You’ve probably seen the same pattern. A creator wants to launch a digital product fast, a friend says “use Gumroad,” and twenty minutes later the browser has ten tabs open asking the same question in different ways: is gumroad safe?

That question is more important than many realize. It isn’t about whether a checkout page is encrypted. It’s also about whether buyers can trust what they’re purchasing, whether refunds are predictable, and whether creators can rely on the platform to keep income flowing without surprise disruptions.

For casual selling, Gumroad can feel convenient. For a business that depends on stable revenue, convenience isn’t enough. You need to know what risks sit underneath the simple setup.

Table of Contents

- Weighing Your Options in the Creator Economy

- What protects the transaction

- What that means in practice

Weighing Your Options in the Creator Economy

A first-time seller and a full-time creator ask “is gumroad safe” for different reasons.

The first seller means, “Can I put up a product tonight and collect payments without causing problems for customers?” The full-time creator means, “Can I trust this platform with my reputation, my support workload, and my income next month?”

Those are not the same question.

Gumroad sits in a category that a lot of creators like because it removes setup friction. You don’t need to build a full store from scratch to sell an ebook, template pack, membership, or download. That simplicity is real, and it’s one reason the platform keeps coming up in creator circles.

But the safety discussion gets oversimplified. People reduce it to card security, which is one layer.

A safe checkout does not automatically create a safe business.

From a consulting perspective, I look at three separate risks:

| Risk area | What buyers care about | What creators care about |

|---|---|

| Payment security | Is my card data protected? | Will transactions be processed securely? |

| Marketplace trust | Is the seller legitimate? | Will customers trust the storefront? |

| Business stability | Can I get support if something goes wrong? | Can I count on payouts and account continuity? |

Gumroad scores better on the first category than many people assume. It gets less comfortable in the second. It gets more serious in the third, especially if the platform is your revenue channel.

That’s why the right answer is not a simple yes or no. For buyers, the main issue isn’t stolen card details. For creators, the bigger issue isn’t encryption. It’s platform dependence, payout reliability, and what happens when something gets flagged.

How Gumroad Secures Payments and Data for Buyers

For transaction security, Gumroad is stronger than many skeptical buyers expect.

