You're probably closer to payment orchestration than you think.

A common path looks like this. A company starts with one payment provider, one checkout, one market. Then it adds a second provider for a new region, a wallet for mobile users, a local bank method for a specific country, maybe BNPL for higher-value purchases, and later some kind of crypto checkout because customers keep asking for it. Nothing breaks all at once, but the stack gets harder to manage every quarter.

Soon, product sees lower approval rates in one market, finance has to reconcile reports from multiple dashboards, and engineering keeps patching edge cases that only exist because each provider behaves differently. That's the moment when payments stop feeling like a feature and start acting like infrastructure.

Payment orchestration is the layer that brings order to that sprawl. It sits between your product and your payment providers, then decides how transactions should flow, where they should route, how failures should retry, and how data should come back into one operational view. The part most guides miss is this: modern orchestration shouldn't only unify cards, wallets, and bank methods. It should also unify fiat and crypto into one balance and settlement flow.

Table of Contents

- Routing decides in real time

- Token vaulting reduces coupling

- Reconciliation turns payment data into operations

- What business leaders usually care about

- What technical teams usually care about

- A short way to test whether you need it

- Is payment orchestration only for large enterprises

- How is this different from using multiple gateways

- Can a business accept crypto and settle in fiat without managing crypto directly

- What's the biggest mistake teams make

Why Your Payment Stack Is Holding You Back

A growing business in three regions often ends up with a payment stack nobody designed on purpose.

The original setup may have been reasonable. One gateway for cards, another provider for a local bank method, a separate tool for subscriptions, and a manual process for finance to map settlements back to orders. Then expansion adds more exceptions. One market needs a different acquirer. Another performs better with a local wallet. A third needs invoices rather than checkout. Every addition solves a local problem, but the whole system becomes slower to change.

That's one reason the category has grown so quickly. The global payment orchestration platform market reached approximately $2.65 billion in 2025 and is projected to grow to $30.1 billion by 2035, while digital transactions globally increased 19% in 2023 alone, according to Spreedly's guide to payments orchestration.

The pain usually shows up in four places

- Checkout performance gets uneven: A payment method works well in one market and poorly in another, but the team has limited visibility into why.

- Engineering loses time to payment plumbing: Each provider has different APIs, failure modes, and reporting formats.

- Finance works from fragments: Settlements, refunds, and disputes live in separate systems.

- Expansion gets expensive: Every new geography means another integration, another contract, and another operational process.

Most teams don't realize they have a payment architecture problem. They describe it as a conversion problem, an ops problem, or a reconciliation problem.

Payment orchestration matters because it reframes those issues as one solvable system problem. Instead of asking, “Which gateway should we add next?” you ask, “What control layer should sit above all of them?”

That shift changes how a business expands. You stop building payments as a collection of exceptions and start managing them as a platform capability. If you're already seeing the warning signs, this breakdown of common pitfalls with global payment processors is a useful companion read because many of those pitfalls appear before companies realize they need orchestration.

A simpler way to think about it

Think of payment orchestration like an air traffic control layer for money movement. Planes still exist. Airports still exist. But something has to coordinate routing, congestion, fallback paths, and safe arrivals.

Without that layer, each connection works on its own terms. With it, the business gets one place to define logic, monitor outcomes, and change direction without rewriting the whole stack.

