Gaspard LEZIN

Global Payments Merchant Portal: A 2026 Guide

Discover what a global payments merchant portal is, its key features, and how modern platforms offer card/crypto payments with instant USDC settlement.

Your first customer in another country feels like proof that the internet works the way we hoped it would. You launch a product in one market, then someone three time zones away buys it while you sleep. Then the operational questions start. Why did one card go through and another fail? Why does the settlement amount look different from the checkout amount? When will the money arrive? Why does your finance lead have to piece together payouts, fees, and currency conversions from multiple dashboards?

That tension is where most founders first run into the limits of old payment infrastructure. Selling globally is easy to imagine and harder to operate. The checkout might look clean to the buyer, but behind it you can still have regional banking delays, currency conversion friction, dispute workflows, and settlement timing you can't predict.

A global payments merchant portal is supposed to be the control center for all of this. In the traditional model, it gives you a place to inspect transactions, review statements, and manage payment operations. In the modern model, it needs to do more. It should help you accept payments globally, understand what happened in real time, and receive revenue in a way that doesn't create more accounting and cash flow problems than it solves.

If you're already dealing with cross-border payment friction, this overview of cross-border payment challenges is a useful companion to the questions founders usually ask once international sales start picking up.

Table of Contents

Introduction The Challenge of Selling Globally

The traditional definition

How the concept has changed

Payment acceptance is only the starting point

The dashboard should answer business questions, not just log events

Settlement visibility shapes how usable your revenue is

Security, disputes, and developer controls need to live in the same system

Why legacy portals create operational drag

Payment Portal Models Compared

SaaS subscriptions across borders

E-commerce checkout without regional patchwork

Paid communities on Discord and Telegram

Freelancers and agencies collecting international revenue

Questions to ask before you commit

A practical selection lens

Introduction The Challenge of Selling Globally

A founder in Berlin sells software to a customer in Canada. Another founder in São Paulo runs a paid community with members spread across Europe and Southeast Asia. A freelancer in Nairobi invoices clients in the US and the UK. They all have the same problem in different forms. The sale happens online, but the money still moves through systems built around banking borders.

The pain usually shows up in small moments first. A support ticket asks why a payment failed. Finance asks how to reconcile the customer-facing currency with the settled currency. Someone on the team wants to know when this week's revenue will land, and nobody can answer with confidence.

That's where the idea of a global payments merchant portal becomes useful. At its simplest, it's the place where a business manages transaction data, customer payments, disputes, and settlement reporting. In practice, it often becomes the main operating console for international commerce.

A merchant portal isn't just a dashboard. It's the place where revenue becomes understandable, traceable, and actionable.

For internet businesses, that distinction matters. If your company is selling in multiple countries, you don't just need a way to accept money. You need a system that shows what happened, why it happened, and what happens next. That includes checkout performance, subscription events, payout visibility, and how all of that maps back to your customer records and internal reporting.

Older portals were built mainly to expose payment data after the fact. Modern teams need something closer to live infrastructure. They need a portal that helps them sell globally without creating avoidable operational complexity.

What Is a Global Payments Merchant Portal

Traditionally, a global payments merchant portal is a web interface offered by a payment processor or acquiring platform. A merchant logs in to review transactions, search for specific payments, download reports, inspect chargebacks, and sometimes manage users or account settings. It sits on top of the processor's underlying systems and gives the business a window into payment activity.

That model still matters, because many companies operate on top of large incumbents. To understand the scale of traditional portals, consider Global Payments. Its merchant portal supports over 3.5 million merchants worldwide, processes more than 50 billion transactions annually, operates in more than 100 countries, and that scale was reinforced by its 2019 merger with TSYS according to Global Payments company background.

For many businesses, that kind of portal is the first place they go after a payment issue appears. They search for a transaction ID, check whether a payment settled, download a statement for accounting, or review a dispute case. That's useful, but it's also reactive. The portal tells you what has already moved through the system.

