Gaspard LEZIN

Best Payment Platform for International SaaS Expansion

Find the best payment platform for international SaaS expansion. A criteria-driven guide to comparing checkout, currency, settlement models, and costs.

Your product is selling in more countries than your finance stack was built for. Signups arrive from Europe, Latin America, Southeast Asia, and the Gulf. Revenue shows up too, but it lands slowly, gets converted at awkward moments, and creates a constant gap between what customers paid and what your business receives.

That gap gets expensive fast.

Most founders start by comparing payment platforms on checkout widgets, API docs, and dashboard polish. Those things matter. But the bigger decision is usually hidden in the payout model. How does money move after the customer clicks pay? Do you wait for bank rails, batch payouts, and FX conversion? Or do you receive settlement in a form that gives you more control over timing, treasury, and cross-border operations?

That’s the lens that matters when choosing the best payment platform for international SaaS expansion. A clean checkout can help conversion. A better settlement model can change the economics of the business.

Table of Contents

Your Guide to International SaaS Payment Platforms

Revenue friction starts after the sale

Slow payouts create operating drag

Local payment expectations vary by market

Compliance becomes a recurring operational tax

Global checkout experience

Multi-currency and FX handling

Settlement and payout model

Payment method acceptance

Subscription management

Compliance and security

A quick comparison table

Stripe

Adyen

Suby

Why settlement changes the whole equation

Where this model fits best

A practical migration checklist

Your Guide to International SaaS Payment Platforms

A familiar pattern shows up when a SaaS company starts expanding well outside its home market. Sales look healthy. Customer demand is real. Support tickets are manageable. But finance starts reporting weird inconsistencies. Payout timing shifts from one region to another. Currency conversion becomes hard to forecast. Reconciliation takes longer every month.

That’s usually the moment the team realizes payments aren't a checkout problem alone. They’re a cash flow system, a risk system, and a growth system at the same time.

I’ve seen founders spend weeks comparing feature lists while ignoring the one question that affects margins every single day. How do we receive our money? Traditional setups often treat settlement as an afterthought. For an international SaaS company, it shouldn’t be an afterthought at all.

A practical way to assess the best payment platform for international saas expansion is to separate the decision into business outcomes, not just product features:

Customer outcome: Can buyers pay in a way that feels local and reliable?

Finance outcome: Can the company predict what it will receive and when?

Operational outcome: Can the team manage compliance, support, disputes, and recurring billing without stitching together too many systems?

Treasury outcome: Does settlement create more banking dependency, or less?

Practical rule: If two platforms look similar at checkout, compare how they settle funds. That’s where the real trade-off usually lives.

A platform can have excellent developer tools and still create friction once money crosses borders. Another can offer broad country coverage and still leave you dealing with payout uncertainty, manual treasury moves, or slow bank transfers.

That’s why payment infrastructure becomes strategic as soon as international revenue starts to matter. The decision shapes approval rates, churn risk, finance workload, and how quickly you can re-invest revenue into growth.

The Core Challenges of Global SaaS Payments

For most SaaS teams, international payments become painful long before they become impossible. The stack works, technically. Customers can often pay. Finance can usually close the month. But the process gets heavier with every new market.

International revenue now accounts for 70% of SaaS revenue, which makes cross-border payment infrastructure central to how these businesses operate, not a side concern, according to Suby’s overview of international SaaS payment platforms.

Revenue friction starts after the sale

The first problem is forced conversion. A customer pays in one currency. The processor settles in another. Your bank may convert again depending on where the account sits and how your entities are structured.

None of that friction is visible in your growth dashboard. It shows up in margin erosion, finance reconciliation, and treasury planning. Teams often discover they’re not optimizing payments for acceptance alone. They’re also absorbing conversion cost and timing risk in the background.

Slow payouts create operating drag

Traditional payout flows can also make a healthy SaaS business feel cash constrained. Bank-dependent settlement introduces waiting, exceptions, and regional inconsistency. Finance teams then build workarounds: more spreadsheets, more internal explanations, more “expected by Friday” language that never feels reliable.

