Gaspard LEZIN

Best Payment Platform for International SaaS Expansion

Choosing the best payment platform for international SaaS expansion? This guide compares models and helps you find a solution for global growth.

Your product may already sell globally. Your payment stack often doesn’t.

A familiar pattern plays out in fast-growing SaaS teams. The first customers outside your home market look like a win, then support tickets start piling up. A card that works locally gets declined abroad. Finance sees payout timing shift from one batch to another. Revenue looks healthy in the billing system, but the amount that lands in the business account keeps moving because conversion happens somewhere inside the payment chain.

The significance of that gap often exceeds initial expectations. International expansion is not just about accepting more cards or adding more currencies to checkout. It’s about choosing a payment model that protects conversion, keeps recurring revenue predictable, and doesn't create a second operations job for finance and product.

The best payment platform for international saas expansion is not automatically the one with the biggest logo list or the longest feature page. It’s the one that fits your settlement model, your subscription motion, your engineering bandwidth, and your tolerance for FX ambiguity.

Table of Contents

Your SaaS Is Global, But Your Payments Are Not

A quick comparison before the framework

What the six pillars actually mean in practice

How the traditional model works

How stablecoin settlement changes the design

Multi-currency support is not the same as FX control

Why payout timing becomes an operating problem

What the product actually does

Where it fits operationally

B2B SaaS with recurring revenue

Paid communities and memberships

Agencies and cross-border client billing

A Framework for Choosing Your Payment Platform

Your SaaS Is Global, But Your Payments Are Not

A SaaS company can launch in a new market in a day. The payment layer usually takes much longer to catch up.

Product ships fast. Marketing localizes the site. Sales starts booking demos in new regions. Then payments become the bottleneck no one planned for. The issue isn't always obvious at first because checkout still works for some buyers, some of the time. That creates a false sense that the setup is good enough.

It rarely is.

Friction emerges in the messy details. International cards are treated differently by issuers. Settlement timing changes by country, processor, and payout rail. Subscription renewals create a second layer of complexity because every recurring charge repeats the same currency and routing decisions month after month.

If your team has to explain every payout variance manually, the problem isn't just finance. It's product infrastructure.

I've seen teams evaluate payment providers too narrowly. They compare headline processing fees, skim over payout mechanics, and assume multi-currency support solves cross-border commerce. That approach misses the actual cost centers, especially for subscription businesses where small payment inefficiencies keep repeating.

A better way to think about this is simple. Your payment platform should reduce operational work as you expand, not create more of it. It should help you accept demand from global customers while keeping settlement, FX exposure, and recurring billing understandable enough that finance, product, and engineering can all trust the numbers.

The Six Pillars of a Global Payment Strategy

A quick comparison before the framework

Before looking at vendors, it helps to compare the operating models they tend to represent.

Model | Best fit | Main strength | Main weakness | What to check first |

|---|---|---|---|---|

Traditional global acquirer | Larger SaaS teams with complex payment optimization needs | Broad local payment reach and mature acquiring infrastructure | Pricing, settlement logic, and FX can become hard to unpack | Authorization strategy, payout timing, contract structure |

Merchant of record style platform | Teams that want tax and compliance help bundled in | Lower operational burden across markets | Less control over some parts of the payment stack | Tax handling, subscriptions, reporting depth |

Stablecoin settlement platform | Internet-native businesses that want predictable settlement in USDC | Clearer payout model and less dependence on banking rails | Requires comfort with wallet-based treasury operations | Customer payment methods, recurring billing support, wallet flow |

Global coverage matters, but not by itself. Platforms such as Verifone, PhotonPay, Airwallex, and PayPal support operations in over 200 countries, and localized payment options can boost checkouts by 20-30% in emerging markets, while 70% of SaaS revenue now comes from international customers, according to the PhotonPay overview of SaaS payment gateways on its payment gateway analysis.

What the six pillars actually mean in practice

The first pillar is settlement speed and predictability. Finance doesn't just need money to arrive. It needs to know when it arrives, in what form, and with what deductions. If payouts feel inconsistent, forecasting gets weaker and reconciliation turns into detective work.

The second is FX exposure and pricing. A lot of teams stop at “we support multiple currencies.” That’s a surface feature. What matters is where conversion happens, who controls the rate, how visible the spread is, and whether recurring renewals keep introducing surprise costs.

The third is payment method coverage. Card acceptance is the baseline, not the end state. Local payment methods often matter market by market, especially when buyer expectations differ from your domestic norm.

The fourth is subscription support. One-time checkouts are easier. SaaS revenue lives and dies on renewal quality, payment retries, customer updates, and the ability to keep recurring charges from turning into involuntary churn.

