You start selling online, things go well, and then international growth turns messy.

A customer in France says their card failed for no obvious reason. A client in Asia pays an invoice, but the amount that finally arrives is lower than expected after currency conversion and intermediary fees. Your team checks the dashboard, then the bank account, then support tickets, and still can't answer a simple question: where is the money, and when can we use it?

That confusion is why cross border payment gateways matter. They sit in the middle of international transactions and make very different financial systems work together. For a business, that means fewer failed payments, clearer routing, and a more predictable path from checkout to usable funds.

This isn't a niche issue. Global cross-border payments reached $190 trillion in 2023 and are projected to surge to $290 trillion by 2030, according to cross-border payment statistics compiled by Electro IQ. If you sell software, subscriptions, services, digital access, or physical products across countries, you're already operating inside that system whether you planned for it or not.

The hard part is that most businesses first encounter global payments as a symptom. Declines. Delays. FX surprises. Chargebacks that are harder to understand than domestic ones. A cross border payment gateway is the infrastructure layer built to reduce that friction.

Table of Contents

- Think of it as a financial diplomat

- The key players in one transaction

- What the gateway does

- Domestic versus cross-border

- Authorization is the first checkpoint

- Capture and settlement are where delays appear

- Why modern routing changes the experience

- A simple example

- FX spreads are often the least visible cost

- Delayed payouts affect cash flow faster than many teams expect

- Compliance and fraud checks multiply across borders

- Chargebacks get harder when multiple jurisdictions are involved

- Start with what lands on your side

- Evaluate cost as a payment path, not a headline fee

- Gateway Evaluation. Traditional vs Stablecoin-Native

- Paylinks for simple sales and invoices

- Embedded checkout for a smoother buying flow

- Direct API and webhooks for custom products

- The model is simple for the buyer and cleaner for the business

- How the product fits real internet businesses

- What's the difference between a gateway and a processor

- Can a cross border payment gateway also handle domestic payments

- What should I ask my accountant if I receive USDC

Introduction Selling Globally Is Harder Than It Looks

A lot of founders assume global payments are just local payments with more currencies. They aren't.

When you sell within one country, most of the system shares the same rules. The customer knows the payment methods. The bank knows the merchant profile. The risk signals are familiar. Settlement follows a pattern your finance team can learn quickly.

Cross-border sales break that simplicity. The buyer may pay with a card issued in one country, through a card network operating globally, to a merchant entity in another country, with settlement handled through a different chain than the authorization path. That's why a checkout can look successful to the customer and still create a headache for the business later.

A familiar growth problem

Take a small SaaS company selling subscriptions worldwide.

At first, international demand looks great. Customers sign up from new regions, traffic grows, and the company feels like it has reached product-market fit beyond its home country. Then the payment issues start surfacing:

- Customers complain about declines: The product works, but some foreign-issued cards don't go through consistently.

- Finance sees margin erosion: Revenue arrives after deductions that weren't obvious at checkout.

- Operations lose time: Support ends up answering payment and payout questions instead of helping users succeed.

None of this means the product is weak. It usually means the payment stack was built for domestic selling, then stretched into international use.

Practical rule: If selling globally feels operationally heavier than selling locally, the problem often sits in the payment infrastructure, not in demand.

The gateway is the bridge

A cross border payment gateway is the layer that helps these transactions move between countries, systems, banks, and compliance environments.

Think of it less like a checkout widget and more like a bridge operator. It has to validate payment details, connect the right institutions, handle international routing, manage risk signals, and support the movement from customer payment to merchant settlement.

For online businesses, this matters most when cash flow gets less predictable than sales. You can close deals and still struggle to understand your revenue timing, costs, and settlement path. That's usually the moment businesses stop asking, "How do we accept international payments?" and start asking the better question: "How do we accept them without creating new problems?"

