Gaspard LEZIN

What is a psp payment service provider? A Quick Guide

Learn what is a psp payment service provider and how PSPs power global online payments in 2026, simplifying cross-border checkout.

A payment service provider (PSP) is your all-in-one partner for getting paid online. Think of it as the middleman that connects your business to the entire world of digital payments, from credit cards to other online methods, all through a single integration.

You don't have to build separate relationships with banks or card networks. The PSP handles all that complexity for you.

What a PSP Really Does for Your Business

Let's get practical. Imagine a customer lands on your checkout page, ready to buy. The PSP is the engine that manages every single step from the moment they hit "Pay" until that money is securely in your account.

Without a PSP, you'd be stuck trying to piece together different services for payment processing, security, and bank settlements. It can be a technical and administrative challenge. A PSP bundles all of this into one package, which is why the market is projected to be worth $148.64 billion by 2035 as more businesses move online. You can see the data behind this explosive e-commerce growth for yourself.

A modern PSP goes far beyond just taking payments. Their job is to make your financial operations simpler, safer, and more global.

Here’s a quick look at the core functions a good PSP manages on your behalf.

Core Functions of a Payment Service Provider

Function | What It Means for Your Business |

|---|---|

Payment Processing | The PSP securely captures customer payment details and sends the transaction request through the necessary networks for approval. |

Multi-Method Support | You can instantly accept payments from all major credit cards, digital wallets, and other popular regional methods your customers prefer. |

Security & Compliance | The PSP handles all the heavy lifting for PCI DSS compliance, protecting sensitive cardholder data and dramatically reducing your risk. |

Unified Settlement | Instead of a messy stream of individual transactions, the PSP gathers all your funds and deposits them into your account in one clean payout. |

As you can see, a PSP consolidates multiple critical roles into one, saving you time and technical headaches so you can focus on your actual business.

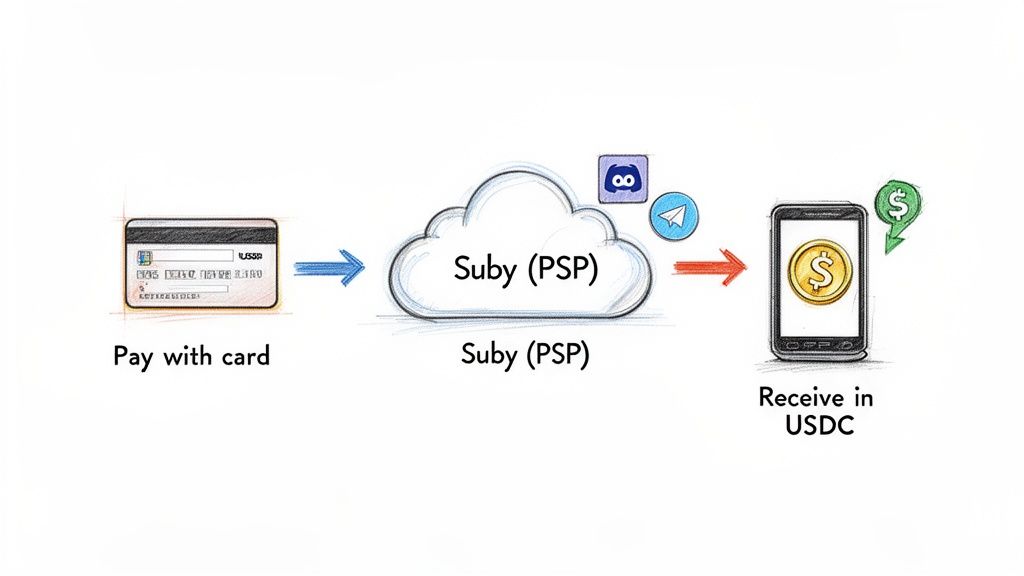

A core benefit of a modern PSP is its ability to bridge different payment worlds. For instance, we provide an API that allows any business to accept traditional card payments from customers, but receive the funds as USDC directly to their digital wallet. This model removes the friction of cross-border banking.

This can be even simpler for specific use cases. For online communities, we offer native integrations with Discord and Telegram that let creators manage subscriptions and paid access without writing a single line of code.

Ultimately, a PSP’s real job is to make getting paid feel effortless, no matter how your customers pay or where they are in the world.