The traditional definition

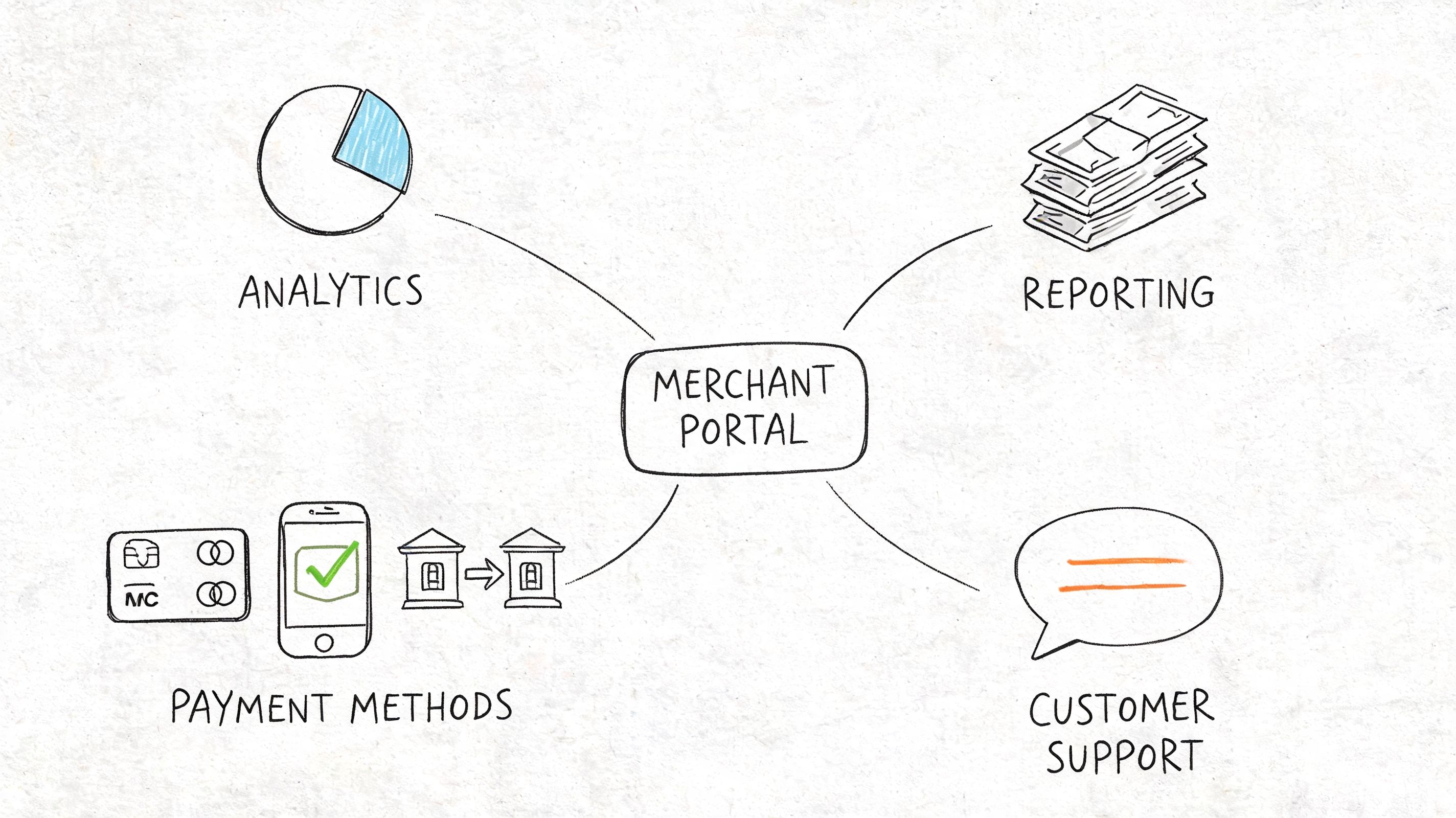

In the legacy model, the portal usually focuses on a few core jobs:

Transaction lookup, so support and finance teams can verify whether a payment succeeded, failed, or was refunded

Reporting access, including statements, exports, and summaries for accounting workflows

Dispute handling, where merchants review chargebacks and submit evidence

Basic account administration, such as user permissions or location-level reporting

This is why founders often underestimate the topic at first. They assume a merchant portal is just a back-office screen. But once the company starts selling across borders, the portal turns into a daily operational tool.

