decision, not just a checkout tool.

That is why the best merchant of record for e-commerce is rarely the one with the longest feature list. It is the one whose liability model, payout timing, currency options, and reporting setup match the way your business operates.

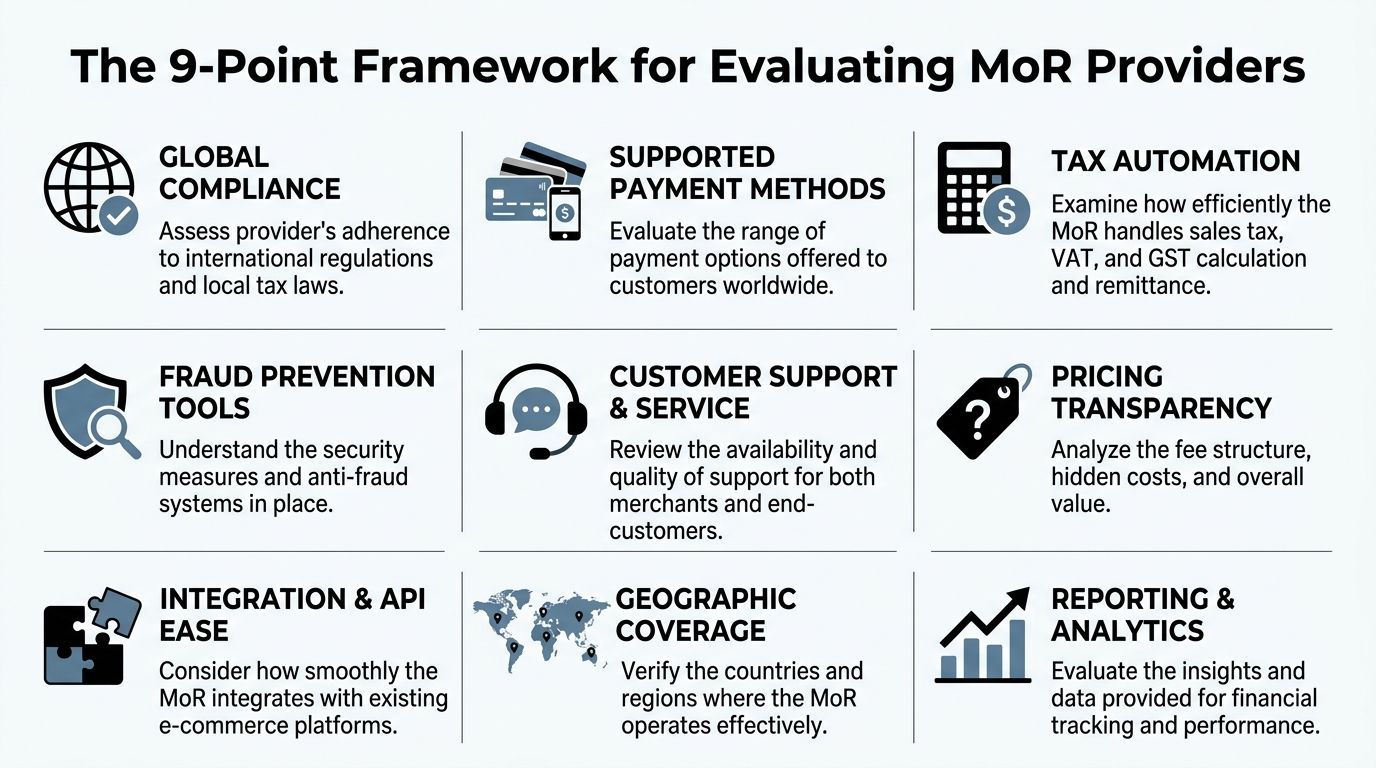

The 9-Point Framework for Evaluating MoR Providers

Most MoR comparisons are too shallow. They focus on visible features and skip the parts that decide whether finance, support, and ops will like the system six months later.

Use this framework instead.

1. Legal liability

Start here. If the provider is not clearly taking the Merchant of Record role, then you are still carrying more exposure than you think.

Read the contract language carefully. You want clarity on who is the legal seller for the transaction, who appears on receipts, and who owns the tax and dispute burden.

2. Tax and VAT handling

A serious MoR should handle tax calculation, collection, and remittance as part of the service. If the provider expects your team to bolt on separate tax logic, that is not much of an operational win.