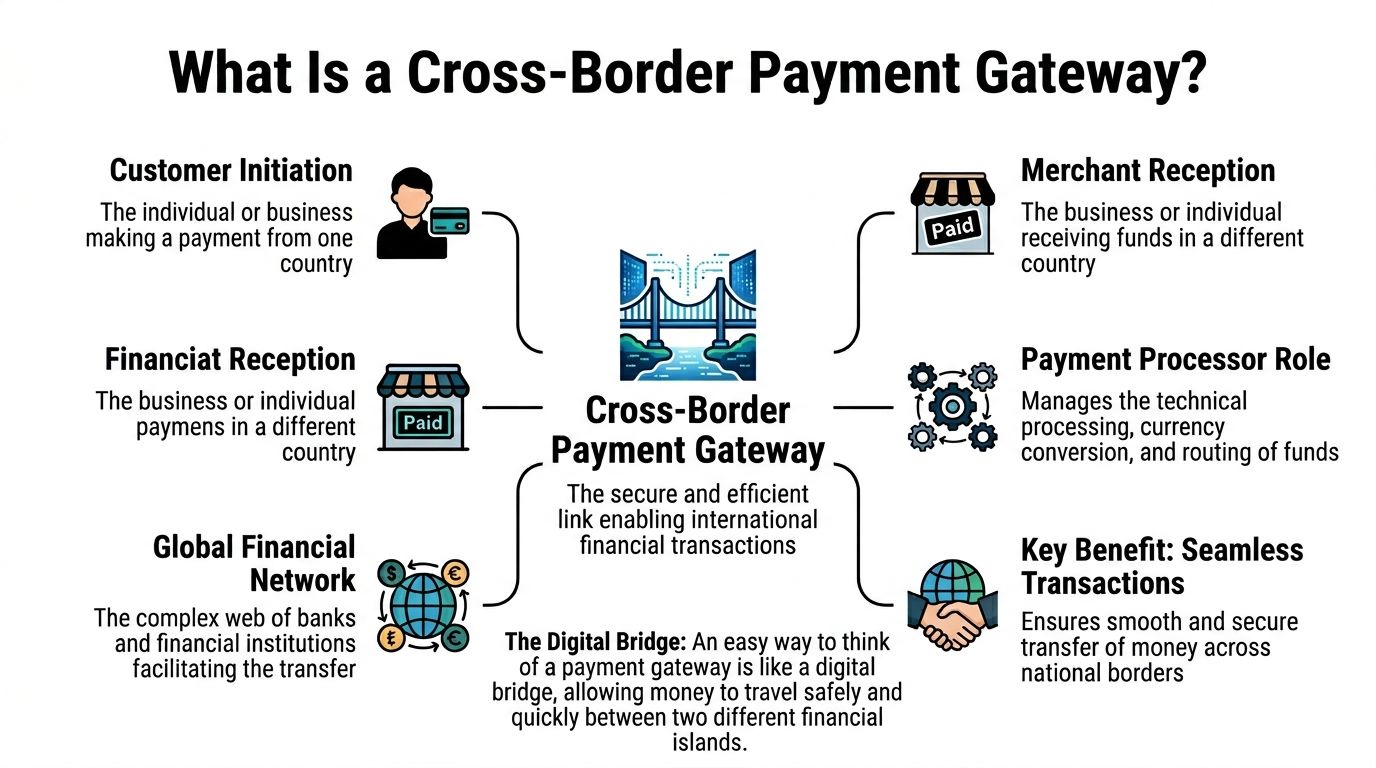

What Is a Cross Border Payment Gateway

A cross border payment gateway is the system that helps a payment move from a buyer in one country to a business in another country.

That sounds simple. In practice, it's coordinating several institutions that don't share the same rails, the same rules, or even the same assumptions about risk. A domestic gateway mostly passes data within one familiar environment. A cross border gateway has to translate between different ones.

Think of it as a financial diplomat

A useful analogy is a financial diplomat.

If two people speak different languages, a diplomat doesn't just translate words. They also interpret rules, expectations, and context so both sides can complete the exchange without confusion. A cross border payment gateway does something similar for money.

It helps different systems agree on questions like:

- Is this buyer legitimate

- Is this card valid

- Which currency is being charged

- Which institution will receive and settle the funds

- Which compliance checks apply in this corridor

That's what makes it different from a basic domestic payment setup.

The key players in one transaction

Most readers get lost because payment articles talk about "the bank" as if there were only one. There usually isn't.

Here's the simpler map:

- Customer: The person or business making the payment.

- Merchant: The company selling the product, service, subscription, or access.

- Issuing bank: The bank or card issuer behind the customer's payment method.

- Acquiring side: The financial institution or processor handling acceptance for the merchant.

- Card networks: Visa and Mastercard connect the parties and pass transaction messages.

