Gaspard LEZIN

A Guide to Modern Cross-Border Payment Solutions

Struggling with slow, costly global transactions? Learn how modern cross-border payment solutions use USDC to simplify payouts and scale your business.

A cross-border payment is simply a transaction where the buyer and seller are in different countries. It sounds straightforward, but if you’ve ever tried to send or receive money internationally, you know the reality is often complex. These payments can be slow, expensive, and frustratingly complicated.

What Is a Cross-Border Payment and Why Is It So Hard?

The main problem is that most international payments still rely on financial systems built decades ago. This outdated infrastructure passes your money through a long chain of intermediary banks, and each stop along the way adds its own fees and delays.

Think about sending an international package. You wouldn't expect it to be opened, rerouted, and stamped by a dozen different post offices, each charging you for the trouble. Yet, that's almost exactly what happens with your money. For any modern internet business trying to operate on a global scale, this process is a major roadblock.

The Hidden Journey of Your Money

Let's say a customer in Japan buys your product using their local currency, yen, but your company is based in the United States. That money doesn't just appear in your U.S. dollar account. Instead, it goes on a winding, behind-the-scenes journey through a network of correspondent banks.

Here’s a rough idea of what that trip looks like:

The customer's bank in Japan starts the transfer.

The funds move to a larger intermediary bank, which handles the currency exchange from JPY to USD.

Sometimes, another intermediary bank is needed to get the funds closer to your bank.

Finally, the money arrives at your bank, which then credits your account.

Every single step in this chain is a point of failure. It introduces delays, unclear fees, and the risk of something going wrong. This system was never designed for the speed and volume of today’s global economy, creating friction that eats directly into your cash flow and profits.

The Staggering Scale of Global Payments

Solving this isn't just a matter of convenience, it's a massive economic necessity. In 2023, the global cross-border payments market was valued at an incredible US$190 trillion. Projections show it growing to US$290 trillion by 2030, which gives you a sense of the sheer scale of money moving around the world to power everything from e-commerce to global supply chains.

But look at the cost. Corporate cross-border payments alone make up US$23.5 trillion of that volume but rack up over US$120 billion in transaction fees. That’s billions of dollars lost to inefficiency.

For a global business, getting paid shouldn't feel like a roll of the dice. The old way forces you to accept currency swings, unpredictable payout times, and high fees as the price of doing business internationally.

A modern approach cuts out the middlemen for a simpler, more direct path to your revenue. It lets your customers pay with familiar methods like credit cards, while you receive the funds quickly and predictably. For instance, a customer can pay with their card, and the business gets its settlement in a stablecoin like USDC. This model completely bypasses the slow, multi-bank process.

Using an API like ours at Suby, any business can start accepting payments by card or crypto. We even have integrations for platforms like Discord and Telegram to help you manage subscriptions and paid communities. This approach simply removes the barriers that make traditional cross-border payments so difficult, letting you grow internationally without the usual financial headaches.