The fifth is compliance and security. This includes card handling, authentication, disputes, and the legal realities around international billing. For teams selling into Europe, VAT becomes its own workflow quickly, and practical resources like Booksmate helps with EU VAT are useful when finance is trying to understand identification requirements before scaling further.

The sixth pillar is developer integration and operations. A payment system isn't only judged at checkout. It’s judged in implementation time, webhook clarity, reporting quality, and how many internal tools your team needs to glue together afterward.

Practical rule: If a platform scores well on conversion but badly on settlement clarity, you haven't solved payments. You've moved the problem downstream.

Comparing Traditional vs Stablecoin Settlement Models

How the traditional model works

Traditional international payment infrastructure is still built around banks, acquirers, card networks, processors, and payout rails that were not designed for internet-native businesses moving fast across borders.

That model can work very well, especially at scale. Enterprise providers like Adyen stand out here. According to the ConnectPay review, direct licenses in major markets can improve authorization rates by 3-7% over intermediaries, but this model is usually best suited to companies doing over $1M in monthly volume and willing to negotiate complex interchange-plus pricing in ConnectPay’s international gateway comparison.

That trade-off is important. You can get stronger payment performance in many markets, but you often accept a more complex commercial and operational setup in return. For large teams, that may be worth it. For smaller or mid-market SaaS companies, it can be too much machinery for the stage they’re in.

How stablecoin settlement changes the design

A stablecoin settlement model changes a more fundamental layer of the system. Customers still need a familiar way to pay, especially by card, but the merchant side no longer depends on the same chain of bank-based settlement and cross-border payout steps.

That shift matters because it changes what the business receives. Instead of collecting revenue through a stack of local banking outcomes, the business receives settlement in USDC. The operating question becomes less about managing fragmented fiat flows and more about whether your team wants a deterministic settlement asset and wallet-based payout setup.

For internet-native companies, that can be a cleaner design. It removes some of the ambiguity around where value moves after checkout and reduces dependence on bank timing. It can also simplify treasury if your business already thinks in digital rails rather than country-by-country bank accounts.

Some teams exploring this architecture start by understanding the mechanics first, then evaluating providers. A practical primer is this overview of a global payment API for cross-border businesses. It helps frame the difference between payment acceptance and settlement, which many buyers still treat as the same thing.

If you're tracking infrastructure trends around digital payment rails more broadly, the Future of Ton blockchain is one example of how payment-adjacent ecosystems are evolving, even though the core decision here is not about trend chasing. It's about choosing a settlement model your finance and product teams can effectively operate.

Traditional acquirers optimize payment acceptance inside the banking system. Stablecoin settlement platforms redesign what happens after acceptance.

The Hidden Costs of FX and Payout Delays

Multi-currency support is not the same as FX control

Many international payment evaluations frequently go wrong. Teams hear “multi-currency” and assume the major problem is solved.

It isn't.

The harder question is what happens to recurring revenue after the initial checkout. The Wise analysis points out that platform comparisons rarely address the compounding effect of FX spreads on recurring billing, and that traditional platforms often bundle FX margins into opaque pricing. It uses the example of a SaaS company with 10,000 subscribers across 30 countries facing unpredictable settlement costs every month, calling this a form of “silent FX hemorrhaging” in Wise’s SaaS payment solutions article.

That phrase fits because the loss often doesn't show up as one dramatic line item. It appears as drift. Margins look slightly worse than expected. Forecasting gets noisier. Finance spends time explaining variances that originate outside the product and outside the billing engine.

A useful way to think about the issue is this:

Checkout currency is customer-facing. It helps conversion and trust.

Settlement currency is operator-facing. It determines what your business receives.

Renewals multiply bad assumptions. Any hidden spread or unclear conversion rule repeats across the life of the customer.

If your current setup leaves you guessing where conversion happened and what margin was applied, you're not managing FX. You're absorbing it.

Why payout timing becomes an operating problem

Payout delays create a different kind of drag. They don't always look expensive in a pricing table, but they can be expensive in practice.

A growing SaaS business uses cash every day. It pays contractors, ad platforms, cloud bills, affiliates, and refunds. When payment revenue arrives on a schedule the team can't reliably predict, operations get tighter than they should be. The result is not only slower finance work. Product teams also feel it when support needs answers about renewals, failed charges, or payout status.

This short explainer is worth watching if you're revisiting your current setup with FX in mind:

For teams that want to reduce this problem at the root, a practical starting point is learning how to avoid currency conversion fees. The important shift is not only finding a cheaper conversion path. It’s structuring payments so conversion and settlement are no longer a recurring source of uncertainty.