How the concept has changed

A modern portal needs to do more than expose raw transaction records. It has to connect payment acceptance, customer events, and settlement outcomes in one place. If you run subscriptions, the portal should show renewal attempts, failed charges, churn signals, and payout timing. If you sell to multiple regions, it should help you understand what your customers paid with and what your business received.

That changes the role of the portal from passive reporting layer to active commerce layer.

Practical rule: If your portal only helps after the payment, it isn't solving enough of the business problem.

This is also where modern internet-native payment systems diverge from traditional bank-centered setups. Instead of forcing merchants to manage card acceptance in one system, subscriptions in another, and settlement visibility somewhere else, modern tools try to unify those flows. The result is a portal that acts less like an archive and more like an operating system for revenue.

For a non-technical founder, the simplest way to think about it is this. The old portal tells you what the bank rails did. The modern portal helps you run commerce across cards, digital assets, subscriptions, and global settlement with fewer moving parts.

Core Features of a Modern Merchant Portal

A modern merchant portal should help a founder answer one practical question fast. Can I see what was paid, what settled, and what my business can use today?

That sounds simple. It rarely is.

Selling globally means one customer may pay with a card, another with crypto, and a third through a recurring subscription. Meanwhile, your team still needs one clear view of orders, payment status, refunds, disputes, and payouts. The portal works like an operations console. It connects customer actions at checkout to the money your finance team is waiting for.

Payment acceptance is only the starting point

Accepting a payment is the first event, not the finished job. A useful portal supports more than one way to collect money, but it also keeps the merchant side predictable after the customer clicks pay.

For many internet businesses, that means a simple structure. Customers pay with the method they trust. The merchant settles in USDC.

That separation matters. Checkout preference belongs to the buyer. Cash flow belongs to the business. If you can let customers pay in familiar ways while receiving a stable digital dollar asset, you reduce two common sources of pain at once: payout delays and FX noise.

The tools that support that model usually include:

Shareable paylinks for invoices, one-off services, and sales handled in chat or email

Embedded checkout for product-led flows inside apps, websites, and hosted purchase pages

Recurring billing support for subscriptions, retainers, and membership products

Multiple payment methods so revenue is not limited by a single rail or region

A founder should read this feature set as a conversion and cash flow question, not a dashboard checklist. More payment options can help close sales. Stable settlement can make revenue easier to forecast.

The dashboard should answer business questions, not just log events

Many portals show a lot of data and still leave teams guessing. A good portal helps support, finance, and product teams find the exact payment event they need without asking another system for context.

Speed matters here. A support lead trying to explain a failed renewal needs the subscription history, payment attempt, and current status in one place. Finance needs a clean export for reconciliation. Product needs to see whether failures are isolated or part of a broader pattern.

A useful dashboard should make these questions easy to answer:

What changed today

Which subscriptions renewed, failed, or are at risk

Which payments are pending, settled, refunded, or disputed

Which customer record matches each payment event

Which payouts are complete and which are still in flight

Fast search helps, but clarity matters more. If a founder has to cross-reference three tools to understand one customer payment, the portal is still doing reporting instead of operations.

The best merchant portals shorten the distance between a customer event and a business decision.

Settlement visibility shapes how usable your revenue is

This is the feature many teams notice late. They focus on getting checkout live, then discover that settlement rules decide how fast money becomes usable.

A modern portal should show payout status clearly, with enough detail that finance and operations can trust it. That means seeing what has settled, what is still pending, and what amount will arrive after conversion or fees. In legacy setups, those answers are often spread across processors, banks, and local payout providers.

Internet-native payment systems improve this by changing the settlement layer itself. If a customer pays by card or crypto and the business receives USDC, the portal can give a more consistent view of funds across regions. That reduces reliance on local bank timing, forced currency conversion, and fragmented payout paths.

Suby is one example of this modern model. It supports card and crypto payment acceptance, paylinks, embedded checkout, subscriptions, webhooks, and native integrations with Discord and Telegram, while settling merchant revenue in USDC.