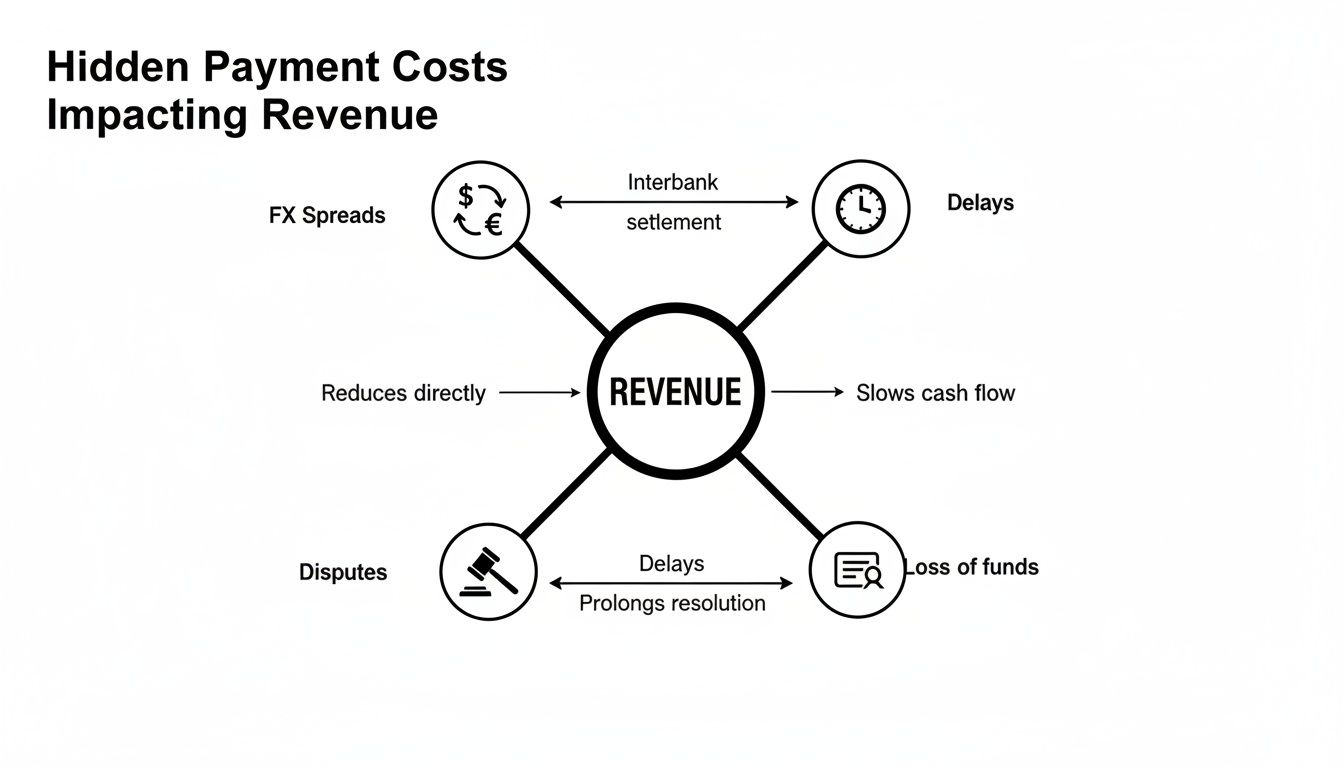

The Hidden Costs Eating Into Your Global Revenue

That big international sale looks fantastic on your dashboard, but how much of that money actually makes it to your bank account? The journey a payment takes across borders is riddled with traps that quietly siphon off your profits, turning a promising revenue stream into a financial headache.

These aren't just minor annoyances. They're real financial and operational drains. For any business selling internationally, spotting these hidden costs is the first step to taking back control of your revenue. Let's pull back the curtain on the four main issues that are probably costing you more than you think.

1. Punishing Foreign Exchange (FX) Spreads

When a customer in another country pays you, that money has to be converted into your home currency. This is where banks and payment processors make a lot of money with something called the foreign exchange (FX) spread.

They don't just use the real, mid-market exchange rate. Instead, they buy the currency at one price and sell it to you at a slightly worse one. That difference, the spread, is their profit, and it functions as a hidden fee. A few cents here and there might not sound like much, but across thousands of transactions, it's a huge deal. Those spreads can easily eat away 2-5% of your total international revenue before it ever touches your books. It's like paying a secret tax just for doing business globally.

The true cost of a cross-border payment isn't the fee you see on your statement. It's the tangled mess of opaque FX markups, frustrating settlement delays, compliance overhead, and a painful dispute process that really hits your bottom line.

One way to sidestep this completely is to move away from traditional currency conversion. When you accept card payments but get paid out in a stablecoin like USDC, you receive a stable, dollar-equivalent digital asset. This shields your revenue from volatile currency markets and those sneaky markups.