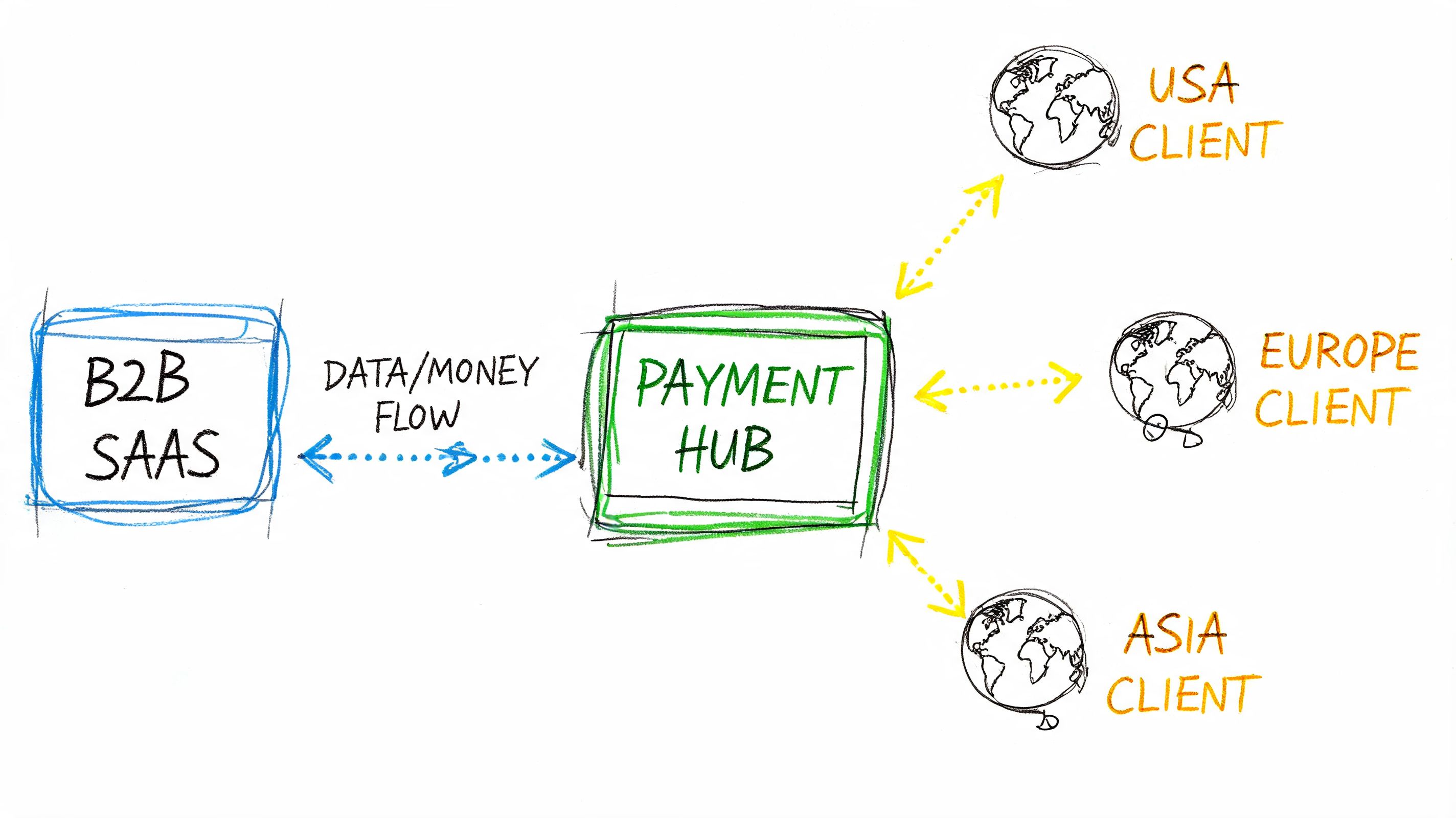

How Suby Solves for International Expansion

What the product actually does

Suby is a payment API for businesses that want to accept payments by card or crypto while receiving settlement in USDC. Customers can pay with Visa or Mastercard, and businesses receive their revenue directly in USDC to their wallet. It also supports one-time payments and recurring subscriptions, plus native integrations for Discord and Telegram where access and subscription lifecycle management need to happen in the same system.

That setup directly addresses the operational problem many international SaaS teams run into. Buyers get a familiar checkout experience. The business doesn't have to manage a patchwork of bank payouts and currency conversions after the fact.

The product documentation and site describe several core capabilities that matter here:

Card and crypto acceptance for global checkout, with merchants receiving USDC regardless of how the customer pays.

API and webhooks for direct integration into SaaS products and custom flows.

Paylinks and embedded checkout for teams that want to launch without building the full payment UI themselves.

