You've probably felt this already. Your product is working, signups are coming in, and then payments become the thing that slows everything down. A customer in one country can pay by card but not by local method. Another wants to pay with a wallet. A third is happy to pay in fiat, but your finance team wants settlement in stablecoins. Suddenly the checkout isn't a form. It's infrastructure.

That's why a SaaS payment gateway matters more than most product managers expect. It isn't just the screen where a user enters payment details. It's the system that decides which payment methods you can support, how safely you can store and route payment data, how subscriptions renew, how failed payments are retried, and how money finally lands where your business needs it.

Older guides usually split this into separate conversations. One stack for cards. Another for bank transfers. Another for crypto. That mental model breaks down when you're building a global web application. Modern SaaS teams need a unified architecture where customers can pay the way they prefer, and the business can settle revenue the way it chooses.

Table of Contents

- Why separate stacks create product debt

- What unified settlement changes

- One product with four practical uses

The Bottleneck to Global SaaS Growth

A lot of SaaS teams hit the same wall. The app scales faster than the payment system behind it. What worked for one market starts to break when customers arrive from different regions, expect different payment methods, or need invoicing and subscription logic that your first integration never planned for.

A SaaS payment gateway is the layer that sits between your product and the payment networks that authorize and settle transactions. In practice, that means it handles checkout collection, secure data transfer, routing, authorization responses, and the events your application needs after a payment succeeds, fails, renews, or gets disputed.

The confusion starts when people treat a gateway like a simple plugin. For a subscription product, it's closer to a revenue operating system. It affects onboarding, renewals, entitlement logic, finance workflows, support tickets, and expansion into new markets.

Where growth usually stalls

The warning signs are easy to spot:

- Regional friction: Customers can sign up, but they can't use the method they trust most.

- Subscription fragility: Renewals fail, and your app doesn't react cleanly.

- Settlement mismatch: Your customers pay one way, but your business needs funds delivered another way.

- Operational sprawl: Finance exports one report, support checks another dashboard, and engineering listens to several different event streams.

Practical rule: If product, engineering, and finance each have a different view of what happened in a payment, your gateway architecture is already costing you time.

Why this matters for product decisions

For a product manager, the gateway shapes more than billing. It changes how you design checkout, account activation, plan upgrades, refunds, access control, and international rollout. If the underlying payment model is fragmented, every new launch takes longer because each payment type becomes its own project.

That's why the right question isn't “Can we accept payments?” It's “Can we accept the methods customers want, automate what happens after payment, and settle revenue in a form the business can use?”

