Most advice about payment gateway pricing starts with the advertised rate. That's the wrong starting point.

If you're shown a fee like 2.9% + $0.30, you're looking at a sticker price, not the full economics of getting paid. For a domestic card transaction, that headline rate may be close enough. For a global business, it usually isn't. Cross-border fees, currency conversion spreads, settlement timing, and operational work all affect what you ultimately keep.

That matters more every year because digital payments are becoming central to how online businesses operate. The global payment gateway market is projected to grow from $35.7 billion in 2025 to $146.1 billion by 2034, a projected 16.9% CAGR, according to Research and Markets' payment gateway market outlook. Bigger market, more providers, more complexity.

Founders often ask the wrong question: "What's your transaction fee?" The better question is, "What is my total effective cost per sale?"

Table of Contents

- Your Payment Gateway's Real Price Is Not What You Think

- Why one fee is really several fees

- Flat-rate vs interchange-plus

- When simplicity helps and when it hurts

- Where international costs actually come from

- Why settlement delay is a cost even when it isn't listed as a fee

- A simple formula for effective cost

- Example one SaaS subscription sold internationally

- Example two digital product sold worldwide

- A side-by-side comparison table

- Is the cheapest published rate usually the cheapest option?

- Why do international sales feel more expensive even when order volume is growing?

- Should I always choose flat-rate pricing if I want simplicity?

- Why does local currency pricing matter so much?

- Can one provider support cards and other digital payment methods together?

- What should I look at first when comparing gateways?

Your Payment Gateway's Real Price Is Not What You Think

Most founders treat payment gateway pricing like shipping. They expect a clear line item and a final total.

Traditional gateways don't work that way. The visible fee is often only the first layer. Once you sell across borders, your payment stack starts to look more like an airline ticket. The base fare gets your attention, but the final bill changes after baggage, seat selection, taxes, and exchange costs.

The same thing happens in payments. A headline rate may look manageable, then your effective cost rises after card type differences, processor markup, extra international fees, and conversion costs. If you only compare pricing pages, you'll miss what hits your margin.

That gap matters because small changes in payment cost scale quickly. On a high-volume store or subscription business, a narrow fee difference can turn into a meaningful margin issue over time.

The useful number isn't the advertised rate. It's the amount left after every fee, conversion, and payout step.

A better way to think about payment gateway pricing is this:

- Sticker price means the rate shown on the pricing page.

- Effective cost means the full cost to accept, convert, settle, and access the funds.

- Operational cost means the friction around those payments, such as reconciliation work, refund handling, and payout timing.

Founders also get tripped up by the word "gateway." In practice, you're paying for several things at once. You're paying for acceptance, routing, risk controls, settlement, and sometimes currency handling. If you sell internationally, those pieces don't stay neatly bundled.

Once you understand that, the pricing discussion changes. You stop asking which provider has the lowest published rate and start asking which model produces the lowest real cost for your business.

Deconstructing Standard Payment Gateway Pricing Models

A card payment fee looks simple from the outside. Underneath, it's layered.

Consider a restaurant bill. You don't just pay for the ingredients. You also pay for the kitchen, staff, rent, and service. Payment gateway pricing works the same way. One transaction fee usually combines several underlying charges.

