You've started accepting customers outside your home market. Revenue is up, but payments are turning into a weekly operations problem. One customer's card fails on renewal, another wants to pay from a local exchange balance, finance is matching payout records by hand, and your support team is answering “how can I pay?” more often than they should.

That's usually the moment stablecoins move from “interesting” to practical. For SaaS founders, the core question isn't whether stablecoins matter. It's which stablecoin belongs in your billing stack.

If you're comparing USDC and USDT for recurring SaaS payments, the obvious differences are only half the story. The harder part is deciding what helps you close revenue today without creating compliance and reconciliation pain later. Most guides stay too shallow on this topic. If you also sell physical or digital add-ons alongside software, this primer on how brands understand crypto payments for branded merch is useful because it shows the same customer-side friction from a different angle. For a SaaS-specific billing lens, it also helps to review billing models for SaaS teams before you lock in payment rails.

Table of Contents

- What USDC signals to a SaaS business

- What USDT signals to a SaaS business

- Why this choice is strategic

- Quick comparison table

- Stability and trust

- Global reach and liquidity

- Regulatory fit and long-term operating risk

- Technology and integration reality

- Choose USDC when finance scrutiny is part of the sale

- Choose USDT when payment access matters more than treasury presentation

- Support both only when your back office is ready

- A simple decision rule for SaaS founders

- The operating model that removes friction

- Four ways to use the same product

- Why this matters for finance operations

The SaaS Growth Problem Beyond Traditional Payments

A familiar pattern shows up when SaaS companies expand internationally. Sales signs customers faster than finance can support them. The product is global, but the payment stack still behaves like a domestic setup.

One team starts in the U.S. with card billing and does fine for a while. Then customers in Latin America ask to pay from exchange balances. A reseller in Southeast Asia wants to settle in stablecoins. An EU client asks questions about issuer transparency and treasury policy before procurement signs. Nothing is broken in isolation. The problem is that every new region adds one more payment exception.

What founders usually notice first

The first symptoms are commercial, not technical:

- Checkout friction: some buyers want to pay, but not by international card.

- Collections delays: finance waits on slower cross-border movement and manual follow-up.

- Renewal risk: subscription billing gets harder when customers prefer methods your stack doesn't support cleanly.

- Back-office drag: accounting spends time matching wallets, chains, and invoices instead of closing the month.

Stablecoins enter the conversation because they solve a real business problem. They let a customer pay in a dollar-denominated digital asset while you settle faster and with fewer banking dependencies.

You're not choosing a token for its own sake. You're choosing what kind of payment operations team you want to run.

For SaaS, that decision usually narrows to USDC or USDT. Both are designed to track the U.S. dollar. Both are widely used in crypto payments. But they serve different business needs. One tends to fit regulated and audit-sensitive workflows better. The other tends to fit global liquidity and customer familiarity better.

That's why USDC vs USDT for SaaS payments: which stablecoin should you accept? isn't a branding question or a market-cap trivia question. It's a decision about customer access, compliance posture, and how much operational complexity your team can absorb.

Understanding the Stablecoin Choice for SaaS

A founder launches stablecoin payments to close more international deals. Three months later, the main question is no longer whether customers will pay in crypto. It is which stablecoin the finance team can support without creating more exceptions, more reconciliation work, or more policy risk.

Stablecoins work as payment rails for SaaS, but they also become part of your billing operations, treasury workflow, and compliance posture. That is why the choice between USDC and USDT is strategic. It affects who can pay you, how easily your team can settle funds, and how exposed you are if processor rules or regional regulation change.

What USDC signals to a SaaS business

USDC tends to fit companies that expect scrutiny from finance, legal, procurement, or enterprise buyers. In practice, that usually means B2B SaaS selling into the U.S. or Europe, platforms with audited financials, or teams that want a payment asset that is easier to explain internally.

The business benefit is not only reputational. USDC usually creates fewer hard conversations with controllers, auditors, and banking partners because its positioning is closely tied to reserve transparency and regulated-market use. If your sales process already includes security reviews, vendor onboarding forms, or treasury questions, that difference shows up long before anyone asks about blockchain details.

USDC also gives you a cleaner base asset for teams that may later expand into stablecoin payout, treasury, or multi-entity settlement flows. The payment decision can lock in downstream operational costs.

What USDT signals to a SaaS business

USDT usually fits demand capture better than policy comfort. In many regions, it is the dollar stablecoin customers already hold and already know how to use. That reduces checkout hesitation and lowers the odds that a buyer drops off because they need to swap assets first.