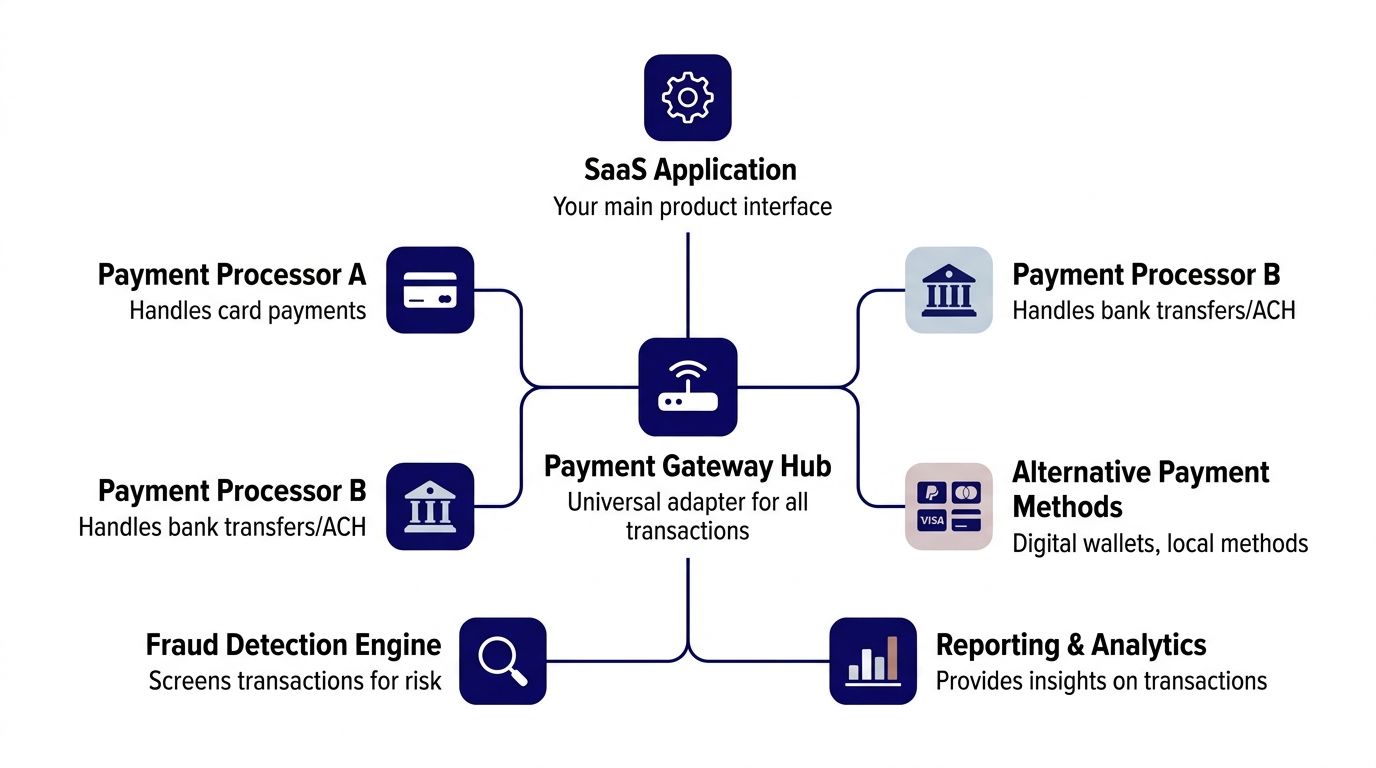

Core Architecture of a Modern SaaS Payment Gateway

A modern gateway works like a universal travel adapter for internet commerce. Your application shouldn't care whether the customer pays by card, wallet, bank method, or crypto asset. It should ask one system to collect payment, return a result, and trigger the right business logic.

That matters because the market for this infrastructure is expanding fast. The global payment gateway market is projected to grow from USD 31 billion in 2023 to USD 161 billion by 2032, with a 20.5% annual growth rate, and large enterprises hold 55% of the market, which shows how central dependable payment infrastructure has become for high-volume SaaS and e-commerce operations (payment gateway market projections and enterprise share).

Payins

The first layer is payins. This is every method your customer can use at checkout.

For a SaaS company, payins shouldn't force separate user experiences for separate rails. One checkout should be able to present the available options and collect the right information for the chosen method. Your app should receive a normalized result, not a different implementation burden for every payment type.

A good payins layer usually answers these product questions:

| Question | What the gateway should handle |

|---|---|

| How does the customer pay? | Card, wallet, bank method, or crypto |

| What does checkout show? | One consistent interface, not multiple disconnected flows |

| What does the app receive? | A unified payment status and event stream |

Unified balance

The second layer is the one older systems often miss. After money comes in, where does it land?

In a siloed stack, card payments settle one way, bank transfers show up elsewhere, and crypto sits in another system. Finance has to stitch the story together after the fact. A unified architecture consolidates incoming funds into one balance view first, then handles conversion or payout from there.

That design simplifies three painful jobs:

- Operations: One place to monitor successful payments, failed renewals, and pending settlements.

- Reporting: A cleaner path to match product events with financial records.

- Product logic: One state model for “paid,” even when payment methods differ underneath.

A gateway should reduce payment complexity before your internal teams ever see it.

Payouts

The third layer is payouts, meaning how the business receives funds, an area where modern systems pull away from older gateways. The incoming method doesn't have to dictate the outgoing settlement method.

A customer might pay by card. The business might want settlement to a bank account. Or the customer pays by card and the business receives USDC. Or the customer pays with a wallet and the business still wants fiat settlement. Those are product and treasury choices, not checkout constraints.

You can see this same architectural shift in platforms focused on payment orchestration for global businesses, where the goal is to route many payment methods through one operating layer instead of adding separate systems one by one.

What older stacks get wrong

Older gateway setups usually grow by patchwork. A team starts with card acceptance, adds local methods later, then bolts on crypto as a side project. The result is predictable:

- checkout logic forks

- reconciliation gets slower

- support needs more manual investigation

- engineering maintains overlapping payment states

A modern SaaS payment gateway should feel boring from the application's point of view. One integration surface. One event model. One operational picture.