What protects the transaction

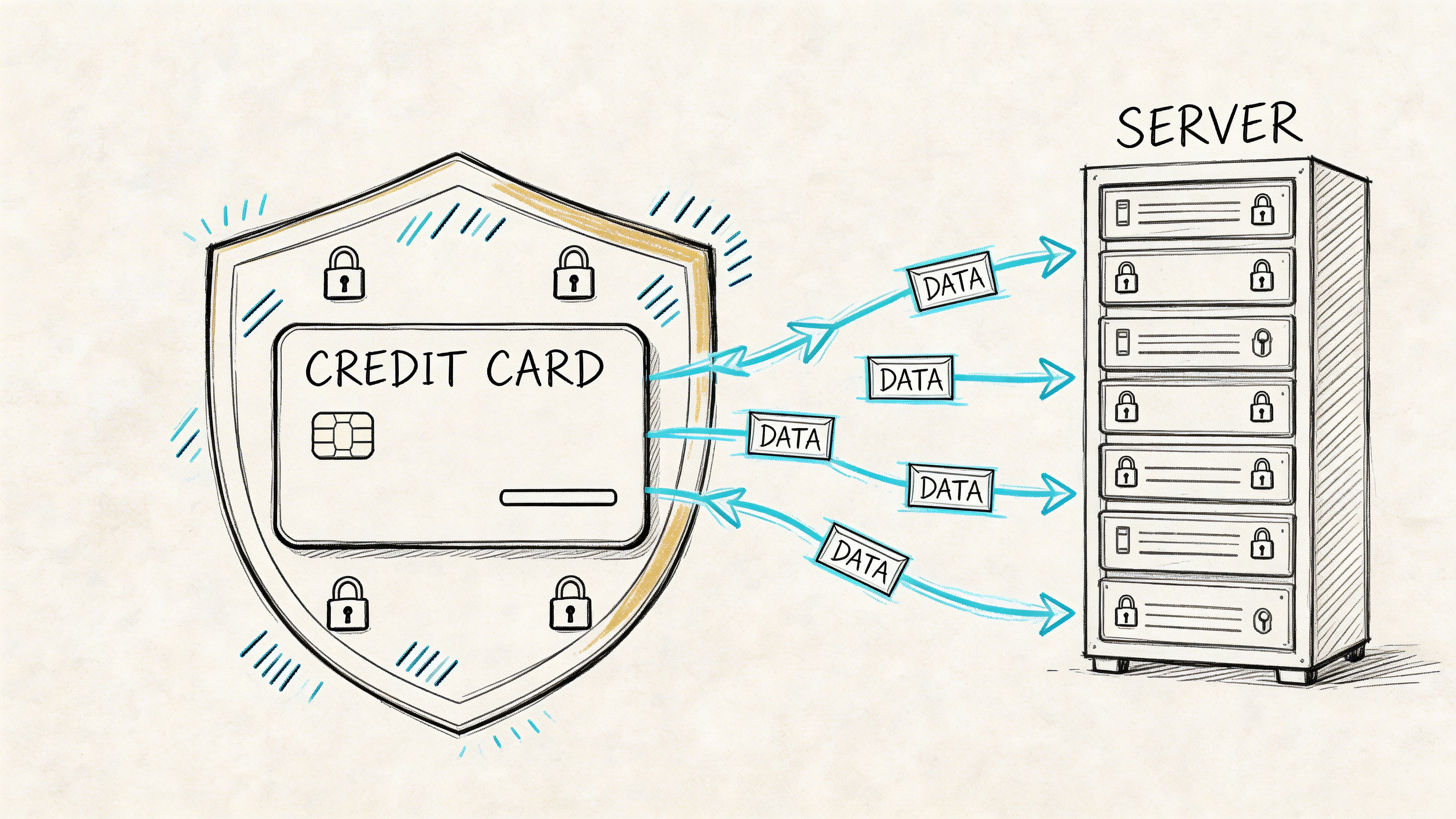

Gumroad says it uses 256-bit TLS encryption with modern SHA2 cyphers for payment transactions, and it processes payments through PCI DSS-compliant providers such as PayPal. It also states that it does not store sensitive card details on its own servers, relying on tokenized representations instead (Gumroad safety documentation).

That matters because the biggest fear most buyers have is clear. They want to know whether entering a card number on a Gumroad checkout page exposes them to obvious payment risk.

In practical terms, the answer is that Gumroad’s checkout security follows the same logic used across modern online payments. If you want a plain-English breakdown, this guide on what is a payment gateway and how it works is useful background for understanding how the checkout, processor, and merchant roles are separated.

A related concept is PCI compliance. If you want the technical side in simpler terms, this explainer on https://www.suby.fi/post/what-is-pci-dss-compliance gives a good overview of why merchants try to avoid storing raw card data themselves.

What that means in practice

For buyers, this setup reduces the risk that a seller can see or misuse card details. It also lowers the impact of a platform compromise because tokenized payment data is not the same thing as storing full card information.

A few practical takeaways matter here:

- Checkout traffic is protected in transit. The encryption layer is there to protect data moving between the browser and Gumroad.

- Card handling is outsourced. That’s often safer than a smaller platform storing sensitive payment details itself.

- Sellers do not get full card details. That limits exposure on the marketplace side.

Practical rule: If your question is “will my credit card be exposed during a normal Gumroad purchase,” Gumroad’s technical setup is reassuring.

This is the part many reviews get right. Gumroad’s payment and transport security are not the weak point. If a buyer is using the site typically, the transaction itself is structured in a way that should feel familiar to anyone who has bought from a mainstream digital platform.

The harder questions start after the payment succeeds.

The Buyer's Risk in an Open Marketplace

A secure transaction is half the story.

Gumroad also operates as an open marketplace model with minimal seller vetting, and by 2026 it is described as serving over 100,000 creators globally. At the same time, refunds are handled at the creator’s discretion rather than through enforced platform policies, which means buyer outcomes can vary a lot from one seller to another (LitExtension’s review).