- Gateway: The coordination layer that securely sends payment data, triggers checks, and helps route the transaction.

What the gateway does

A cross border payment gateway usually handles a mix of technical, financial, and compliance tasks.

Some are visible to the merchant. Many aren't.

| Function | Why it matters |

|---|---|

| Secure payment data transfer | The customer can submit card details safely at checkout |

| Transaction routing | The payment gets sent through the most suitable path available |

| Currency handling | The business can charge in one currency and settle in another, if needed |

| Risk and fraud screening | Suspicious activity can be flagged before funds move |

| Status communication | The merchant gets updates on success, failure, or next actions |

A good mental model is this: the gateway doesn't create demand, but it decides how much friction demand turns into.

Domestic versus cross-border

A domestic gateway works inside one payment neighborhood. A cross border payment gateway works between neighborhoods that use different roads, different languages, and different checkpoints.

That's why international payment acceptance can't be judged only by whether the checkout page looks polished. A better test is whether the system can move money across borders with clear routing, manageable risk, and predictable settlement.

Unpacking the Mechanics of Global Payments

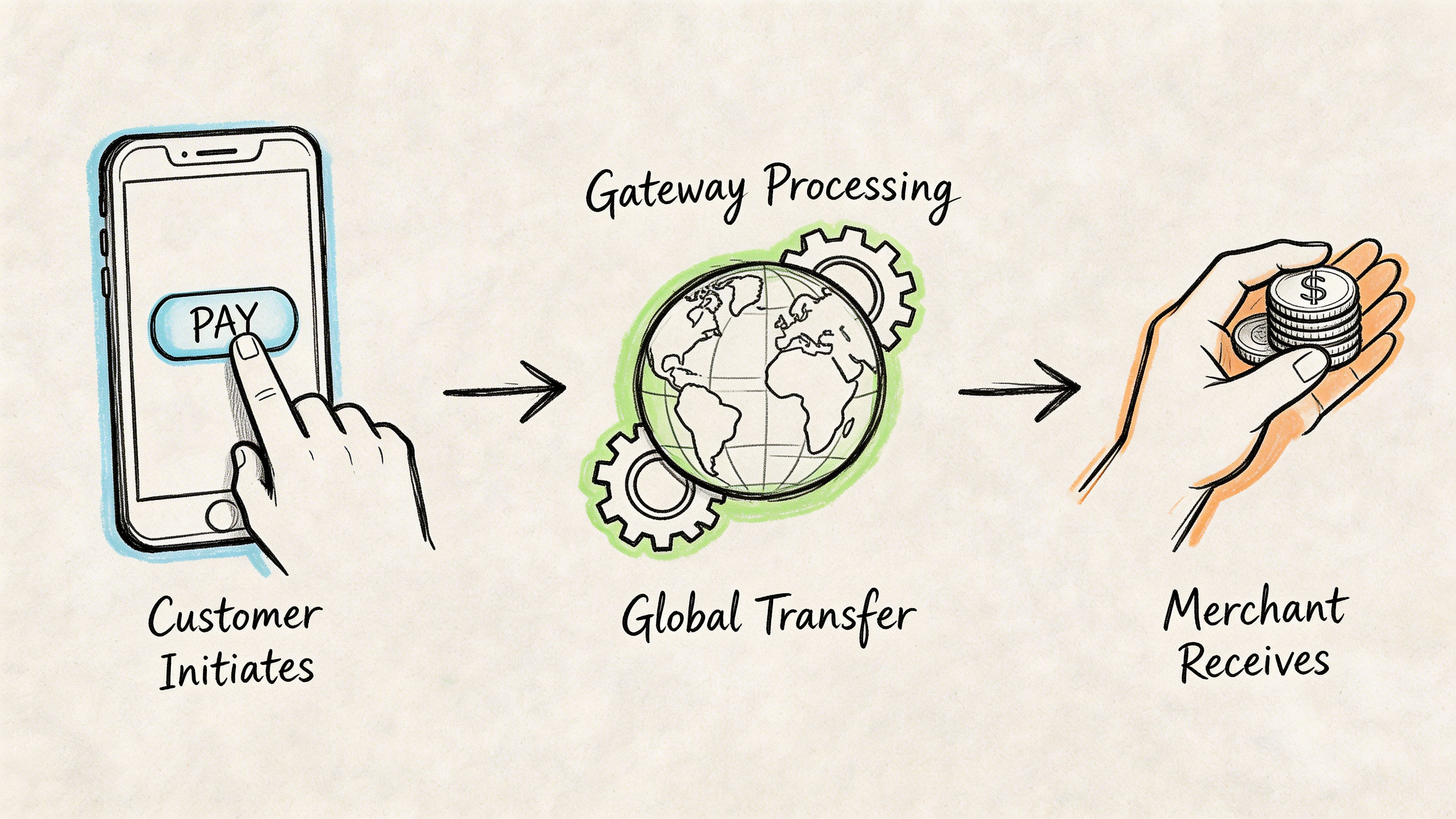

One international payment can involve more moving parts than many teams expect.

A customer clicks pay. The UI looks instant. Under the surface, several checks and messages begin moving between the merchant, the gateway, the acquiring side, the card network, and the issuer.

Authorization is the first checkpoint

Authorization is the first yes or no.

The customer submits payment details. The gateway securely passes that information onward. The issuer then checks whether the card is valid, whether the account can support the purchase, and whether the transaction matches its risk rules.

If that answer is yes, the payment is authorized. That doesn't mean the merchant has the money yet. It means the system has reserved the path for the transaction.

This is one place where businesses get confused. "Approved" at checkout isn't the same thing as funds being available for use.

Capture and settlement are where delays appear

After authorization, the merchant or platform captures the funds. That's the formal request to complete the payment.

Then comes settlement, which is where money moves to the merchant side. In domestic payments, this can feel relatively straightforward. In cross-border flows, it can slow down because the transaction may pass through multiple institutions, currencies, and review layers before final funds arrive.

That's why a business can see:

- A successful customer payment

- A delay before usable revenue appears

- A final amount that differs from the initial expectation because of FX or routing costs

Each handoff adds complexity. Each intermediary can add time, fees, or exceptions.

Why modern routing changes the experience

