You're probably dealing with this already. A customer in another country reaches checkout, tries to pay, and disappears. Sometimes the issue is trust. Sometimes it's a card decline. Sometimes the customer expected a wallet, bank transfer, or installment option you don't offer. From the merchant side, the pain shows up later as fragmented payouts, awkward reconciliation, FX leakage, and payout timing you can't really control.

That's why alternative payment methods matter now. They're not just a checkout add-on for edge cases. They've become part of the core payment stack for any business selling online across borders. The practical question isn't whether customers want more ways to pay. It's how to give them that choice without making your finance and operations teams absorb the complexity.

Table of Contents

- Start with the business model, not the payment catalog

- Integration gets messy faster than most teams expect

- What a unified setup changes

- Regional behavior changes the right payment mix

- Use cases where APM strategy is operational, not cosmetic

Beyond Credit Cards The New Reality of Global Payments

Card acceptance still matters, but a card-only mindset creates blind spots. If you sell internationally, you're not just processing payments. You're navigating local payment habits, different approval paths, and the downstream effect of how those payments settle back to your business.

That changes the merchant conversation. The old view was simple. Add more payment options to reduce friction at checkout. The better view is broader. Payment method choice affects conversion, yes, but it also affects routing, settlement speed, reconciliation workload, and what currency you ultimately hold after the sale.

The market has already moved. Digital wallets were the leading payment method for ecommerce in North America in 2024, with a 39% share of transaction volume, ahead of credit cards at 32% according to Checkout.com's overview of alternative payment methods. That matters because it shows customer behavior has shifted past the point where wallets and other alternative payment methods can be treated as optional extras.

Practical rule: If your checkout only reflects how your acquiring bank wants to process payments, it probably doesn't reflect how your customers want to pay.

For merchants, the more interesting shift is on the back end. APMs let you separate two decisions that used to be bundled together. The customer can use the payment method they trust, while you choose how revenue is routed, settled, and held. That opens the door to more predictable treasury management, especially for businesses that want to avoid constant banking friction and unstable payout timing.

If you're already thinking about where payments and digital assets overlap, this short guide to tokenization for crypto investors is useful background because it helps explain why modern payment systems increasingly focus on programmable settlement, not just front-end checkout.

Why this matters in day-to-day operations

A failed payment isn't just a lost order. It can trigger support tickets, retries, disputes, accounting work, and delayed revenue recognition. When that happens repeatedly across markets, payments stop being a conversion issue and become an operations issue.

The merchants that handle this well usually do one thing differently. They treat alternative payment methods as part of market access and cash management, not just user interface design.

What Exactly Are Alternative Payment Methods

Alternative payment methods are easiest to understand if you stop thinking about them as a list of brand names and start thinking about them as different payment rails.

A rail is the path money takes from the customer to the merchant. Some payments travel over traditional card networks. Others move through bank-to-bank systems, wallets, or method-specific schemes built for particular markets and devices.

Think in terms of rails, not logos

The core technical distinction is straightforward. An alternative payment method is defined by whether the transaction is routed through card networks or through an account-to-account, wallet, or scheme-specific rail, as explained in Solidgate's APM guide.

That sounds technical, but the business effect is simple. Different rails create different trade-offs around checkout friction, fraud exposure, reversibility, settlement flow, and coverage by region.

Here's the mental model I use:

- Card-based but easier for the customer: Mobile wallets like Apple Pay or Google Pay often still rely on the underlying card network, but they reduce typing and use device authentication.

- Bank-based and direct: Open banking and real-time transfer methods move money from the customer's bank account without relying on card rails in the same way.

- Wallet-based ecosystems: Some digital wallets hold credentials, stored value, or a direct relationship with the user that sits above the merchant checkout.

- Installment-led methods: BNPL changes not just the payment path, but the customer's decision process at the moment of purchase.

- Digital currency rails: These can support global settlement without depending on traditional bank payout infrastructure in the same way.

The main categories merchants actually deal with

Most businesses don't need a giant taxonomy. They need a usable map.