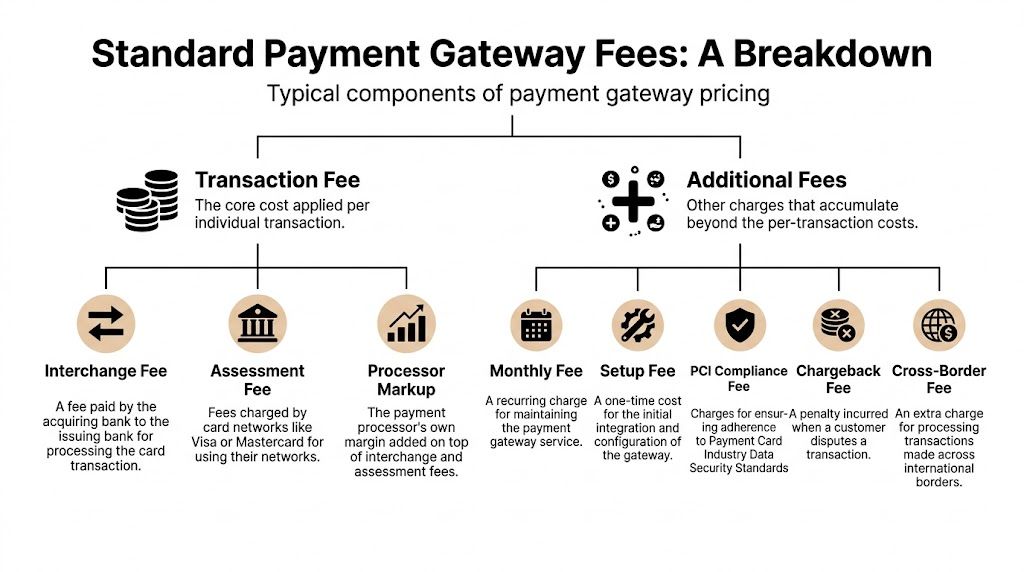

Why one fee is really several fees

At a basic level, a standard card transaction fee often includes these layers:

- Interchange fee. This is the base cost tied to the card transaction and paid within the card ecosystem.

- Assessment or network fee. This covers use of the card network.

- Processor or gateway markup. This is the provider's margin for packaging the service and making it usable for merchants.

Then there are the extras that may sit outside the transaction fee:

- Monthly platform fees

- Setup or account fees

- PCI-related charges

- Chargeback costs

- Cross-border surcharges

If you only look at the headline percentage, you don't know how much of the cost is fixed by the card ecosystem and how much is provider margin.

That distinction matters because different pricing models expose or hide those layers.

Flat-rate vs interchange-plus

Most founders first encounter flat-rate pricing because it's easy to understand. You pay one published rate per transaction, and the provider handles the complexity behind the scenes.

The advantage is convenience. The drawback is that convenience can become expensive as your volume grows or your customer mix changes.

By contrast, interchange-plus pricing separates the underlying interchange cost from the provider's markup. That sounds more complicated, but it can be more efficient if you process enough volume to care about fee precision.

A concrete example helps. For a $100 domestic US transaction, a flat-rate model at 2.9% + $0.30 costs $3.20. An interchange-plus model can bring that same transaction down to roughly $2.20 to $2.70, according to Spreedly's explanation of payment gateway fees and pricing.

That same source notes that rewards cards can carry interchange as high as 2.95%, which is one reason flat-rate pricing can become inefficient. The provider has to price for a wide range of outcomes, and the merchant often absorbs that blended margin.

When simplicity helps and when it hurts

Flat-rate pricing is often a reasonable starting point when you want fast setup and predictable billing.

Interchange-plus tends to make more sense when:

- You process higher volume and small fee differences matter.

- Your card mix is favorable because debit and lower-cost cards don't need to subsidize expensive cards as heavily.

- You want clearer negotiating power because the provider markup is easier to isolate.

If you're comparing providers, it helps to review practical buying guides alongside fee mechanics. A resource like best payment processing software for small business can help you frame the software-side tradeoffs, but you still need to inspect the fee model underneath.

Practical rule: If a provider makes pricing sound effortless, ask what assumptions are being averaged into that simplicity.

Another point causes confusion. Founders sometimes think "interchange-plus is always cheaper." It isn't. If your volume is low, your operational priorities may justify a flat rate. The lesson isn't that one model wins in every case. The lesson is that payment gateway pricing is a model choice, not just a number.

The Hidden Costs of Selling to a Global Audience

Domestic transactions are the easy part. International payments are where margins start leaking in places your pricing page never mentioned.

When you sell to buyers in other countries, your fee stack usually adds costs for location, currency movement, and payout flow. Each one may look manageable on its own. Together, they change the economics of the sale.