Recurring subscriptions for businesses that need ongoing billing, not just one-off payments.

Discord and Telegram integrations for paid access, memberships, and online communities.

A real-time dashboard for visibility into payments, subscriptions, churn, and payouts.

All-inclusive pricing starting at 5 percent, as listed on Suby pricing.

Where it fits operationally

This model is most attractive when your business values predictable settlement more than maximum complexity in local acquiring optimization.

If you're a SaaS team with a global customer base, the practical benefit is straightforward. Customers can pay by card. Revenue arrives in USDC. You don't need to build treasury around a growing set of fiat balances, local bank relationships, or delayed payout windows. That also changes how engineering scopes the work, because the payment integration and the settlement outcome stay closer together.

Security and compliance are part of the product story as well. Suby states that it works with a PCI-DSS Level 1 certified processing partner and supports strong customer authentication, two-factor authentication, dispute handling, and zero-fee refunds through its official materials and documentation.

For teams that already think globally and operate online-first, a simpler settlement model often matters more than another layer of banking abstraction.

This won't be the right choice for every company. If your main objective is squeezing maximum authorization performance from negotiated enterprise acquiring across many large markets, a traditional enterprise provider may still fit better. But if your priority is reducing FX ambiguity, avoiding payout delays, and giving product and finance a cleaner operating model, this architecture is much easier to justify.

Practical Use Cases for a Modern Payment Layer

B2B SaaS with recurring revenue

A B2B SaaS company selling to customers in North America, Europe, and Asia usually wants the same three things from payments. Checkout should feel familiar, subscription billing should work without custom recovery logic everywhere, and finance should know what revenue landed.

A modern payment layer helps when the team wants to decouple customer payment preference from merchant settlement complexity. Buyers can still pay in a way they recognize, while the operator gets a more consistent payout outcome. That means less time spent reconciling payment behavior across markets and more time improving pricing, packaging, and retention.

Paid communities and memberships

Creators and community operators have a different problem. Their biggest pain is often not international card acceptance by itself. It’s the manual work around access control, subscription state, and member churn.

When payments and community access live in separate tools, the workflow gets brittle fast. Someone pays, then support has to confirm it. Someone cancels, then access removal happens late. Someone renews, then the role update doesn't fire. Native integrations with Discord and Telegram make this category much easier to operate because payment status and access control stay tied together.

A good payment system for memberships doesn't stop at charging the card. It also decides who should have access right now.

Agencies and cross-border client billing

Agencies and freelancers often sit in between SaaS and services businesses. They invoice internationally, but they still feel many of the same payment pains. Clients want to pay by card. The business owner wants fast receipt of funds and doesn't want every invoice to become a currency question.

For this use case, the same criteria that identify the best payment platform for international saas expansion can also be a good fit outside pure SaaS. The key requirement is not the business model label. It’s whether the company values clean cross-border collection and a simpler settlement path. Agencies dealing with clients across several regions usually benefit from the same traits SaaS teams do, namely predictable payout flow, fewer banking dependencies, and less manual follow-up.

A Framework for Choosing Your Payment Platform

The right choice usually becomes obvious once you stop comparing gateways as if they all solve the same problem.

Start with these questions:

Do you need the deepest possible local acquiring stack, or do you need simpler global operations?

If payment optimization at enterprise scale is the priority, traditional acquirers may justify their complexity.How much FX uncertainty can your margins tolerate?

If renewals and international settlements keep creating unexplained variance, the settlement model deserves more attention than the checkout layer.What does finance need in order to trust the numbers?

Reliable payout timing and a clear settlement asset matter more than many feature lists suggest.How much custom payment infrastructure does engineering want to own?

Some teams want complete flexibility. Others want API, webhooks, subscriptions, and reporting to work without stitching together extra systems.Are your use cases broader than checkout alone?

If you also need paylinks, subscriptions, and community access flows, your platform should support those directly.

For buyers comparing options, this guide to the best international payment gateway is a useful companion read because it sharpens the difference between broad acceptance and operationally clean settlement.

The biggest mistake is picking a platform that looks strong in demos but pushes complexity into finance after launch. The better decision is the one your team can still operate cleanly after thousands of renewals, cross-border payouts, and support events.

Suby is a payment gateway and Merchant of Record. Your customers pay with card, bank transfer, Apple Pay, Google Pay, Klarna, and more, or stablecoins, and you get paid out to your bank account, or directly in stablecoins (USDC, EURC) to your wallet, anywhere in the world, no bank account required. It supports subscriptions, paylinks, and embedded checkout, with native Discord and Telegram integrations for paid access, and as a merchant of record it handles tax and compliance across markets. For international SaaS expansion, that combination gives you predictable settlement instead of FX drift and delayed bank payouts.