Gaspard LEZIN

Your Guide to Merchant of Record for Global Sales

What is a merchant of record? Learn how it simplifies global sales, tax compliance, and payment liability to help you scale your business with confidence.

So, you've built a fantastic product and you're ready to sell it to the world. But as soon as you look beyond your own borders, you run into a wall of complexity, like international taxes, different payment laws, fraud risks, and currency conversions. It's enough to make anyone's head spin. This is where a Merchant of Record (MoR) comes in.

Think of an MoR as your business's international sales agent. They're the legal entity that takes on the messy, complicated, and risky parts of selling to customers globally, so you don't have to.

What Is a Merchant of Record?

At its core, a Merchant of Record is the company that is legally responsible for a transaction with your end customer. When a customer in Germany or Japan buys your software, they aren't technically buying it from you. Instead, the MoR steps in, legally "buys" the product from you for a split second, and then "sells" it directly to the customer.

This simple-sounding switch is incredibly powerful. It means the MoR's name appears on the customer's credit card statement, and more importantly, they assume all the legal and financial liability for that sale. You get to sell your product, and they handle the rest.

What Does an MoR Actually Do?

An MoR's job is to absorb the entire backend financial operation of selling online. This isn't just a simple payment gateway; it's a comprehensive service that shoulders significant burdens. To give you a clearer picture, here's a quick summary of what a Merchant of Record typically handles.

Merchant of Record at a Glance

Responsibility Area | What the MoR Handles |

|---|---|

Payment Processing | Manages all card payments, local payment methods, and currency conversions. |

Tax & Invoicing | Calculates, collects, and remits sales taxes (like VAT/GST) to government bodies. |

Fraud & Risk | Takes the financial hit for fraudulent transactions and manages chargeback disputes. |

Global Compliance | Stays up-to-date with local laws, payment regulations, and data security standards (PCI-DSS). |

By offloading these critical functions, you're free to focus on what you do best, which is building and marketing your products. The MoR effectively becomes a shield, protecting your business from the risks and administrative headaches of global commerce.

The MoR becomes the liable party for the entire sale, shielding your business from significant risk. You get the revenue from a global customer base without having to become a global tax and legal expert overnight.

This model is exploding in popularity for a reason. As businesses chase international growth, the complexity becomes a major bottleneck. The Merchant of Record software market is expected to rocket to $35.43 billion by 2032, a massive increase from its $13.2 billion valuation in 2025. This trend makes perfect sense when you consider that 72% of transactions are now digital, and companies are desperate for a simpler way to manage cross-border sales. You can dig deeper into these numbers in this global MoR software market report.

It's important to know that while MoRs handle the entire liability stack, they aren't the only solution for global payments. For instance, a platform like Suby offers a different approach. It provides a powerful API that allows any business to accept payments by card or crypto, where customers pay with their card and businesses receive USDC. This is a great fit for businesses that want to streamline their international cash flow but prefer to retain control and manage their own tax and compliance obligations.