Where international costs actually come from

There are three common sources of extra cost in global payments.

First, some providers add a cross-border fee because the card or transaction is international.

Second, they may apply an FX spread when the customer pays in one currency and you settle in another. That spread often hides in the exchange rate rather than appearing as a clean line item.

Third, there are secondary operational costs around settlement and reconciliation. These may not look like fees, but they affect cash access and finance overhead.

The quantitative picture is clearer than many merchants expect. Payabl's payment gateway pricing guide says cross-border and multi-currency fees can add 1-3% per transaction, while FX spreads add another 0.5-2%. Combined with a base fee such as 2.9% + $0.30, the total cost for a $100 international sale can reach 4-6.5%.

That same guide gives a useful benchmark from the merchant side. A UK business with £20K in monthly international sales could see total fees of more than £3700, a blended rate of 3.7%.

If you want a deeper breakdown of the moving parts in global transactions, this overview of a cross-border payment gateway is a helpful companion read.

Why settlement delay is a cost even when it isn't listed as a fee

Founders often treat settlement timing as an operations issue. Finance teams know it's a pricing issue too.

If your provider takes days to settle funds through traditional banking rails, you carry several hidden burdens:

- Working capital pressure. You're waiting to access revenue you've already earned.

- Forecasting noise. Payout timing gets harder to map cleanly.

- Support overhead. Customers think payment was instant, while your internal teams still wait for availability.

- Currency exposure. The longer funds move through conversion and banking layers, the more uncertainty you absorb.

Indeed, "cheap" pricing can become misleading. A provider may publish a competitive transaction rate while still creating a slower, less predictable payout flow for international revenue.

Small international fees don't stay small when they stack on every order, every renewal, and every payout cycle.

The hidden-cost problem gets worse when teams localize prices for conversion. That step is usually good for revenue, but if the provider's currency handling is opaque, each local-price sale can carry an embedded spread that isn't obvious to the business owner reviewing dashboards later.

For global merchants, payment gateway pricing isn't just about acceptance. It's about what happens after the card is approved.

How to Calculate Your True Cost Per Sale With Examples

Once you stop trusting the headline rate, the next question is practical. How do you calculate the actual cost of a sale?

Use a simple rule. Start with the visible processing fee, then add every charge created by geography, currency, and payout mechanics. If any of those pieces are unclear, treat the pricing as incomplete until the provider explains it.

A simple formula for effective cost

Your true cost per sale can be framed like this:

| Cost layer | What to include |

|---|---|

| Base acceptance cost | The published transaction fee and fixed fee |

| Card and market adjustments | Any extra fee for international cards or regions |

| Currency cost | FX spread, conversion markup, or local currency pricing cost |

| Exception handling | Chargebacks, refunds, and related service fees |

| Settlement friction | Delay, banking movement, and reconciliation overhead |

That last row is the one teams skip. It isn't always a neat line on the invoice, but it still changes margin and cash access.

A customer-facing detail also matters here. 93% of global consumers say pricing in their local currency significantly influences purchase decisions, according to Airwallex's 2025 payment processing statistics roundup. That same source says traditional localization methods often include FX markups of 2-5%, and links those frictions to the 70% average cart abandonment rate in cross-border e-commerce.

So localization can help conversion, but it can also increase cost if your provider handles currency poorly.

Example one SaaS subscription sold internationally

Let's say you run a SaaS business and charge customers monthly. A customer sees a localized price, pays by card, and your provider settles later in a different currency.

In a traditional model, your effective cost may include:

- The base card processing charge

- An extra fee because the card is international

- An FX markup because the customer paid in local currency

- Admin work around matching settlement amounts to invoices

The tricky part isn't just the direct fee total. Subscription businesses feel these issues repeatedly. Every renewal runs through the same pricing logic, so small inefficiencies persist month after month.

For recurring revenue businesses, I suggest asking one question per renewal flow: "Does this payment return the same currency economics every time, or do they drift depending on country, card type, and payout route?"