Legacy international payment systems often rely on long bank chains and fixed paths. Modern systems are more dynamic.

One way to understand this is through multi-rail orchestration. Instead of sending every transaction through one default route, the system can evaluate different rails and pick the path that best fits cost, speed, and operational constraints.

According to Lightspark's cross-border payments API guide, multi-rail orchestration architectures dynamically route transactions across fiat, crypto, and hybrid rails to optimize speed and cost, and historical benchmarks show crypto rails reducing costs by 40-70% in high-friction corridors.

That doesn't mean every business should use every rail. It means the architecture matters. If your gateway only knows one route, your business inherits the weaknesses of that route.

For a more foundational overview of gateway roles and transaction flow, this guide on payment gateway basics is useful background.

A short visual explanation can help here:

A simple example

Suppose a customer in one country pays by card for a subscription sold by a business operating globally.

The buyer experiences one checkout. The merchant may be dealing with several hidden questions at once:

- Will the issuer approve this cross-border card payment

- Will the payment be captured immediately or later

- What currency will the customer see

- What currency or asset will the business receive

- How long until those funds are usable

When teams say global payments feel unpredictable, this is what they mean. The customer sees one click. The business manages an entire chain.

The Hidden Costs and Hurdles of Selling Globally

A customer in France pays by card. Your store lists prices in euros. Your finance team reports in dollars. A few days later, the payout arrives late, the amount is lower than expected, and support is answering a refund question in a different time zone. That is what cross-border friction looks like in practice.

The hard part is not one dramatic failure. It is a chain of smaller problems that chip away at margin, forecasting, and team time.

FX spreads are often the least visible cost

Currency conversion works like a toll road with the price hidden until after the trip. The customer completes checkout, the payment is approved, and the merchant still may not know the exact effective conversion cost until settlement happens.

That creates a planning problem, not just a payment problem.

If you sell into several markets, even modest FX variation can make it harder to set prices, measure channel performance, and explain why expected revenue does not match received revenue. Teams often focus on the listed processing fee because it is easy to compare. The less obvious cost is the spread applied somewhere between customer payment and merchant settlement.

This is one reason more companies are comparing providers by payout model, not just checkout coverage. A guide to the best international payment gateways is useful if you want to compare how providers handle settlement currencies and cross-border costs.

