You start looking for a razorpay alternative when the payment stack that worked locally starts slowing down everything else.

At first, Razorpay often feels good enough. You can get checkout live, collect domestic payments, and keep the finance side simple. The problem shows up later, usually when you add overseas customers, remote contractors, subscription billing, or a second market that doesn't want to pay and settle the way your home market does.

Then the hidden work appears. Finance has to reconcile multiple currencies. Ops has to explain payout timing to the team. Product has to answer why a payment succeeded but usable cash still isn't available. Support gets dragged into disputes that are really settlement issues in disguise.

That isn't a small edge case anymore. The global payment gateway market was valued at USD 26.7 billion in 2024 and is projected to reach USD 48.4 billion by 2029, which tells you how quickly businesses are being pushed toward more scalable payment infrastructure (MarketsandMarkets payment gateway market report).

A useful comparison doesn't stop at feature checklists. It has to answer a harder question. When your customers are global, how much operational drag does each provider add after the payment goes through?

Table of Contents

- Look at total processing cost, not headline rates

- Treat settlement as a product decision

- Developer fit matters more than brochure features

- How difficult is it to migrate from Razorpay to a new payment provider

- What are the compliance and tax implications of receiving revenue in USDC

- Can I still serve customers who want to pay in their local currency

- Should I pick the gateway with the lowest listed fee

Why Your Business Needs a Razorpay Alternative

A lot of teams don't replace Razorpay because they dislike it. They replace it because the business changed.

The common failure point

The usual pattern looks like this. An India-first company starts selling software, services, or memberships to buyers outside India. Revenue grows, but the payment workflow gets messier instead of cleaner.

International acceptance comes with higher fees. Payout timing becomes less predictable. The team starts caring about foreign exchange spreads, settlement delays, and documentation because all three now affect cash flow.

Razorpay can still process payments in that setup. But for a global business, "can process" isn't the same as "fits the operating model."

A payment gateway stops being just a checkout tool once your finance and ops teams spend time working around it.

Why bank-centric infrastructure starts to hurt

Traditional gateways were built around bank rails first. That works reasonably well when your customers, settlement currency, and operating entity all sit in the same region. It gets clunky when they don't.

The friction shows up in a few places:

- Settlement mismatch: Customers may pay in one currency while your team needs working capital in another.

- Delay risk: Funds can be authorized today but only become usable after the bank cycle clears.

- Planning uncertainty: Revenue recognition may be straightforward, but treasury planning isn't.

- Cross-border overhead: You end up managing payment acceptance, conversion, and payout as separate problems.

A razorpay alternative becomes necessary when those costs are no longer occasional. They become part of the weekly workflow.

For builders, this matters because payments shape product decisions. Pricing, subscription design, support burden, and international rollout all depend on how fast and predictably money arrives. If your gateway adds friction every time you grow into a new market, it's not just a finance issue. It's a growth constraint.

Key Criteria for Evaluating Payment Gateways

If you're comparing providers, ignore the homepage pitch for a moment. The useful questions start after checkout succeeds.

Look at total processing cost, not headline rates

Advertised processing fees are only part of the bill. What matters is the effective cost of getting paid and being able to use that money.

Check these items closely:

- Card processing fees: Start with the posted rate, but don't stop there.

- FX conversion exposure: Hidden spreads matter because they reduce margin on international sales.

- Dispute handling: Actual cost includes the time your team spends investigating payment issues.

- Operational overhead: Manual reconciliation, payout tracing, and reporting work all belong in the calculation.

If you're reviewing pricing models, this breakdown of payment gateway pricing is a useful way to think beyond the sticker rate.

Treat settlement as a product decision

It is common for teams to treat settlement as a finance detail. That's a mistake.

A provider can have good checkout UX and still create back-office drag if payouts are slow or inconsistent. Traditional platforms often rely on bank payout cycles, which means the payment event and the spendable cash event are separate.

That affects:

- Cash flow planning

- Refund handling

- Vendor payments

- Subscription businesses that need predictable recurring revenue timing

Practical rule: If finance has to ask "when will this actually land?" more than once a week, settlement is part of your product stack, not just your payments stack.

Developer fit matters more than brochure features

Builders usually care about how quickly a system goes live and how reliably it behaves after launch.

Look for:

- API and webhook quality: You want clear event models, not guesswork.

- Checkout flexibility: Hosted pages, paylinks, and embedded checkout each solve different use cases.