If the answer is "it depends," your finance model is doing more work than it should.

You can compare that logic with a plain-English breakdown of what are stripe fees, especially if you're trying to understand why the advertised card rate often isn't the whole story in subscription businesses.

Example two digital product sold worldwide

Now take a digital product seller with buyers across multiple countries.

For each sale, the founder might see a dashboard entry that looks healthy. Revenue came in, customer paid, order succeeded. But the effective margin changes if:

- One buyer used a domestic card

- Another used an international card

- One paid in your settlement currency

- Another paid in a local currency that triggered conversion

- Your provider batches payouts on a delayed schedule

This is why two orders with the same list price can produce different net outcomes.

A practical method is to audit a sample of recent international sales and classify each one by:

- Customer country

- Checkout currency

- Settlement currency

- Published fee

- Any extra international or FX fee

- Actual net received

That sample doesn't need to be huge to be useful. You're looking for patterns, not perfection.

If finance has to explain why two identical-priced orders net differently, the pricing model is already too opaque.

A side-by-side comparison table

Here is a simple comparison format you can use internally.

Example Cost Calculation for a $100 International Sale

| Fee Component | Traditional Gateway Example | Suby (All-Inclusive Model) |

|---|---|---|

| Base processing fee | Published card fee applies | Included in all-in pricing |

| Cross-border fee | May be added separately | Included in all-in pricing |

| FX markup | May be embedded in conversion | Not applicable when business receives USDC |

| Settlement model | Bank-based payout flow may add delay and reconciliation work | USDC settlement to wallet |

| Total cost visibility | Split across several moving parts | One clear fee model |

Notice what this table does not do. It does not pretend every provider charges the same line items in the same way. It gives you a framework for comparing clarity, not just price.

That matters because with international payments, lower visible pricing can still produce a higher effective cost.