That advantage is strongest for SaaS companies selling into markets where card acceptance is inconsistent, banking rails are slower, or crypto-native payment behavior is already common. In those cases, USDT can act as the collection asset that gets the invoice paid, even if your team prefers to settle or treasury in something else later.

USDT's strength is reach. Its trade-off is that some finance and compliance teams will treat it as the asset that needs more internal justification.

If you are still evaluating the operational setup, this guide on how businesses can accept crypto payments covers the implementation basics. Some customers also fund subscriptions through crypto cards that support USDT, which can influence how much direct wallet acceptance you need.

Why this choice is strategic

The visible difference is at checkout. The hidden difference is what happens after the payment lands.

Choose the wrong default and you may still collect revenue while making month-end close harder, limiting processor options, or forcing a migration later when a new market, auditor, or partner raises the bar. For SaaS, the better decision is usually the one that matches both your customer mix and your tolerance for operational overhead.

A useful way to frame it is simple:

- Collection fit: Which asset do target customers already hold and trust?

- Compliance fit: Which asset creates fewer issues with finance, legal, and counterparties?

- Settlement fit: Which asset is easier for your team to reconcile, convert, or retain?

- Future-fit: Which choice still works if you expand into stricter jurisdictions or larger accounts?

Founders often compare USDC and USDT as tokens. The better comparison is between operating models.

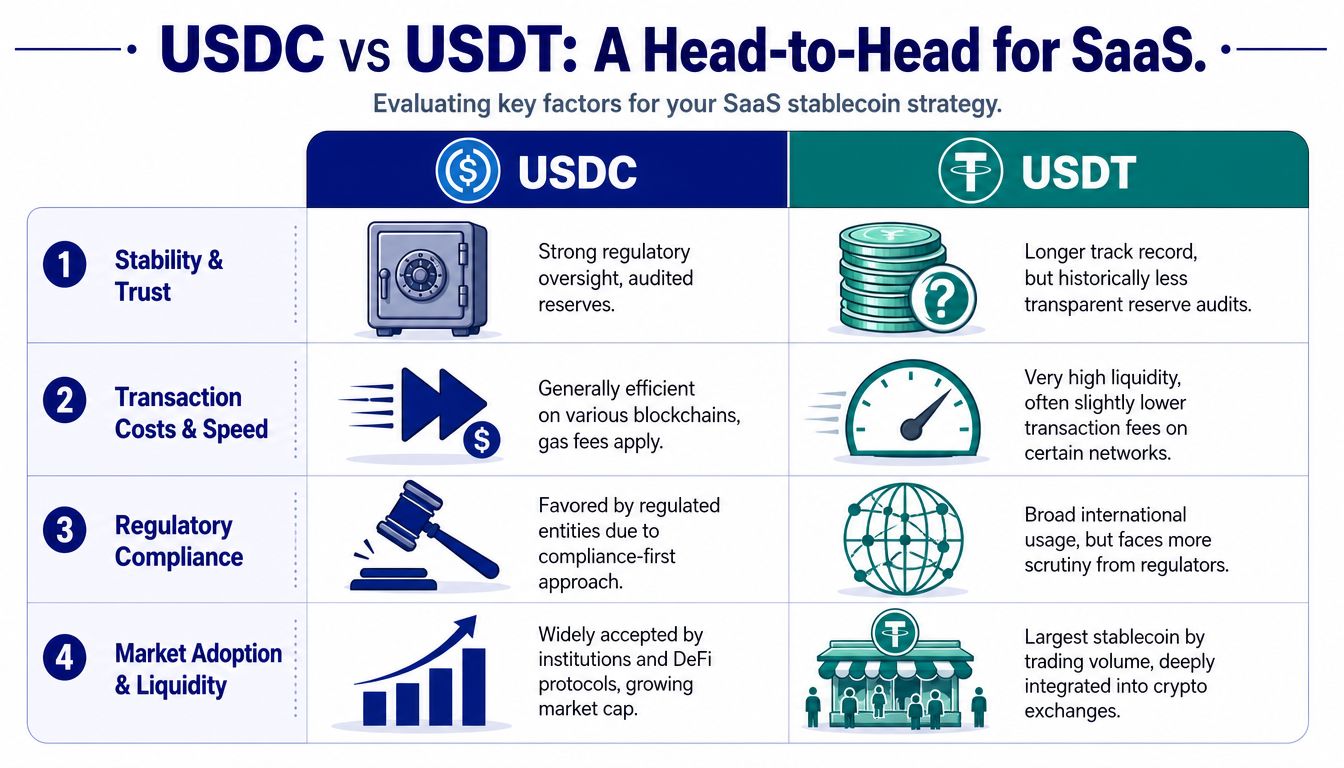

USDC vs USDT A Head-to-Head Comparison for SaaS

A founder in Berlin and a founder in Singapore can both ask, "Should we accept stablecoins?" and arrive at different answers for good reasons.

