Gaspard LEZIN

Best Payment Platforms for Non-US Founders

Find the best payment platforms for non-US founders. Our guide compares Stripe, Paddle, Suby, and more on fees, payouts, and global access.

You've built a product, customers are ready to pay, and the main friction starts after checkout. A card processor supports your buyers but not your company registration. Another approves the account, then holds payouts for days or routes funds through banking rails you cannot easily access. A third works fine for US founders and turns into a constant workaround for everyone else.

That is the actual filter non-US founders need to use.

The question is not just who can process a payment. It is who will onboard your entity, support the countries where your customers live, settle funds in a form you can use, and avoid draining margin through FX spreads, payout delays, reserves, or extra compliance friction. If you sell software, services, or digital products, the answer often depends as much on settlement and account eligibility as on checkout conversion. Founders comparing payment stacks often start with card acceptance, then realize the harder problem is what happens after the charge clears. For teams also evaluating the top digital product selling platforms, that distinction matters even more.

The international payments market has fragmented as cross-border commerce has grown. Non-US founders now have three real paths: traditional fiat processors such as Stripe or Checkout.com, Merchant of Record platforms such as Paddle or Lemon Squeezy, and newer options that keep customer payment methods familiar while settling to stablecoins instead of bank payouts. Earlier research from GoCardless on international payment gateways makes the same broad point. Cross-border collections are no longer a one-model category.

If you're trying to choose the best payment platform for a non-US company, start with one practical decision. Do you want standard bank payouts, with all the country, banking, and settlement constraints that come with them, or do you want to accept familiar payment methods and receive settlement in USDC through a stablecoin-native system such as Suby? That single choice usually eliminates half the list.