- Subscription support: Recurring billing needs to work without fragile custom logic.

- Documentation quality: Teams move faster when the docs answer edge cases early.

Security belongs here too. If you're reviewing vendors, it helps to understand the basics of adherence to PCI DSS compliance so you know what the provider should handle and what still sits with your team.

A final filter is reach. Global coverage is useful, but only if it matches your customers' payment behavior and your own settlement needs. A broad acceptance footprint doesn't automatically solve payout friction.

Reviewing Traditional Global Alternatives

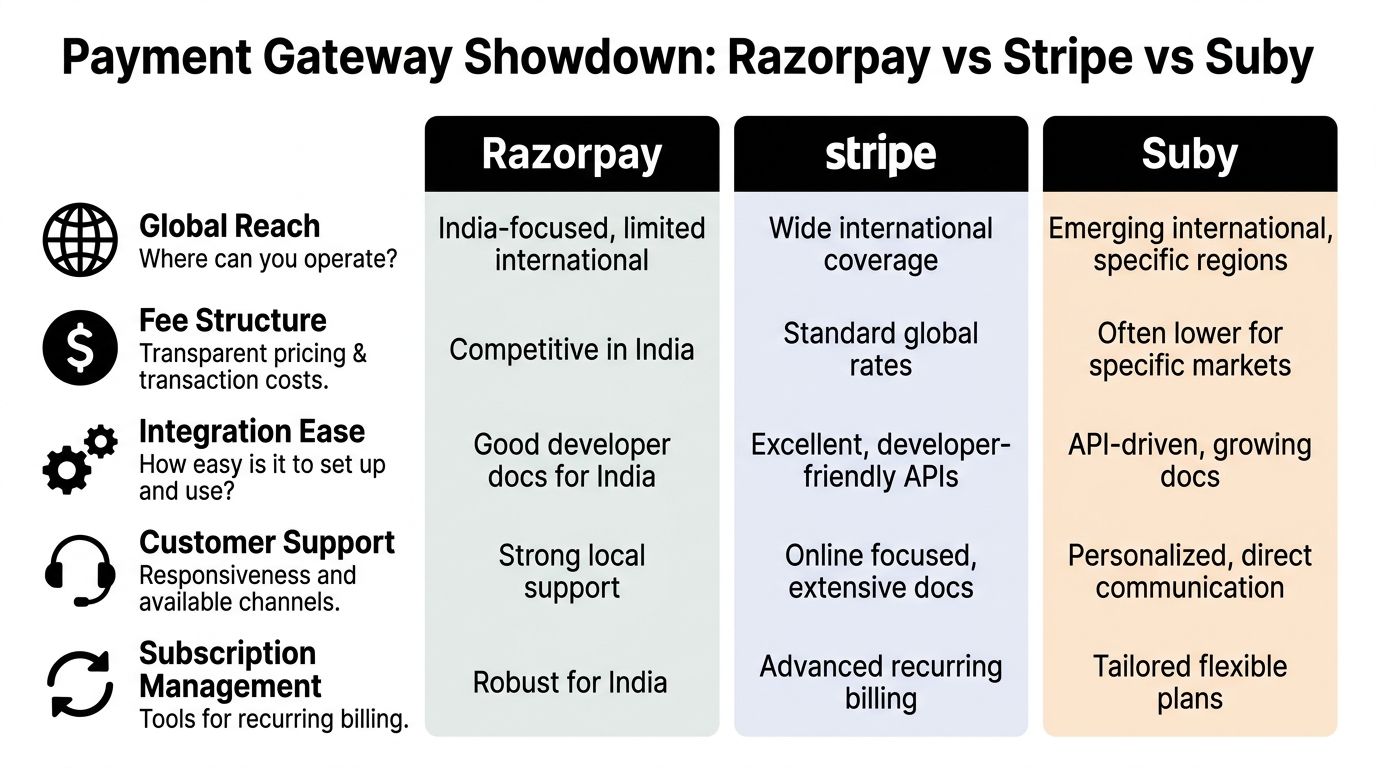

For many businesses searching for a razorpay alternative, the shortlist quickly narrows to PayPal and Stripe. That's rational. Both are mature, widely recognized, and easier to justify internally than a niche processor.