A modern alternative changes the handoff point. Instead of accepting cards internationally and then passing the merchant through more bank conversions, some providers keep the familiar card checkout on the front end and settle the business directly in USDC on the back end. That can reduce FX uncertainty because the merchant receives a dollar-denominated digital asset rather than waiting for another conversion layer to finish.

A core difficulty with FX is uncertainty. If finance cannot predict the landed amount, pricing discipline gets weaker.

Delayed payouts affect cash flow faster than many teams expect

Three extra days can be manageable once. Repeated every week, it changes how the business operates.

Ad budgets get capped earlier. Refunds become harder to time. Teams keep larger cash buffers because they do not fully trust when funds will clear. For businesses with subscriptions, marketplaces, or frequent contractor payouts, settlement timing becomes an operating constraint.

Some platforms also apply rolling reserves, extra review periods, or corridor-specific payout rules. Those controls may be normal from a risk perspective, but they still make cash planning harder for the merchant.

The stablecoin-native model, for example, stands out in a practical way. The customer still pays with a card. The merchant receives USDC directly. That shortens the distance between a successful checkout and usable funds, especially compared with payout flows that wait on multiple banking intermediaries.

Compliance and fraud checks multiply across borders

Moving money across borders is part logistics, part trust system. Every party in the chain wants proof that the transaction is legitimate, allowed, and properly documented.

That means KYC, AML checks, sanctions screening, card network rules, tax treatment, local data requirements, and fraud controls can all show up around the same payment flow. A provider may carry some of that burden, but your operations team still feels the effect through onboarding delays, payment reviews, and reconciliation work.

J.P. Morgan's 2025 trends for financial institutions reports broad concern about fraud exposure and rising cybercrime costs. For merchants, the practical questions are simpler and more immediate:

- How often will good payments be declined

- How much manual review will the team need to handle

- Which compliance tasks sit with the gateway, and which stay with us

- How quickly can payment issues be investigated and resolved

If your team also needs to work through reporting and accounting treatment for incoming international funds, this resource on tax implications of cross border money transfer is a useful starting point.

Chargebacks get harder when multiple jurisdictions are involved

A domestic dispute is usually annoying but familiar. An international dispute adds more variables.

The issuer may be in one country, the customer in another, and the merchant entity somewhere else. Evidence standards can vary. Timelines can feel less predictable. Even if the sale was valid, the merchant may spend more time gathering documents, translating context, and explaining the transaction path.

That extra work matters because chargebacks are not only a revenue issue. They also pull time from support, finance, and risk teams.

What merchants usually underestimate

| Friction point | What it affects most |

|---|---|

| Opaque FX conversion | Margins and pricing confidence |

| Slow settlement | Cash flow and operational planning |

| Cross-border fraud screening | Approval rates and review workload |

| International chargebacks | Support time and revenue recovery |

The common problem is predictability. Global selling gets easier when the business can estimate what a payment will cost, when funds will arrive, and whether settlement will land in a form that is immediately useful. That is why the combination of familiar card acceptance and direct USDC settlement is getting more attention. It addresses problems that standard cross-border setups often leave unresolved.

How to Evaluate a Cross Border Payment Gateway

A buyer in Brazil pays with a card. Your checkout shows a successful transaction. Three days later, finance is still asking four practical questions. What amount will arrive, in which currency, after which deductions, and when can the team use it?

That is the right place to start.

A cross border payment gateway should be evaluated from the end of the payment flow, not the front. The checkout matters, but the merchant experience is defined by settlement. If the customer pays smoothly and the business still deals with delayed payouts, unclear FX, or extra conversion steps, the gateway solved only part of the job.

Start with what lands on your side

Global payments work like a relay race. Card acceptance is one handoff. Settlement is the finish line. Many teams spend too much time comparing the baton and too little time studying whether anyone crosses the line cleanly.

Ask the provider to explain the payout path in plain language:

- Settlement currency: Do you receive fiat, a mix of currencies, or direct settlement in USDC?

- Settlement timing: Are payouts tied to bank cutoffs and local banking hours, or designed to arrive on a more predictable schedule?

- Deductions: Can you see where fees are applied, or do costs appear in separate layers across processors, banks, and FX providers?

- Reconciliation: Will your finance team be able to match orders, fees, and payouts without manual detective work?

The stablecoin question matters more than many merchants expect. A familiar card checkout can still end with direct USDC settlement for the merchant. That model changes the back half of the transaction without asking customers to learn a new payment behavior. For businesses selling across borders, that can reduce the usual gap between "customer paid" and "funds are ready to use."