Essential Capabilities for Subscription and Web Apps

Subscription products have different needs from one-time checkout flows. You're not just capturing a payment. You're maintaining a billing relationship over time. That means your gateway needs to support recurring logic, event-driven automation, and a broad enough method set for customers in multiple regions.

A useful test is simple. If your team has to build major billing behavior outside the gateway because the gateway only handles raw transactions, you're not choosing a payments layer. You're choosing a low-level rail and rebuilding the missing pieces yourself.

Recurring and Metered Billing

Recurring billing is the core requirement for most SaaS products. Monthly subscriptions, annual plans, free-trial conversions, add-ons, and seat-based expansions all depend on the system's ability to charge again later without making the customer repeat checkout.

Metered billing adds a second layer of difficulty. Your app has to calculate usage, pass billable amounts, and make sure the invoice and charge happen in the right order. If the payment stack can't support that cleanly, billing leaks into product logic and becomes hard to test.

What to look for:

- Recurring charge support: Your gateway should handle subscription renewals as a native concept, not as a manual cron job your team maintains.

- Plan lifecycle events: Upgrades, downgrades, and cancellations need predictable event handling so access control stays accurate.

- Failure workflows: When a renewal fails, the system should surface that event immediately so your app can trigger dunning, notify the customer, or apply a grace period.

API Integration and Webhooks

For developers, APIs and webhooks are where a gateway becomes usable. For product managers, they're how payment events turn into user experience.

A modern gateway API should enable businesses to accept both fiat and cryptocurrency payments in one checkout, and automate subscription renewals with real-time webhook notifications for payment events, as shown in the Suby Merchant API introduction.

That matters because your app shouldn't poll a dashboard to learn what happened. It should react to events as they occur.

Common patterns include:

- Payment succeeded and the app provisions an account or upgrades a workspace.

- Renewal failed and the app starts a recovery flow.

- Subscription canceled and the app schedules entitlement changes.

- Invoice paid and your finance workflow closes the outstanding balance.

If you can't describe your payment lifecycle as events your app listens for, you'll end up managing revenue by support ticket.

There's also an organizational benefit here. Product can define the customer journey, engineering can subscribe to events, and finance can reconcile against the same transaction timeline. That's much easier than spreading logic across manual exports and custom scripts.

If you're reviewing monetization structure alongside payment architecture, it helps to refine your SaaS business strategy before you finalize the implementation. Pricing and billing logic tend to harden quickly once they're wired into production systems.

Support for Global Payment Methods

Many SaaS teams underestimate the problem. They assume “international payments” means showing a currency selector. In practice, global support means meeting customers with the payment behavior they already trust.

That usually includes a mix of:

- Cards and wallets: The baseline for most online software sales.

- Bank-based methods: Important when customers prefer account-to-account flows.

- Crypto alongside fiat: Increasingly relevant when your audience is global, internet-native, or treasury-sensitive.

The important point is architectural. These methods shouldn't create separate businesses inside your app. Your checkout can present different options, but your internal model should still work as one commerce system.

A strong SaaS payment gateway also lowers developer workload here. Instead of adding one method, then another, then another, your team integrates one payment layer that abstracts the variation. That gives product teams more freedom to expand internationally without renegotiating the entire billing stack every quarter.

Navigating Security, Compliance, and Reconciliation

Payment infrastructure gets abstract until the first audit request, failed dispute review, or month-end reconciliation problem. Then everyone suddenly cares about how data moved, who touched it, and whether the records line up.

This is why the gateway should act like a shield. Your app needs payment capability, but it shouldn't need direct exposure to raw card data or fragmented settlement records just to do its job.

What the gateway should shield you from

To be compliant, a SaaS payment gateway must use PCI-DSS Level 1 certified partners and enforce TLS/SSL encryption and tokenization to protect payment data during transit between the customer, merchant, and acquiring bank, as outlined in this payment gateway security and compliance overview.

In plain terms, that means:

- Sensitive payment data is encrypted early: The details are protected before they travel through the payment stack.

- Tokenization replaces raw card data exposure: Your internal systems work with tokens instead of storing PAN details directly.

- Authorization happens through compliant intermediaries: The gateway routes the request to card networks and issuers, then returns the result.