2. Unpredictable Settlement Delays

Old-school payment networks, especially the SWIFT system used for international bank wires, are notoriously slow. A single transfer can take 3 to 5 business days to land in your account, and that's if everything goes smoothly. If it gets flagged at an intermediary bank, you could be waiting even longer.

This isn't just inconvenient, it wreaks havoc on your cash flow. Imagine having to wait a full week for money from a sale you made today. It makes financial planning a nightmare and can hamstring your ability to pay suppliers, fund marketing, or reinvest in growth. The money is yours, but it’s stuck in a complex, archaic system you have no control over.

A better way is to get your money almost instantly. For example, Suby offers an API that lets any business take card payments and receive the funds as USDC in minutes, not days. That kind of speed and predictability is a game-changer for any modern internet business that needs to move fast.

3. The Crushing Weight of Compliance

Trying to keep up with international payment rules is a massive headache. Every country has its own set of regulations for payments, taxes, and data privacy. Just staying compliant demands a ton of time, expensive legal advice, and specialized knowledge, all of which add up to serious operational costs.

For smaller businesses, this complexity can be a dealbreaker, stopping global expansion before it even starts. The risk of getting it wrong and facing heavy fines is just too high. Even huge corporations have entire teams dedicated to this problem. If you want to dig deeper into the financial side of things, we wrote a detailed article on how to avoid currency conversion fees.

4. Frustrating Cross-Border Disputes

Chargebacks are already a pain. But when they happen across borders, the complexity multiplies. You're suddenly dealing with different consumer protection laws, language barriers, and time zone gaps that can drag a simple dispute out for weeks.

Every minute your team spends on these issues is time they aren't spending on growing the business. And if you lose the dispute, you're out the revenue and the product. It’s just another layer of risk and cost baked into every international sale.

When you're running a business that sells to customers worldwide, the way you get paid is a huge deal. It’s not just about money landing in your account. The underlying system, what we call the payment "rails", dictates how fast you get your cash, how much it costs, and how much of a headache it is to manage.

To really get a handle on this, you need to understand the three main ways money moves across borders: the old-school bank wire system, the familiar card networks, and the new kid on the block, stablecoin rails. Each has its own quirks, and picking the right one can make or break your international operations.

Comparing the Three Main Cross-Border Payment Rails

Let's dive into how these systems actually stack up for a modern internet business.

1. Bank Transfers (The SWIFT System)

For a long time, the only real option for international transfers was the SWIFT network. Think of it as a messaging system that lets banks talk to each other across the globe. It’s built on a web of "correspondent banks," meaning your customer's payment doesn't travel directly to you. Instead, it hops from one partner bank to another until it finally reaches your account. For a deeper dive, here's a great resource for understanding how SWIFT payments work.

This system was designed for a different era. For today's online businesses, it's riddled with problems:

It’s slow. A transfer routinely takes 3-5 business days to finally settle. That’s a long time for your revenue to be stuck in limbo, which can really mess with your cash flow.

It’s expensive and unpredictable. Every bank in that correspondent chain can skim a fee off the top. You never know exactly how much will be deducted, so the amount you receive might be a nasty surprise.

It’s a black box. Once a payment is sent, tracking it is nearly impossible. You’re left wondering where the money is, which means more time spent on administrative follow-ups.

It’s easy to think of fees as the only cost, but the real damage to your bottom line comes from a mix of hidden issues.

These aren't just minor annoyances, they are real drains on your profit and your team's time.

2. Card Networks (Visa, Mastercard)

Card payments are what your customers know and trust. For anyone running an e-commerce or SaaS business, offering a seamless checkout with Visa or Mastercard is non-negotiable for conversions. From the customer’s perspective, it’s simple and instant.

But behind the scenes, it’s a different story for you, the merchant.

While a card transaction is much faster than a SWIFT wire, the settlement process still relies on traditional banking systems. This means you're still exposed to currency conversion fees, high chargeback risks, and payout holds from payment processors that can tie up your funds for days.