How a PSP Manages Your Customer's Payment Journey

Let's walk through what actually happens when a customer hits "Buy Now" on your site. From your perspective, it’s a single click. But behind the scenes, your PSP is kicking off a rapid-fire sequence of events to get you paid.

The moment your customer enters their card details, the PSP’s integrated payment gateway springs into action. Its first job is to grab that sensitive information and encrypt it, wrapping it in a secure digital package. This is non-negotiable, as it's what protects the data as it travels from the customer's browser to the financial networks.

From Authorization to Settlement

Once encrypted, that package of information is fired off to the appropriate card network, like Visa or Mastercard. The network then acts as a messenger, pinging the customer's bank (the issuing bank) for a quick status check.

The issuing bank needs to answer a few critical questions in milliseconds:

Is this a real, active account?

Does the customer have enough money or credit for this purchase?

Does anything about this transaction look suspicious or fraudulent?

The bank sends a simple "yes" or "no" back down the line. The PSP catches this response and immediately tells your website whether the payment was approved or declined. A "Payment Successful" message appears for your customer, and the PSP formally authorizes the transaction.

Think of the PSP as a master translator and coordinator. It takes a complex, multi-step conversation between different banks and networks and turns it into a single, clean outcome for your business, all in about two seconds.

This is what a unified payment flow, managed by a PSP, looks like in practice.

As you can see, the PSP acts as your single point of contact. It handles all the back-and-forth with global payment systems so you can focus on one thing: receiving your funds.

The Final Step: Getting the Money in Your Account

But the PSP's job isn't over once the payment is approved. Next, it works with its acquiring bank partner to officially collect the money from your customer’s bank.

The PSP then gathers all your approved transactions for the day (or another set period) into one consolidated batch. Instead of getting hundreds of tiny deposits, you get one clean transfer.

This final settlement step is where innovative PSPs really shine. A customer in Japan might pay with a card, but a modern provider like Suby can settle that transaction for you directly in a stablecoin like USDC. You get paid in a consistent digital currency, sidestepping the complexities and fees of traditional currency conversion.

Ultimately, the PSP bundles dozens of separate, tedious tasks, including security, fraud checks, multi-bank communication, and fund settlement, into a single, reliable service. This not only makes your life easier but also creates a smooth and trustworthy checkout experience that keeps customers coming back.

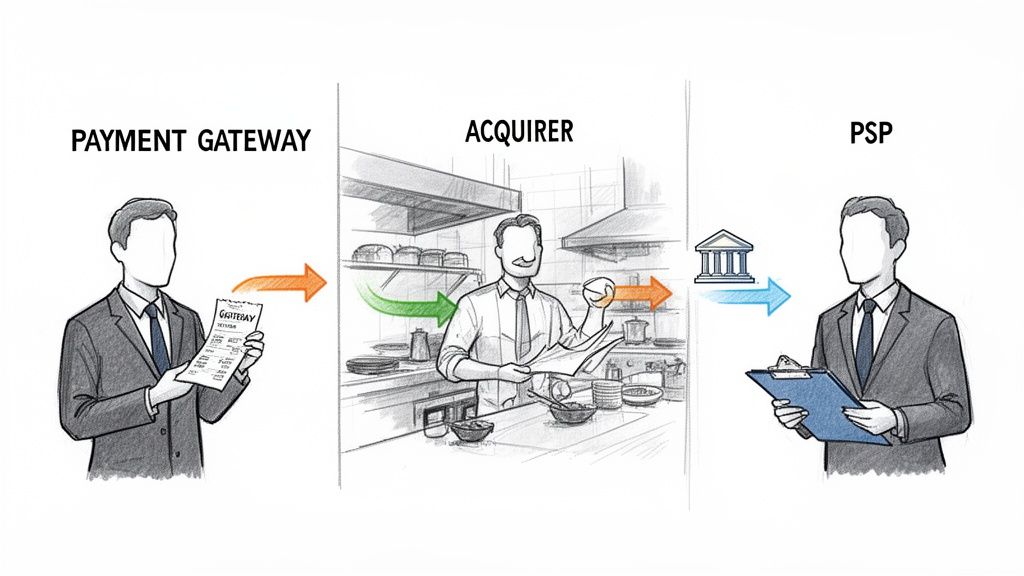

PSP vs Payment Gateway vs Acquirer Explained

When you start accepting payments online, you quickly run into a sea of confusing terms. What’s a PSP? How is that different from a payment gateway or an acquiring bank? It's easy to get lost, but a simple analogy can clear things up fast.