USDC is usually the safer default for SaaS companies that sell into compliance-heavy U.S. and EU environments. USDT is often the stronger collection asset when customers already hold it, move it often, and care more about liquidity than treasury policy. The right choice depends less on token branding and more on what your finance team, customers, and payment stack have to absorb after launch.

Quick comparison table

| Factor | USDC | USDT |

|---|---|---|

| Best fit | Regulated SaaS, U.S. and EU buyers, corporate treasury workflows | Global customer collection, emerging markets, crypto-native buyers |

| Compliance posture | Stronger fit for compliance-led environments | Weaker fit for compliance-gated jurisdictions |

| Market liquidity | Deep and institutionally favored | Largest global stablecoin liquidity footprint |

| Customer familiarity | High in regulated fintech and treasury contexts | Very high in global trading and cross-border crypto usage |

| Operational risk if used alone | Lower for regulated recurring billing | Higher where processor or jurisdiction rules may tighten |

| Best role in SaaS | Default settlement and billing asset for regulated flows | Acceptance asset where customer convenience is the priority |

Stability and trust

For SaaS, "trust" is not an abstract brand question. It shows up when a controller asks whether they can book recurring revenue cleanly, when a bank asks what sits behind incoming funds, or when an enterprise buyer routes your payment terms through procurement.

USDC generally creates fewer follow-up questions in those workflows. Its positioning around reserve transparency and attestations fits better with companies that already have internal controls, treasury policies, or external reporting requirements. If your average contract value is high and renewals pass through finance review, that difference has direct implications for close rates and operational effort.

USDT wins on a different axis. It remains the stablecoin many customers already use in global crypto markets, especially outside the U.S. and Western Europe. That makes it easier to collect from buyers who value speed, availability, and familiar rails over formal compliance framing.

A practical rule helps here. If sales calls regularly include legal, finance, or procurement, bias toward USDC. If growth depends on reducing payment friction for crypto-native users in multiple markets, USDT deserves serious consideration.

Global reach and liquidity

USDT is the more natural fit in many international collection flows because customers already hold it.

Analysts at Triple-A found that USDT leads stablecoin usage in both supply and transaction volume, and remains especially common in lower-value payment activity and cross-border usage. For self-serve SaaS, freelancer tools, trading software, and products selling into regions where local banking is less predictable, that translates into a simple commercial advantage: fewer customers need to swap assets before they can pay you.

That convenience can lift conversion. It can also increase support load if you accept USDT across several chains without a clean settlement policy.

I have seen teams underestimate that second part. A checkout page that says "we accept USDT" sounds straightforward. Key questions come later. Which networks do you support, how do you detect underpayments, what happens when a customer sends the right asset on the wrong chain, and who reconciles all of that at month-end?

If your users already spend through crypto cards that support USDT, that is another signal that USDT matches how they manage funds day to day.

If you are evaluating how those payment flows fit into recurring billing, this guide to choosing a crypto payment gateway for SaaS billing is a useful operational reference.

Regulatory fit and long-term operating risk

The hidden cost in this decision is not the first payment. It is the fifth renewal, the annual audit, or the processor review that happens after stablecoin volume becomes material.

USDC is usually easier to defend in regulated billing environments. Circle explains its reserve and compliance model in its USDC transparency and reserve materials. For SaaS teams selling to larger companies, that kind of documentation reduces internal debate. Finance teams can point to a clearer paper trail, and counterparties are less likely to treat the payment method as an exception case.

USDT can still work well for collections. The risk is concentration. If you build your recurring billing setup around USDT alone, you may create avoidable migration work later if a processor, banking partner, auditor, or regional compliance policy becomes less comfortable with that choice. That risk is higher for EU-focused or enterprise-heavy SaaS than for global self-serve products.

Many comparison articles stop too early. Founders do not just need to know which token is bigger or more popular. They need to know which choice is cheaper to operate over two years, after accounting for finance review, policy changes, accounting treatment, and settlement flexibility.

Technology and integration reality

The token decision is really a billing architecture decision.

USDC has become a common settlement asset for businesses because it is widely supported and often selected for treasury-oriented workflows. USDT's strength is different. It is present on the networks and venues many customers already use, which lowers payment friction at the edge.

