You are looking for the best merchant of record because your current setup is starting to hurt.

Maybe tax registrations are getting messy. Maybe chargebacks are eating support time. Maybe payouts arrive slower than your business can tolerate. Maybe you sell globally, but your payment stack still behaves like a local setup. If you are already dealing with subscription billing, international cards, VAT, or chargeback fraud, the decision stops being about a checkout page and starts being about operating model.

That is why this list focuses on practical trade-offs, not brochure language.

A merchant of record takes legal responsibility for the transaction. In practice, that means the provider handles payment processing, tax collection and remittance, fraud controls, compliance obligations, and chargeback workflows. The category is growing fast because more digital businesses want that burden off their plate. The global Merchant of Record Compliance market reached USD 8.2 billion in 2024 and is projected to reach about USD 25.3 billion by 2033 at a 13.7% CAGR. That tells you something important. MoR is no longer a niche workaround for edge-case cross-border sellers. It is infrastructure.

The harder part is picking the right model.

Some providers are strongest for SaaS. Some are better for digital products. Some lean enterprise. Some are simple to launch but become expensive or rigid later. And some are addressing the payout friction that older MoR models still leave unresolved.

Table of Contents

- Best for teams that need pricing control more than self-serve simplicity

- Questions to answer before you sign

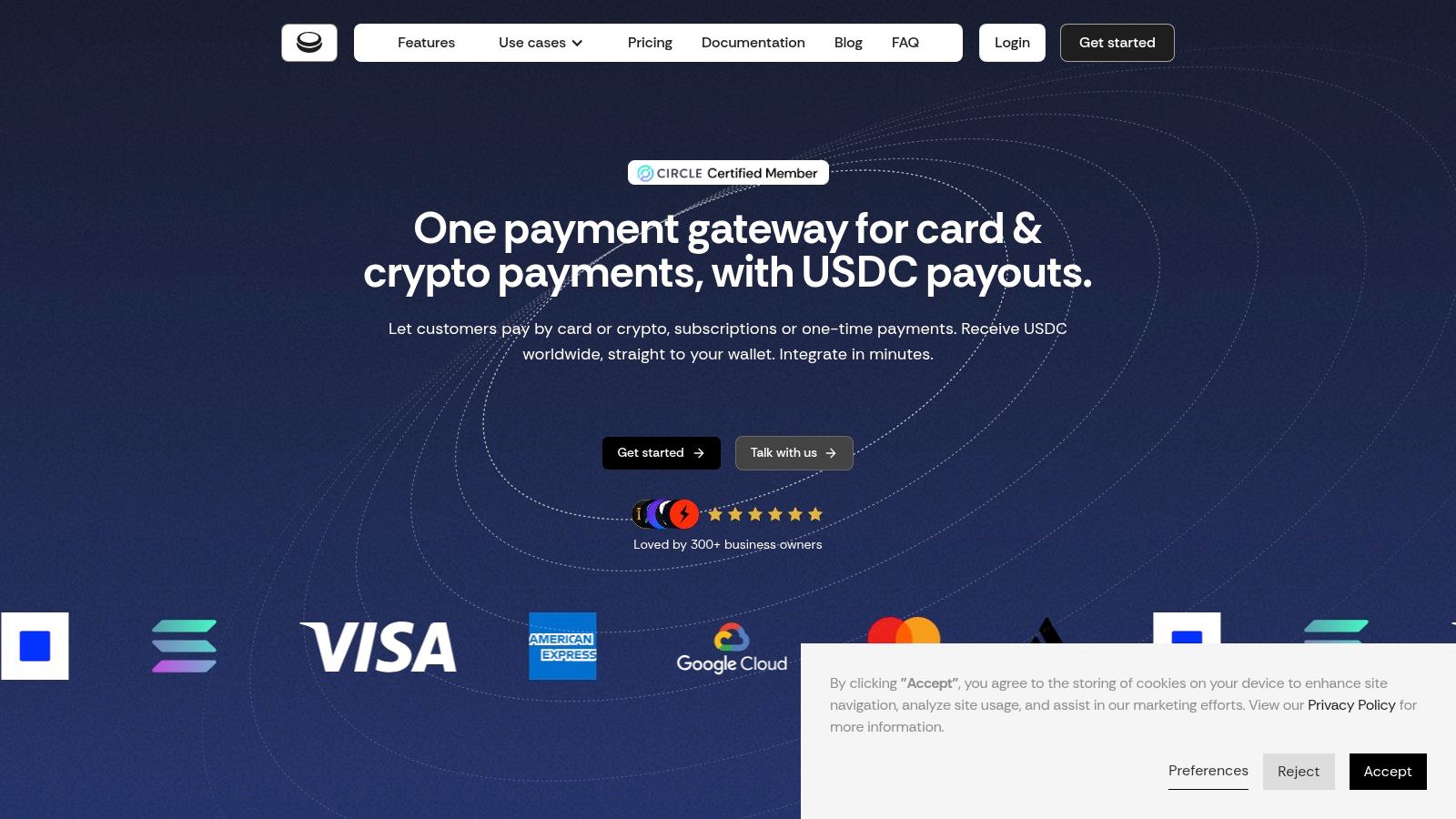

1. Suby

If payout friction is your main problem, Suby deserves the first look.

Most merchant of record reviews focus on tax and compliance. That matters, but operators feel the pain later, when settlement timing is unpredictable and cash flow planning gets fuzzy. That gap shows up often in market commentary around MoR selection, especially on payout speed and reliability. Suby takes a different route by letting customers pay with cards or crypto while businesses receive USDC.

Why Suby stands out

Suby is built for internet-native businesses, creators, and developers that want global payments without bank-led settlement friction. Customers can pay with Visa or Mastercard, and Suby also supports crypto payments including USDC, USDT, ETH, SOL, and BNB. The important operational point is simple. Users pay with cards, businesses receive USDC.

That changes the payout conversation.