Early on, a quick comparison helps:

| Platform | Where it stands out | Main limitation for global operators |

|---|---|---|

| PayPal | Familiar buyer experience and broad international recognition | Settlement still follows traditional rails |

| Stripe | Strong developer tooling and broad payment support | Cross-border settlement still brings bank-cycle friction |

| Razorpay | Useful for India-centric operations | Regional focus becomes restrictive as expansion grows |

Where PayPal works well

PayPal is still one of the easiest names to explain to customers and finance teams. According to G2's Razorpay alternatives page, PayPal is rated 4.4/5 and supports payments in 200+ countries and 140+ currencies, which is why it stays near the top of so many shortlists.

That reach matters when you need a fast path into international selling. Buyers already know the brand. In some markets, that familiarity reduces hesitation at checkout.

It can also be a practical choice for:

- Freelancers and agencies billing overseas clients

- Small sellers that want simple cross-border acceptance

- Teams with limited engineering bandwidth

Its fee model is still important to read carefully. The verified range for PayPal is 2.29% to 4.99% plus fixed fees. That can be workable for some categories, but less attractive once volume grows or margin gets tighter.

Where Stripe works well

Stripe earns its place on the list for different reasons. It is more infrastructure-oriented.

The same G2 source lists Stripe at 4.4/5, and the broader comparison material around Razorpay alternatives highlights its strong international support. Stripe is usually the better fit when your product team wants programmable payments instead of just a checkout button.

In practice, Stripe is strong for:

- SaaS products with recurring billing needs

- Marketplaces that need more flexible money movement

- Developer-led teams that want powerful APIs

There's also a useful industry comparison on Adyen payment processing if you're weighing enterprise-style payment architecture against more developer-first systems.

Where both still create friction

The biggest issue isn't whether PayPal or Stripe can accept global payments. They can. The issue is what happens after acceptance.

Verified comparison data notes that Stripe often outperforms Razorpay on international capabilities, supporting 135+ currencies and intelligent routing, but both Stripe and Razorpay still rely on traditional settlement cycles, typically in the T+2 to T+7 day range, and both expose merchants to FX costs (Dodo Payments comparison of Razorpay and Stripe).

That leads to a practical trade-off:

- Strong acceptance layer

- Mature tooling

- Good ecosystem support

- But settlement still depends on legacy payout flows

If your problem is checkout conversion, traditional global gateways may be enough. If your problem is settlement certainty, they usually aren't.

Often, comparisons conclude prematurely. They score the gateway on APIs, plugins, and geography, then ignore the operational cost of waiting, converting, and reconciling. For an internet-native business, those aren't side issues. They're part of margin.

Suby A Modern Alternative Built for USDC Settlement

Most gateway comparisons stay inside the same design assumption. Customer pays by card, processor moves funds through banking rails, merchant waits for settlement, then deals with conversion and payout.

That model is familiar, but it isn't the only one.

What changes when settlement is native to USDC

A different approach is to separate how the customer pays from how the business receives funds.

Suby is one example of that model. It provides an API that lets businesses accept payments by card or crypto, while the business receives revenue in USDC. It also supports paylinks, embeddable checkout, recurring subscriptions, webhooks, and native integrations for Discord and Telegram use cases such as paid access and community memberships. Product details are documented on the official Suby website.

The practical difference is straightforward. Users can pay with cards, businesses receive USDC.

That matters because a large gap in the payment market still gets ignored. Verified market analysis notes that stablecoin-native settlement remains undercovered in gateway comparisons, even though stablecoin transaction volume surged 47% year over year to $10.8T in 2025, while traditional platforms still expose merchants to FX markups and bank delays (Xflow's Razorpay alternatives analysis).

For operators, the appeal isn't novelty. It's simpler money movement.

- No forced bank-first payout flow

- Less exposure to conversion spread

- Faster access to usable funds

- Cleaner global treasury handling

Who this model fits best

This setup isn't for every business.

If you're tied to domestic bank settlement, local acquirer relationships, and country-specific payout rules, a traditional provider may still fit better. The same is true for teams whose accounting stack assumes every payout lands through standard bank channels.

But stablecoin settlement solves real pain for internet-native businesses:

- Global SaaS teams charging customers across regions

- Agencies and freelancers who don't want revenue trapped behind payout timing

- Creators and community operators managing subscriptions and access in Discord or Telegram

- Online businesses that want one acceptance layer, even when customers pay with different methods

The key idea is simple. Card acceptance and crypto acceptance don't need to force the merchant into old payout infrastructure. If your business already operates globally, that separation can remove a lot of friction.