The issue isn’t only speed. It’s predictability. When settlement timing changes across processors, countries, or banking partners, planning gets harder for payroll, vendor payments, and working capital.

Most global SaaS payment pain doesn’t come from one dramatic failure. It comes from constant small frictions that stack up across every market.

Local payment expectations vary by market

Customers don’t all pay the same way. What feels standard in one country can be unfamiliar or unavailable in another. That matters because localized payment options can boost checkouts by 20 to 30% in emerging markets, as noted in this analysis of payment platforms for international SaaS expansion.

If your checkout is globally available but locally mismatched, you’ll lose buyers without always knowing why. The issue may look like weak demand when it’s really payment method fit.

A stronger platform should help with:

Local relevance: Presenting payment methods customers already trust

Currency clarity: Reducing confusion at checkout and after billing

Authorization resilience: Lowering avoidable failures tied to regional mismatch

Compliance becomes a recurring operational tax

The final challenge is administrative. Cross-border SaaS payments create more review, more controls, and more edge cases. Teams need to think about authentication requirements, dispute workflows, customer records, and region-specific rules. If your processor leaves too much of that burden on your internal team, growth gets expensive in ways that don’t show up on a pricing page.

For a grounded look at how compliance pressure affects payment operations, Buttercloud's fintech expertise is a useful reference.

An Evaluation Framework for Payment Platforms

A payment platform should be judged the same way you’d judge core infrastructure. Not by demo polish, but by how it behaves under scale, across markets, and under finance scrutiny.

Global checkout experience

The first test is what the buyer sees. A strong platform lets you present pricing cleanly, reduce friction at payment, and support the way international customers buy.

That includes local currency display, region-appropriate payment flows, and a checkout that doesn’t feel imported from a different market. If buyers hesitate at the final step, your acquisition costs go up because more paid traffic dies at the point of payment.

Good checkout design isn’t just aesthetic. It affects trust.

Multi-currency and FX handling

Many teams underestimate the problem. Multi-currency support sounds good, but you still need to know where conversion happens and who absorbs the cost.

Ask these questions early:

Display versus settlement: Can you show local prices while settling in a currency that works for your business?

FX responsibility: Is the platform converting for convenience, or forcing conversion where you’d rather keep control?

Treasury clarity: Can finance forecast settlement without guessing which balances will be converted and when?

If you’re comparing providers, it helps to review their pricing model alongside these settlement mechanics. A useful companion read is this breakdown of payment gateway pricing, especially if your current provider looks inexpensive until FX and payout friction are included.

Settlement and payout model

This is the most overlooked category, and often the most important. Traditional providers usually settle to bank accounts on their own timetable. That can be acceptable for domestic sales. It gets harder when your revenue base is global and your treasury needs are time sensitive.

A better framework is simple. Does the platform give you predictable access to funds, or does it add more dependency on banks, conversion steps, and payout schedules?

Decision lens: Features help you collect money. Settlement design determines how usable that money is once collected.

Payment method acceptance

Cards matter. So do local methods in many regions. For some businesses, digital asset acceptance also matters, especially when customers are global and internet-native.

What “good” looks like depends on the business model. A B2B SaaS company may prioritize card reliability and invoicing support. A community business might need card and crypto acceptance in the same checkout. The right platform should fit the audience you already serve, not the average merchant profile.

Subscription management

Recurring billing is where small gaps become churn. Dunning, retry logic, plan changes, failed payment recovery, and lifecycle communication all affect retention. A provider can support subscriptions on paper while still leaving too much manual work for your team.

Look for a setup that handles:

Billing continuity: retries, reminders, and renewal logic

Plan flexibility: upgrades, downgrades, and cancellations without custom patchwork

Operational visibility: clear status for active, failed, and at-risk subscriptions

Compliance and security

This is the category nobody wants to think about until there’s a problem. For SaaS businesses expanding internationally, that’s too late. Security standards, authentication flows, and dispute handling need to be built into the provider’s operating model.