Instead of waiting on traditional banking rails, merchants receive settlement in USDC to a wallet. For global businesses, that simplifies treasury handling, reduces FX headaches, and makes cross-border revenue more predictable. If you want a broader primer on the model, Suby explains the basics in its guide to the merchant of record model.

Suby also gives you multiple ways to launch:

- Paylinks for fast selling: Useful for freelancers, agencies, creators, and small SaaS teams that need to start charging quickly.

- Embedded checkout for product-led flows: Better when checkout should feel native inside your app or site.

- API and webhooks for deeper control: Best for developers that want automated subscription logic, internal tooling, or custom post-payment actions.

The platform also has a real-time dashboard for payments, subscriptions, churn, and payouts, plus native Discord and Telegram integrations for memberships and paid community access.

If your business lives in Discord or Telegram, built-in access control matters more than generic billing features. Manual role management becomes operational debt fast.

Where Suby fits best

Suby is strongest for teams that care about speed, predictability, and low operational overhead across borders. That includes SaaS, online communities, agencies, consultants, and digital sellers that do not want to build separate tooling for checkout, subscriptions, community access, and payout tracking.

Security and risk controls are also a strength. Suby uses a PCI-DSS Level 1 certified processing partner, supports strong customer authentication and two-factor flows, includes layered fraud controls, handles disputes, and offers zero-fee refunds based on its product documentation.

Its biggest trade-off is also obvious. Settlement is in USDC. If your finance team needs fiat payouts into a bank account, you will need an external conversion step or be comfortable operating with a wallet-native treasury flow. For some businesses, that is a feature. For others, it changes internal accounting and approval workflows.

Pricing is another detail to verify before you commit. Suby states that pricing starts at 5 percent and presents predictable, all-inclusive positioning, while other product messaging references a 4% card-fee example on the website. Exact terms should be confirmed on the official pricing page.

In practice, Suby is the best merchant of record on this list for teams that want a modern payment rail, not just outsourced tax handling. It is compelling when delayed settlements are costing more than the headline processing fee.