Security, disputes, and developer controls need to live in the same system

Payments grow more complex as volume grows. More customers means more edge cases, more failed payments, more refund requests, and more dispute risk. The portal should help the business handle those cases without creating a separate workflow for each one.

That usually includes:

Authentication and compliance controls to reduce fraud and account risk

Dispute visibility so teams can react quickly when chargebacks or payment claims appear

APIs and webhooks so engineers can sync payment events into product logic, analytics, and internal systems

Exportable data for finance reviews, audits, and reconciliation outside the portal

Some companies start with no-code tools like paylinks and hosted checkout. Others push payment events into a larger product stack with APIs. A modern merchant portal should support both approaches, because the primary goal is operational clarity. The business needs one system that helps it collect revenue, understand settlement, and act on exceptions before they turn into cash flow problems.

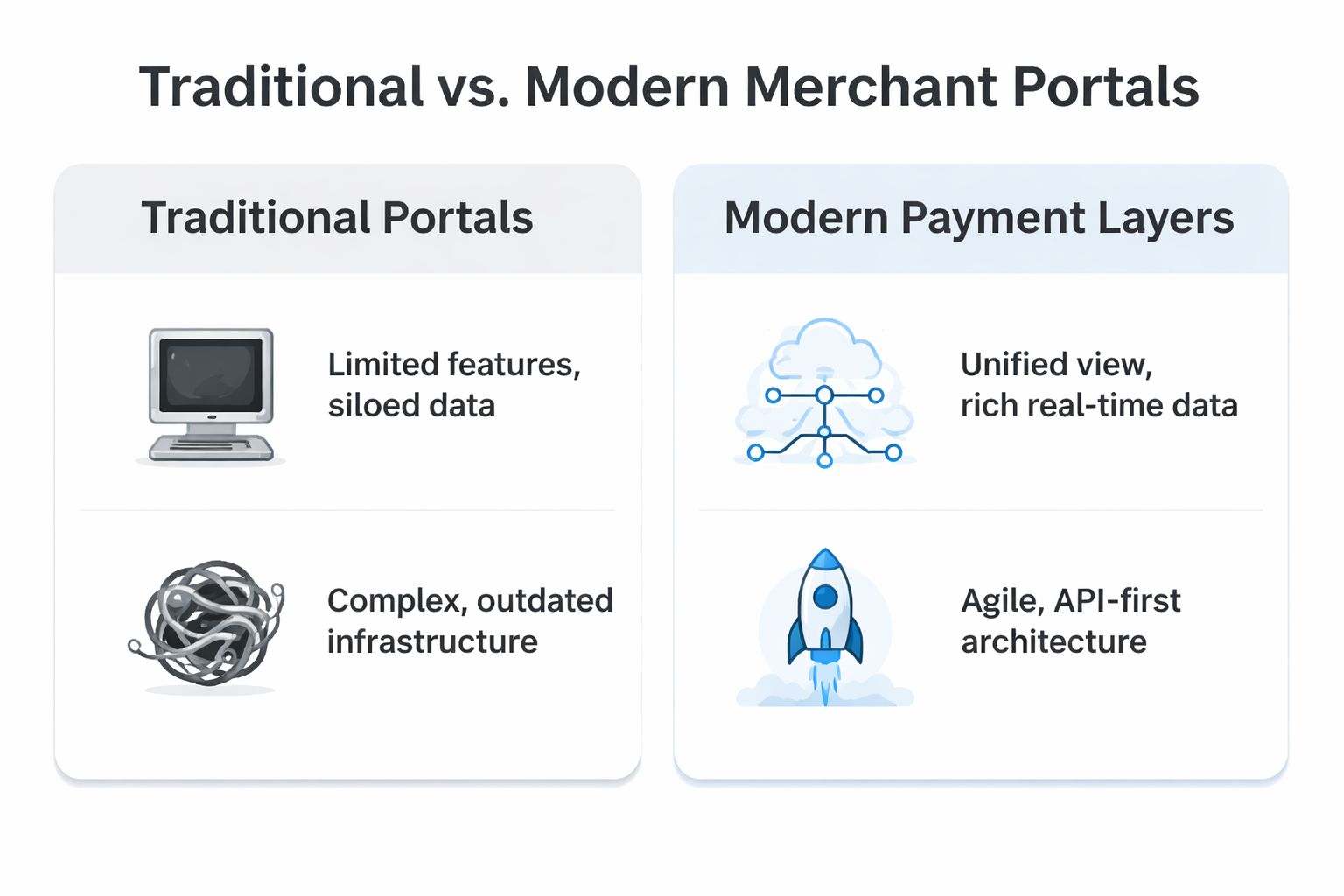

Traditional Portals vs Modern Payment Layers

Traditional merchant portals are often perfectly competent at reporting. The problem is deeper than reporting. The underlying rails still shape payout speed, reconciliation effort, and whether your finance team can forecast cash movement with confidence.

Why legacy portals create operational drag

One recurring gap in traditional systems is multi-currency reconciliation. Documentation may explain how to export payment data, but not how to track FX conversion cleanly or map cross-border transactions into accounting tools when customers pay in many currencies. Another common gap is settlement predictability. Merchants often can't see clearly when funds will arrive because holds and reserve logic aren't transparent, as noted in Global Merchant Portal help resources.