Payment safety is not seller safety

The easiest way to explain Gumroad is this. It’s closer to a digital farmer’s market than a tightly curated retail store.

That model has upside. It lowers barriers for independent creators. It also means buyers get access to niche products they might never find on larger storefronts.

The downside is obvious to anyone who has worked in marketplace risk. The platform can protect the payment rail while still leaving the buyer with inconsistent product quality, misleading descriptions, weak support, or a seller who disappears after the sale.

A buyer should not assume these three things are the same:

- A secure checkout

- A trustworthy seller

- A fair refund experience

They are separate.

If you buy from a known creator with an established audience, Gumroad can work smoothly. If you buy from a thin profile with vague copy and no track record, the transaction may still process safely, but that doesn’t make the offer safe in a broader sense.

For anyone evaluating these risks more broadly, this article on https://www.suby.fi/post/payment-fraud is useful because it separates technical payment fraud from the broader problem of trust and merchant behavior.

Where refunds get messy

Refund handling is where buyers feel the marketplace model most directly.

Because creators control refunds, the experience is inconsistent. One seller may solve an issue in a single reply. Another may argue, stall, or deny the request even when the product falls short of what the listing implied.

That doesn’t mean Gumroad is uniquely bad. It means Gumroad places more responsibility on the buyer to vet the seller before purchase.

Here’s the buyer-side checklist I’d use before paying:

| Check | Why it matters |

|---|---|

| Look for creator history | A seller with a visible track record is easier to trust |

| Read the product page carefully | Vague promises signal weak fulfillment |

| Check for outside presence | A website, social profile, or community adds accountability |

| Read refund language before purchase | You need to know whether the seller sounds clear or evasive |

Most payment problems on Gumroad are not “my card got stolen.” They’re “the product wasn’t what I expected” or “the seller won’t handle the refund the way I hoped.”

So, is gumroad safe for buyers? Technically, often so. Commercially, it depends far more on the seller than many buyers realize.

Is Gumroad Safe for Creators and Their Income?

The safety discussion becomes more serious here.

Many articles stop at buyer checkout security. That misses the part creators lose sleep over, which is whether the platform is dependable when revenue starts to matter.