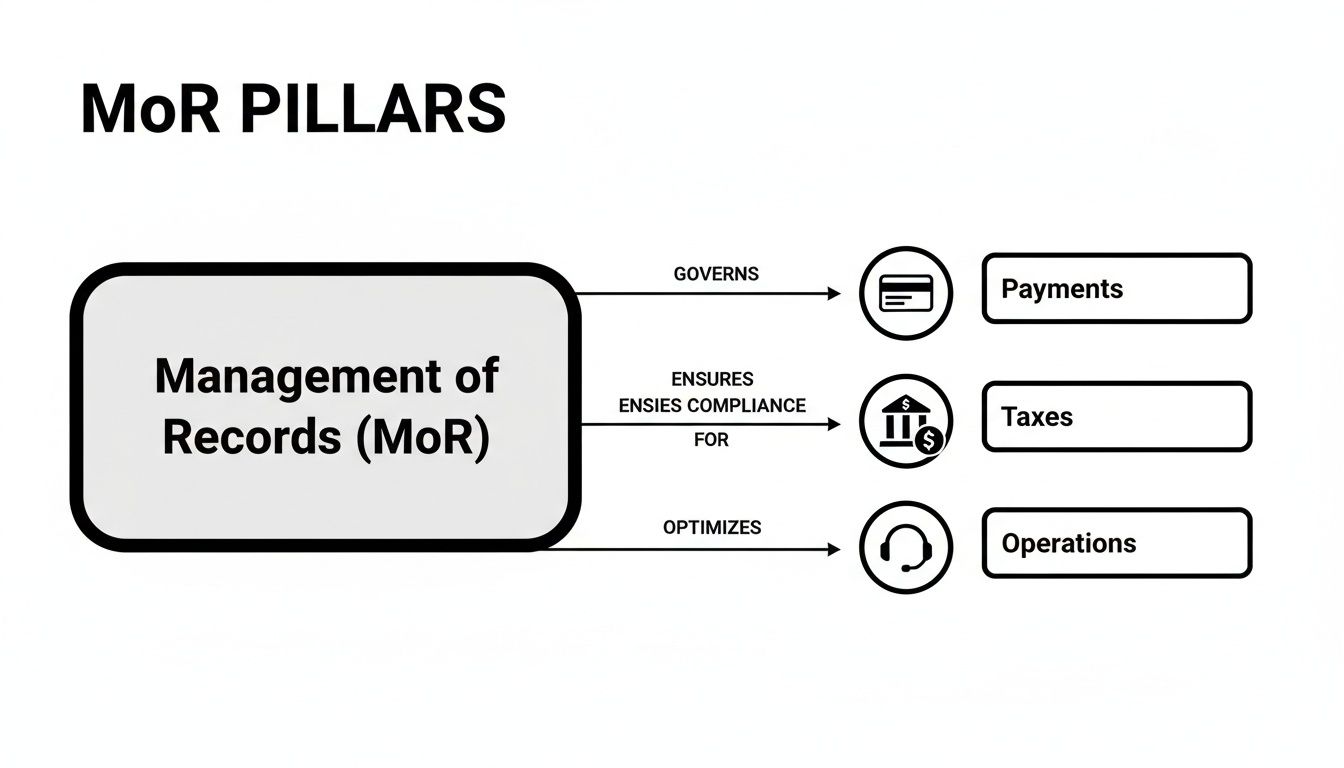

The Three Pillars of MoR Responsibility

Think of a Merchant of Record as more than just a payment processor. They step in and legally take on the full financial and regulatory weight of every single sale you make. This responsibility rests on three core pillars that essentially create a protective bubble around your business, letting you sell anywhere in the world without drowning in liability.

Each pillar handles a different, often messy, part of doing business online. By understanding them, you'll see just how much an MoR does behind the scenes, and why it’s a world away from a simple payment gateway.

Pillar 1: Payment Liability

The first and most obvious pillar is Payment Liability. This is where the MoR puts its own money on the line for every transaction. It's not just about getting the customer's payment to you; it's about owning the entire financial journey of that payment, warts and all.

Here’s what that actually means:

Handling Chargebacks and Disputes: When a customer disputes a charge, the MoR steps in to manage the fight. If they lose the dispute, the MoR eats the cost, not you. This alone can save you from a huge financial drain and countless hours of administrative headaches.

Managing Fraudulent Payments: The MoR is on the hook for sniffing out and blocking fraud. If a bad payment gets through their defenses, it’s their loss, not yours.

Covering Transaction and Currency Fees: All those pesky bank fees, processing costs, and currency conversion charges are bundled and handled by the MoR. This makes your revenue predictable and your accounting much simpler.

Simply put, the MoR takes on full payment liability so the revenue you earn is the revenue you keep. You're shielded from the chaotic and costly world of chargebacks and online fraud, two of the biggest risks of selling internationally.

Pillar 2: Tax and Compliance Liability

Next up is Tax and Compliance Liability. For most businesses, this is the single most complex and valuable service an MoR provides. Selling globally throws you into a maze of tax laws that are constantly changing and wildly different from one country to the next.