Think of your online business as a busy restaurant.

A payment gateway is like the waiter. They’re the front-line. They take the customer’s payment information at the checkout “table” and securely pass it back to the kitchen.

An acquiring bank is the kitchen manager. This entity receives the payment order, communicates with the customer's bank to get the funds approved, and manages the entire transaction behind the scenes.

A PSP, or payment service provider, is the general manager of the entire restaurant. They oversee everything, including the waiter, the kitchen, and the final delivery of funds to your bank account, making sure the whole process runs smoothly.

Most businesses today prefer to work with a PSP for one simple reason: it's like hiring a single, experienced general manager instead of trying to manage the waiter and kitchen staff yourself.

Why Simplicity Matters

If you decided not to use a PSP, you'd be signing up for a lot more work. You would need to find and set up separate contracts and technical connections with both a payment gateway and an acquiring bank. This DIY approach means juggling multiple relationships, separate fee schedules, and a much heavier lift for your developers. Some businesses do explore alternatives to Stripe and other payment gateways, but these often handle just one piece of the puzzle.

A PSP wraps all these functions into one neat package. You get one agreement to sign, one team to call for support, and a single API to integrate into your website or app. It’s a huge time and money saver. While the PSP handles everything, the gateway is still a crucial component; you can learn more about what exactly a payment gateway does in our detailed explainer.

To help you see the differences clearly, here’s a quick breakdown of each role.

PSP vs Gateway vs Acquirer at a Glance

This table offers a comparative look at the roles and responsibilities of each entity in the payment ecosystem.

Entity | Primary Role | Who Needs It? |

|---|---|---|

Payment Gateway | Securely captures and transmits customer payment data from the merchant's site to the payment network. | Any business that wants to accept online payments. |

Acquiring Bank | A financial institution that holds the merchant's account, receives payment approvals from the customer's bank, and deposits funds. | Any business that accepts card payments. It's the bank that "acquires" the funds for you. |

Payment Service Provider (PSP) | An all-in-one service that bundles gateway, acquiring, and other features like fraud detection and reporting into a single platform. | Businesses of all sizes looking for a simple, unified solution to manage all their payment needs. |

Ultimately, a PSP's main job is to take a set of very complicated financial processes and make them feel incredibly simple for the business owner.

The core value of a PSP is consolidation. It bundles multiple complex financial services into a single, easy-to-use package, saving businesses immense time, money, and technical resources.

Modern PSPs like Suby push this simplicity even further. We give businesses a single API to accept traditional card payments alongside crypto. For community-driven businesses, we even offer native integrations for Discord and Telegram to handle subscriptions and paid access right where your users are. It’s about making sure that no matter how your customer wants to pay, the experience is seamless for them and the settlement, which arrives in your account as USDC, is just as simple for you.

The Real-World Benefits of Using a PSP

So, what’s the real-world payoff of using a payment service provider? It all boils down to one powerful concept: simplicity. Instead of trying to piece together separate vendors for payment processing, security, and banking, a PSP brings everything under one roof.

Think about the headaches this solves. Your developers work with one clean API, not three different ones. You have one contract to sign, one set of fees to understand, and one number to call when you need help. This frees up an incredible amount of time and mental energy, letting you focus on what you do best, growing your business, instead of getting tangled in payment infrastructure.

Simplified Integration and Enhanced Security

A modern PSP essentially gives you a universal adapter for money. Their API allows you to start accepting payments from anyone, anywhere, whether they're using a credit card or crypto, all through a single, straightforward integration. It doesn't just stop at taking payments, either. A good PSP can plug right into your existing systems to power sophisticated e-commerce automation, driving real efficiency and growth.

Then there’s the security angle, which is a massive weight off your shoulders. If you handle credit card data yourself, you’re on the hook for meeting the Payment Card Industry Data Security Standard (PCI DSS). This can be a complex, expensive, and never-ending compliance battle.

When you work with a PSP, they absorb the vast majority of that burden. They process and store the sensitive cardholder data on their own highly secure, certified systems. This drastically reduces your risk, liability, and the chance of a devastating data breach. You get to offer a trustworthy, secure checkout experience without having to become a cybersecurity expert overnight.

Cost Reduction and Global Reach

Using a PSP can also be a smart move for your bottom line. Bundling services usually leads to more predictable transaction fees than you'd get by paying a gateway, acquirer, and processor separately. But the real cost savings come from the operational efficiencies and, with modern providers, some truly game-changing settlement models.