You’re not only evaluating fraud prevention. You’re evaluating whether the platform reduces internal burden or creates more process around every exception.

Comparing the Top International Payment Contenders

Most comparison articles stop at “good API,” “global reach,” or “trusted brand.” That’s useful, but incomplete. For international SaaS, the more honest comparison is this: which platform helps you accept payments globally, and which platform gives you the cleanest settlement outcome after the transaction is approved?

A quick comparison table

Feature | Stripe | Adyen | Suby |

|---|---|---|---|

Global checkout reach | Strong currency coverage and mature APIs | Strong enterprise global coverage | Built for global online payments with card and crypto acceptance |

Developer integration | Very strong | Strong, but heavier enterprise implementation | API, webhooks, paylinks, and embedded checkout |

Settlement model | Traditional processor and bank-linked settlement | Traditional enterprise settlement model | Businesses receive USDC |

Best fit | Developer-led SaaS teams | Large, complex organizations | Internet-native businesses that want card payments with USDC settlement |

Subscription support | Strong recurring billing tooling | Strong recurring and enterprise billing support | Supports one-time payments and recurring subscriptions |

Operational trade-off | Flexible, but bank and payout logic still matter | Powerful, but onboarding and implementation can be heavier | Requires comfort with wallet-based USDC settlement |

For another broad market view of platform trade-offs, this roundup on 2026 payment processor selection is useful, especially if your shortlist also includes more mainstream SMB options.

Stripe

Stripe is often the default starting point for SaaS teams, and for good reason. It supports payments in more than 135 currencies, offers highly flexible APIs, and is trusted by Shopify, Amazon, and DocuSign, according to ConnectPay’s review of international payment gateways.

That combination makes Stripe attractive to engineering-led companies. Teams can move quickly, customize extensively, and avoid the clunky feel that some older processors still carry. If your product roadmap depends on strong developer tooling, Stripe remains a serious option.

The trade-off is less about checkout quality and more about operating model. Stripe still sits in the traditional processor framework. Settlement, bank account dependencies, and payout timing are part of the equation. For many SaaS businesses, that’s fine. For companies optimizing global treasury and payout predictability, it may leave unresolved friction.

Adyen

Adyen tends to fit organizations with more scale, more entities, and more operational complexity. It’s often chosen by teams that need a serious enterprise payments layer across multiple markets and channels.

Its strengths are structural. Adyen is built for larger implementations, centralized control, and advanced payment operations. If you have internal payment specialists, complex reporting needs, or regional acquiring considerations, that matters.

The trade-off is that Adyen isn’t usually the fastest path for a lean SaaS team. Implementation and onboarding can feel heavy if what you need is straightforward global recurring billing with clean settlement.