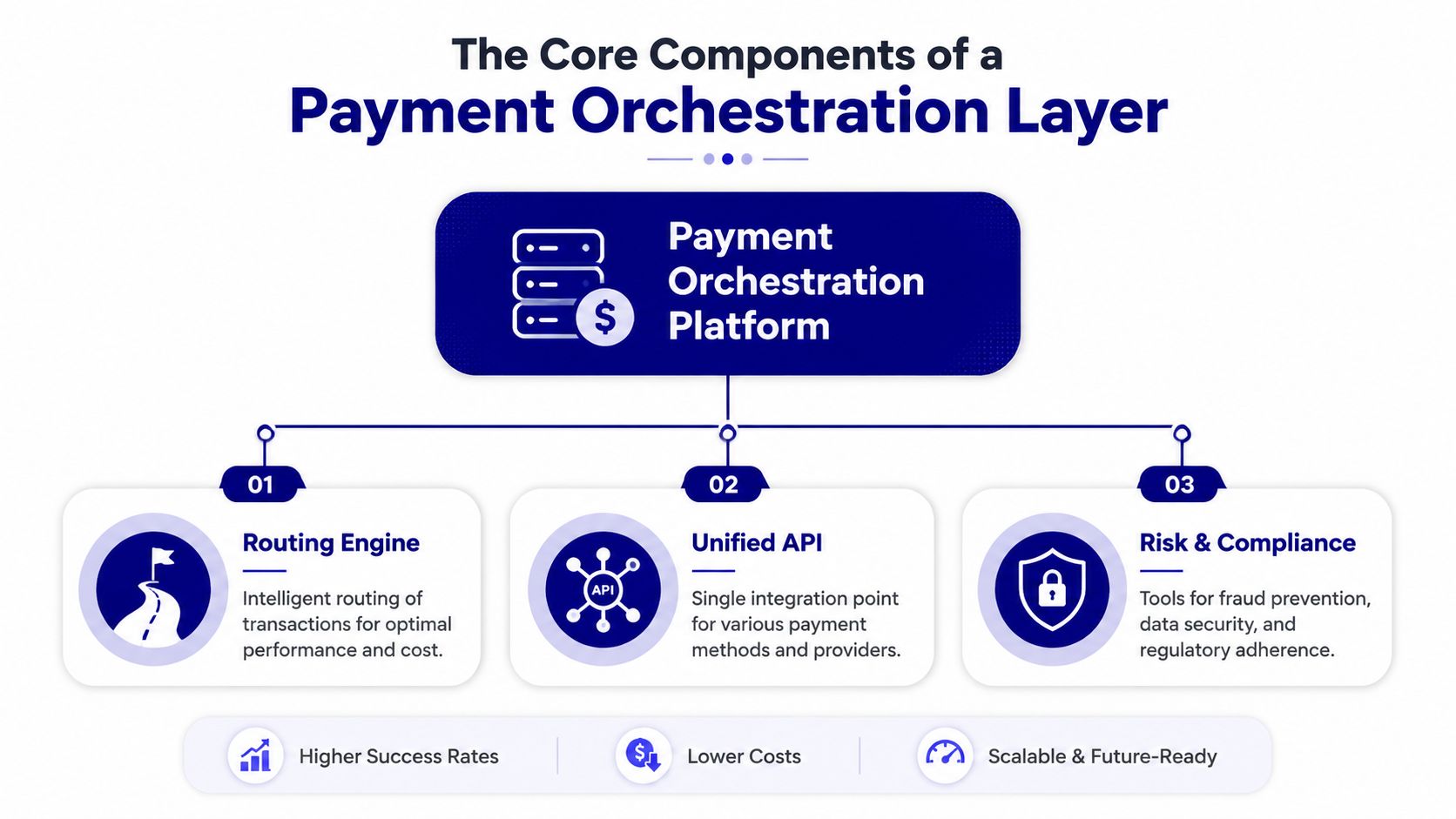

The Core Components of a Payment Orchestration Layer

Payment orchestration sounds technical because it is technical. But the important parts are easy to understand once you strip away vendor jargon.

At the center is one idea. A payment orchestration layer gives you a single control plane for many payment methods and providers. That control plane usually rests on three pillars: routing, token handling, and unified operations.

Routing decides in real time

Routing is the brain.

When a customer submits a payment, the orchestration engine evaluates the transaction and chooses where to send it. In mature systems, that routing layer operates with latency between 20–50 ms and can produce an immediate 2–4% lift in authorization rates by scoring multiple providers and automatically retrying failures, as described in Redis's explanation of payment orchestration architecture.

That sounds abstract, so here's a plain example. A card payment from France may do better through one provider, while the same card brand from another region may perform better through a different one. If the first route fails for a recoverable reason, the system can retry through a backup path without asking the customer to start over.

Practical rule: Smart routing is useful only if the business can change rules without rebuilding checkout.

If you want a concrete way to picture that integration layer, Supercenter's integration capabilities are a helpful example of how modern platforms expose many downstream systems through a cleaner connection point.

Token vaulting reduces coupling

Token vaulting is less visible, but it matters just as much.

In simple terms, a token vault stores payment credentials in a reusable, secure form so your business doesn't have to tie customer payment data to one provider's internal format. That gives you flexibility. If you need to add a processor, shift recurring billing logic, or change routing later, you aren't forced to rebuild around locked data.

Often, readers get confused. They assume orchestration is mostly about adding more payment methods. It isn't. A big part of the value is reducing dependency on any single provider's data model and checkout logic.

Reconciliation turns payment data into operations

The third pillar is unified reconciliation.

This is the difference between “payments happened” and “the business can operate.” Every charge, retry, refund, payout, and dispute needs to show up in a way finance, ops, support, and product can understand. If routing is the brain, reconciliation is the memory.

A useful orchestration layer should make these jobs easier:

| Function | Without orchestration | With orchestration |

|---|---|---|

| Transaction view | Separate provider dashboards | One operational view |

| Failure analysis | Different error formats | Normalized patterns |

| Provider comparison | Manual spreadsheet work | Side-by-side monitoring |

| Finance workflows | Reconcile each source separately | Consolidated reporting flow |

The technical details differ by platform. The underlying business need does not. You want one place where teams can understand what happened to money, why it happened, and what to change next.