This is where things get really interesting for any business operating on a global scale.

For any merchant selling internationally, the biggest silent killers of profit are often currency conversion fees and agonizingly slow payout times. A modern PSP can wipe out both of these problems by settling your payments in a stablecoin like USDC.

Here’s how that works in practice. Imagine a customer in Germany buys from you using their Visa card. A provider like Suby processes that payment, and instead of waiting for a wire transfer, you receive the funds to your bank account, or in stablecoins (USDC, EURC) to your digital wallet almost instantly.

This completely bypasses the slow, expensive, and outdated international banking system. Suddenly, there are no surprise currency exchange markups, no three-to-five-day settlement delays, and no need to open and manage foreign bank accounts just to get paid.

This model gives you a few powerful advantages:

Faster Access to Revenue: Your cash flow gets a massive boost when funds settle in minutes or hours, not days.

Predictable Payouts: You receive the exact amount you charged, in USDC. No more losing money to unpredictable currency fluctuations between the sale and the settlement.

Reduced Operational Friction: You can manage all your global revenue from one simple digital wallet, dramatically simplifying your financial operations.

By embracing stablecoin settlements, a PSP delivers a payment solution that is genuinely built for the borderless nature of the internet, giving you faster, cheaper, and more predictable access to your own money.

How to Choose the Right PSP for a Global Business

Picking a payment service provider is a much bigger deal than most founders realize. It’s not just a technical tool; it's the financial engine of your business. The right PSP can feel like a genuine partner in your growth, while the wrong one will silently bleed your resources and stunt your global reach. To make the right call, you have to look past the shiny advertised rates and dig into what really matters.

The global payments space is absolutely massive, and it's on track to blow past USD 5.3 trillion by 2030. A huge driver of this is the shift to cloud-based solutions, which now make up 60% of all new payment setups because of their sheer flexibility. At the same time, regulations like Europe's Instant Payments Regulation are rewriting the rules for cross-border money movement. If you want to get a sense of where things are headed, you can learn more about the future of payment businesses and the trends shaping the next few years.

With all that noise, how do you find the one that fits? It comes down to asking a few pointed questions.

How Fast Will You Actually Get Paid?

For any business operating globally, cash flow is king. So, the first and most critical question for any potential PSP is: when does my money actually become my money?

Traditionally, you’d be stuck waiting for days while your revenue snakes its way through the international banking system. The PSP holds your funds, batches them, and eventually initiates a wire transfer, creating a painful gap between making a sale and having cash in the bank.

But modern PSPs are flipping this model on its head. Some now let your customers pay with their card as usual, but you receive the settlement almost instantly as USDC stablecoin. This completely bypasses the old-school banking rails. The advantages are huge:

Near-instant settlements: Your revenue lands in your digital wallet in minutes or hours, not days.

No forced currency conversions: You get to sidestep the hidden FX fees that chip away at your profits every time you move money across borders.

Simple treasury: You can hold, manage, and deploy your global revenue in a single, stable, dollar-equivalent currency.

Choosing a PSP with stablecoin settlements isn't just a niche play anymore, it's a core strategic decision. It gives you immediate, predictable access to your revenue, which is a superpower for running a lean, internet-native business.

Look Beyond the Headline Rate: What’s the True Cost?

That low transaction fee you see on a PSP’s homepage is almost never the full story. The total cost of ownership is what you need to focus on. It’s a combination of the obvious fees and the hidden ones that only show up later.

Think beyond that 2.9% + $0.30. You need to ask for a full fee schedule. What are the setup fees? Are there monthly minimums? What will you lose on currency conversion and cross-border payouts? A transparent provider will have no problem breaking this down for you.

Our guide on how to accept international payments offers a framework for calculating these often-overlooked costs so you can make a true apples-to-apples comparison.

Will It Actually Work With Your Tech?

Finally, you need to think about how this new piece of your financial stack will plug into everything else. How easy is it to get started, and can it adapt as you grow?

Look for a provider that offers both simplicity and power. Does it have a clean, well-documented API that gives your developers the control they need for custom work? On the flip side, does it have simple, no-code tools like embeddable checkout forms that keep customers on your site?

For many businesses, getting to market quickly is everything. At Suby, for example, we built a powerful API for developers who want total control, but we also offer native integrations for platforms like Discord and Telegram. This means a community-based business can start selling subscriptions and managing member access without needing a developer, proving that the right PSP can meet you where you are today and still be ready for where you're going tomorrow.