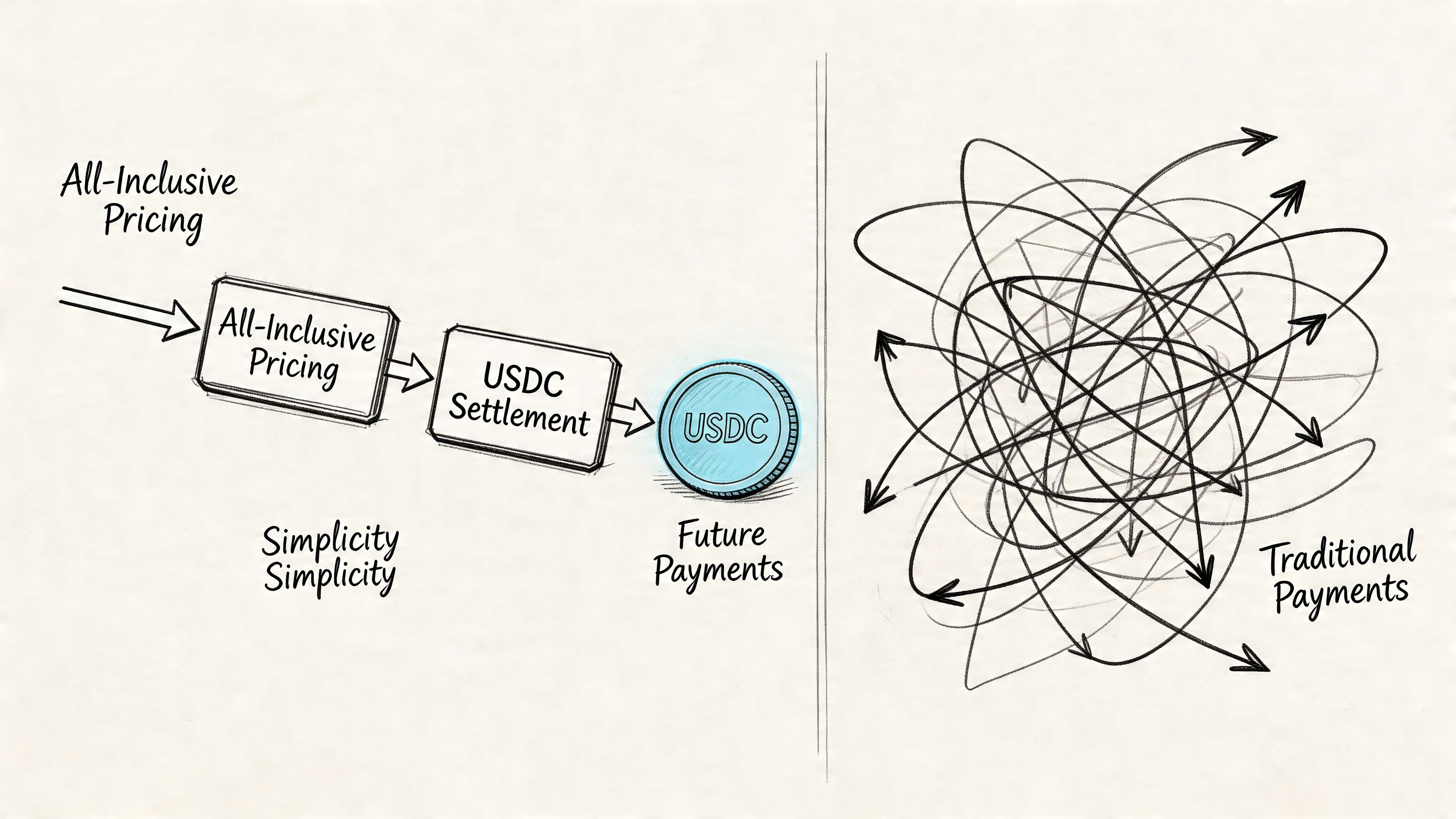

A Modern Approach with All-Inclusive Pricing and USDC Settlement

The old model separates acceptance, currency conversion, and payout into different layers. That's why so many merchants struggle to pin down the exact cost of a global sale.

A newer model simplifies the stack by collapsing those layers into one pricing approach and one settlement outcome.

Why founders care about total cost of ownership

For global businesses, the deeper problem isn't only transaction pricing. It's total cost of ownership.

That includes direct fees, conversion costs, payout timing, internal reconciliation, and the uncertainty that comes from moving money through multiple banking and FX layers. Razorpay's discussion of payment gateway pricing impact on margins frames this clearly. It notes that merchants can lose 7-10% on cross-border sales once compounded FX markups and delays are included. The same source also points to a documented alternative, a stablecoin-based gateway model with 5% all-inclusive pricing and instant USDC settlement.

That doesn't mean every business should switch models immediately. It means founders should compare the full payment system, not just the front-end transaction rate.

How the new model works in practice

A stablecoin settlement model changes the design of the payment flow.

The customer can still use familiar payment methods. The business then receives settlement in USDC, which removes the need for the old chain of bank conversions and payout uncertainty. That shifts the conversation from "What extra fees might appear?" to "What is the single settlement outcome?"

For internet-native businesses, that matters because payment operations become more predictable:

- Revenue arrives in one settlement asset

- FX handling doesn't sit between checkout and payout

- Cross-border complexity is reduced

- Finance teams spend less time decoding provider statements

There's also a product angle. Some providers in this category offer an API for payment acceptance, support one-time payments and subscriptions, and add native community monetization tools through Discord and Telegram. The core pattern is simple: users pay with cards or crypto, and businesses receive USDC.

A useful overview of that operating model is this guide on how to accept crypto payments for business.

One short demo explains the shift well:

The important point isn't novelty. It's accounting clarity.

A transparent all-in fee is often easier to evaluate than a lower advertised fee with variable currency and payout costs attached.

This model won't remove every payments challenge. Disputes still exist. Customer support still matters. Checkout quality still matters. But it does remove one of the biggest sources of confusion in payment gateway pricing, which is the gap between what the provider advertises and what the merchant receives.