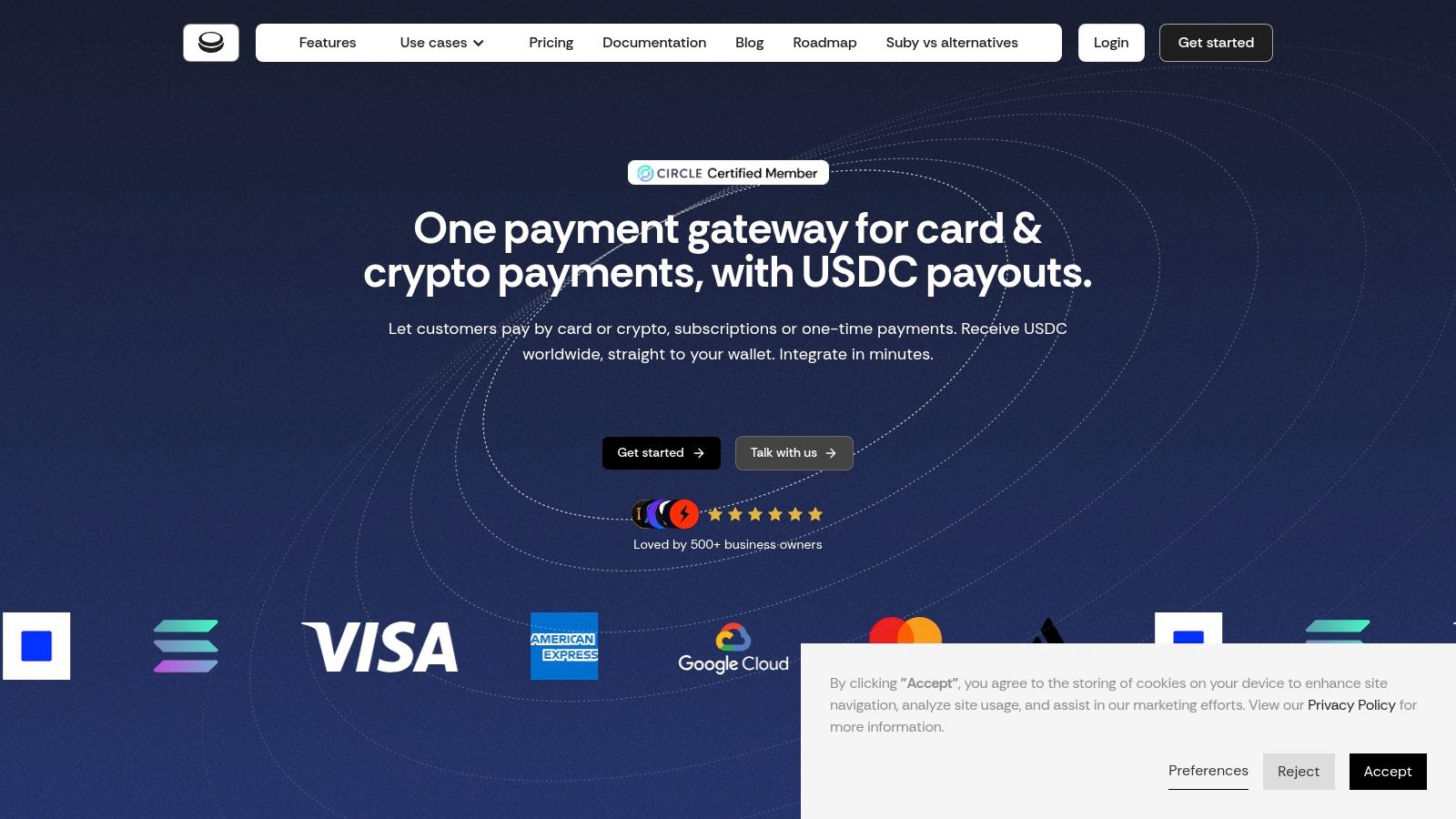

Suby

For businesses that care most about how they receive funds, Suby changes the comparison because the settlement model is different. Customers can pay by card or crypto, and businesses receive USDC. That matters if your current pain comes from bank delays, FX conversion friction, or not knowing when funds will land in a usable form.

This is the core distinction. Most platforms optimize acceptance first and settlement second. Suby is designed around both. It provides an API for businesses that want to accept payments by card or crypto, supports recurring subscriptions and one-time payments, and also offers native Discord and Telegram integrations for paid access, memberships, and community monetization. In practical terms, users pay with cards, businesses receive USDC.

If your company is global by default, settlement in a digital dollar can be more operationally useful than waiting for cross-border bank payouts in fragmented currencies.

That won’t fit every team. Some finance departments are still structured entirely around bank payout workflows. If that’s your internal reality, a traditional processor may be easier politically even if it’s less efficient operationally.