A Modern PSP in Action: Suby

All this theory is great, but what does a modern payment service provider actually look like in the real world? Let's use our own platform, Suby, as a concrete example. We built Suby to connect traditional card payments with the efficiency of stablecoin finance, creating a new model for what a PSP can do for a global business.

The experience is seamless for your customers. They see a normal checkout page and pay with their Visa or Mastercard, just like they would anywhere else. The magic happens on your end. Instead of waiting days for money to clear through a bank, you get paid almost instantly in USDC directly to your digital wallet.

Bypassing Global Payment Friction

We designed this model specifically to solve the biggest headaches that come with international sales. By settling payments in a stablecoin like USDC, businesses can completely sidestep the slow, expensive, and unpredictable legacy banking system.

This gives any business operating across borders some serious advantages:

No International Bank Accounts Needed: Forget the red tape. You can accept payments from customers anywhere without the hassle of opening and managing bank accounts in different countries.

Eliminate SWIFT Delays: Your money isn't stuck in the correspondent banking network for three to five business days. Payouts are fast and direct.

Avoid Surprise Currency Fees: Because you're paid in USDC, you don't get hit with forced currency conversions or the hidden FX markups that chip away at your revenue on every single sale.

The core idea is simple but powerful: give customers a familiar card payment experience while giving businesses a faster, cheaper, and more predictable way to get paid in USDC. This approach makes global commerce accessible to anyone with an internet connection.

Flexible Tools for Modern Businesses

A modern PSP has to be adaptable. We know that a SaaS startup has different needs than a community creator, so we've built flexible tools for both developers and non-technical users. The goal is simple: make it easy to get paid, no matter how you've built your business.

For anyone needing a custom setup, our full-featured API lets you integrate card or crypto payments directly into your own platforms. But you don't have to be a developer to get started. We also offer native integrations for popular community platforms like Discord and Telegram. These are perfect for creators looking to sell subscriptions or manage paid access for their audience, all without writing a single line of code.

Whether you run an e-commerce store, a SaaS company, or a thriving online community, a modern PSP gives you the right tools to get paid from anywhere in the world. To dive deeper into the specifics, check out our complete guide on what a PSP payment service provider is.

Common Questions About Payment Service Providers

It’s only natural to have a few questions when you're figuring out the best way to handle payments. Let's tackle some of the most common ones that come up for business owners.

Are PSPs Actually Secure?

Absolutely. In fact, using a reputable PSP is one of the most secure ways to handle payments. Security isn't just a feature; it's their entire business model.

Top-tier providers are always PCI DSS compliant, which is the global gold standard for protecting card data. They use a combination of encryption and tokenization to ensure that sensitive customer information is never exposed. For you, this means a massive reduction in your own security burden and liability. You're effectively outsourcing the riskiest part of the payment process to experts.

What's the Real Difference Between a PSP and a Merchant Account?

Think of it this way: a traditional merchant account is just one ingredient. To actually accept a payment, you'd still need to find a separate payment gateway to connect your website to the bank. It's a DIY approach that requires multiple contracts and integrations.

A PSP, on the other hand, is the complete meal. It bundles the merchant account, payment gateway, and processing services into one neat package. You get a single point of contact, one integration, and a much simpler way to manage everything. It’s a true all-in-one solution.

Why Would My Business Want to Be Paid in USDC?

For any business with international customers, getting settlements in USDC is a game-changer. It lets you completely sidestep the slow, expensive, and unpredictable world of traditional cross-border bank transfers.

For a global business, stablecoin settlements mean no more waiting days for international bank transfers to clear, no more surprise currency conversion fees eating into your profits, and no need to open foreign bank accounts. You get near-instant access to your revenue in a stable, dollar-pegged currency you can manage from anywhere.

Simply put, it’s about getting your money faster, cheaper, and with far more control. Customers pay with a card, and you receive USDC.

Suby is a payment gateway and Merchant of Record. Your customers pay with card, bank transfer, Apple Pay, Google Pay, Klarna, and more, or stablecoins, and you get paid out to your bank account, or directly in stablecoins (USDC, EURC) to your wallet, anywhere in the world, no bank account required. As a modern payment service provider, Suby bundles the gateway, acquiring, PCI DSS compliance, and settlement into one API, so you get all the reach of a global PSP without the SWIFT delays or FX markups.