Your Checklist for Evaluating Payment Gateways

When you're comparing providers, don't ask for a pricing page first. Ask for a cost map.

A cost map tells you where fees appear, when funds settle, what currency you receive, and which exceptions create extra charges. If a provider can't explain that clearly, the pricing is not clear.

Pricing questions to ask before you sign

Use these questions in sales calls and procurement reviews.

- What is the fee for international cards? You want a direct answer, not a broad statement about global coverage.

- How do you handle currency conversion? Ask whether the provider applies a markup or spread, and where that appears.

- Do you publish an all-in rate or a base rate with extras? This tells you whether the provider is optimizing for transparency or marketing.

- Are refunds and disputes priced separately? These don't affect every transaction, but they do affect the business.

- Do subscriptions introduce extra billing costs? Some providers package recurring billing differently from one-time payments.

A useful response from a provider sounds concrete. A weak response sounds like "it varies by market" without detail.

Operational questions that change the real cost

This second set is where experienced operators separate from first-time buyers.

- When do funds settle, and in what form? Timing and payout format affect working capital.

- Do we receive bank payouts or wallet settlement? That changes speed and cross-border handling.

- What does reconciliation look like? If statements are hard to map back to orders, your finance cost rises.

- What happens when a customer pays in one currency and we report in another? Such currency differences often create hidden friction.

- Can the system support our actual business model? Subscriptions, online communities, paylinks, API-driven sales flows, and digital access all have different needs.

I also suggest requesting one sample statement before committing. Not a polished pricing PDF. A real statement or realistic fee breakdown.

If you can't explain the invoice to your finance lead in one pass, the provider has not made pricing simple.

One final filter helps. Separate "easy to buy" from "easy to operate." Plenty of gateways are easy to sign up for. Fewer are easy to run globally without surprise costs, payout confusion, or constant support tickets.

Good payment gateway pricing isn't just low. It's understandable.

Conclusion The Path to Transparent Global Payments

The headline rate on a gateway pricing page is rarely the number that matters most.

For global businesses, the actual cost of accepting payments includes the visible transaction fee, the less visible currency and cross-border charges, and the operational friction created by delayed or unclear settlement. That's why payment gateway pricing should be evaluated as a full system, not a single percentage.

Founders who understand total effective cost make better choices. They compare what the customer pays, what the provider takes, what currency arrives, and how quickly they can use the funds.

That shift is pushing the industry toward simpler models. Transparent, all-inclusive pricing and USDC settlement offer a cleaner way to think about global payments. Less hidden complexity. More predictable outcomes. Better decisions.

Frequently Asked Questions About Gateway Pricing

Is the cheapest published rate usually the cheapest option?

Not necessarily. A low published rate can still lead to a higher effective cost if the provider adds cross-border fees, currency spread, or slow settlement.

Why do international sales feel more expensive even when order volume is growing?

Because the fee stack changes. Geography, payout currency, and reconciliation effort can all make the net result weaker than the gross revenue suggests.

Should I always choose flat-rate pricing if I want simplicity?

Only if simplicity is your priority and the economics still work. Flat-rate pricing is easier to understand, but it can hide inefficiencies as volume grows.

Why does local currency pricing matter so much?

Customers prefer seeing prices in their own currency. That can improve trust and purchase intent, but only if the provider's conversion handling is transparent enough that you don't give margin back on every sale.

Can one provider support cards and other digital payment methods together?

Yes, some providers do that. What matters is the settlement model behind it. If the checkout is unified but the payout flow is still fragmented, you may still inherit complexity on the back end.

What should I look at first when comparing gateways?

Start with settlement. Ask what you receive, when you receive it, and what costs appear between customer payment and your final payout.

If you're evaluating a simpler model for global payments, Suby is worth a look. Suby provides an API that lets businesses accept payments by card or crypto, while businesses receive USDC. It also offers native integrations with Discord and Telegram for subscriptions, paid access, and online communities. The core idea is straightforward: users pay with cards, businesses receive USDC.