A Merchant of Record takes this entire burden off your shoulders by:

Calculating Sales Tax, VAT, and GST: The MoR figures out exactly which consumption tax applies based on each customer’s location, whether it's VAT in the UK, GST in Australia, or a specific sales tax in a U.S. state like California.

Collecting and Remitting Taxes: After charging the correct tax, the MoR is legally responsible for filing all the right paperwork and sending the money to the dozens of different tax agencies around the globe.

Maintaining Regulatory Compliance: This also includes meeting strict payment security standards. You can dive deeper into these rules in our guide on what PCI DSS compliance is and why they’re non-negotiable.

Honestly, global tax is so complicated that it’s normally a job for specialists. Looking at what a tax accountant does gives you a glimpse of the expertise needed, and an MoR has all of that baked right into its service.

Pillar 3: Operational Liability

The final piece of the puzzle is Operational Liability. This pillar covers all the day-to-day administrative work and customer service issues tied directly to billing. By outsourcing these tasks, you free up your team to focus on what they do best, which is building great products and keeping customers happy.

An MoR’s operational duties include:

Billing-Related Customer Support: The MoR becomes the first point of contact for customers with questions about an invoice, a specific charge, or a payment method.

Managing Refunds: When a customer needs a refund, the MoR handles the entire process, from executing the financial reversal to managing the paperwork.

Subscription Management: For SaaS and other recurring revenue businesses, the MoR manages the entire subscription lifecycle, including automated billing, dunning (chasing failed payments), and renewals.

With online sales continuing to boom, the value of having a partner manage these three pillars is clearer than ever. The merchant acquiring market, which underpins MoR services, has grown into a massive industry for a reason. An MoR's ability to absorb payment risks, tax headaches, and operational burdens is what makes it such a powerful ally for any business with global ambitions.

How a Merchant of Record Compares to Other Payment Models

Picking the right payment model is one of those crucial decisions that can define your company's growth trajectory. It's a choice that ripples through everything, from your team's day-to-day workload to your global sales potential and legal exposure. A Merchant of Record (MoR) is a powerful solution, but it’s just one of several ways to handle payments.

To really get a feel for its value, you need to see how an MoR stacks up against the other options out there, like going it alone as your own merchant, using a Payment Service Provider (PSP), or selling through a third-party marketplace. Each path comes with its own set of trade-offs on liability, cost, and control. It's a different world from simply finding the best payment gateway for WooCommerce.

The image below breaks down the core functions an MoR takes off your plate.

As you can see, an MoR bundles the complexities of payments, tax compliance, and operations into a single, managed service, which can be a game-changer for businesses looking to scale.

MoR vs. Being Your Own Merchant

The most basic choice you have is whether to handle everything yourself or partner up. When you act as your own merchant, you’re in the driver's seat, which means you hold all the control, but also all the risk. You are the legal entity selling the product, making you responsible for every single part of the transaction.

This means your team is on the hook for:

Securing and maintaining a merchant account with an acquiring bank.

Managing all the technical aspects of payment processing.

Absorbing 100% of the liability for costly chargebacks and fraud.

Calculating, collecting, and remitting sales taxes and VAT in every jurisdiction you sell to.

A Merchant of Record, on the other hand, steps in and assumes all of those burdens for you. The MoR becomes the seller on paper, effectively insulating your business from the financial and legal liability of each sale. That’s the core trade-off, where you give up a small slice of revenue in exchange for nearly eliminating risk and operational headaches.

MoR vs. Payment Service Provider (PSP)

This is a big point of confusion for many businesses. A Payment Service Provider (PSP) and an MoR are not the same thing, as they play fundamentally different roles. A PSP is essentially a technical connector; it builds the bridge between your website and the card networks required to process a payment. You can learn more in our detailed guide on what a PSP is.

While a PSP handles the payment flow, you are still the merchant of record. The PSP doesn't take on liability for taxes, fraud, or chargebacks. When a customer disputes a charge, that's your problem to solve. If you owe sales tax in another country, your finance team is responsible for figuring it out.