That creates friction in very ordinary workflows. A founder wants to know whether to hire next month. Finance wants to close books. Support wants to explain a payout delay. The portal shows transactions, but not always the answer to the business question behind them.

The real divide isn't old dashboard versus new dashboard. It's old settlement rails versus modern settlement rails.

A modern payment layer approaches the same problem differently. It doesn't just visualize activity from bank-led infrastructure. It changes where settlement happens and how merchants receive funds. For businesses selling globally, that can mean fewer forced conversions, fewer payout unknowns, and a cleaner path from sale to usable revenue.

Payment Portal Models Compared

Feature | Traditional Merchant Portal | Modern Payment Layer (e.g., Suby) |

|---|---|---|

Primary role | Reporting and account management after transactions occur | Payment acceptance, revenue operations, and settlement in one layer |

Settlement method | Usually bank-based payout rails | Can settle merchant revenue in USDC |

Payout visibility | Often limited, especially around holds and release timing | Designed for more direct, predictable settlement flows |

Currency handling | Often creates reconciliation work when customer currency and settlement currency differ | Reduces FX handling complexity when merchants standardize on USDC settlement |

Global operations | Coverage may exist, but workflows still reflect regional banking constraints | Better suited to internet-native businesses operating across borders from day one |

Integration style | Portal first, APIs second | API, webhooks, checkout, and paylinks as core building blocks |

Typical pain point | Data is available, but money movement is still hard to forecast | Simpler revenue flow, but requires merchants to be comfortable with wallet-based settlement |

This comparison isn't about declaring one model obsolete for every business. A domestic retailer with local bank operations may be fine with a classic processor portal. But for SaaS companies, creators, agencies, and cross-border e-commerce teams, the settlement layer often determines whether growth feels manageable or chaotic.