Table of Contents

Why Suby stands out

Who should pick it

Where Stripe still wins

Best use case

Where it fits

Why founders choose it

Where it works best

What to expect

When it makes sense

Best fit

Where it earns a spot

Top 10 Payment Platforms for Non‑US Founders, Features & Fees

The Final Decision Bank Rails or Stablecoin Rails

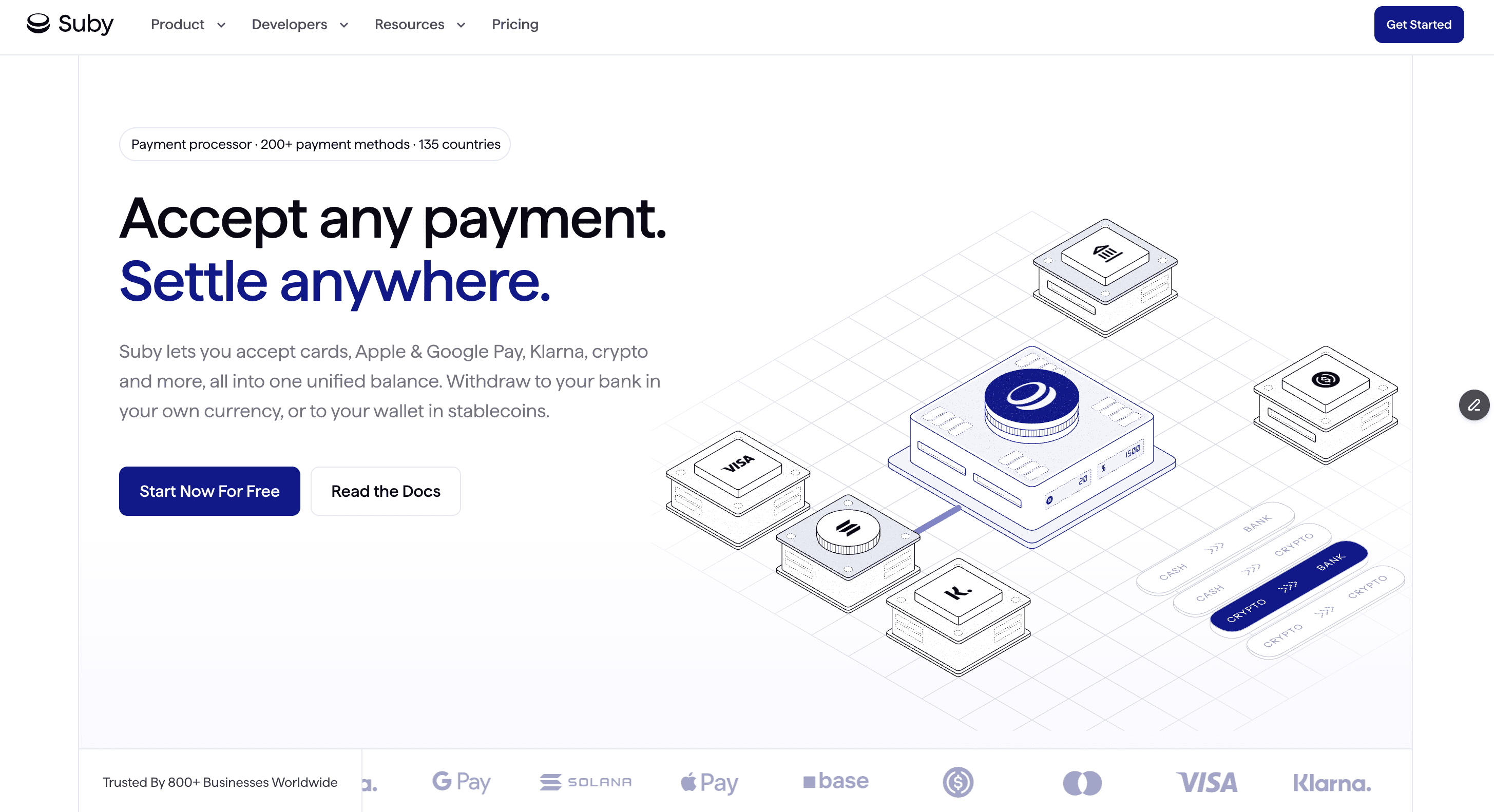

1. Suby

Suby is the most interesting option on this list if your main problem isn't checkout conversion alone, but settlement. Customers can pay with cards or crypto, and the business receives USDC. That matters for founders who don't want to depend on local bank support, SWIFT timing, or cross-border payout rules that change by country.

This is why I'd put Suby at the top for internet-native businesses, agencies, global SaaS teams, and creators running subscriptions or paid communities. It solves the front-end and the back-end in one flow. Customers get familiar ways to pay, and the business gets revenue in USDC instead of waiting on bank rails.

A closer look helps.

Why Suby stands out

Suby offers a payment API, paylinks, embeddable checkout, and webhooks for businesses that want to launch quickly or build directly into an existing product stack. The practical pitch is simple. Users pay with cards, businesses receive USDC.

That stablecoin-native model fills a gap most listicles miss. Traditional gateway roundups often focus on fiat processors, while a separate review notes that Suby settles revenue instantly in USDC to wallets and positions its all-inclusive pricing at 5%, which is worth verifying on Suby pricing before making a decision because current rates should always come from the official page.

Practical rule: If your business already keeps treasury in USDC, a bank payout is often the extra step, not the goal.

Suby also stands out for community monetization. If you sell subscriptions, paid access, or private memberships, it includes native Discord and Telegram integrations for access control and subscription lifecycle management. That's a real operational advantage over piecing together checkout, bot tools, and manual role updates. If you sell digital access, it also pairs well with these top digital product selling platforms.

Who should pick it

Suby makes the most sense if you want predictable settlement and don't want your payment stack tied to a specific banking setup. It's especially practical for founders in regions where fiat payouts are slow or unreliable, and for teams that want card acceptance without ending up trapped by banking friction after the payment clears.

Its trade-off is clear too. Settlement is in USDC by design. If your finance team needs local fiat deposits as the final destination, you'll need an off-ramp step.

A few strengths stand out in day-to-day use:

Unified acceptance: Customers can pay by card or crypto, while the business receives USDC.

Flexible setup: You can use paylinks, embedded checkout, or the API depending on how custom your stack is.

Built-in community tooling: Discord and Telegram access management removes a lot of manual work for membership businesses.

Security and operations: Suby documents support for a PCI-DSS Level 1 certified processing partner, strong customer authentication, dispute handling, and zero-fee refunds on its official website.

2. Stripe

Stripe is still the default answer for a lot of software companies, and there's a reason for that. It's available in more than 42 countries and is widely used by SaaS startups, marketplaces, and e-commerce businesses because the API, billing tools, and multi-currency support are strong, according to XflowPay's payment platform analysis.