Think of it this way: A PSP is like hiring a courier to move money from your customer to your bank. An MoR is like hiring a full-service distributor who handles the entire sale, manages all the risk, and then pays you your share.

Suby, for instance, offers a streamlined way to accept card or crypto payments via a simple API, with all your revenue settled directly in USDC. This is fantastic for simplifying cash flow and avoiding currency swings. However, with this model, you remain your own merchant and retain full responsibility for your own tax and compliance obligations.

MoR vs. Marketplace

Selling on a marketplace like Amazon, Etsy, or Apple's App Store is another popular route. In this scenario, the marketplace itself typically acts as the Merchant of Record. They process the payments, handle sales tax, and manage customer billing, which makes it incredibly easy to start selling quickly.

But that convenience comes with some serious strings attached:

Brand Dilution: Your product is just one of many, listed right next to your biggest competitors. The marketplace's brand always comes first, not yours.

High Fees: Marketplaces are known for taking a significant cut from every single sale, which can eat into your margins.

No Customer Relationship: You get little to no direct access to your customer data, making it nearly impossible to build loyalty or a long-term relationship.

Strict Rules: You're playing in their sandbox, so you have to follow their strict rules on everything from product listings to marketing.

A marketplace can be an excellent sales channel, but relying on it exclusively means surrendering control over your brand, your customers, and ultimately, your profitability. An MoR gives you the best of both worlds: you offload the back-office complexity while still selling directly from your own website, owning your brand, and keeping your customer data.

MoR vs. PSP vs. Marketplace: A Head-to-Head Comparison

To make the differences even clearer, let's break down how these models compare side-by-side. This table highlights the key trade-offs you'll make in terms of who holds the liability and what it costs you.

Feature | Merchant of Record (MoR) | Payment Service Provider (PSP) | Marketplace |

|---|---|---|---|

Sales Tax & VAT Liability | MoR assumes full liability. | You are fully liable. | Marketplace assumes liability. |

Chargeback & Fraud Liability | MoR assumes full liability. | You are fully liable. | Marketplace assumes liability. |

Branding & Customer Experience | Full control on your own site. | Full control on your own site. | Limited; controlled by the marketplace. |

Customer Data Ownership | You own all customer data. | You own all customer data. | Marketplace owns the data. |

Typical Cost Structure | All-in-one fee (% of sale). | Per-transaction fees + monthly fees. | High commission (% of sale). |

Implementation Effort | Simple; single integration. | Complex; requires merchant account. | Simple; list products on platform. |

Ultimately, the right choice depends entirely on your business goals, your appetite for risk, and how much control you want to maintain over your brand and customer relationships.

When Should You Use a Merchant of Record?

Figuring out if you need a Merchant of Record (MoR) is a critical fork in the road for any growing online business. It's more than just a backend payment decision; it's about how you plan to scale, where you focus your team's energy, and how much risk you're willing to handle yourself.

While being your own merchant gives you ultimate control, there comes a point where the administrative weight starts to crush your momentum. An MoR is the partner you bring in when you're ready to go global without getting tangled in a web of global regulations. Here are the clear signals that it’s time to start looking for one.

You're Selling Globally or Planning to Expand Fast

The classic reason to look for an MoR is simple: you're selling across borders. If you already have customers in a few different countries or have big plans to enter new markets, the operational headaches can pile up fast.

Think about it. Each country has its own way of doing things:

Local payment methods: Someone in the Netherlands will expect to pay with iDEAL, while a customer in Germany might look for Sofort. An MoR has these popular local options ready to go from day one.

Currency headaches: Juggling multiple currencies, shifting exchange rates, and banking fees adds a whole layer of financial management you probably didn't sign up for.

Tax laws: This is the real monster. Every country, and often, every state or province, has its own rules for sales tax, VAT, and GST, especially for digital goods.

A Merchant of Record is designed specifically for this kind of complexity. Instead of your team spending months untangling the rules for each new country, an MoR lets you flip a switch and start selling. They’ve already done the hard work of setting up the legal and financial rails.