Unlocking Growth with Payment Orchestration

The biggest mistake people make is treating payment orchestration as back-end cleanup.

It can reduce complexity, yes. But its more important job is helping the business grow without paying a penalty every time it adds a market, method, or provider. That's why the conversation usually lands with both the CFO and the engineering lead.

What business leaders usually care about

Leaders usually don't ask for orchestration by name. They ask for better conversion, faster market entry, and fewer payment-related fire drills.

That's where the economics of fragmentation become useful. Merchants using 5+ gateways for local methods face 22% higher integration overhead and 15% more failed transactions, while API-first orchestration with 100% method coverage can cut onboarding time by 63%, according to TNSI's discussion of orchestration layers.

Those numbers matter because they describe two hidden costs at once. First, every extra gateway adds operational drag. Second, more connections do not automatically mean a better checkout if those systems fail differently and report differently.

Here's the business case in plain language:

- Higher payment success: Better routing and fallback logic can save otherwise lost orders.

- Lower operational friction: Teams spend less time reconciling mismatched records.

- Faster expansion: New markets don't always require a brand-new payment build.

- More pricing flexibility: Businesses can offer more ways to pay without redesigning their whole stack.

For teams working internationally, this broader guide for global SaaS growth is useful because it shows how payment method choice and multi-currency operations affect expansion beyond the checkout itself.

Here's a short walkthrough before the next point:

What technical teams usually care about

Engineering teams usually care about a different set of tradeoffs. They want fewer brittle integrations, less provider-specific logic in application code, and a way to change payment behavior without shipping a risky release every time.

A solid orchestration layer helps by creating separation between product logic and payment-provider complexity. Checkout calls one API. The orchestration layer handles downstream variation.

Good payment architecture doesn't remove complexity. It moves complexity into the right layer.

This is also where analytics become strategic. If product, finance, and engineering all see the same normalized payment data, the team can spot patterns instead of arguing over conflicting dashboards. A payment system becomes much easier to improve when everyone is looking at the same event stream, which is why a focused view on payment analytics matters so much once you operate across methods and regions.

A short way to test whether you need it

You probably need payment orchestration if several of these are true:

- You're adding local methods market by market: Each launch creates a fresh integration project.

- You already use multiple providers: But you still don't have a single decision layer above them.

- Your finance team reconciles across many systems: Settlement visibility comes late or manually.

- Your product team wants more payment options: But engineering pushes back because each addition increases maintenance.

If none of that sounds familiar, a simpler payment setup may still be enough. Orchestration becomes valuable when your payment surface area grows faster than your team's ability to manage it cleanly.

A Practical Look at Orchestrated Payment Flows

Most explanations of payment orchestration stop at routing. That's useful, but incomplete.

The harder real-world question is this: What happens after different kinds of money come in? Cards, wallets, bank methods, BNPL, and crypto can all create revenue, but if they settle into separate systems, the business still ends up managing multiple balances, multiple conversions, and multiple operational handoffs.

From customer payment to one balance

A practical orchestrated flow should feel simple from the outside.

The customer picks a payment method. That could be a card, wallet, bank transfer, BNPL option, or crypto payment. The platform processes that choice through the right rail, handles the provider-specific work in the background, then returns one result to the merchant system.

What matters next is settlement design. In a fragmented setup, card payments may settle to a bank account, crypto may land in a separate wallet flow, and finance still has to manually merge those worlds. In a better design, every payment lands in one unified balance first, then the business decides how to receive funds from there.

That's the gap many guides ignore. ACI Worldwide's discussion of orchestration highlights that most guides miss the fiat-and-crypto unified balance problem. It also notes that 68% of global SaaS firms accept crypto, yet often lack a single balance for USD/EUR/USDC, and that unified fiat-crypto orchestration has reduced settlement latency by 41% for cross-border e-commerce.

Why the unified balance matters

A real product example provides clarity. Suby provides an API that lets businesses accept payments by card or crypto, and it also offers native integrations with Discord and Telegram for use cases like subscriptions, paid access, and online communities. It's one product with four ways to use it: Suby Payments for API-first card and crypto acceptance through one checkout, Suby Crypto for crypto payments with swap handling, gas sponsorship, and settlement to a non-custodial wallet or the Suby balance, Suby Gating for paid access to Discord, Telegram, downloads, and courses, and Suby Invoicing so a client can pay how they want while the business receives what it wants.

The key mental model is straightforward:

- Customers pay how they prefer: card, wallet, bank, BNPL, or crypto

- Funds land in one balance: instead of splitting payment operations by rail

- The business chooses settlement: to a bank account or in stablecoins such as USDC, in the currency it wants

A useful example is the card-to-USDC flow. A customer pays by card. The business receives settlement in USDC. That isn't the only flow, but it shows why unified orchestration matters. The merchant doesn't need separate customer-facing checkouts and separate treasury logic just because the incoming and outgoing forms of money differ.