Essentially, card networks solve the customer's problem, but not yours. You still face delays and uncertainty when it comes to getting your hands on your own money.

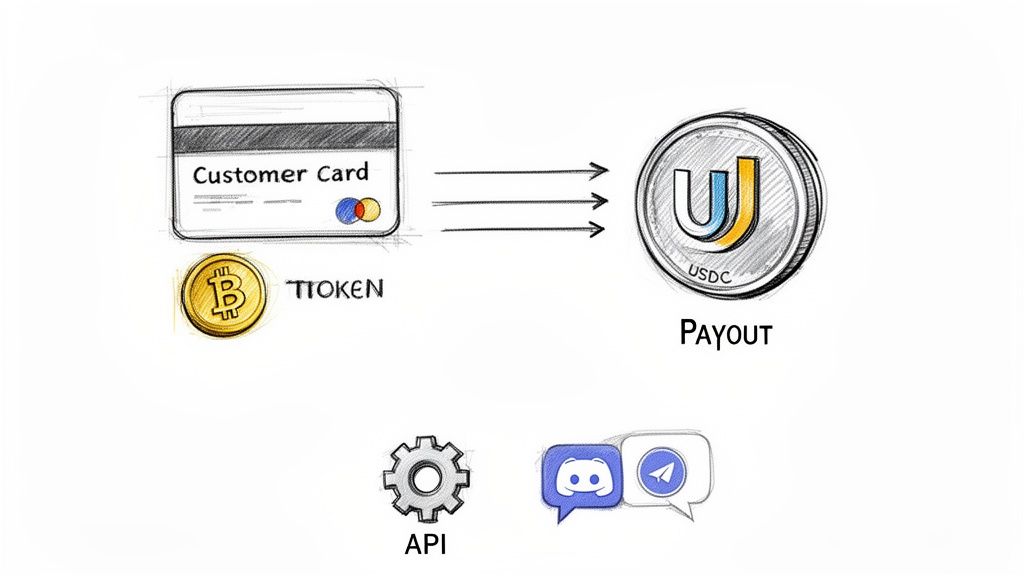

3. Stablecoin Rails (USDC Payouts)

This brings us to the most modern and efficient option: payment rails built on stablecoins like USDC. Instead of navigating the maze of correspondent banks, stablecoins create a direct, digital path for money to travel from point A to point B.

The momentum behind this shift is undeniable. Over 70 countries now have their own real-time payment systems, and customers' expectations for speed are changing fast. While banks still handle over 90% of B2B cross-border volume, many are now partnering with fintechs or integrating stablecoin solutions to keep up. Just look at the new payment links between Hong Kong and Thailand, which allow for instant transfers with just a mobile number, completely cutting out old-school paperwork.

Here’s how it works for your business: a customer pays on your site using their credit card as usual. On the backend, that payment is converted and settled to your corporate wallet as USDC in a matter of minutes.

The advantages are crystal clear:

Near-Instant Speed: Payouts settle in minutes, not business days. And it works 24/7, including weekends and holidays.

Radical Transparency: The fees are simple and upfront. You completely sidestep the hidden currency conversion spreads that quietly eat away at your revenue.

Complete Control: Every transaction is recorded on a public ledger, giving you an immutable and instant confirmation that the funds have arrived.

The goal is to get the best of both worlds, a familiar checkout for your customers and modern, efficient settlement for your business.

Combine a trusted user experience with backend efficiency. Your customers see a familiar card payment form, while your business benefits from the speed and stability of USDC settlement.

This hybrid model gives you high conversion rates at the point of sale and fast, predictable access to your revenue. It's exactly what we built Suby to do, making this powerful flow accessible through a simple API.

By leveraging stablecoin rails, you can operate globally without the friction that has plagued international business for decades. If you want to dig deeper into the technology, check out our guide on how to choose the right online payment gateway for your business.