For many companies, tax administration is the whole reason to adopt an MoR in the first place.

3. Payment rails and customer payment options

Customer-facing payment flexibility matters, but the useful question is not “How many methods are listed on the pricing page?”

Ask instead:

- Where are your customers located

- Which methods do they prefer

- Does the provider support cards well in your target regions

- Can the setup handle both one-time and recurring transactions

A broad payment menu looks good in demos. It only matters if it matches your customer mix.

4. Settlement speed

Weak evaluations often fall apart here. Teams spend hours comparing checkout UX and almost no time on payout mechanics.

Settlement speed affects payroll timing, ad spend, inventory planning, and whether finance trusts the revenue number on the dashboard. Slow settlement is not just annoying. It changes how aggressively you can operate.

5. FX exposure and fee structure

Do not stop at the headline fee. Look for hidden margin loss in currency conversion, payout conversion, dispute fees, and refund handling.

A provider can look affordable and still become expensive if your business sells internationally but settles through slow banking rails in a currency that is not natural for your treasury.

The core cost of an MoR is not the advertised fee. It is the gap between gross sales and usable net revenue.

6. Chargeback and dispute handling

Ask what happens after a disputed transaction, not before it. You want to know who manages evidence, who communicates with the networks, and how losses are allocated.

Some platforms are clean at checkout and painful during disputes. That trade-off usually appears only after volume grows.

7. Integration model

Product and engineering teams care most at this stage. Some businesses want hosted checkout for speed. Others need embedded checkout, API control, webhooks, or subscription tooling that fits an existing stack.

Look at:

- Checkout flexibility: Hosted, embedded, or API-driven

- Subscription support: Renewals, retries, billing changes

- Data flow: Webhooks, reporting, export quality

- Operational fit: How much custom engineering you need to launch and maintain it

8. Geographic coverage

Coverage is not just a map on a landing page. It is a combination of tax support, payment acceptance, local checkout relevance, and reliable settlement.

A provider may “support” a market but still create friction there. That is why a true fit matters more than broad claims.

9. Developer and operator experience

The best MoR setup works for more than one team. Engineering needs documentation and predictable APIs. Finance needs reporting. Support needs transaction clarity. Growth needs a checkout they can optimize without opening a major implementation project.

This is often the tie-breaker when two providers look similar on paper.

A simple scorecard to use internally

| Criterion | What to ask |

|---|---|

| Liability | Who is legally responsible for the transaction |

| Tax | Who calculates, collects, and remits tax |

| Settlement | How and when do funds arrive |

| Fees | What costs appear beyond the headline rate |

| Integration | How much work does launch and maintenance require |

If you use this framework, the best merchant of record for e-commerce becomes easier to evaluate. You stop buying a feature set and start choosing an operating model.

Comparing Top Merchant of Record Providers in 2026

A founder launches in the US, picks up customers in Germany, Singapore, and Brazil, then finds the primary problem is not checkout. It is settlement. Revenue arrives late, lands in the wrong currency, and creates extra FX and treasury work every month.

That is the lens that makes this category easier to evaluate. The useful comparison is not just feature set versus feature set. It is operating model versus operating model, especially at the settlement layer.

Merchant of Record Provider Comparison

| Criterion | All-in-One Platform (e.g., Shopify) | Digital Goods Specialist (e.g., FastSpring) | Stablecoin Settlement Layer (e.g., Suby) |

|---|---|---|---|

| Best fit | Broad e-commerce operations, especially SMBs | SaaS, software, digital goods | Global-native businesses focused on payout predictability |

| Core strength | Commerce stack in one system | Tax and compliance depth for digital sales | Settlement in USDC rather than traditional bank payout flow |

| Operational trade-off | Can be broad rather than specialized | May be less suited to physical goods | Requires comfort with USDC treasury and wallet-based settlement |

| Checkout control | Usually strong within platform ecosystem | Strong for digital purchase flows | Depends on API, paylink, or embedded implementation model |

| Tax burden reduction | Good if using MoR capabilities | Strong for digital cross-border complexity | Useful when paired with a model that automates transaction handling |

| Main evaluation lens | Platform convenience | Compliance and digital billing fit | How, when, and in what currency you receive funds |

All-in-one platforms

All-in-one platforms suit merchants that want fewer systems to manage. Storefront, checkout, apps, and core operations sit in one environment, which usually lowers launch friction and makes day-to-day execution simpler.