If you have a supported entity and want maximum developer control, Stripe is hard to ignore. You can prototype fast, use hosted checkout if you want less frontend work, and expand into subscriptions and invoicing without replacing the core stack.

Where Stripe still wins

Stripe is best when engineering velocity matters more than payout structure. Teams that want to build custom billing logic, platform flows, or a polished checkout usually move faster with it than with many legacy processors.

But non-US founders need to be careful. Platform quality and founder eligibility are two different questions. Some non-US businesses can use Stripe smoothly, while others run into country support limits, bank account requirements, or payout friction. If you're weighing those trade-offs, this alternative to Stripe breakdown is worth reading.

Stripe is excellent software. It isn't automatically the best operational fit for a founder outside the markets it supports cleanly.

Costs also need a realistic view. The verified data tied to this topic notes transaction fees around 3% plus conversion costs, with settlement windows in the multi-day range. That's workable for many teams, but it's rarely the cheapest or simplest path once international payouts become a core issue.

3. PayPal including PayPal Checkout

A common non-US founder setup looks like this. Customers know and trust PayPal, sales come in from several countries, and checkout conversion improves the moment the PayPal button appears. Then the harder question shows up after the sale. How fast do funds settle, what does FX cost, and how reliably can you move money out if you do not have US banking infrastructure?

That is the primary lens for PayPal.

PayPal is still one of the easiest ways to add buyer familiarity, especially for consumer transactions. If your audience already uses PayPal, offering it can reduce hesitation and recover orders that a card-only checkout might lose. For some markets, that trust effect is the main reason to add it.

Best use case

PayPal fits best as a conversion tool, not as the core operating rail for a global company. It helps at checkout. It is less convincing if your main priority is clean treasury flow, predictable payouts, and low-friction international settlement.

The trade-off for non-US founders is operational control. Availability, holds, reserves, dispute handling, and withdrawal options can vary a lot by country and account profile. A setup that feels fine at low volume can become harder to manage once larger balances, recurring transactions, or cross-border refunds enter the picture.

Margins matter here. PayPal can look acceptable on headline processing fees, then get more expensive once currency conversion and settlement friction are included. If you sell internationally, it is worth understanding how to avoid currency conversion fees before you treat PayPal proceeds as usable net revenue.

I usually view PayPal as an add-on payment method rather than the main stack. Traditional fiat processors such as PayPal can help you capture demand, but they are not built around fast global payouts for founders without US banking. That is where the gap with merchant of record models and stablecoin-native options becomes obvious. If your priority is buyer trust at checkout, PayPal deserves a test. If your priority is reliable access to funds across borders, it usually needs a second system behind it.

4. Payoneer

A common scenario for non US founders looks like this. A client wants to pay in USD, you do not have a US bank account, and you need the money to arrive without weeks of banking friction. Payoneer is built for that problem.

I see Payoneer less as a checkout platform and more as payout infrastructure. It works well for agencies, freelancers, exporters, and marketplace sellers who need local receiving accounts in major currencies and a practical way to collect cross-border payments. If your revenue starts with invoices or platform payouts, Payoneer can cover a real gap that Stripe, PayPal Checkout, or a Merchant of Record usually do not solve in the same way.

Where it fits

Payoneer is strongest after the sale, not at the moment of conversion. It helps you receive funds, hold balances, and move money across countries without opening a traditional US banking setup. For a founder outside the US, that is often the difference between being able to invoice globally and having to ask clients for awkward workarounds.

The trade-off is product depth. Payoneer does not give you the same subscription billing stack, hosted checkout control, or tax-handling layer you would get from a direct processor or a merchant of record model for digital businesses. If you sell SaaS or memberships online, Payoneer usually sits behind the business as a collection rail, not in front of it as the growth engine.

Costs can also become less attractive once FX and withdrawal friction enter the picture. That may be acceptable in B2B services, where getting paid reliably matters more than shaving every basis point off processing. It is less appealing for founders comparing fiat rails with stablecoin-native options like Suby, where the main appeal is faster settlement and fewer banking dependencies.

Best for invoices and payouts: Strong fit for agencies, freelancers, cross-border service businesses, and marketplace earnings.