Razorpay vs Stripe vs Suby A Side-by-Side Comparison

A side-by-side view makes the trade-offs easier to see.

Payment Gateway Feature Comparison

| Feature | Razorpay | Stripe | Suby |

|---|---|---|---|

| Primary fit | India-first businesses | Global SaaS, marketplaces, developer-led teams | Global online businesses that want card or crypto acceptance with USDC settlement |

| International posture | Limited compared with broader global platforms | Strong international capability | Built around global internet-native payouts |

| Settlement model | Traditional payout flow | Traditional payout flow | USDC settlement |

| Currency and routing focus | Domestic-first with some international support | Strong multi-currency support and intelligent routing | Focus on reducing payout and FX friction rather than bank-based settlement |

| Subscription support | Available, especially for India-centric use cases | Advanced recurring billing | Supports recurring subscriptions |

| Integration options | Good for India-focused teams | Strong API-driven implementation | API, webhooks, paylinks, embedded checkout |

| Community monetization | Not a core differentiator | Not a core differentiator | Native Discord and Telegram integrations |

| Operational trade-off | Useful domestically, harder as cross-border complexity grows | Excellent tooling, but settlement still follows bank cycles | Different treasury model, better fit for teams comfortable receiving USDC |

A short walkthrough helps if you want to see the comparison in motion.

What the table means in practice

Razorpay is still a sensible tool if most of your customers, operations, and settlement needs stay close to India. The pain begins when cross-border revenue becomes a core part of the business instead of an occasional add-on.

Stripe is the stronger international system in the traditional gateway category. It has better reach, better routing, and better developer ergonomics for many use cases. If you want maximum flexibility within a bank-based settlement model, it's usually the cleaner choice.

But the decisive difference is settlement architecture.

When a business bills customers in multiple regions, the work doesn't end at authorization. Someone has to manage when funds arrive, in what form they arrive, and how much value gets lost in conversion and delay. Traditional providers improve acceptance. They don't fully remove that second layer of work.

Teams often compare gateways as if checkout is the whole product. For cross-border businesses, payout design matters just as much.

A stablecoin-settlement model changes the backend path. Customers still pay in familiar ways, but the merchant receives USDC instead of waiting for bank-driven payout handling. That can be a cleaner operating model for software businesses, agencies, and community-driven products that already work internationally by default.

The choice isn't really "which gateway has more features." It's "which money flow matches how the business operates."