Cross-Border Payment Rails: A Comparison

To put it all into perspective, here’s a side-by-side look at how the different rails compare on the factors that matter most to a business.

Feature | Bank Transfers (SWIFT) | Card Networks | Stablecoin Rails (USDC Payouts) |

|---|---|---|---|

Settlement Speed | 3-5 business days | 2-3 business days | Minutes, 24/7 |

Cost | High, with hidden intermediary fees | Moderate, with FX markups & scheme fees | Low, transparent transaction fees |

Transparency | Opaque; difficult to track funds | Moderate; some visibility through processor dashboards | Fully transparent on-chain tracking |

Cash Flow Impact | Significant negative impact; funds locked up | Moderate delay; funds held by acquirers | Minimal impact; near-instant access to funds |

Global Reach | Extensive, but with high friction | Excellent for customer checkout | Global, with a single integration |

Operational Overhead | High; requires manual tracking and reconciliation | Moderate; managing disputes and holds | Low; automated and verifiable |

As you can see, while traditional systems have their place, modern rails built on stablecoins offer a clear advantage in speed, cost, and control, the three things that matter most when you're scaling a global business.

A Modern Solution for Global Internet Businesses

So far, we've painted a pretty grim picture of traditional cross-border payments. The delays, hidden fees, and operational headaches aren't just minor annoyances, they're real obstacles that stop a global internet business from scaling. But what if you could just sidestep that entire broken system?

That’s where a modern approach comes in, one built from the ground up for the speed of today's digital economy. The core idea is surprisingly simple: break the connection between how your customer pays and how your business gets paid. Let customers use whatever method they're comfortable with, while you get your money quickly, predictably, and without losing a big chunk to currency conversion.

This diagram shows the magic of a modern payment layer. It carves a direct path from your customer's wallet to your revenue, cutting out that long, expensive chain of intermediary banks that slows everything down.

A Unified Layer for Global Commerce

The ideal setup acts as a single, unified payment layer for your business, pulling together the best parts of both traditional and modern payment rails. It lets you accept payments from literally anywhere in the world and receive your funds in a stable digital currency like USDC.

Here’s how that simple, powerful flow works in practice:

Your customer pays on your site or via a payment link. They can use their credit card or even their own crypto, whatever feels familiar and trustworthy to them. This is key for keeping conversions high.

Behind the scenes, the payment is processed and settled to your business almost instantly.

You receive your revenue directly as USDC in your company's digital wallet, often in a matter of minutes, not days.

This model is a direct answer to all the problems we've talked about. You completely bypass the sluggish, multi-day settlement cycles of the SWIFT network. You also sidestep those punishing FX spreads that quietly eat away at your profits. If you're looking to innovate, understanding the role of crypto in international trade is a good place to start.

By combining familiar card acceptance with fast USDC payouts, you get the best of both worlds. Customers get a smooth checkout, and your business gets the speed, cost savings, and predictability it needs to thrive globally.

This approach completely changes your cash flow. Instead of waiting around for funds to crawl through multiple banking systems, you have immediate access to your revenue. It puts you back in the driver's seat of your company’s finances.

Built for How Modern Businesses Operate

A modern cross-border payment solution has to do more than just move money. It needs to provide tools that fit how internet businesses actually work, whether you're a developer-led SaaS company, a solo creator selling digital goods, or a growing e-commerce brand.

For example, a platform like Suby acts as a global payment layer that combines card and crypto acceptance with fast USDC settlements. It’s designed to help companies sell worldwide without getting tangled up in currency conversion, banking delays, or payout uncertainty. We provide an API that allows any business to accept payments by card or crypto, and we also offer native integrations with Discord and Telegram for use cases like subscriptions, paid access, and online communities.

Here are some of the practical tools you should look for:

A Simple and Powerful API: For developers, a clean, well-documented API is non-negotiable. It allows you to build custom payment flows, automate invoicing, and manage subscriptions by integrating directly into your websites, apps, and backend systems.