Less ideal for online checkout: Subscription products and consumer flows usually need another layer for billing and conversion.

Useful for non US founders: It can help you collect major currencies without opening a US bank account.

If I were running a service business, I would seriously consider Payoneer. If I were building a global SaaS company and cared about checkout conversion, tax setup, and fast access to funds, I would treat it as one piece of the stack, not the whole stack.

5. Paddle

Paddle sits in a different category from most processors here because it operates as a Merchant of Record. For non-US founders selling SaaS or digital products, that can remove a huge amount of tax and compliance work from day one.

That's the core appeal. Paddle becomes the seller of record, so you don't carry the same operational burden around tax calculation, collection, and remittance that you would with a direct processor.

Why founders choose it

If you're a small SaaS team without a finance or tax function, Paddle can be a relief. You get a checkout and subscription setup that's designed for software sales, and you avoid a lot of jurisdiction-by-jurisdiction headaches.

The trade-off is flexibility. Merchant of Record platforms are opinionated by nature. They simplify compliance because they sit in the middle of the transaction, but that also means you give up some control over the exact payment architecture and customer flow.

For many founders, that's still a good trade. If you're comparing this route with other MoR models, this explanation of a merchant of record setup is useful context.

For lean SaaS teams, paying more for a Merchant of Record can be cheaper than building compliance in-house badly.

I'd choose Paddle when tax burden is the main blocker and your business is firmly in SaaS or digital goods. I'd look elsewhere if settlement flexibility or custom payment routing matters more than offloading compliance.

6. Lemon Squeezy

Lemon Squeezy has become a popular choice with indie founders for a reason. It packages payments, subscription handling, and Merchant of Record logic into something that feels easier to start with than an enterprise payment stack.

For a solo builder or small software team, that simplicity matters. You can sell digital products and subscriptions without becoming an expert in tax compliance first.

Where it works best

Lemon Squeezy is a good fit when speed matters more than payment architecture depth. If you want a storefront, paylinks, subscription support, and a relatively clean setup process, it's attractive.

It also helps that the platform is oriented around digital products rather than broad retail complexity. That usually means fewer moving parts for indie SaaS and template, course, or software sellers. If you are weighing the two, it is worth understanding why founders prefer Lemon Squeezy over Stripe for early digital-goods sales before you commit to either.

The limitation is scale complexity. Once a business needs more custom routing, tighter control over payout behavior, or a specialized finance stack, all-in-one simplicity can start to feel restrictive. That doesn't mean you'll outgrow it quickly. It means you should choose it for convenience, not because it's the final form of global payments.

I'd shortlist Lemon Squeezy if your business is small, digital-first, and you want compliance handled with minimal setup. I wouldn't make it the automatic choice for a business that already knows it needs custom billing flows or nonstandard payout requirements.

7. FastSpring

FastSpring has been around long enough to earn trust with software sellers that want a Merchant of Record partner instead of a raw processor. Its value is straightforward. It handles payments, subscriptions, and global tax responsibilities in one package.

That makes it especially relevant for software vendors that want to sell globally without turning billing compliance into an internal project.

What to expect

FastSpring is rarely the flashy choice. It's the operational choice for teams that want an established vendor handling the messy parts of software commerce.

Its localized checkout and broad support for international selling are useful, but the bigger story is what it removes from your team's workload. Tax collection, remittance, and compliance overhead can consume far more time than founders expect.

The trade-off is the same one you see with most Merchant of Record platforms. You gain simplicity and reduce legal exposure, but you lose some control and may pay more than you would with a processor-only setup.

This is usually a good fit for software companies that want to stay focused on product and growth. It's less compelling for founders who already have a strong internal finance setup and want finer control over payment economics.

8. Checkout.com

Checkout.com is more enterprise-leaning than most of the tools above. If Stripe feels startup-friendly and easy to self-serve, Checkout.com feels like the platform you move toward when payments become a dedicated function inside the company.

That's not a criticism. It's a useful distinction.

When it makes sense

Checkout.com supports businesses in 159 countries, according to the verified data associated with this topic. That kind of international footprint matters if you're expanding fast and need broad coverage from one provider.

It's strongest when a company wants advanced routing, reporting, and more flexibility in commercial structure than a packaged SMB processor usually gives. Larger teams often appreciate that. Smaller teams often find it heavier than they need.