For a SaaS operator, the expensive mistakes are rarely about blockchain mechanics alone. They come from fragmented wallet operations, inconsistent chain support, refund handling, and reconciliation exceptions across tokens and networks. Supporting both USDC and USDT can be smart, but only if your system normalizes incoming payments into one ledger and one reporting process.

Otherwise, dual acceptance creates operational drag. Finance has more exceptions to review. Support handles more payment tickets. Treasury has to decide what to retain, what to convert, and when.

That trade-off is worth making for some businesses. It is not worth making by default.

A good decision framework is simple:

- Choose USDC first if your SaaS sells to regulated businesses, larger companies, or buyers in markets where finance scrutiny is part of the sale.

- Choose USDT first if customer acquisition depends on meeting crypto-native users where they already hold funds.

- Accept both only if your payment stack can standardize collection, reconciliation, and settlement without adding manual work across teams.

Here's a useful walkthrough before you decide how much complexity to own directly:

Real-World Scenarios When to Choose USDC or USDT

A founder closes a customer in Germany, sends the invoice, and then finance asks a predictable question. Will this payment choice create extra review, treasury exceptions, or settlement risk later? That is the right question to ask.

The practical choice between USDC and USDT depends on where revenue comes from, who approves payment on the buyer side, and how much operational mess your team can absorb after the money arrives. Founders often frame this as a token comparison. In practice, it is an ops and risk decision.

Choose USDC when finance scrutiny is part of the sale

USDC fits SaaS companies selling into procurement-led environments. If buyers include U.S. companies, European businesses, fintechs, or larger organizations with finance controls, USDC is usually the safer default.

Use it for cases like these:

- Enterprise subscriptions with annual contracts, vendor onboarding, or legal review

- Products sold to regulated businesses that already have treasury or compliance requirements

- Higher-value invoices where payment method questions can slow approval

- Teams that want cleaner settlement policy internally for accounting, treasury, and audit review

The benefit is not just optics. It reduces friction in the parts of the deal that happen after the commercial yes. Finance teams are more likely to accept a payment rail they can document internally without extra explanation. That matters if your goal is to expand stablecoin acceptance without creating a recurring internal debate every quarter.

Choose USDT when payment access matters more than treasury presentation

USDT is often the better collection asset for self-serve or crypto-native SaaS. If your users already keep balances on exchanges, trade in stablecoins regularly, or operate in markets where USDT is the default dollar substitute, accepting it can improve conversion.

Typical use cases include:

- Lower-ticket subscriptions where ease of payment matters more than formal treasury review

- International SaaS sold to individuals or small businesses outside the U.S. and Western Europe

- Products with a strong crypto-native user base such as trading tools, analytics, bots, or community software

- Growth teams optimizing for completed checkout, especially where card acceptance is weak or expensive

In these cases, rejecting USDT on principle can cost revenue. Customers pay with what they already hold. If they need to swap assets first, some will drop before checkout is complete.

Support both only when your back office is ready

Accepting both can be the right move for SaaS companies serving two very different buyer groups. One segment wants USDC because finance cares. Another arrives with USDT because that is what sits in the wallet.

The hidden cost shows up after launch. Reconciliation gets harder across chains. Refunds need clearer rules. Treasury has to decide what stays on balance sheet, what gets converted, and how exceptions are handled. Support also gets dragged in when a customer sends the right token on the wrong network.

Support both only if these conditions are already true:

- Your customer base is distinctly split by geography, buyer type, or wallet behavior

- Your payment stack consolidates inflows into one ledger and one reporting process

- Your finance team has a written policy for settlement, conversion, refunds, and retained balances

If you do not have that infrastructure yet, one stablecoin is usually the better business decision.

A simple decision rule for SaaS founders

Choose USDC if the sale touches procurement, legal, or treasury review.

Choose USDT if the sale depends on meeting crypto-native customers where they already hold funds.

Accept both only if the added conversion benefit is worth the operational overhead across finance, support, and treasury.

That is the primary trade-off. The token choice affects checkout, but the larger cost sits in settlement operations and long-term risk management.

How Suby Simplifies Stablecoin Payments and Settlement

Most SaaS teams don't need another argument about tokens. They need payment infrastructure that lets customers pay however they want while finance receives money in a format the business can use.