Evaluate cost as a payment path, not a headline fee

A listed processing rate is only one line item. The full cost encompasses the entire route the money takes.

For example, a provider might advertise competitive card acceptance fees but settle through multiple banking intermediaries, each adding conversion spread, transfer fees, or timing risk. Another provider may keep the front-end checkout familiar while simplifying settlement into a single, easier-to-model flow. On paper, the first option can look cheaper. In practice, the second may be easier to budget and operate.

A useful evaluation checklist includes:

- Price clarity: Can finance explain the fee model without making assumptions?

- Checkout fit: Does the gateway support the card networks and payment methods your buyers already use?

- Dispute handling: How are chargebacks, fraud checks, and customer authentication managed across borders?

- Integration range: Can the team start with hosted payments, then add embedded checkout, API calls, and webhooks as the business grows?

- Settlement design: Does the provider rely fully on legacy bank payout rails, or can it settle in a digital dollar such as USDC?

If your team is comparing providers side by side, this guide to the best international payment gateway options is a helpful companion.

Gateway Evaluation. Traditional vs Stablecoin-Native

| Feature | Traditional Gateway | Stablecoin-Native Gateway |

|---|---|---|

| Customer checkout | Familiar card experience | Familiar card experience can stay the same |

| Merchant settlement | Often depends on bank payout cycles and fiat conversion | Can settle directly in USDC |

| FX exposure | Merchant may absorb conversion costs and rate movement | Lower if settlement happens natively in USDC |

| Fee visibility | Total cost can be spread across processing, banking, and FX layers | Cost path is often easier to trace |

| Operations | More banking coordination and payout tracking | Fewer intermediaries can simplify treasury workflows |

| Build options | Varies by provider | Often supports paylinks, embedded checkout, and API-based setups |

One more filter helps. Ask whether the provider is built for your operating model, not just for payment acceptance in theory. A SaaS company with recurring billing, an agency sending invoices, and an ecommerce brand optimizing checkout speed will not evaluate integration in the same way. Teams refining the buying flow itself may also want the Ecommerce Web Development Guide as a practical reference.

The core question is simple. After the customer pays, does the gateway leave your team with fewer moving parts or just a different set of them?

Choose the option that makes settlement clearer, faster, and easier to reconcile. In cross-border commerce, that is where payment infrastructure starts to feel useful instead of expensive.

Common Integration Patterns for Online Businesses

Once a business chooses a gateway model, the next question is practical. How do you put it in front of customers?

The right answer depends less on company size and more on workflow. A freelancer, a SaaS team, and a creator selling community access don't need the same integration pattern.

Paylinks for simple sales and invoices

Paylinks are the lightest setup.

You create a payment link, send it by email, chat, invoice, or DM, and the buyer completes checkout on a hosted flow. This works well for agencies, consultants, freelancers, and small teams selling custom packages or one-off work.

Paylinks are useful when:

- You don't need a full checkout build

- Your sales happen through conversation

- You want to collect payment before delivery or onboarding

They're also a good first step for businesses testing new international markets without changing their site architecture.

Embedded checkout for a smoother buying flow

Embedded checkout fits businesses that want the payment experience to stay inside their own product, landing page, or store.

This pattern is common for SaaS signups, e-commerce flows, paid access pages, and digital product purchases. It gives the merchant more control over branding and usually creates a more cohesive customer experience than sending buyers to a separate page.

If your team is also improving the broader shopping flow, this Ecommerce Web Development Guide is a useful companion resource because payment conversion is often tied to site structure, not just processor choice.

Direct API and webhooks for custom products

API integration is for teams that need control.

A direct API lets your product create payment sessions, subscriptions, and checkout logic in a way that matches your app. Webhooks then notify your system when events happen, such as a payment succeeding, failing, renewing, or being disputed.

This pattern is strongest when you need:

- Custom subscription logic

- Automated provisioning after payment

- Internal reconciliation workflows

- Access control tied to payment status

For implementation details, this guide on implementing a payment gateway gives a practical overview.

Choose the simplest pattern that matches the job. Businesses often overbuild too early, then spend months maintaining payment logic that a hosted checkout or paylink could have handled.

A good gateway should let you start simple and add complexity only when your product needs it.