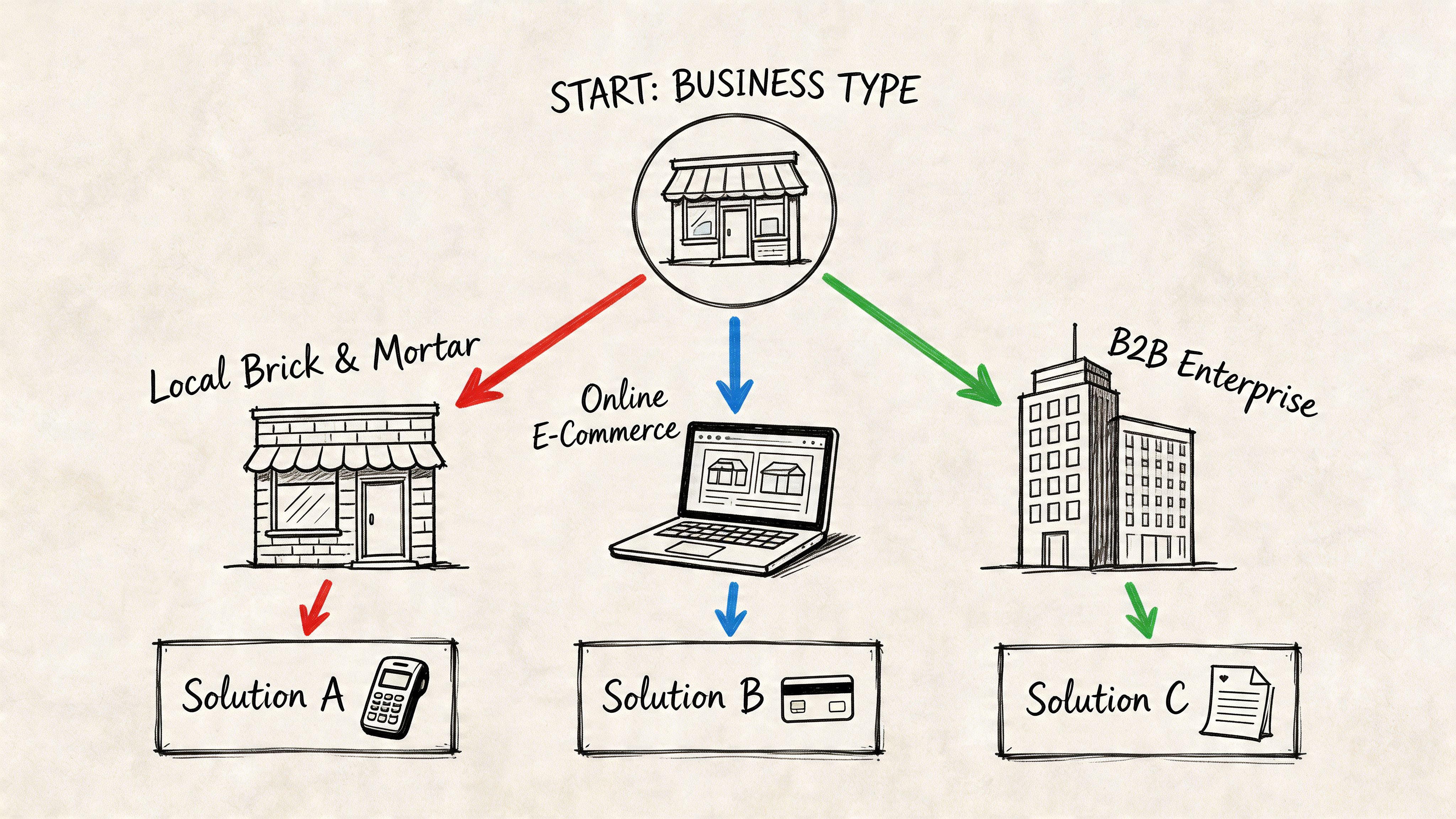

Which Payment Solution Is Right for You

There's no universal winner. The right razorpay alternative depends on where your friction lives.

Choose based on operating model

If you're mostly serving India and your finance team is comfortable with domestic settlement, Razorpay can still be enough. It doesn't solve every international edge case well, but not every business needs that.

If you're a larger software company or marketplace that wants broad global acceptance, mature APIs, and extensive billing tooling, Stripe is often the practical pick. It fits teams that can tolerate traditional payout timing and the extra finance work that comes with cross-border operations.

If your business is online-first and globally distributed from day one, the better fit may be a system built around direct digital settlement rather than bank-first settlement. That matters most for:

- SaaS companies with customers across regions

- Agencies and freelancers that want fewer payout surprises

- Creators and membership businesses selling recurring access

- Discord and Telegram communities that need payment and access control in one workflow

A simple decision rule

Use this as a filter:

- Choose Razorpay if domestic strength matters more than international flexibility.

- Choose Stripe if developer tooling and global card acceptance are the priority.

- Choose a USDC-settled model if your biggest pain is FX leakage, payout delay, and treasury uncertainty.

The mistake is choosing based only on who can process the payment. Most providers can. The better question is who leaves your team with the least manual work after the payment succeeds.

Frequently Asked Questions

How difficult is it to migrate from Razorpay to a new payment provider

Usually less difficult than teams expect. The hard parts are recurring billing migration, webhook rewiring, reconciliation updates, and customer communication. One-time payments are simpler. Subscriptions need more planning.

What are the compliance and tax implications of receiving revenue in USDC

That depends on your entity, accounting setup, and jurisdiction. Treat settlement currency as a finance and compliance decision, not just a product choice. Get your accountant or legal adviser involved before switching payout flows.

Can I still serve customers who want to pay in their local currency

Yes, in many setups the customer payment method and the merchant settlement method don't have to be the same. That's the key distinction many global businesses care about.

Should I pick the gateway with the lowest listed fee

Not by itself. The lowest visible fee can still lead to higher effective cost once you include FX spread, delay, disputes, and reconciliation work.

If your business sells globally and you'd rather let users pay with cards while your team receives USDC, Suby is worth evaluating. It's built for online businesses and creators that want card or crypto acceptance, recurring billing, API-based integration, and native Discord or Telegram monetization without relying on slow bank payout flows.