Digital wallets

These include products where the wallet provider manages the customer relationship and often stores payment credentials or balances. They usually reduce friction because the customer doesn't have to type card details at checkout.Mobile wallets

These are device-driven and usually tokenize an existing card or bank account. From the shopper's perspective, they feel fast and familiar. From the merchant's perspective, they often preserve the card authorization path while improving the user experience.Bank transfers and open banking

These methods are attractive when you want direct account-to-account movement and less dependence on card interchange structures. They can be especially relevant in markets where bank-based payments are already normal.Buy now, pay later

BNPL can help when the purchase needs financing logic, not just payment acceptance. It's less about replacing cards entirely and more about reducing decision friction on higher-ticket orders.Cryptocurrency and stable settlement flows

Some businesses accept digital asset payments directly. Others use them more strategically, as a way to receive settlement in a stable digital dollar format even when the customer paid through a different front-end method.

The useful question isn't “Which APMs exist?” It's “Which rails fit the way my customers buy, and which settlement flow fits the way my business operates?”

If you follow payments hiring or market specialization, even niche roles now focus on APM operations and technical routing. That's visible in postings like these AUSFF Bitcoin options, which are a reminder that adjacent digital asset topics often show up around payment method selection, settlement design, and market-specific acceptance requirements, even when the merchant's real need is simpler than the terminology around it.

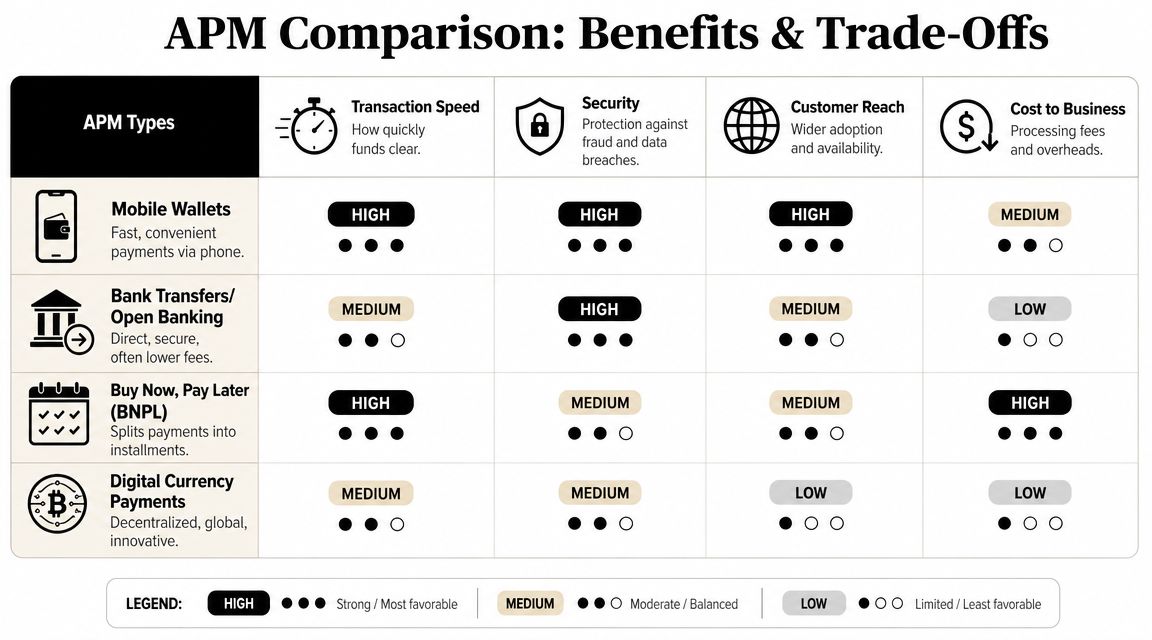

Comparing APMs A Look at Benefits and Trade-Offs

Alternative payment methods aren't better than cards by default. They're better at specific jobs.

That's the right way to compare them. A mobile wallet can improve speed and trust at checkout while still keeping you inside card-network economics. A bank transfer can reduce certain costs and dispute patterns, but it may fit some countries and business models better than others. BNPL can help close a sale, but it changes the transaction economics and customer support picture.

The broader shift is already visible at market level. Non-card payment methods accounted for 61% of global e-commerce transactions in 2024, according to Nuvei's analysis of alternative payment methods. For merchants, that makes APM strategy a routing, localization, and settlement-cost decision, not just a checkout design choice.