A Modern Solution The Suby Approach

A common cross-border payment problem looks like this. A customer in one country is ready to pay with a card, but the business on the other side still has to guess what will arrive, when it will arrive, and what will be lost to conversion and payout delays.

That gap exists because checkout and settlement solve different jobs. Checkout is the customer-facing moment. Settlement is the business-facing outcome. Many payment explanations treat those as one system, but for global sellers, they often feel like two separate problems.

One model that deserves more attention combines a standard card checkout with stablecoin settlement. The customer pays in a familiar way. The business receives USDC directly. That changes the part merchants usually struggle with most, which is what happens after the payment is approved.

According to J.P. Morgan's discussion of cross-border payment megatrends, stablecoin and crypto infrastructure are becoming part of the broader cross-border payments conversation. What often gets missed is the practical hybrid setup, where the front end still feels like a normal card payment while the back end settles in a digital dollar.

The model is simple for the buyer and cleaner for the business

Suby is one example of that approach.

The core flow is easy to follow. A customer pays by card or with supported crypto. The business receives USDC. You can picture it like keeping the storefront familiar while changing the settlement rail behind the counter. The buyer does not need to learn a new payment behavior just because the merchant wants a more predictable result.

For a business selling internationally, that design can remove several points of uncertainty at once:

- Clearer settlement outcome: The business receives USDC instead of waiting for a traditional cross-border bank payout to complete.

- Less FX guesswork: Revenue is easier to understand when settlement does not depend on a later bank conversion step.

- Fewer banking delays in the payout path: The merchant is less exposed to the timing and friction of conventional cross-border disbursement flows.

Suby also supports card and crypto acceptance through an API, which means the settlement model can fit into products that need more than a basic checkout page.

How the product fits real internet businesses

This model is most useful when you map it to the way a business sells.

A freelancer may need to send a payment request to a client in another country and get paid without waiting through a chain of banking intermediaries. A SaaS company may want subscription checkout that feels normal to the customer but settles in USDC for easier treasury handling. A platform team may need payment events to trigger account access, provisioning, or internal reconciliation automatically.

Suby supports those common entry points, including one-time payments and recurring subscriptions. It also includes native integrations with Discord and Telegram, which matters for internet-native businesses that sell access, memberships, or community subscriptions. In those cases, payment collection and access control sit close together, which reduces manual admin work.

A few practical use cases:

| Business type | Common need | Relevant pattern |

|---|---|

| Freelancer or agency | Send payment requests to clients globally | Paylinks |

| SaaS or web app | Collect recurring subscription payments | Embedded checkout or API |

| Creator or community manager | Charge for memberships or access | Checkout plus Discord or Telegram integration |

| Developer platform | Automate payment events and internal workflows | API and webhooks |

The value here is operational, not theoretical. Customers keep using a payment method they already trust. The business gets a settlement asset designed to be more predictable across borders.

That hybrid design is easy to miss if you only compare traditional gateways with crypto-only checkouts. Many businesses do not want to push customers into an unfamiliar payment flow. They want to keep card acceptance at the front, while improving settlement on the back end. For international SaaS companies, agencies, e-commerce brands, and online communities, that can be a practical alternative to adding more bank accounts, more conversion steps, and more payout uncertainty.

Frequently Asked Questions

What's the difference between a gateway and a processor

A gateway handles the secure transmission of payment details and helps coordinate the transaction flow. A processor handles the movement and processing logic with the financial institutions involved. In practice, many platforms combine both, which is why the terms often blur together.

Can a cross border payment gateway also handle domestic payments

Yes, many can. If the system is built well, it should support domestic and international transactions without forcing you to run separate payment stacks. The primary question isn't whether it can do both. It's whether it keeps costs, routing, and settlement predictable in both cases.

What should I ask my accountant if I receive USDC

Ask how your business should record settlement receipts, how gains or losses are treated if conversion happens later, and what documentation you should keep for tax reporting and reconciliation. The right treatment depends on your jurisdiction and entity structure, so this is one place where customized professional advice matters.

If your business sells internationally and you're tired of card acceptance on one side and payout uncertainty on the other, Suby is worth evaluating. It gives businesses a way to accept payments by card or crypto, while receiving settlement in USDC, and it also supports API-based integrations plus native Discord and Telegram flows for subscriptions, paid access, and online communities.