Common Workflows and Integration Patterns

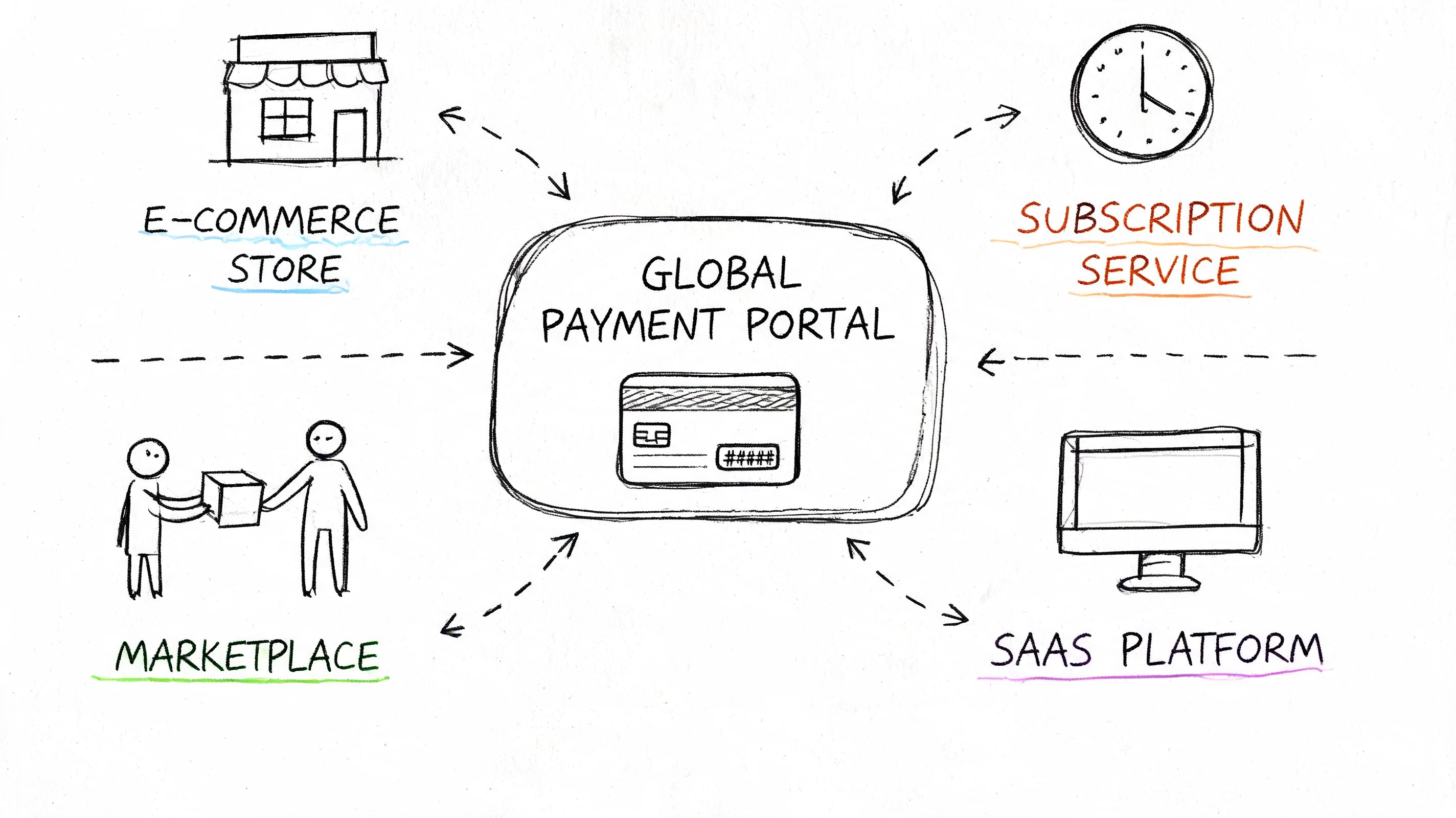

The easiest way to understand a modern global payments merchant portal is to look at how different businesses use one. The workflow changes depending on what you sell, who you sell to, and how much control you want over the payment experience.

SaaS subscriptions across borders

A SaaS company usually wants payments to feel invisible. A user signs up, enters payment details, and the billing system handles renewals, failed payments, and access changes without manual work.

In a traditional setup, platform onboarding can require structured API boarding with validated merchant details, including business and bank data, and even low-risk profiles may still take 24 to 48 hours according to Global Payments embedded boarding guidance. That model reflects legacy payment architecture. It works, but it adds process.

A more modern SaaS flow usually looks like this:

The product triggers checkout when a user selects a plan.

Payment events flow back by webhook so the app can activate, pause, or cancel service automatically.

Subscription status appears in the portal alongside payment history and payout visibility.

Revenue settles in USDC, which removes a lot of the friction of dealing with multiple banking corridors.

If you're evaluating API-first options for this kind of flow, this guide to global payment APIs is useful for thinking through implementation tradeoffs.

E-commerce checkout without regional patchwork

An e-commerce merchant has a different problem. The catalog may be simple, but buyer behavior is messy. One customer wants to use a card. Another prefers a digital asset. Someone abandons because the checkout feels unfamiliar. Someone else completes the purchase, but the merchant later has to reconcile what was charged versus what was received.