You Don't Have an In-House Tax and Legal Army

Be honest: does your finance team have the bandwidth to calculate, file, and remit Value-Added Tax (VAT) for every customer in the EU? What about tracking sales tax nexus laws across all 50 U.S. states or handling Goods and Services Tax (GST) in Australia and Canada?

If that question makes you break out in a cold sweat, you're a perfect candidate for an MoR. Global tax compliance isn't something you can just "figure out." The penalties for getting it wrong are steep, from crippling fines to audits that can halt your growth entirely. An MoR steps in and takes on 100% of this liability, essentially becoming your outsourced global compliance department.

You Want to Offload Financial and Fraud Risk

Every online sale carries risk, especially from fraudsters and chargebacks. As you grow, you become a bigger target. Managing disputes and eating the cost of fraudulent transactions can become a major drain on your time and revenue.

An MoR absorbs this risk for you. Because they process transactions at such a massive scale, they have incredibly sophisticated fraud prevention systems. When a chargeback happens or a fraudulent purchase gets through, the MoR takes the financial hit, not you. This keeps your revenue predictable and protects your bottom line.

This is exactly why the MoR model is booming, and if you sell physical or digital goods online it pays to compare the best merchant of record for e commerce before committing. The global Merchant of Record software market is expected to hit $6.46 billion by 2025, driven by e-commerce and the unique demands of SaaS and subscription companies. You can dive deeper into this trend by checking out this market analysis on MoR adoption.

You Sell Digital Products, Subscriptions, or Community Access

The MoR model is practically tailor-made for businesses selling digital goods like software, e-books, and online courses. The tax laws for these products are notoriously confusing and change all the time. An MoR specializes in this and stays on top of it for you.

For subscription businesses, the benefits are even clearer. An MoR manages the entire customer billing lifecycle, including:

Handling automated renewals.

Running dunning campaigns to chase down failed payments.

Ensuring your subscription terms comply with local consumer protection laws.

This is also a game-changer for creators and community managers who monetize access to platforms like Discord or Telegram. An MoR can manage the entire subscription process compliantly, no matter where your members are in the world.

It's important to remember that an MoR, which takes on full liability, is just one option. Other tools focus on simplifying specific parts of the payment process. A platform like Suby, for example, offers a streamlined way for businesses to accept card or crypto payments globally with a simple API and get settled in USDC. This is great for simplifying international cash flow, but with Suby, you are still your own merchant. That means you remain responsible for your own taxes and legal compliance.