2. Paddle

A common SaaS scenario looks like this. Billing works, growth is picking up, and the finance lead is tired of reconciling payments, taxes, subscriptions, fraud reviews, and support tickets across separate tools. Paddle is built for that stage.

Paddle acts as the merchant of record for software companies and takes on billing, indirect tax, chargeback handling, fraud checks, and buyer-facing billing support. This operational model reduces the number of systems your team has to own internally. If you want a broader view of billing stack options outside the MoR model, this comparison of subscription billing software is useful context.

Best for SaaS teams consolidating billing and compliance

Paddle makes the most sense when a company wants one commercial stack instead of a patchwork of payments, tax software, subscription logic, and recovery tools. For early-stage and mid-market SaaS teams, that can remove a lot of operational drag. Fewer vendors means fewer handoffs between finance, product, support, and engineering.

Its ProfitWell and Retain products are part of the appeal. If your team cares about subscription analytics and dunning without wiring together separate systems, Paddle can keep that work under one contract and one data model. That is the practical reason operators shortlist it.

The trade-off is flexibility. A more opinionated platform is easier to launch, but it can get harder once your billing model stops looking like standard B2B SaaS. Usage pricing, edge-case invoicing flows, partner revenue splits, or nonstandard payout requirements are the places to test early. Teams comparing modern alternatives for creators or smaller software businesses also review a Paddle and Lemon Squeezy alternative for global payments and MoR setup.

Where Paddle deserves closer scrutiny

Pricing is the first area to pressure-test. Paddle is not the kind of product where every cost detail is obvious from a simple self-serve pricing page. That does not make it expensive by default, but it does mean you should model total cost, not just the headline fee. Ask about cross-border FX treatment, refund handling, dispute costs, and any revenue thresholds that change commercial terms.

Payout operations also matter. Many teams focus on tax coverage and checkout localization, then realize later that settlement timing affects cash flow more than expected. If your finance team runs tight payroll cycles, spends heavily on acquisition, or needs predictable treasury planning, ask direct questions about payout timing, reserves, account reviews, and exception handling before you migrate.

Paddle is a strong fit for:

- SaaS companies with recurring billing

- Software and AI products selling internationally

- Teams that want fewer billing and compliance vendors

It is less comfortable for:

- Marketplace or multi-party payout models

- Businesses with unusual billing logic

- Teams that need more control over settlement rails or treasury flows

My practical take is simple. Paddle is a mature option for software companies that want to offload billing operations to a vendor with category depth. Just verify how much standardization you are accepting in return, because the convenience is real, and so are the constraints.

3. FastSpring

FastSpring has been in this category long enough that many operators treat it as the default comparison point.

That longevity matters when you are evaluating risk. Mature merchant of record vendors have more established tax processes, broader digital-goods experience, and less need to prove the model itself.

A mature option for software and digital goods

FastSpring is focused on software, SaaS, and digital product businesses. It handles payment processing, tax, compliance, fraud management, refunds, localized checkout, and subscriptions under one roof. For companies selling downloadable software, licenses, or recurring digital services, that scope is practical and familiar.

Its scale also signals category maturity. FastSpring processes over 1 billion dollars in worldwide transactions annually, and its category page on G2 showed 5,809 verified user reviews as of April 2026. That does not make it the right fit for every business, but it does show that merchant of record is not an experimental corner of commerce anymore.

FastSpring is strongest when you need:

- Localized selling: Currency, regional payment experience, and tax handling for international buyers

- Digital product workflows: A platform that already understands software-style sales

- Subscription support: Recurring billing without assembling a custom stack

What to watch before signing

FastSpring is mature, but maturity cuts both ways.

The upside is proven coverage and a long operating history. The downside is that some teams experience account differences depending on product type, support interactions, or business complexity. Public pricing is not posted in a simple self-serve way, so you should expect a commercial conversation.