The business lens that matters

When I look at APM selection from a product and operations angle, five criteria usually matter most:

How fast the customer can complete payment

Friction kills intent. Wallets often win here because they compress the checkout flow.How the merchant pays for acceptance

Some methods make sense on headline processing cost but create hidden costs in reconciliation, customer support, or regional setup.How reversible the payment is

Chargeback exposure is not the same across rails. That matters if your business gets hit with dispute-heavy patterns.How quickly funds become usable

Settlement timing changes cash planning. It also changes how much working capital friction your business absorbs.How broadly the method travels across markets

Some APMs are great locally and weak internationally. Others are globally familiar but less optimal in specific countries.

Alternative Payment Method Comparison

| APM Type | Settlement Speed | Typical Fees | Chargeback Risk | Global Reach |

|---|---|---|---|---|

| Mobile wallets | Often fast for authorization, settlement follows the underlying network | Varies by processor and underlying rail | Similar to card-based flows when routed over card networks | Strong in many mature ecommerce markets |

| Bank transfers and open banking | Can be fast, sometimes near real time depending on rail | Often attractive where account-to-account is established | Generally different dispute profile from card payments | Highly regional, strongest where local bank rails dominate |

| BNPL | Merchant usually gets a clear payment outcome at checkout | Can be expensive relative to simpler methods | Consumer dispute dynamics differ from standard card checkout | Strong in specific consumer segments and product categories |

| Digital currency payments | Can be fast once the network confirms | Depends on provider, conversion path, and payout design | Different operational risk model than card disputes | Useful for global internet-native buyers and settlement flows |

A few patterns show up consistently in practice:

- Mobile wallets are excellent at reducing checkout friction, especially on phones. They don't automatically solve cost or settlement issues.

- Bank-based methods can improve margin structure and reduce reliance on card rails, but they require localization discipline.

- BNPL is a sales tool as much as a payment method. It makes more sense for businesses with larger baskets or purchases that benefit from installment framing.

- Digital currency payments are most interesting when paired with stable settlement goals, especially if the merchant wants to reduce dependence on bank payout windows.

A payment method can improve conversion and still be a bad operational fit. The right question is whether it improves revenue after support, reconciliation, and settlement are accounted for.

If you're comparing providers that help assemble this stack, a practical reference point is this guide on an alternative to Stripe, which is useful for thinking about what merchants really need once they go beyond a single card processor.

How to Choose and Integrate APMs for Your Business

Most businesses make the same mistake at the start. They ask, “Which payment methods should we add?” The better question is, “Which customer segments and settlement constraints are we trying to solve?”

Start with the business model, not the payment catalog

A SaaS company with recurring billing needs different rails from a cross-border agency sending invoices or a creator monetizing a private community. The checkout may look similar to the customer, but the operational priorities aren't the same.

Use these filters first:

Market fit

Start with where your customers are and what they already trust. A payment method that performs well in one region may be nearly irrelevant in another.Payment pattern

One-time high-value purchases, recurring subscriptions, prepaid access, and community memberships all behave differently.Payout preference

This is the part many teams ignore. Ask what currency you want to hold after the sale, how often you want settlement, and whether bank payouts create delays or conversion losses through FX.Operational tolerance

Every direct APM integration brings more reporting logic, more edge cases, and more reconciliation work.

Integration gets messy faster than most teams expect

One APM looks manageable. Four or five can become a small payments program.

Each method may bring its own webhook behavior, refund workflow, dispute handling, settlement timing, and reporting format. Finance teams then have to match customer payments, processor statements, fees, and final payouts across multiple systems. Product teams have to manage fallbacks, retries, localization, and checkout logic by region.

If you want a quick signal that this has become a serious specialist function, even hiring markets reflect it. Roles focused on technical operations for APMs, like these Unlimit jobs on Blockchain Jobs, exist because multi-method payment operations get complex very quickly.

Operator's view: The cost of supporting many payment methods rarely sits in the first integration. It shows up in exceptions, accounting, support tickets, and payout handling.

A short explainer helps here:

What a unified setup changes

A more practical approach is to unify acceptance while simplifying settlement. Instead of wiring every method into separate operational paths, you use one integration layer that lets customers pay in the way they prefer while the business receives a consistent payout result.

That's where an API approach becomes more strategic than a simple checkout plugin. For example, Suby's business payment flow shows a model where any business can accept payments by card or crypto, and also use native Discord and Telegram integrations for subscriptions, paid access, and online communities. The key point is operational. Users pay with cards, businesses receive USDC. That separates customer choice from merchant settlement in a very practical way.