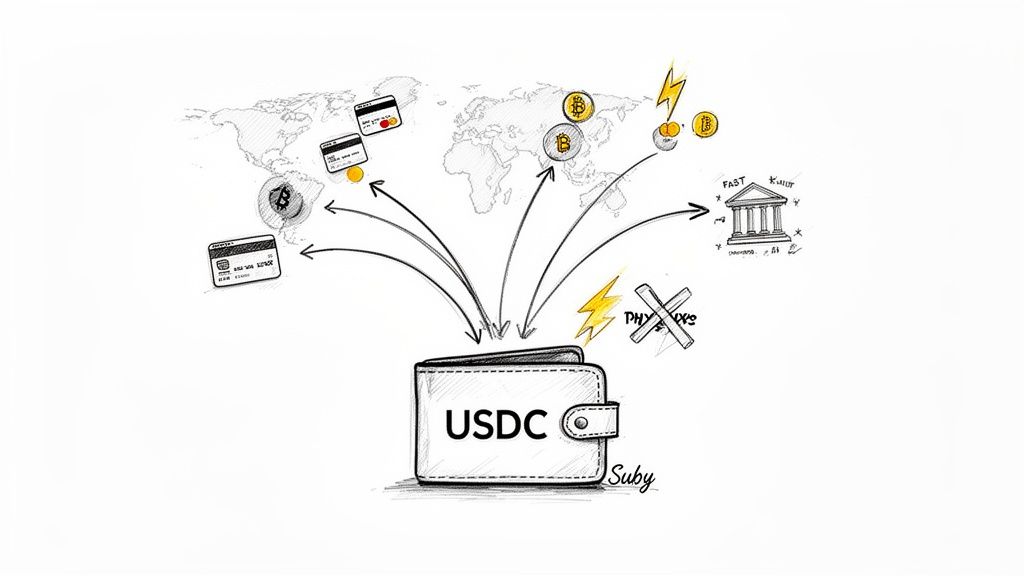

How Suby Streamlines Your Global Payments

While a Merchant of Record can be a great way to offload legal and tax burdens, it’s not the only solution for selling globally. There's another path, one that tackles the operational headaches and cash flow problems of international business head-on. This is where a specialized payment layer like Suby fits in.

Let’s be crystal clear: Suby is not a Merchant of Record. When you partner with us, you are still your own merchant. This means you retain full control and responsibility for your business's tax, compliance, and legal duties for every transaction.

Instead of acting as a reseller, Suby gives you a powerful payment infrastructure designed to cut through the red tape of getting paid. Our focus is squarely on eliminating the friction that kills global revenue, like painful currency conversions, volatile exchange rates, and week-long bank settlements.

Receive Global Payments with Predictable Payouts, to Your Bank or in Stablecoins (USDC, EURC)

The idea behind Suby is simple but powerful. Your customers pay from anywhere in the world using their card or crypto, and you get paid instantly in USDC directly to your wallet.

This completely changes the game for modern internet businesses. Gone are the days of juggling multiple currency accounts, losing a cut of your revenue to surprise exchange rate swings, or staring at your bank account waiting for an international wire to land. Your revenue shows up fast, in a stable digital dollar format you can count on.

Think of it this way: Suby solves the cash flow problem of selling internationally. Your customers get a simple, familiar checkout, and you get fast, stablecoin revenue without the usual banking delays and currency nightmares.

This approach is perfect for businesses that want to keep direct control over their finances and customer relationships but still need to simplify a critical piece of the global sales puzzle. If you want to dig deeper into this topic, you can learn more about overcoming the challenges of cross-border payments in our detailed guide.

Built for Modern Creators and Developers

We designed Suby for speed and simplicity. You can monetize your work worldwide without needing a big team or a massive budget. We offer a few different ways to get up and running in minutes.

For developers, our straightforward API and webhooks make it easy to embed a world-class payment system right into your application. This gives you the power to create custom checkout flows and automate your backend for any business model you can dream up.

Don't write code? No problem. Our shareable paylinks can be sent directly to clients or posted anywhere online, making it incredibly easy to accept payments for services, digital goods, or one-off projects.

Suby also comes with native integrations for the platforms where communities thrive:

Discord: Automatically grant or revoke access to paid servers and private channels based on a user's subscription status.

Telegram: Manage membership in your private groups and communities by linking access directly to a successful payment.

These tools give creators and community managers everything they need to launch and grow subscription-based businesses with minimal operational overhead. By bringing payment processing, access management, and subscriptions under one roof, Suby provides a clear path to global revenue, all while you stay in the driver's seat as your own merchant.

Choosing Your Path to Global Sales

Alright, we've unpacked the different models, from taking on the full weight of being a merchant of record yourself to layering in different payment solutions. Now comes the hard part: making a decision. This isn't just a technical detail; it's a strategic choice that will define how you grow, where you can compete, and how much complexity you're willing to own.

The good news is that you don't need a complex consulting project to find your way. By asking a few honest questions, you can get a clear picture of what your business truly needs. The goal is to choose a path that fuels your international growth, not one that bogs you down in paperwork and risk.

A Practical Self-Assessment Framework

Let's get practical. To figure out your next move, grab your team and work through these four key areas. This isn't about ticking boxes; it's about having a realistic conversation about your capabilities and ambitions.

Map Your Global Footprint: First things first, where are you actually selling? Make a list of every single country where you have customers today or plan to expand within the next year. Be thorough, don't just list the big ones. This map is your starting point for understanding your true tax and legal exposure.