One thing I would scrutinize with FastSpring is settlement behavior and deductions. Not because that concern is unique to FastSpring, but because it is easy to underestimate how much net payout quality affects operations. A provider can look efficient on paper while still creating finance friction if payout timing, reserves, or adjustments are hard to forecast.

Ask every MoR vendor the same three questions: when funds settle in normal conditions, what triggers holds or reviews, and what reporting explains deductions line by line.

FastSpring is a solid candidate if you sell software globally and want a veteran provider with broad digital commerce experience. It is less compelling if your business needs unusual payout design, creator-community workflows, or a newer settlement model that avoids traditional banking lag.

4. Lemon Squeezy

Lemon Squeezy became popular for a simple reason. It is easier to understand than many older merchant of record platforms.

For indie developers, creators, and small software teams, that simplicity can matter more than advanced enterprise capabilities.

Fast to launch, easy to understand

Lemon Squeezy states that it acts as merchant of record and handles sales tax and VAT collection and remittance for sales processed on its platform. It supports cards and PayPal, subscriptions, licensing, hosted or overlay checkout, and customer portal flows.

The main practical advantage is pricing transparency. In a market where many providers push you into sales calls before you can model costs, Lemon Squeezy publishes a fee structure. That makes it easier for founders to estimate margins and launch without commercial back-and-forth.

If you are comparing small-business-friendly options, this Lemon Squeezy alternative guide is relevant, especially if payout model and cross-border settlement flexibility matter to you.

Where small-business simplicity becomes a limit

Lemon Squeezy works best when your needs are straightforward.

That means:

- Simple product catalog: A few digital products or subscriptions

- Lightweight support expectations: You want self-serve tooling, not white-glove implementation

- Small-team operations: You need speed more than deep customization

The weak point is that all the little add-ons can matter. International fees, PayPal handling, and subscription-related surcharges can raise your effective cost. Store reviews and onboarding standards can also feel strict for some merchants, which is common in platforms trying to control risk tightly.

It is also not the provider I would choose first for a complex B2B billing motion, deep quoting requirements, or unusual account structures. Once your business starts needing more control over packaging, finance operations, buyer support boundaries, or payout engineering, you may outgrow it.

Lemon Squeezy earns its place on this list because it solves the early-stage launch problem well. It is not necessarily the best merchant of record once the business gets more operationally complex.

5. Verifone 2Checkout

Verifone’s 2Checkout platform is useful when you are not committed to one payment operating model yet.

That flexibility is its main selling point. It can support merchant of record, payment service provider, or hybrid approaches depending on how much responsibility you want to outsource.

Useful when you need model flexibility

Some businesses are not ready to hand over the full transaction stack immediately. Others want MoR in some regions and a different setup elsewhere. 2Checkout is one of the better-known options for that kind of middle ground.

It also has broad international coverage. The provider supports 40+ payment methods, 100+ currencies, and 200+ markets, which makes it relevant for merchants with diverse buyer payment preferences or less mainstream regional payment needs.

That matters most when checkout localization is a growth lever, not a compliance requirement.

The trade-off is operational clarity

The challenge with flexible platforms is that flexibility often comes with more decisions, more contract detail, and more need for upfront diligence.

With 2Checkout, I would pay close attention to:

- Commercial model fit: Are you buying MoR because you need legal liability transfer, or just broad payment acceptance?

- Add-on scope: Subscriptions, invoicing, and localized options may be packaged differently than you expect

- Risk policy: Account review standards and acceptable-use interpretations should be understood before launch

This is a platform I would shortlist if you have international demand, want broad payment method support, and need room to choose between MoR and non-MoR models. It is less appealing if your top priority is an opinionated, modern, self-serve experience.

The best use case is a business that values flexibility over elegance.

6. PayPro Global

A common PayPro Global use case looks like this: the product team wants regional pricing, the growth team wants discount tests, and finance still needs clean reconciliation at month end. That combination rules out simpler MoR setups fast.

PayPro Global is strongest when pricing structure is part of the business model, not a checkout setting. If you sell software with multiple plans, local offers, upgrade paths, licensing variations, or frequent packaging tests, it gives you more room to configure commercial logic than many lighter MoR tools.