Shareable Checkout Links: Not every business needs a complex integration. For invoicing a client, selling a digital product, or even taking a one-off payment, being able to generate a simple payment link in seconds is a game-changer. You can share it anywhere, in an email, on social media, or in a direct message.

Native Community Integrations: The creator economy is a massive driver of global commerce. A modern payment solution should integrate directly with platforms like Discord and Telegram. This lets community managers easily monetize their groups with paid access, exclusive roles, and recurring subscriptions, all handled automatically.

This is the power of a unified system. Whether you integrate via an API, embed a checkout, or just send a payment link, the core benefit is the same. The customer's payment method is completely separated from your payout. Your business receives fast, stable, and predictable revenue in USDC, letting you focus on growing your business, not chasing down payments.

Your Checklist for Choosing a Payment Provider

Picking a payment provider feels like a huge commitment, because it is. Your choice directly affects your revenue, how quickly you can access your cash, and how much time your team spends on manual work. It's easy to get lost in slick marketing, but this checklist will help you ask the right questions and see past the promises.

Think of these as the questions you need to ask to find a real partner, one that actually solves payment friction instead of just creating new headaches.

How (and When) Do You Actually Get Paid?

This is, without a doubt, the most important question. The answer tells you everything about a provider’s setup and what it will mean for your cash flow. Don’t let them get away with vague answers like "soon."

What currency do payouts land in? Do they force you into a local currency conversion before you ever see the money, or do you get settled in a stable asset like USDC? Getting paid in USDC gives you control. It protects your revenue from the hidden spreads baked into forced currency conversions.

How long does settlement really take? Get a specific timeline, from the second a customer clicks "pay" to when the money is in an account you control. Is it the standard "2-3 business days" (which can stretch over a weekend), or is it a few minutes, 24/7? For any modern business, getting your capital almost instantly is a massive advantage.

The Gold Standard: The best-case scenario is simple: your customer pays with their card, and you receive USDC in your wallet almost immediately. This model eliminates both settlement delays and currency risk in one go.

What Is the True, All-In Cost?

Payment fees can be tricky. A low headline rate looks great on a pricing page, but it’s often a smokescreen for other charges that nickel and dime your revenue away. You need to know the total cost of every single transaction.

A transparent partner has nothing to hide. Suby, for example, has a clear pricing model starting at 5% that’s designed to be all-inclusive. When you compare that to the effective cost of other platforms, once you factor in FX markups and operational headaches, it often comes out ahead. You can see the full breakdown on the official pricing page.

To find out what you’ll really be paying, ask:

Do you charge foreign exchange (FX) markups? This is the most common hidden fee. It can easily skim 2-5% off every international sale you make, and you might never even see it on an invoice.

Are there fees just to get my money out? Some providers will charge you for payouts or internal transfers. You shouldn't have to pay a toll to access your own funds.

What happens when a dispute or refund occurs? Make sure you understand the financial hit you’ll take if a transaction needs to be reversed.

Is It Built for How You Actually Work?

Your payment system should enable your business model, not hold it back. It needs to have the right tools whether you’re a developer-first SaaS company, a creator building a paid community, or a freelancer invoicing clients across the globe.

Think about how you sell and ask if the provider is built for it.

Is there a well-documented API? If you need to build custom payment flows, a simple, powerful API is non-negotiable for automating things like invoicing and subscriptions.

Can you create a simple payment link in seconds? For quick one-off sales or simple invoices, being able to generate a shareable checkout link is a huge time-saver.

Does it connect with community platforms? If you run a paid community on Discord or Telegram, native integrations that can handle subscriptions and automate access are a game-changer. This is a core part of what we've built at Suby.

Asking these tough questions upfront helps you find a solution that offers the speed, transparency, and tools you need to grow your business internationally, without the usual drama.