For a product manager, the practical implication is important. You can still design a smooth checkout and recurring billing flow without asking your own application to become a compliance-heavy payment vault.

Why reconciliation gets messy fast

Reconciliation is where bad architecture becomes expensive. If cards settle in one system, bank transfers in another, and crypto in a third, finance has to manually match application events with payout records. Support often gets pulled in because the customer says they paid, the app says they didn't, and someone has to trace the gap.

A unified balance and dashboard model reduces that confusion. Instead of asking three systems what happened, your team starts from one ledger view and traces outward only when needed.

Here's the operational difference:

| Fragmented setup | Unified setup |

|---|---|

| Multiple exports | One primary balance view |

| Different settlement timelines | One normalized reporting layer |

| Manual matching across tools | Cleaner mapping between app events and funds movement |

Security and reconciliation are connected. The same architecture that keeps sensitive data out of your app also gives finance a cleaner record of what happened.

Teams that need to simplify this workflow often focus on payment reconciliation for modern commerce operations, because the cost is rarely the transaction alone. It's the hours spent explaining the transaction later.

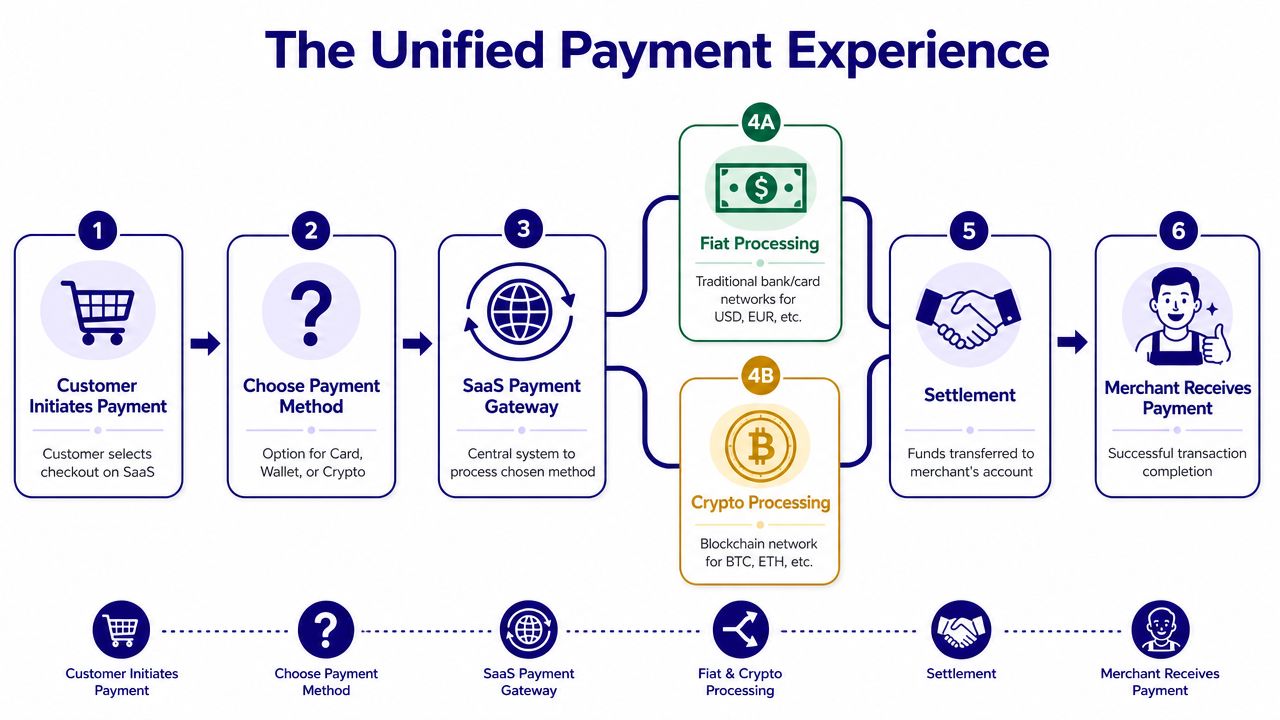

The Rise of Unified Fiat and Crypto Payments

Most payment guides still describe fiat and crypto as separate lanes. That's already outdated for many SaaS businesses. Customers increasingly expect choice at checkout, while businesses want more control over settlement after the payment clears.