If you want to see how teams usually approach the implementation side of this, this walkthrough on payment gateway API integration gives a practical framing for the developer workflow behind these kinds of payment flows.

The real win isn't adding crypto as another button. It's making fiat and crypto behave like parts of the same operating system.

How to Choose and Implement an Orchestration Solution

Choosing an orchestration platform is really about choosing constraints.

Every vendor promises simplicity. What you're buying is a set of tradeoffs around control, coverage, reporting, security, and settlement flexibility. If you don't define those clearly up front, you can replace one form of payment sprawl with another.

What to evaluate before you sign

Start with the basics, but don't stop there.

- API quality: Documentation should make common flows easy to understand. Look for clear webhook behavior, predictable error handling, and a clean sandbox experience.

- Method coverage: You want broad support for cards, wallets, bank methods, BNPL, and, if relevant to your business, crypto.

- Settlement options: Many evaluations stay too shallow. Ask how funds land, where they land, and whether incoming and outgoing currencies can differ.

- Pricing transparency: Pricing depends on the payment method used, so don't rely on a single flat-rate assumption. Check exact figures on the provider's pricing page.

- Security and compliance: Review confirmed controls, support processes, and dispute handling.

- Operational visibility: Reporting should work for finance and product, not just payment specialists.

A modern platform should also help you avoid a new form of lock-in. A single API is useful only if it gives you flexibility rather than hiding hard dependencies under a cleaner dashboard.

What a modern product can look like

It helps to evaluate products by use case, not just by category label.

One example is a single product that supports several operating models. That may include an API-first stack for developers, a crypto gateway for businesses that want to accept crypto without handling swaps or gas directly, a gating product for paid communities and digital access, and invoicing for agencies or freelancers who want the client to choose the payment method while the business chooses settlement.

If you're evaluating a provider shaped like that, check whether the flows all share the same underlying balance and payout logic. That's the difference between one product with multiple surfaces and several separate tools packaged together.

Don't ask only, “Can this accept more payment methods?” Ask, “Can this simplify how money lands and how we get paid?”

A practical rollout sequence

Implementation usually goes better when teams stage it.

| Step | What to do | Why it matters |

|---|---|---|

| 1 | Map current payment flows | You need a baseline before changing routing |

| 2 | Separate checkout logic from provider logic | This reduces migration risk |

| 3 | Launch with one or two priority methods | Early wins are easier to measure |

| 4 | Add reporting and reconciliation workflows | Ops pain often shows up after go-live |

| 5 | Expand settlement choices | This is where treasury flexibility starts paying off |

A careful rollout also means checking support and service expectations in advance. If a provider's customer support process or SLA model is unclear, that becomes a real operational issue once payment volume grows.

Common Questions about Payment Orchestration

Is payment orchestration only for large enterprises

No. Large enterprises adopted it early because they felt payment complexity first. But the need shows up much earlier now, especially for SaaS companies, digital sellers, agencies, marketplaces, and online communities operating across borders.

The better test isn't company size. It's payment complexity. If you support several payment methods, serve more than one market, or want customers to pay one way while the business settles another way, orchestration becomes relevant quickly.

How is this different from using multiple gateways

A multi-gateway setup means you have several payment connections.

Payment orchestration means you also have an intelligent management layer above them. That layer decides routing, retries, reporting, and operational consistency. Without it, multiple gateways often create more complexity than resilience.

Can a business accept crypto and settle in fiat without managing crypto directly

Yes, that's one of the most useful outcomes of a unified payment design.

The important point is not just “accept crypto.” It's whether the platform abstracts the operational complexity that usually comes with it. In a unified setup, the customer can pay with crypto, while the business receives funds in the form it wants for operations, whether that's bank settlement or stablecoins such as USDC.

What's the biggest mistake teams make

They optimize checkout input but ignore settlement output.

A team spends months adding methods customers can use, then leaves finance and treasury with multiple balances, manual conversions, and disconnected reporting. The customer-facing side improves, but the business-facing side stays fragmented.

That's why the most useful definition of payment orchestration is broader than routing. It's the system that coordinates how money is accepted, how it is normalized into one operating view, and how it is paid out in the form the business wants.

If your team wants a payment setup where customers can pay by card or crypto and your business can settle to a bank account or in stablecoins like USDC, Suby is one option to evaluate. It provides an API for accepting payments by card or crypto, supports native Discord and Telegram integrations for subscriptions and paid access, and is designed around the core idea that customers pay any way they want while businesses get paid the way they choose. Pricing depends on the payment method used, so check the pricing page for exact details.