Getting Started with Global Payments Today

After digging into all the friction and hidden costs of cross-border payments, you might be thinking an upgrade is a massive, complicated project. But it's not. With the right tools, you can start accepting international payments in minutes, not weeks, and finally ditch the headaches of old-school finance.

This isn't some far-off future technology; it's here and ready to go. You can literally create an account, generate your first payment link, and make a global sale in the time it takes to grab a coffee. That kind of speed makes selling worldwide a real possibility for any business, no matter how small.

From Idea to Global Sale in Minutes

Let's say you have a new digital product to sell, an international client to invoice, or a growing community you want to monetize. Instead of wrestling with bank approvals and clunky integrations, a modern payment layer lets you get straight to business using simple tools built for the way we work online.

Here’s how quickly you can get moving:

Selling Digital Products: Create a payment link for your new e-book or software. Just drop it on your site or in a social media post, and customers anywhere can pay instantly with their card.

Invoicing Clients: Generate a professional invoice with a payment link built right in. Your client pays in their local currency, and you get your money fast without worrying about surprise fees.

Monetizing Communities: Set up paid access or subscriptions for your members around the globe.

It all boils down to a simple, powerful idea: your customer gets a familiar card payment experience, while your business gets fast, predictable USDC settlement. This hybrid model gets rid of currency risk and cash flow delays, so you can focus on your business instead of your bank.

Monetize Communities on Discord and Telegram

One of the most practical applications is monetizing online communities. Platforms like Suby can automate access management for Discord and Telegram, letting creators sell memberships and digital access globally. The payment processing, access control, and subscription management are all handled in one place, cutting out all the manual admin work. As our own documentation shows, you can launch in minutes and scale internationally without needing any extra payment infrastructure. You can learn more about how to set up and manage community monetization with our documentation.

Ready to see how simple it is in practice? We've put together a complete walkthrough to guide you. Check out our guide on how to accept international payments and take the first step toward leaving outdated payment systems behind.

Frequently Asked Questions

We get a lot of questions about how USDC actually works for business payouts. Here are answers to a few of the most common ones we hear from merchants just like you.

Is Receiving USDC as a Business Complicated?

Not in the slightest. Getting paid in USDC is surprisingly straightforward. All you really need is a compatible digital wallet, which you can have up and running in just a few minutes. When you use a provider like Suby, we send payouts directly to your wallet address.

This way, you get to skip the headaches of managing multiple international bank accounts and avoid the notorious delays that come with SWIFT transfers. The funds show up fast, giving you immediate control over your revenue to manage, convert, or use however you see fit. It’s a much simpler way to handle treasury for a global business.

How Do I Handle Accounting for USDC Revenue?

You can treat your USDC revenue much like you would any other foreign currency. Most modern accounting software makes it easy to track these transactions and record the value of the USDC at the exact moment you receive it.

Because USDC is pegged 1:1 with the US dollar, its value is stable. This makes bookkeeping much simpler compared to dealing with volatile cryptocurrencies.

Platforms like Suby give you a clear dashboard showing your complete transaction history, which you can export for your records at any time. Of course, we always recommend chatting with a qualified accountant to make sure all your local tax and reporting obligations are covered.

What Is the Main Benefit of Card Payments with USDC Settlement?

The real magic here is getting the best of both worlds: a familiar, trusted payment experience for your customers and a far more efficient backend for your business. Your customers pay with their Visa or Mastercard, a process they already know and trust, so you don't have to worry about your checkout conversion rates dropping.

Meanwhile, on your end, the funds settle almost instantly as USDC. This model gives you a seamless front-end for your buyers and fast, low-cost, predictable cash flow for your business, all without the usual currency risks or frustrating payout holds. Our API allows any business to accept payments by card or crypto, and we offer native integrations with Discord and Telegram.

Ready to modernize your cross-border payment flow? With Suby, you can accept card payments from customers worldwide and receive fast, predictable USDC settlements. Get started in minutes.