Why separate stacks create product debt

The market gap is clear. 34% of SaaS companies want to accept crypto alongside cards, but only 12% of major providers offer a native, unified crypto checkout without third-party integrations, which forces businesses to maintain separate systems and adds technical overhead (unified crypto and card checkout gap in SaaS).

That split creates avoidable problems:

- product has to design around two payment experiences

- engineering maintains separate integrations

- finance reconciles different settlement rails

- support learns multiple failure paths

A unified architecture fixes the model at the source. The customer chooses how to pay. The business chooses how to receive funds. Those decisions don't need to be locked together.

What unified settlement changes

The design is particularly compelling for global SaaS. A modern gateway using stablecoin rails can convert multiple payin methods into a unified balance and support cross-border settlement without relying entirely on local banking corridors. In the material describing this model, platforms using stablecoin settlement rails are associated with near-instant revenue confirmation and predictable fees per payin method, while traditional gateways can add 2% to 4% in FX markup and delay payouts by 3 to 5 business days (stablecoin settlement and cross-border payout context).

A practical example is the card-to-USDC flow. The customer pays by card because that's what feels normal to them. The business receives USDC because that's better for treasury, vendor payments, or international settlement. That's not a niche edge case anymore. It's a clean answer to the mismatch between customer preference and merchant settlement needs.

Later in the buying journey, this same principle also matters for invoicing and one-off payments. The client may want to pay by bank, card, or wallet. The business may still want funds delivered in stablecoins or to a bank account in another currency.

The video below shows the broader payment model in action.

One product with four practical uses

One example of this model is Suby's crypto payments for business flow. Suby provides an API that lets businesses accept payments by card or crypto, and it also offers native Discord and Telegram integrations for subscriptions, paid access, and online communities. The core model is simple: customers pay any way they want, businesses get paid the way they choose.

The product can be used in four ways:

- Suby Payments: An API-first payment stack to accept cards and crypto through one checkout, with subscriptions, paylinks, and webhooks.

- Suby Crypto: A crypto payment gateway that handles token swaps, sponsors gas fees, and settles either to a non-custodial wallet or to the Suby balance.

- Suby Gating: Paid access for Discord, Telegram, digital downloads, and online courses.

- Suby Invoicing: The client chooses how to pay, while the business receives funds the way it prefers.

Here's the product view referenced above.

Pricing depends on the payment method used, so it's important to check the provider's pricing page for current per-method figures rather than assume a flat rate.

Evaluating and Implementing Your SaaS Payment Gateway

By the time you evaluate providers, most of the important questions aren't about checkout design. They're about operating model. Can this gateway support the billing logic your app needs now, and the settlement flexibility your business will need later?

A practical evaluation checklist looks like this:

- Checkout flexibility: Can customers pay by the methods your audience already uses, without forcing separate user journeys?

- Subscription support: Does the gateway natively support recurring billing, renewals, and event-driven lifecycle management?

- Developer surface area: Are API objects, webhooks, and dashboard workflows clean enough for product and engineering to share one payment model?

- Settlement options: Can the business receive money in the form and currency it prefers?

- Operational visibility: Will finance and support be able to reconcile what happened without stitching together several tools?

There's also a hard business case for getting this right. Average SaaS transaction failure rates can reach 14.7%, and modern gateways with dynamic FX rails and multi-currency settlement can reduce these failures by up to 30% (SaaS payment failure rates and reduction potential). If your product sells across borders, gateway architecture directly affects recovered revenue.

Implementation usually follows one of two paths:

- Full API integration when payments are closely tied to onboarding, account provisioning, and in-app billing workflows.

- Paylinks or invoicing flows when you need speed, lower engineering effort, or a way to support manual sales and client billing without building every surface first.

Start with the payment events your application must react to, then choose the checkout and settlement model that produces those events cleanly.

Migration is where teams often hesitate. The safest approach is usually incremental. Launch new flows first, map webhooks into your billing state machine, verify reconciliation, then move existing cohorts in stages when operational visibility is solid.

A SaaS payment gateway isn't just a utility. It's part of the product, part of the finance stack, and part of your expansion strategy.

If you're building for international customers and need one system where customers can pay by card, wallet, bank, or crypto while your business settles to a bank account or in stablecoins like USDC, Suby is worth evaluating. Review the API, checkout flows, Discord and Telegram integrations, and the pricing page for the payment methods you plan to support.