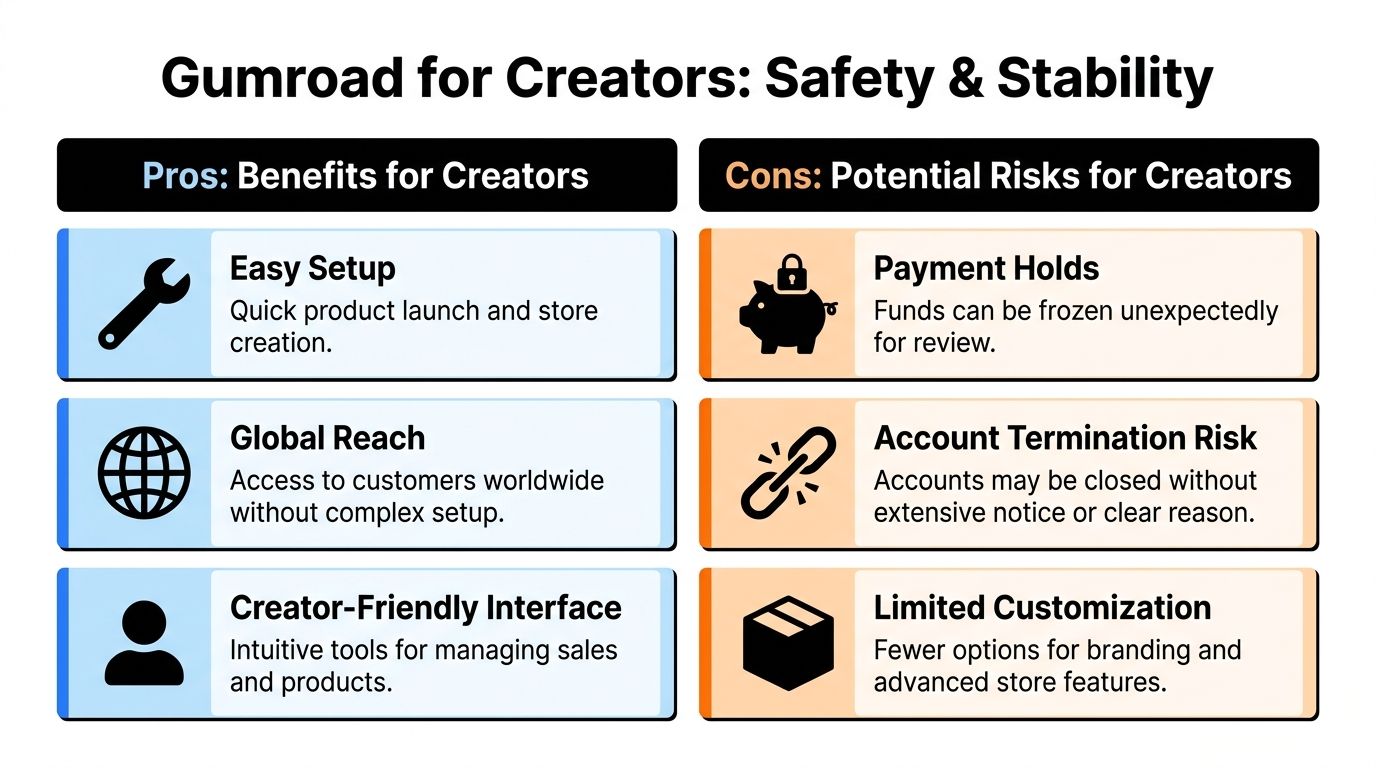

Operational Risk

A recurring concern in creator reviews from 2024 to 2026 is payout reliability and account suspension risk. One analysis notes reports of payment delays, unclear fee structures, and sudden account suspensions without warning, including creators describing 30-90 day holds or permanent bans tied to disputed policy issues (analysis here).

That doesn’t prove every creator will face these problems. It does show the risk is material enough that serious sellers shouldn’t dismiss it.

If your Gumroad store is a side channel, a hold is annoying. If it pays your rent, the same event becomes a business continuity problem.

The issue is not losing access to one payout cycle. It’s the compound effect:

- Cash flow gets interrupted

- Customer support piles up

- Launch plans slip

- Trust in the platform drops fast

What creators should take seriously

I advise creators to separate “easy to start” from “safe to depend on.”

Gumroad is easy to start. That’s a real advantage. But creator safety depends on whether you can predict revenue flow, understand enforcement decisions, and recover quickly if support is slow or opaque.

A simple risk view helps:

| Creator concern | Why it matters |

|---|---|

| Payout delays | Delayed access to funds can disrupt payroll, contractors, or personal income |

| Account reviews or suspensions | One platform decision can stop sales and payouts at the same time |

| Policy opacity | If the reason is unclear, fixing the issue gets harder |

| Single-platform dependence | Revenue concentration increases platform risk |

If one dashboard controls your checkout, customer access, and payouts, a single account problem can shut down the whole business.

That’s the practical distinction many “is gumroad safe” articles miss. Buyer safety is about transaction protection. Creator safety is about operational resilience.

For hobby sellers, Gumroad may be a reasonable tool. For businesses with subscriptions, launches, affiliates, contractor payments, or a team relying on revenue timing, the margin for disruption is smaller.

That’s where Gumroad starts to feel less like a lightweight storefront and more like a single point of failure.

Practical Tips to Stay Safe When Using Gumroad

Most Gumroad problems are manageable if you approach the platform with the right expectations.

For buyers

Use Gumroad the way you’d use any open marketplace. Trust signals matter.

- Check the seller before you buy. Look for a real online presence, prior product history, and signs that the seller exists beyond one sales page.

- Read the listing like a contract. If the description is vague, overly hyped, or avoids specifics about what’s included, assume support could be just as vague.

- Review refund terms first. Since refunds are frequently creator-led, you want to know the seller’s stance before payment, not after disappointment.