For that business, an embedded checkout and a single portal matter more than a sprawling stack of plugins. The merchant needs one place to see order-linked payments, refund history, and settlement outcomes. If they sell digital goods globally, the same portal should also help support answer questions fast when a customer says, "I paid, but I can't access what I bought."

Paid communities on Discord and Telegram

Creators and community operators often have the least patience for banking-heavy tooling. They don't want a finance workflow. They want paid access to work.

Native integrations allow a creator to sell recurring or one-time access, connect payment to membership logic, and have the system grant or remove access automatically inside Discord or Telegram. The merchant portal becomes less about statements and more about member lifecycle control, and on Telegram specifically a portal funnel that moves people from a public channel to a paid group can do most of that conversion work in seconds.

For paid communities, the real product isn't the payment itself. It's reliable access control tied to successful payment events.

That sounds narrow, but it's a major reduction in manual work. Instead of checking screenshots, chasing failed renewals by hand, or updating member status manually, the payment system and the community system stay in sync.

Freelancers and agencies collecting international revenue

Freelancers and agencies need less infrastructure, but they care a lot about timing. They don't want to send an invoice and then wonder how long the transfer will take, what fees will be deducted, or whether the client will hit a banking issue on the way.

A paylink-based workflow fits this use case well:

Create a payment request tied to a service, milestone, or retainer

Send a single link instead of collecting bank details across regions

Let the client pay by familiar method

Receive revenue in USDC, which can simplify cross-border collection if the business already operates on wallet-based settlement

This is one of the clearest examples of why the portal matters. The freelancer doesn't need a finance department, but they still need records, payment status, refunds, and proof of payment in one place. The portal becomes the operating layer for a very lean business.

How to Choose Your Global Payment Solution

A founder lands their first wave of overseas customers and revenue starts coming in from three or four countries at once. Sales look healthy, but finance gets messy fast. One provider shows successful payments, the bank balance updates later, fees appear in different places, and support has to answer basic payout questions by asking engineering. That is the moment a payment tool stops being a checkout decision and becomes an operating decision.

The right global payments merchant portal should make money movement easy to follow from customer payment to usable funds. For internet-native businesses, that often matters more than adding one more payment button. If your business sells across borders, you are choosing how long settlement takes, how much FX friction you absorb, and how much manual work your team carries every month.

Questions to ask before you commit

Start with the path of funds. A simple test helps. Ask what the customer pays with, what your business receives, and how clearly your team can see the handoff between those two moments.

Then pressure-test the system with practical questions:

How do payouts arrive, and on what timeline

Does your business settle to a bank account, in USDC, or through both options

Can support review payment status and history without relying on engineers

Can finance export records that match reconciliation needs

Can the system handle your real mix of payments, such as subscriptions, one-time charges, or gated access

Are APIs and webhooks available if payments need to trigger product actions

If you are comparing checkout and gateway providers more broadly, Grumspot's guide to payment gateways is a useful market-level reference because it frames the choice around business operations, not just feature grids.

A practical selection lens

Legacy merchant portals were built around bank-centered workflows. They are often good at recording transactions after the fact, but weaker at giving fast, flexible settlement across borders. Modern internet businesses usually need something else. They need a payment layer that supports familiar customer payment methods while reducing payout delays, regional banking friction, and conversion loss from foreign exchange.

That is why stablecoin settlement matters in this category. If customers can pay in common methods, but the business settles in USDC, the portal starts to work more like a clear ledger and less like a chain of banking handoffs. The benefit is not novelty. The benefit is shorter distance between a successful sale and funds your business can use with confidence.

If you want a wider comparison of providers built for cross-border selling, this overview of the best international payment gateway options is a helpful shortlist to review alongside each vendor's payout model and integration approach.

Suby is a payment gateway and Merchant of Record. Your customers pay with card, bank transfer, Apple Pay, Google Pay, Klarna, and more, or stablecoins, and you get paid out to your bank account, or directly in stablecoins (USDC, EURC) to your wallet, anywhere in the world, no bank account required. With API and webhook workflows plus native Discord and Telegram integrations, the merchant portal becomes a clear ledger from customer payment to usable funds, which is exactly what makes cash flow predictable and international sales easier to run.