If your company doesn't have someone who actively owns payments, enterprise processors can create as much work as they remove.

I'd consider Checkout.com when your volume is meaningful, your markets are spread out, and you're ready for a sales-led relationship. I wouldn't put it at the top for an early-stage founder who just needs to start taking payments quickly.

9. Adyen

Adyen is built for scale. It's the kind of platform large e-commerce and marketplace businesses pick when they want direct acquiring, unified commerce, and more control over how payments run across channels.

For non-US founders, the question isn't whether Adyen is capable. It is. The question is whether your business is large enough to justify the operational weight.

Best fit

The verified data for this article notes that Adyen supports merchants across 159 countries. That reach is substantial, but it comes with a more enterprise-style implementation approach than plug-and-play tools.

If you need online, in-app, and point-of-sale support in a unified setup, Adyen is one of the strongest names on the market. If you mainly need a checkout page and subscription billing, it can be more platform than you need.

Another useful detail from the verified data is qualitative rather than numerical. Adyen's integration burden tends to be higher than lighter developer-first tools. That matches the practical experience many teams report. It's powerful, but it expects maturity from the business using it.

I'd recommend Adyen for larger operations that already know payments is a strategic capability. I wouldn't recommend it as the first stop for most non-US founders trying to solve basic international collection and payouts.

10. 2Checkout Verifone

2Checkout, now part of Verifone, earns its place because it's often a practical middle ground. It gives international merchants access to a wide set of payment methods and localized checkout options without requiring the complexity of a more enterprise-heavy provider.

That makes it attractive for cross-border e-commerce businesses that want broader payment method support than cards alone.

Where it earns a spot

The verified data available for this topic says 2Checkout operates in 200 countries, supports more than 100 currencies, and is viewed as a strong affordability option among non-US SMBs in Europe-focused operations, based on Wise's international payment gateway roundup.

That doesn't make it the automatic winner. Plans matter, and extra fees can show up depending on the payment methods or regional options you need. So the platform has to be reviewed at the pricing-plan level, not just at the headline feature level.

Where 2Checkout tends to work well is for merchants who want localization without negotiating separate contracts across multiple providers. That convenience is real. The trade-off is that the most advanced capabilities may sit behind higher-tier plans, and some businesses outgrow the packaged approach.

If you want broad method coverage with less enterprise overhead, 2Checkout is a reasonable platform to test. If you need deep custom routing or a treasury model built around USDC settlement, it won't cover the full problem.

Top 10 Payment Platforms for Non‑US Founders, Features & Fees

Provider | Core features | Payment methods & settlement | Integration & UX | Pricing & predictability | Best for / USP |

|---|---|---|---|---|---|

Suby | Global payment layer; one‑time & subscriptions; paylinks, embeddable checkout, API + webhooks; Discord/Telegram access management | Visa/Mastercard + crypto (USDC, USDT, ETH, SOL, BNB); revenue settled directly to merchant USDC wallet (no bank/SWIFT) | Launch in minutes; developer‑friendly API; real‑time dashboard; built‑in subscription lifecycle | Flat, all‑inclusive fee marketed as predictable (verify current rates on pricing page) | Internet‑native businesses & creators needing predictable USDC settlements and built‑in community access controls |

Stripe | Full payments platform with Billing, Invoicing, Hosted Checkout and developer tooling | Cards + many alternative methods; multi‑currency support; bank settlements (country onboarding required) | Rich APIs, webhooks, hosted checkout; mature docs and ecosystem | Pay‑as‑you‑go; add‑on product fees can increase total cost | Companies wanting deep developer control and extensible payments stack |

PayPal (Checkout) | Wallet + processor with checkout and seller protection | PayPal wallet, cards, Pay Later; country‑specific fee schedules | Quick setup; familiar consumer checkout that often boosts conversion | Transparent per‑country fees (varies by currency/transaction) | Merchants seeking high consumer recognition and fast go‑to‑market |

Payoneer | Cross‑border receipts, cards, mass payouts and account consolidation | Local receiving accounts (USD, EUR, GBP, JPY, etc.); 70+ currencies supported | Account‑centric UX for payouts and consolidated balances | Fees depend on account type and FX; practical for invoicing/receipts | B2B sellers and marketplaces needing local receiving accounts without a US bank |