The key is to choose based on the bottleneck you have. If the bottleneck is API flexibility, Stripe is compelling. If it’s enterprise scale and internal payment operations, Adyen makes sense. If the bottleneck is settlement predictability across borders, a card-pay-in and USDC-payout model deserves serious consideration.

The Modern Approach Card Payments and USDC Settlement

The old model asks international SaaS companies to optimize around banking constraints. The newer model starts from the internet’s actual operating environment. Customers pay online. Businesses sell across borders. Treasury needs faster and cleaner movement of funds.

Why settlement changes the whole equation

When users pay with Visa or Mastercard and the business receives USDC, several persistent problems get simpler. You reduce dependence on bank payout timing. You avoid building treasury around repeated currency conversion. You also get a clearer handoff between payment collection and fund control.

This matters most for companies that already operate globally by default. SaaS founders, digital product teams, agencies, and online communities don’t need more banking complexity. They need payment acceptance that feels normal to the customer and settlement that feels predictable to the business.

That’s why stablecoin-based settlement is more than a payments feature. It changes how revenue behaves once it leaves the checkout. For teams exploring treasury options after settlement, this guide on how to earn safe stablecoin yield is a helpful starting point, especially if finance is thinking beyond simple receipt of funds.

A model like this is also easier to work with when you want one system for both mainstream and internet-native buyers. If you’re evaluating mixed acceptance flows, this overview of how to accept crypto payments for business adds useful context.

Where this model fits best

This approach is especially practical when your business looks like one of these:

Global SaaS products: You bill customers in many markets and don’t want cross-border bank payout friction.

Online communities: You monetize access inside Discord or Telegram and need payment plus access control in one workflow.

Agencies and freelancers: You sell internationally and prefer receiving USDC instead of waiting on international bank settlement.

Developer-led teams: You want an API and webhooks instead of a manual finance process stitched together from multiple tools.

Later in the buying process, teams usually want to see the flow in action. This walkthrough helps with that:

The biggest mindset shift is simple. Don’t evaluate the platform only by how a customer pays. Evaluate it by how your business gets paid.

Migrating to a New Global Payment Platform

Changing payment infrastructure is one of those projects that sounds smaller than it is. The technical integration is only one layer. The primary work is making sure billing continuity, customer trust, and finance operations survive the transition cleanly.

A practical migration checklist

Start with the operating model, not the API.

Map your current flows: List where checkout happens, how subscriptions renew, how disputes are handled, and where settlement lands today.

Define the future state: Decide what you want to improve first. Checkout localization, recurring billing reliability, settlement predictability, or a mix of the three.

Audit dependencies: Note where your CRM, analytics, support tooling, and finance processes rely on the existing processor.

Then move into implementation planning.

Test the integration path: Use sandbox environments, simulate renewals, and verify webhook behavior before touching production traffic.

Handle customer billing data carefully: Existing subscriptions, tokenized payment details, and renewal timing need a clear migration plan.

Plan communications early: Some users may need to re-authenticate or update payment methods. Tell them plainly and before the switch.

A technical implementation guide like this payment gateway migration reference is useful once you’ve already agreed on the business requirements.

Go live in stages if you can.

Launch advice: Migrate one region, one customer segment, or one pricing plan first. A controlled rollout exposes edge cases without putting your whole revenue base at risk.

Watch support tickets, failed payments, renewal behavior, and settlement flow closely in the first days after launch. The right migration isn’t the one that looks clean in a project tracker. It’s the one customers barely notice, while finance immediately feels the improvement.

Suby is a payment gateway and Merchant of Record. Your customers pay with card, bank transfer, Apple Pay, Google Pay, Klarna, and more, or stablecoins, and you get paid out to your bank account, or directly in stablecoins (USDC, EURC) to your wallet, anywhere in the world, no bank account required. It provides an API, paylinks, embedded checkout, recurring subscriptions, and native Discord and Telegram integrations for paid access and online communities. For international SaaS expansion, that model makes settlement a product decision, so predictable payouts stop being an afterthought as you add markets.