Shopify is the clearest example. On G2, it ranks prominently in the Merchant of Record category (G2). That kind of adoption matters for practical reasons. Agencies know the stack, operators are easier to hire for it, and app support is usually broad.

This category tends to work well for:

- SMBs selling physical goods

- Merchants that want one main commerce platform

- Teams that prioritize operational convenience

The trade-off shows up when the business model gets more specialized. Subscription edge cases, digital fulfillment logic, and finance workflows built around faster or more flexible settlement can push a broad platform outside its comfort zone.

Digital goods specialists

Digital goods specialists are usually a better fit for software, SaaS, and other businesses that sell across borders without shipping inventory. The value is less about storefront breadth and more about billing logic, tax handling, and support for digital transaction flows.

FastSpring fits that profile well and is widely regarded as a strong option for software and digital sellers. That matters if the goal is to offload more of the cross-border transaction burden instead of stitching together separate tools for billing, tax, and compliance.

This category usually fits:

- SaaS companies

- Software sellers

- Digital product businesses

- Teams expanding internationally without setting up local entities first

The limitation is scope. Teams selling physical goods, running marketplace structures, or needing custom payout behavior can find these platforms too narrow.

Stablecoin settlement layers

This category changes the decision because it starts with the payout side, not just the checkout side. That is a meaningful shift for operators who care about cash timing, treasury visibility, and reducing dependence on bank rails.

A stablecoin-based model lets customers pay through familiar methods while the business settles in USDC. For some companies, that is cleaner than waiting on cross-border bank payouts and then absorbing delays, fees, and FX conversion after the sale. Businesses exploring this route usually start by understanding the mechanics of accepting crypto payments for business before deciding whether USDC should sit inside their normal finance workflow.

This model is often a strong fit for:

- Remote-first businesses

- Companies paying vendors or contractors internationally

- Agencies and internet-native operators

- Businesses that want more control over settlement timing and currency exposure

The trade-off is straightforward. Finance teams need to be comfortable receiving and managing USDC. If the business still wants every payout converted back into local fiat through traditional banking, a large part of the advantage disappears.

What works best by business type

The practical choice usually looks like this.

- Sell physical goods through a central storefront: An all-in-one platform is often the cleanest operational fit.

- Sell software or subscriptions across borders: A digital goods specialist will usually map better to the billing and tax workload.

- Care most about payout timing, currency control, and modern settlement rails: A stablecoin settlement model deserves serious consideration.

The best merchant of record for e-commerce is rarely the provider with the longest feature list. It is the one that removes the constraint that hits operations and cash flow first. In a lot of international businesses, that constraint sits at the settlement layer.