- Watch for scam patterns. If you want a broader primer on suspicious behavior across consumer platforms, this piece on spotting and avoiding fake profiles or scams on online platforms is useful because the same red flags show up in seller accounts too.

For creators

Treat Gumroad as a channel, not your entire safety net.

- Keep records of everything. Save customer communications, receipts, product files, policy notes, and dispute-related messages. If anything gets questioned, documentation helps.

- Reduce refund friction. Clear product descriptions, prompt replies, and visible delivery terms lower the chance that disappointed buyers escalate into disputes.

- Avoid overdependence. If Gumroad is your route to revenue, platform risk becomes business risk.

- Back up your audience access. Keep your customer list, community access logic, and delivery systems organized outside any one storefront when possible.

Diversification is not paranoia. It’s basic platform hygiene for creators whose income matters.

Many creators stay safe on Gumroad because they sell clean products, communicate well, and don’t rely on the platform for every operational function. Problems become far more painful when all sales, all customers, and all payouts run through one account.

A Modern Alternative for Global Creator Businesses

Once a creator moves beyond casual sales, the actual requirement changes. You’re no longer looking for the fastest way to upload a file. You’re looking for payment infrastructure that supports a business cleanly.

What serious sellers need

The needs are consistent:

- card acceptance for mainstream buyers

- recurring billing when subscriptions matter

- predictable settlement

- a way to plug payments into a site, app, community, or workflow you control

That’s why many growing sellers compare marketplaces with dedicated payment tools. If you’re evaluating that shift, this overview of https://www.suby.fi/post/best-platforms-for-selling-digital-products is a useful starting point because it frames the decision around control, not launch speed.

A more stable setup means separating the store experience from the payment layer so the business is not locked into a marketplace’s rules, support speed, and seller policy decisions.

Where a dedicated payment layer fits better

Suby is built for that use case. It provides an API that lets businesses accept payments by card or crypto, and it also offers native integrations with Discord and Telegram for subscriptions, paid access, and online communities. Its primary commercial model is simple: users pay with cards, businesses receive USDC.

That matters for international businesses because settlement predictability becomes part of platform safety. If your customers can pay in a familiar way and your business receives USDC directly, you avoid much of the uncertainty that comes from waiting on traditional payout cycles.

This is especially relevant for internet-native businesses that don’t want their revenue flow tied to one marketplace account.

A short product walkthrough helps show how that model works in practice:

Suby also supports one-time payments and recurring subscriptions, along with paylinks, embedded checkout, API integration, and webhooks. Customers can pay using Visa or Mastercard, as well as supported crypto assets, while merchants receive revenue in USDC.

That’s a different category from Gumroad. It’s not an open creator marketplace. It’s a payment layer for businesses that want more control over checkout, access, subscriptions, and settlement.

If I’m advising a creator testing a first product, Gumroad can be a quick option. If I’m advising a serious online business that needs reliability across borders, I’d favor infrastructure that reduces payout uncertainty and platform dependency from day one.

Your Platform Is Your Foundation Choose Wisely

So, is gumroad safe?

For payment and card security, yes, Gumroad presents a credible technical setup. Buyers are not taking unusual risk by entering payment details into a standard Gumroad checkout.

For marketplace trust, the answer is mixed. The platform’s open structure means buyers still need to judge sellers carefully, and refund consistency depends heavily on the creator.

For creator business safety, the answer becomes tougher. Reports of payout delays, opaque enforcement, and sudden account issues point to a risk that serious businesses should not ignore. A platform can be secure in the narrow technical sense and still be unstable as the foundation of your income.

That’s the primary takeaway. Gumroad is safe enough to start with. It is not consistently safe enough to depend on.

If your business is growing, your standard should change. You need more than a simple storefront. You need predictable settlement, fewer platform dependencies, and payment infrastructure you control.

A lot of platform decisions look small at the beginning. They seldom stay small once revenue, customers, and operations are tied to them.

If you want a more stable setup than a marketplace, take a look at Suby. Suby gives businesses an API to accept payments by card or crypto, plus native Discord and Telegram integrations for subscriptions, paid access, and online communities. Customers pay with cards, and businesses receive USDC.