That's where Suby fits. It's payment infrastructure for the global internet economy. Businesses can accept payments by card or crypto through an API, and it also offers native Discord and Telegram integrations for subscriptions, paid access, and online communities. The model is straightforward: customers pay any way they want, businesses get paid the way they choose. That can mean card, wallet, bank, or crypto on the customer side, and settlement to a bank account or in stablecoins like USDC on the business side. One important flow is customer pays by card, business receives USDC, but that's one option, not the only one. Suby also processes payments as a Merchant of Record facilitator, so it automatically handles tax compliance by location and payment processing while settling revenue directly into stablecoins like USDC to the merchant's wallet, according to Circle's partner profile for Suby.

The operating model that removes friction

The operational value is in abstraction. Your customer doesn't need to use the same payment method that your finance team wants to settle in.

That matters because the best customer collection asset and the best treasury asset are often not the same. A global SaaS company might want to accept card payments from one segment, crypto from another, and still standardize settlement into a single stablecoin or bank payout path.

Suby provides an API that lets developers integrate both card and crypto payments with a checkout flow that requires only five lines of code, supporting one-time payments and recurring subscriptions where customers can pay via credit card, wallet connect, or exchange deposit while the merchant receives funds in USDC, according to Suby's official site.

Four ways to use the same product

The useful way to think about it is as one product with four operating modes:

- Suby Payments: an API-first payment stack to accept cards and crypto through one checkout.

- Suby Crypto: a crypto payment gateway that handles the swap, sponsors the gas, and settles to a non-custodial wallet or to the Suby balance.

- Suby Gating: paid access for Discord, Telegram, downloads, and courses.

- Suby Invoicing: clients pay how they want while the business receives what it wants.

This matters for SaaS because the payment stack rarely stops at subscription checkout. Teams usually need links, invoices, recurring billing, community access, and payout flexibility in the same operating environment.

Why this matters for finance operations

The most overlooked cost in the USDC versus USDT debate is reconciliation. If you let customers pay in multiple ways but finance still gets one coherent settlement path, you avoid a lot of unnecessary cleanup.

That's why the “customer pays card, business receives USDC” flow is so practical. You preserve conversion on the front end and simplify treasury on the back end. The same principle applies if customers pay by wallet, bank, or crypto and the business wants bank settlement instead.

Two final points matter here:

- Pricing depends on payment method used, so there isn't one flat rate. Check Suby pricing for exact current figures.

- Native integrations exist for Discord and Telegram, which makes the product relevant beyond core SaaS checkout, especially for software businesses with paid communities or gated customer access.

If your main concern is not just acceptance, but settlement control, that architecture is often more important than which stablecoin sits in the customer's wallet.

Making Your Final Decision A Quick Checklist

A founder closes a customer on stablecoin billing, then discovers the underlying problem a month later. Finance is chasing payment confirmations across chains, sales is answering compliance questions mid-procurement, and the original coin choice now looks like an operations decision, not a checkout decision.

Use this checklist to make the call with those second-order costs in mind:

- Where are your customers based? USDC is usually the cleaner default for SaaS companies selling into the U.S. and Europe, especially if legal, finance, or procurement will review your payment setup. If a meaningful share of customers already holds and prefers USDT, forcing USDC can create avoidable payment friction.

- What kind of buyer are you selling to? Enterprise contracts usually reward a conservative choice with a clearer compliance posture. Self-serve and SMB motions often benefit more from accepting the asset customers already use.

- How do you want to settle revenue? Decide this before choosing what to accept. Some SaaS teams want bank settlement for payroll and taxes. Others want stablecoin balances for treasury, vendor payments, or global contractor payouts. The right acceptance setup follows that settlement requirement.

- Can your finance team reconcile this cleanly every month? Supporting both USDC and USDT can help conversion, but only if your ledger, billing, and reporting workflows normalize those inflows without manual cleanup. If they do not, payment flexibility on the front end becomes accounting overhead on the back end.

- How much regulatory and migration risk are you willing to carry? A stablecoin choice is easy to make and harder to unwind once customers are invoiced, subscriptions are live, and contracts reference a billing process. If you expect larger accounts, audits, or tighter policy review later, choose the option your business can still defend in two years.

- Do you need a single stablecoin policy? Many SaaS companies do better with a routing model. Let customers pay with the asset they prefer, then convert and settle into the currency or stablecoin your finance team wants to hold.

For most SaaS businesses, the practical default is straightforward. Use USDC if trust, procurement, and long-term compliance matter most. Accept USDT as well if your growth depends on regions and buyer segments where it is already the working dollar.

If you want a setup where customers can pay by card, wallet, bank, or crypto while your business settles to a bank account or in stablecoins like USDC, Suby is worth evaluating. It gives SaaS teams one API for card and crypto payments, supports recurring billing and invoicing, and includes native Discord and Telegram integrations for subscriptions, paid access, and online communities.