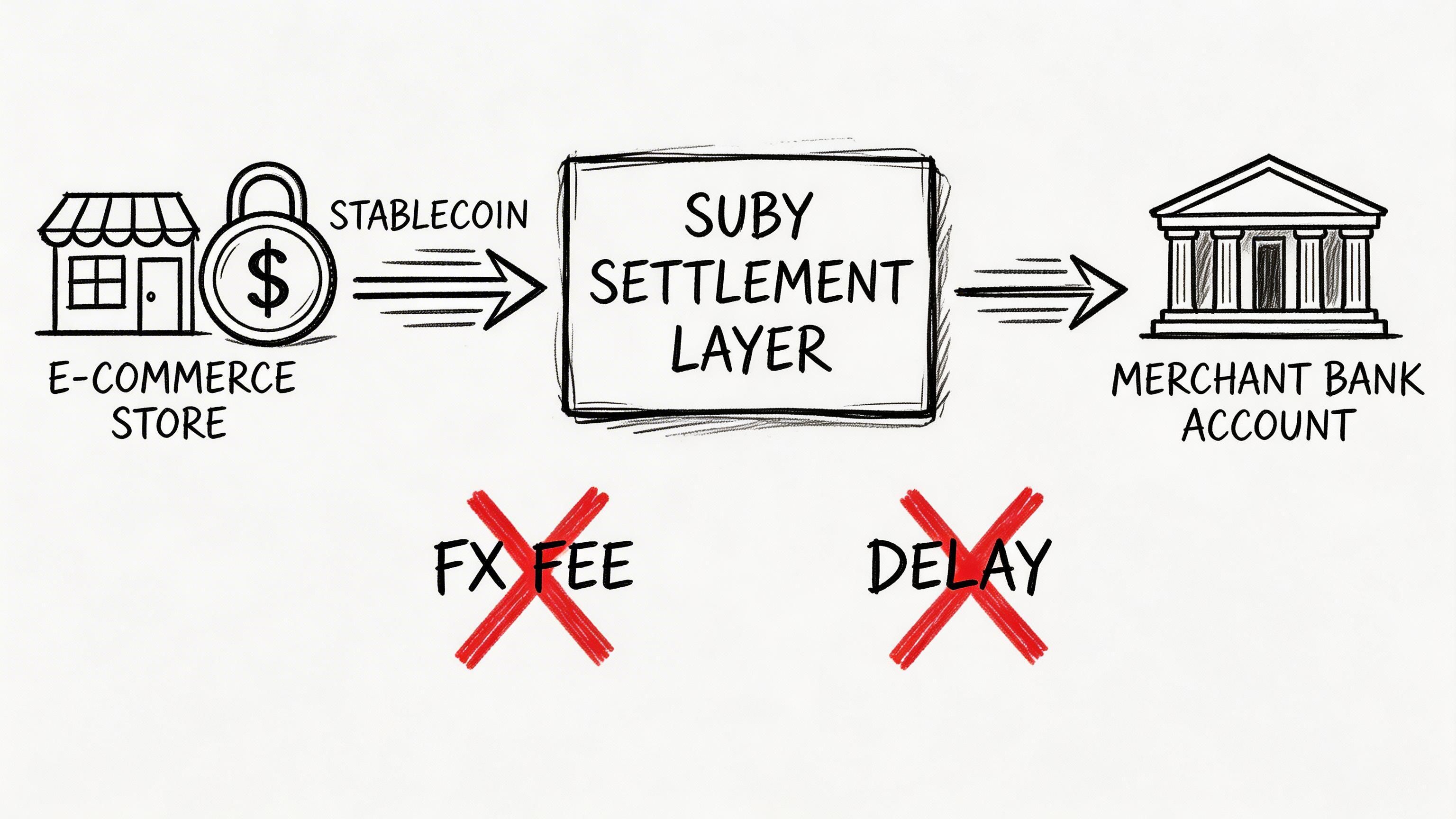

A Closer Look at Stablecoin Settlement with Suby

Most MoR content treats settlement like a footnote. For operators, it should be near the top of the decision tree.

The flow that changes the finance experience

Suby is a payment API for online businesses and creators that lets customers pay by card or crypto, while the business receives USDC. In plain terms, users pay with familiar methods like Visa or Mastercard, and merchants settle in USDC rather than waiting for traditional bank payout flows.

That matters because settlement format changes how a business handles treasury. If your customers are global but your banking setup is local, you usually absorb friction somewhere. It shows up in conversion, timing, or FX. A USDC-based settlement flow removes part of that pressure.

The product supports shareable paylinks, embedded checkout, API integrations, and webhooks. It also supports one-time payments and recurring subscriptions. That gives teams a few different ways to launch without forcing the same implementation pattern on every business.

What is useful in practice

The value is clearest when you look at common use cases:

- Online businesses with global customers: Card acceptance stays familiar for the buyer, while the merchant receives USDC.

- Developers building custom flows: API and webhook support make it possible to integrate payments into an existing product.

- Creators and communities: Native integrations with Discord and Telegram support paid access, subscriptions, and membership operations.

- Teams tired of payout uncertainty: Revenue settles in USDC with a more predictable structure than bank-dependent payout models.

A concise overview of this broader model sits in Suby’s guide on how to accept crypto payments for business, though the practical point here is straightforward. Users pay with cards, businesses receive USDC.

Pricing and operational details

Suby’s pricing starts at 5% and is described as all-inclusive on its official pricing materials. The product documentation also states support for customer payments via Visa, Mastercard, and crypto assets including USDC, USDT, ETH, SOL, and BNB, while merchants receive revenue directly in USDC.

Security and payment operations are handled with a PCI-DSS Level 1-certified processing partner, and the documented product features include strong customer authentication, dispute handling, zero-fee refunds, and a real-time dashboard for payments, subscriptions, churn, and payouts.