Paddle | Merchant‑of‑Record (MoR) handling payments, tax, compliance and chargebacks | Multiple payment methods via MoR; vendor remittance handled by Paddle | Embedded checkout, subscription tooling and analytics | Custom/negotiated pricing; MoR includes tax/compliance costs | SaaS/digital sellers who want to offload tax and compliance liability |

Lemon Squeezy | MoR for digital goods with subscriptions, licensing and marketing tools | MoR covers payments and taxes; global availability (200+ countries) | Fast setup with paylinks, embeddable checkout, built‑in email/audience tools | Pricing tied to subscriber counts or plan tiers | Indie SaaS and small teams selling digital products with marketing needs |

FastSpring | MoR focused on software/SaaS with localized checkout and tax remittance | Full MoR payments and global tax handling; localized currencies/methods | All‑in‑one checkout and subscription management | Flat all‑in‑one pricing with optional add‑ons | Software vendors wanting an out‑of‑the‑box global sales solution |

Checkout.com | Enterprise payment processor with advanced routing, reporting and pricing | Cards and 150+ currencies; domestic acquiring in many markets | Enterprise tooling and reporting; sales‑led onboarding | Choice of fee structures (including interchange++), sales‑negotiated | Scale‑ups and enterprises that need global routing and pricing flexibility |

Adyen | Direct acquiring + payment platform across online, in‑app and POS | Wide global coverage; interchange++ and method‑specific pricing | Unified commerce capabilities; enterprise integrations | Interchange++ transparent pass‑through; sales‑led onboarding | Large ecommerce/platform businesses requiring direct acquiring and scale |

2Checkout (Verifone) | Global processor with localized checkouts and many local methods | Support for 45+ payment methods; localized checkout depending on plan | Packaged plans with add‑ons for regional methods | Plan fees and add‑ons vary by region and feature set | Merchants needing broad local payment coverage without multiple contracts |

The Final Decision Bank Rails or Stablecoin Rails

Choosing among the best payment platforms for non-us founders comes down to one operational question. What do you want the money to become after the customer pays?

If the answer is a standard bank payout in local or foreign fiat, then the right platform usually depends on your business model. Stripe is strong when developer tooling matters and your entity is well supported. PayPal is useful when buyer familiarity helps conversion. Payoneer is practical for invoices and marketplace payouts. Paddle, Lemon Squeezy, and FastSpring make sense when tax and compliance are bigger problems than payment flexibility. Checkout.com and Adyen are better fits once payments become a serious internal function, not just a plugin.

But there's a second path that matters more now than it did a few years ago. You can accept familiar customer payment methods, especially cards, and settle revenue in USDC instead of waiting on traditional payout rails. That is an entirely different setup. It reduces your dependence on local banking, avoids a lot of FX friction, and gives you a more predictable settlement destination if your business already operates globally.

That's why stablecoin-native systems deserve a different level of attention in this category. They aren't just another processor with slightly different fees. They change the payout layer itself. For many non-US founders, especially those running online-first businesses, that solves the harder half of the problem.

Suby is the clearest example in this list. Users pay with cards, businesses receive USDC. That's the value proposition in plain language. It also adds practical tools that matter for modern internet businesses, including paylinks, API access, subscriptions, and native Discord and Telegram integrations for paid communities and access control.

The catch is simple and worth stating plainly. Stablecoin settlement is ideal if you want wallet-based treasury and predictable cross-border access to revenue. It's less ideal if your business is built around direct fiat deposits into local bank accounts and you don't want an off-ramp step. That isn't a flaw. It's a design choice, and the right one depends on how your company already operates.

So the final decision is less about which platform has the most features on a pricing page. It's about which rail matches your business reality.

If your company is comfortable living on bank rails, choose the processor or Merchant of Record that best fits your compliance burden and integration needs. If your company wants faster global payouts, more predictable settlement, and less dependence on cross-border banking infrastructure, stablecoin rails are often the cleaner answer.

If you want a payment stack built for that second model, Suby is the platform to look at first. It lets customers pay with cards or crypto while your business receives USDC, and it adds API access, subscriptions, paylinks, and native Discord and Telegram integrations for paid access and community monetization.