That matters in practice. A lot of teams do not outgrow basic payment acceptance because volume rises. They outgrow it because pricing gets messy.

Best for teams that need pricing control more than self-serve simplicity

PayPro Global covers the standard MoR responsibilities you expect: payment processing, tax handling, remittance, fraud controls, compliance coverage, and localized checkout. The difference is that it tends to fit companies that want tighter control over how products are packaged and sold across markets.

The trade-off is speed and operational effort.

This is not the option I would pick if the goal is to go live in the fewest possible steps with an opinionated product. PayPro Global makes more sense when the business can justify extra implementation work in exchange for more control over pricing and offer design. For some teams, that is a good deal. For others, it becomes another system that sales, finance, and engineering all need to interpret differently.

Questions to answer before you sign

The right diligence here is operational, not theoretical. I would verify three things early:

- Implementation scope: How much custom setup is required to support your exact pricing model, billing logic, and checkout flows?

- Approval and payout process: What underwriting, documentation, or review steps can slow launch, reserves, or settlements?

- Reporting detail: Will finance get reports that make deductions, taxes, fees, and settlements easy to reconcile without manual cleanup?

Those answers determine whether PayPro Global saves work or shifts it to your team.

As noted earlier, the MoR category is getting more specialized. PayPro Global fits that shift. It is built for sellers that need more than a simple checkout and basic tax coverage. If your business treats pricing as a growth system, it belongs on the shortlist. If your bigger problem is payout speed, cross-border treasury friction, or moving to newer settlement rails such as the stablecoin model platforms like Suby use, PayPro Global may solve the front-end sale without fixing the back-end money movement.

For software companies with nuanced pricing strategy, that can be a fair trade. For simpler sellers, it is often extra overhead.

7. Global-e

Global-e is the outlier on this list because it is not trying to win software startups.

It is built for cross-border e-commerce, especially physical goods brands that need localization, duties handling, and operational support for international retail expansion.

Built for cross-border retail, not software-first billing

If you sell apparel, beauty, consumer goods, or another physical product category internationally, Global-e can make a lot of sense. It can act as merchant of record, localize prices and currencies, support market-specific payment methods, and manage duties and taxes in a way that aligns with cross-border retail operations.

That is a different problem than SaaS billing.

Software businesses care more about subscriptions, invoicing logic, and digital tax workflows. Retail brands care about landed cost presentation, logistics coordination, and reducing checkout friction for international buyers. Global-e is designed around that second set of needs.

When Global-e is the right call

Global-e is the right choice when international retail expansion is a board-level initiative and operational complexity is expected.

It is less likely to be the right choice if you are:

- A small digital seller: The platform is typically aimed higher

- A SaaS company: Subscription-first teams need different strengths

- A creator business: Community monetization and recurring access are not the core use case

The trade-off with Global-e is that enterprise-grade cross-border retail support comes with custom pricing, longer implementation cycles, and a heavier relationship model. That is fine if the business needs it. It is overkill if you do not.

For physical commerce brands going international, Global-e is one of the strongest names to evaluate. For software and creator businesses, it is the wrong category fit.

Top 7 Merchant of Record Comparison

| Product | Implementation complexity | Resource requirements | Expected outcomes | Ideal use cases | Key advantages |

|---|---|---|---|---|---|

| Suby | Low–Medium, paylinks/embeddable/API | Developer time + crypto wallet or fiat conversion workflow | Fast stablecoin (USDC) settlements, reduced payout delays | Internet-native businesses, creators, developer-first SaaS | Unified card+crypto acceptance, USDC settlements, community access automation |

| Paddle | Low, MoR onboarding; simple integration | Minimal internal tax/billing resources (handled by Paddle) | Full MoR coverage: taxes, chargebacks, buyer support | SaaS/subscription companies wanting MoR simplicity | Offloads tax/chargeback liability; built-in revenue/retention tooling |