This model will not fit every finance team. Some companies still want fiat in a bank account because that matches internal controls, vendor workflows, or accounting policy. But if your business already operates globally and thinks in digital treasury terms, stablecoin settlement can be a cleaner operating setup than legacy payout rails.

Its appeal is not novelty. It is reducing the gap between a successful checkout and usable funds.

How to Choose the Right MoR for Your Business

The right choice depends less on rankings and more on where friction currently lives in your business.

If you run a traditional e-commerce store

Choose the system that simplifies store operations first. If your business depends on catalog management, fulfillment workflows, and a broad app ecosystem, the convenience of an all-in-one platform usually outweighs the value of a more specialized setup.

This is especially true for physical goods merchants. Your complexity often sits outside the payment event, in shipping, returns, and inventory coordination.

If you sell software, subscriptions, or digital products

Pick for compliance depth and billing fit.

A digital goods specialist is usually the stronger match when your team wants the Merchant of Record to absorb tax handling, recurring billing complexity, and cross-border transaction risk in a more focused way. That matters more than storefront flexibility if your product is downloaded, provisioned, or renewed rather than shipped.

If settlement friction is the primary problem

Some businesses do not struggle with checkout conversion as much as with what happens after checkout. Payout delays, FX exposure, and cross-border banking friction are the blockers.

In that case, a stablecoin-settlement model is worth serious attention. If customers can keep paying by card while your business receives USDC, the operational benefits can be more meaningful than another round of checkout tweaks.

A short decision filter

Ask these four questions internally:

Where does revenue get stuck today

At checkout, in tax operations, or in payout and treasury?What are you selling

Physical goods, software, subscriptions, digital access, or a mix?Who needs to live with the system every day

Engineering, finance, support, growth, or all of them?What will break first when you expand

Tax handling, local payment support, or settlement logistics?

The best merchant of record for e-commerce is not the provider with the most features. It is the one that removes the most expensive bottleneck in your current operating model.

If you answer those questions, the shortlist usually becomes obvious.

Common Questions About Merchant of Record Services

Is an MoR the same as a payment processor

No. A payment processor moves money between the customer, acquiring bank, and merchant account. A Merchant of Record owns the commercial transaction. That usually includes tax collection, invoicing, compliance duties, and the customer-facing charge on the statement.

That difference matters when something goes wrong. If a payment fails, gets disputed, or creates a tax obligation in a new market, the question is not only who processed the card. The question is who is legally and operationally responsible for the sale.

Are MoRs only for digital businesses

They are most common in software, SaaS, online memberships, and other digital products because those categories create cross-border tax and subscription complexity fast.

They can also make sense in e-commerce. The fit depends on what creates the bigger burden in your operation. For physical goods, logistics and fulfillment often stay outside the MoR scope. For digital add-ons, subscriptions, warranties, or access-based products, the MoR model can remove a meaningful amount of finance and compliance work.

When does handling compliance in-house make sense

It makes sense when your business already has finance, tax, and legal operators who can manage registrations, filing, invoicing rules, dispute workflows, and audit trails without slowing growth.

In practice, many teams underestimate the ongoing overhead. The work is not only about setting things up once. It is about keeping every market current as rules change and transaction volume grows. For SaaS companies expanding into the EU or Asia, manually managing compliance can cost an average of $50K per year according to the 2026 provider comparison from Gapp Group (Gapp Group).

Can an MoR help with chargebacks and fraud

Yes, often in a very practical way.

The important question is how far that responsibility goes. Some providers absorb more of the chargeback workflow and fraud screening. Others provide tools, while your team still carries a meaningful share of the operational burden. Read the contract language closely, especially around dispute liability, reserve policies, and payout holds after fraud spikes.

Does the settlement currency matter that much

Yes. For many operators, it matters more than another payment method on the checkout page.

Settlement affects when cash arrives, what FX costs get shaved off before funds hit your account, how treasury forecasts revenue, and whether your team has to manage delays across banking rails. A provider can look strong on checkout features and still create back-office friction if payouts are slow, opaque, or forced into the wrong currency.

This is why I treat the settlement layer as a core selection criterion. If customers pay by card but your business needs faster access to USD-denominated funds, stablecoin settlement can solve a real operating problem, not just a technical one.

If your business wants a payment setup where users pay with cards and your team receives USDC, Suby is built for that flow. It provides an API for card and crypto payments, supports subscriptions, paylinks, webhooks, and native Discord and Telegram integrations for paid access and online communities.