Assess Your Compliance Readiness: Now, have an honest look at your team. Do you have in-house experts who live and breathe global sales tax, VAT, and GST? Can they confidently manage remittances in every single jurisdiction on your map? This is a critical gut-check. Underestimating the compliance burden is one of the fastest ways to run into trouble when you act as your own merchant of record.

Calculate Your True Payment Costs: Your payment processing statement is only part of the story. You need to dig deeper. What are you really paying in currency conversion fees, international wire costs, and most importantly, the hours your team spends managing providers and reconciling accounts? These "soft costs" can be a massive, hidden drain on your profitability.

Determine Your Risk Tolerance: Finally, how much financial risk can your business stomach? Think about the real-world impact of chargebacks and fraud on your cash flow. If you have a high tolerance for risk and the resources to fight it, acting as your own merchant might be viable. If not, you’ll want a solution that takes that liability off your plate.

This self-assessment isn't about finding one "right" answer. It's about building a clear, honest picture of your company's specific situation. The results will point you directly toward the model that makes the most sense for you right now.

After this evaluation, you’ll know whether you need a full merchant of record to handle all the legal and tax liability for you. Or, you might find that a streamlined payment layer is a much better fit. For instance, a solution like Suby allows you to remain your own merchant but simplifies your cash flow by letting you accept card payments globally and receive settled funds as USDC. This gives you faster access to revenue with far more control.

Common Questions About the Merchant of Record Model

As you start looking into selling globally, you'll inevitably run into the term "merchant of record." It can seem complicated, but it doesn't have to be. Let's clear up some of the most common questions people have.

Is a Merchant of Record Just Another Name for a Payment Gateway?

That’s a common point of confusion, but they play fundamentally different roles.

Think of a payment gateway as a secure digital messenger. Its only job is to encrypt your customer's payment details and shuttle them safely from your website to the bank for approval. You are still the one making the sale, and all the liability, from taxes to returns, sits with you.

A merchant of record, however, becomes the legal seller of your product for that transaction. They don't just pass along payment info; they take on the full financial and legal responsibility for the sale itself. This means they're on the hook for calculating and remitting taxes, dealing with chargebacks, and staying compliant with local laws.

What Does It Actually Cost to Use an MoR?

Most MoR providers bundle all their services into a single, all-inclusive fee. This is usually a percentage of your revenue, often ranging from 5% to 10% per transaction, sometimes with a small fixed fee on top.

At first glance, that might seem steep compared to the fee from a basic payment processor. But it's crucial to look at what's packed into that number. It covers not just payment processing but also currency conversion, sophisticated fraud prevention, and most importantly, the enormous headache and expense of managing global tax and legal compliance.

Are MoR Services Only for Big Companies?

Not anymore. While MoR solutions were once the domain of large enterprises with deep pockets, the game has changed. Today, many providers are built specifically for startups, independent creators, and small businesses.

For a smaller team, an MoR can be a game-changer. It opens the door to international markets right from the start, without the need to hire an in-house team of finance and legal experts just to handle cross-border sales. When you get down to picking a specific provider, a focused breakdown like this paddle vs fastspring comparison for software sales can show how two established MoRs stack up on fees and features.

How Is My Customer's Data Handled by an MoR?

When you partner with a merchant of record, they take on the role of the data controller for the transaction itself. This is a big deal. It means they become legally responsible for protecting that customer data in line with privacy regulations like GDPR in Europe and CCPA in California.

They are also required to maintain full PCI DSS compliance, the gold standard for securing credit card information. In effect, a huge piece of the data security and compliance burden is lifted off your shoulders and placed onto the MoR's.

Suby is a payment gateway and Merchant of Record. Your customers pay with card, bank transfer, Apple Pay, Google Pay, Klarna, and more, or stablecoins, and you get paid out to your bank account, or directly in stablecoins (USDC, EURC) to your wallet, anywhere in the world, no bank account required. Whether you want a full Merchant of Record to absorb tax and compliance liability, or a payment layer where you stay your own merchant and simply settle global sales faster, Suby gives you both paths without handing over control of your customer relationships.