For a lot of internet-native businesses, that's the actual goal. Not “add every APM.” Add the right payment options, then keep your internal payout and treasury workflow simple.

APMs in Action Regional Trends and Use Cases

The fastest way to get APM strategy wrong is to assume online buyers behave the same everywhere. They don't. What feels normal in one market can feel awkward or untrustworthy in another.

That's why regional payment behavior matters more than generic checkout advice. In developed markets alone, customer adoption patterns already show meaningful divergence. In the U.S., a 2024 survey found that 72% of consumers had adopted online or mobile payment accounts like PayPal, Zelle, or Venmo. In Australia, nearly one-third of the population used Buy Now Pay Later in the past year, as noted in Primer's guide to alternative payment methods in the U.S..

Regional behavior changes the right payment mix

In Europe, bank-linked and domestic methods often carry more weight in the buying experience than many non-European merchants expect. In parts of Latin America, local real-time transfers and cash-adjacent payment habits still shape who can buy online at all. Across Asia, wallets and app-centric payment flows are often embedded in daily digital behavior rather than treated as separate checkout tools.

This has a practical implication. Localization is not just translation and local currency display. It includes payment familiarity, settlement logic, and method availability tied to region.

A business expanding internationally should usually ask:

- Which method feels domestic to the buyer?

- Which method lowers support friction after purchase?

- Which methods create payout fragmentation on the merchant side?

If you're evaluating expansion from the merchant side, this guide to cross-border payment challenges is a useful companion because it focuses on what happens after the sale, not just how the checkout looks.

Use cases where APM strategy is operational, not cosmetic

For SaaS companies, the best APM mix usually supports low-friction signup and predictable recurring collections. The issue isn't just initial conversion. It's whether renewals, retries, and customer communication remain manageable across countries.

For ecommerce brands, APMs can help match local buyer expectations and reduce the number of customers who reach checkout but don't trust the final payment step. In practice, that often matters most in mobile-heavy buying journeys.

For agencies and freelancers, settlement can matter more than checkout variety. A client may want to pay by card because it's familiar on their side, while the business receiving funds may prefer to avoid traditional cross-border payout delays and FX handling.

For creators and community operators, payment is tightly linked to access control. Discord and Telegram monetization work best when billing, renewals, and access changes happen in one flow instead of across several tools.

APM selection becomes much easier when you decide what you want to optimize. Buyer trust, margin, payout speed, and treasury simplicity often pull in different directions.

That's why the best setup is rarely the one with the most logos on the checkout page. It's the one where payment choice improves customer completion while settlement stays predictable for the business.

Building a Future-Proof Payment Strategy

Alternative payment methods now sit at the center of online commerce, but the strategic takeaway isn't just “offer more options.” More methods can increase conversion and expand market reach, yet they also add routing complexity, reconciliation work, and payout fragmentation if you handle them badly.

The stronger approach is to separate the customer's payment preference from the merchant's settlement preference. Let the buyer use the method that feels normal to them. Then design your back end so the business receives revenue in a form that is stable, predictable, and easy to operate around.

What holds up over time

Payment stacks age badly when they're built around one acquirer, one region, or one payout assumption. They hold up better when they're designed around a few durable principles:

Customer-side flexibility

Don't force every buyer through the same payment behavior.Merchant-side consistency

Settlement, reporting, and treasury handling should stay simple even if the checkout options expand.Regional adaptability

The payment mix should be easy to localize without rebuilding your whole stack.Operational clarity

If finance and support teams can't explain where the money is and when it lands, the setup will become expensive to maintain.

The businesses that handle global payments well usually land on the same conclusion. Choice belongs at checkout. Simplicity belongs in settlement.

That's also why stable settlement models are getting more attention. If customers can pay by card or digital asset, but the business consistently receives a stable digital dollar balance, the merchant avoids a lot of the usual friction around FX, banking delays, and scattered payout schedules. For many online businesses, that's a significant upgrade.

If you want a cleaner way to offer customer payment choice without inheriting the usual payout mess, Suby is worth a look. It provides an API that lets businesses accept payments by card or crypto, supports native Discord and Telegram flows for subscriptions and paid access, and keeps the merchant side simple: users pay with cards, businesses receive USDC.