| FastSpring | Medium, MoR integration and localization | Sales/onboarding effort; platform manages tax/refunds | Mature MoR operations, localized checkout and subscription support | Digital product and SaaS vendors seeking established MoR | Global footprint, clear pricing-mode docs, established platform |

| Lemon Squeezy | Low, hosted checkout, quick launch | Small team; transparent fees; optional add-ons | Rapid launch, tax remittance, licensing and subscription support | Indie creators, small SaaS, developer products | Transparent pricing, fast onboarding, creator-focused features |

| Verifone (2Checkout) | Medium–High, flexible models and integrations | Enterprise integration effort; custom pricing and add-ons | Broad payments/currency coverage; flexible MoR/PSP options | Large/global digital commerce and enterprise sellers | Flexible MoR/PSP models, extensive payment and currency support |

| PayPro Global | Medium–High, configurable platform for complex flows | Developer resources for advanced pricing/packaging; sales onboarding | Highly configurable pricing, localized MoR coverage and risk controls | SaaS/software with complex pricing and packaging needs | Deep configurability and developer tooling for dynamic pricing |

| Global-e | High, enterprise integration and logistics setup | Significant enterprise resources; custom pricing | End-to-end cross-border MoR with duties/tax and logistics support | Physical goods brands expanding internationally at scale | Strong localization, duties/tax management, logistics and commerce integrations |

Final Thoughts

The best merchant of record is not the one with the longest feature list. It is the one that removes the specific bottleneck slowing your business down right now.

If your main problem is tax and compliance burden, most established MoR vendors can help. If your main problem is launching quickly with minimal setup, tools like Lemon Squeezy or Paddle may be attractive. If you run complex software pricing, PayPro Global deserves attention. If you sell physical goods internationally, Global-e is built for a different level of cross-border retail execution.

But there is one issue that too many merchant of record comparisons still underplay. Payout quality.

That matters more than many teams realize. You can outsource tax, fraud screening, and chargeback liability, then still end up with settlement timing that makes planning harder than it should be. In practice, a merchant of record is not a compliance decision. It is a cash-flow decision, a support decision, and a product decision too.

This is why I would group providers into two broad camps.

The first camp solves legal and operational burden. That is valuable and often enough. The second camp also rethinks how revenue reaches the merchant. That is where newer settlement models start to stand out, especially for internet-native businesses that do not want to depend on slow bank-led payout cycles.

Suby is the clearest example of that second camp in this list. Instead of treating payout as an afterthought, it is built around a simpler model. Users pay with cards, businesses receive USDC. For companies operating globally, that can reduce friction around banking delays, FX exposure, and settlement uncertainty. It also makes Suby relevant beyond standard SaaS billing, for creators, online communities, agencies, and developers who want one system for payment acceptance, subscriptions, and access control across Discord and Telegram.

That does not mean every business should switch immediately to stablecoin settlement. Some finance teams still need fiat-first treasury flows. Some organizations will prefer a familiar enterprise MoR even if payout speed is not ideal. That is fine. The important part is not to choose blindly based on headline branding or generic “all-in-one” claims.

Before you sign with any provider, ask five blunt questions: What exactly do buyers pay with? What exactly do we receive, and when? What fees or deductions are visible only after contract review? What triggers holds, reviews, or delayed settlement? How hard is it to migrate away later?

If a vendor gives vague answers, keep looking.

The merchant of record market is growing because the underlying problem is real. Businesses want to sell globally without becoming experts in tax law, payment compliance, and fraud operations. That is reasonable. But the best merchant of record for your company depends on which burden you are trying to remove. Legal burden, engineering burden, support burden, or payout burden. The strongest buying decisions happen when you know which one matters most.

If you want a merchant of record built for modern internet businesses, Suby is worth a close look. It gives you an API to accept payments by card or crypto, supports one-time payments and subscriptions, and includes native Discord and Telegram integrations for paid access and online communities. Customers pay with cards, and your business receives USDC. That is the core advantage. Faster, more predictable global revenue without the usual banking friction.