Gaspard LEZIN

A Guide to Adyen Payment Processing in 2026

Explore Adyen payment processing with our complete 2026 guide. Learn how its unified platform works, its fees, and how it compares to modern solutions.

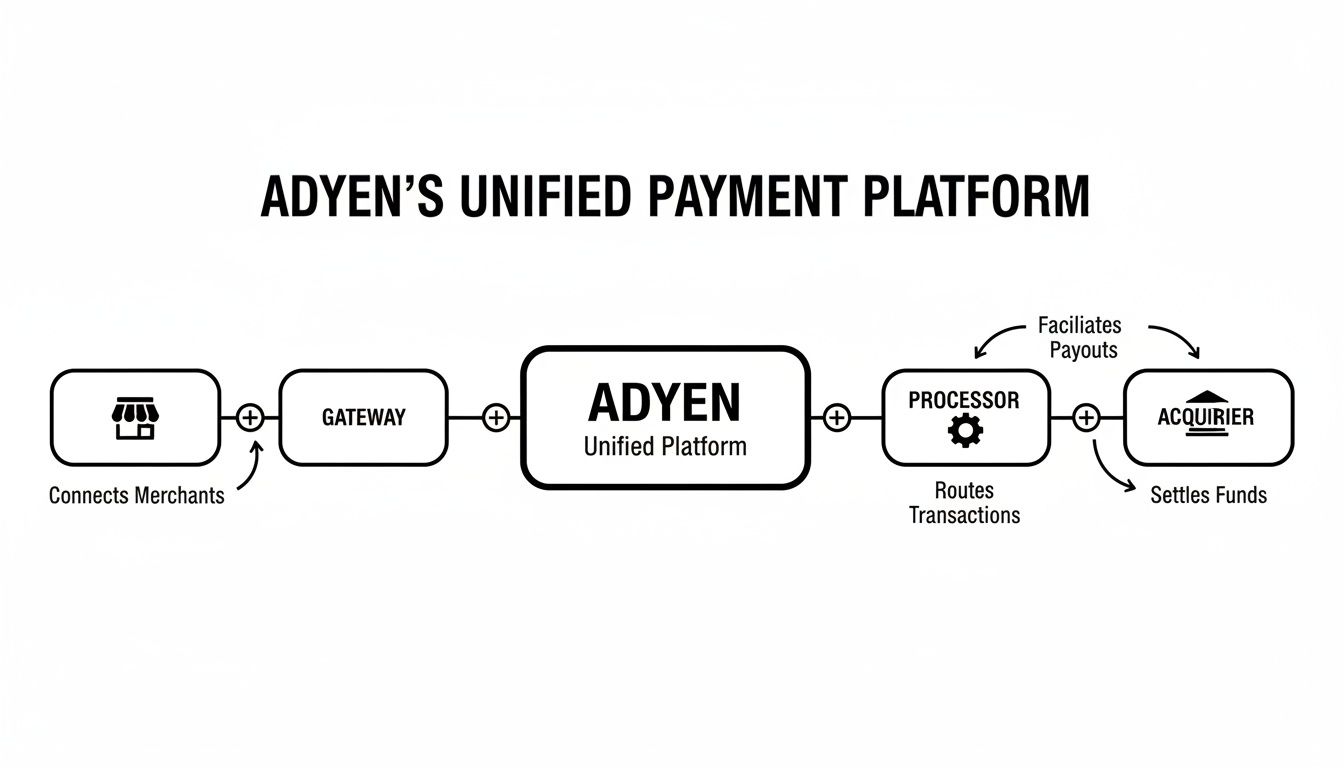

Adyen's platform is best understood as a single, unified system for everything related to payments. It rolls the functions of a payment gateway, a processor, and an acquiring bank into one cohesive platform. For businesses, this means you can manage every transaction, whether it happens online, in an app, or at a physical store, through a single partnership.

The Financial Control Tower for Global Business

Think about how messy international payments can get. Traditionally, you'd have one company acting as your payment gateway to capture the transaction, another to process it, and a collection of acquiring banks in different countries to actually settle the funds. It's a complicated web of vendors, contracts, and technical integrations that can quickly become a nightmare to manage.

Adyen was built to fix this specific problem. It acts as a single "control tower" for your global payments.

This is possible because Adyen operates on a full-stack infrastructure, meaning they built and own every piece of the payment flow. From the moment a customer hits "pay" to the final settlement in your bank account, Adyen is the only party involved.

To see what a difference this makes, let's compare the old way with Adyen's approach.

Adyen's Unified Platform At a Glance

Component | Traditional Model | Adyen's Unified Model |

|---|---|---|

Payment Gateway | A separate third-party vendor that captures payment details. | Built directly into the platform, capturing data from all channels. |

Payment Processor | Another vendor responsible for routing the transaction data. | Handled internally by Adyen's own processing engine. |

Acquiring Bank | A network of different banks required for each region you sell in. | Adyen holds its own banking licenses, acting as the acquirer globally. |

This integrated system isn't just about convenience; it fundamentally changes what's possible with your payment data.

Here’s what that really means for a business:

Simplified Operations: You're dealing with one partner, one contract, and one technical integration for all your payment needs worldwide.

Richer Customer Data: Since Adyen sees the entire transaction, it can connect the dots between online and in-store purchases, giving you a complete picture of customer behavior.

Effortless Global Expansion: Want to start selling in Japan and accept Konbini payments? You just enable it in your Adyen dashboard. There's no need to find and integrate a new local payment partner.

At its core, unified commerce is about breaking down the walls between your sales channels. Adyen's platform is designed to give you a single view of your customer, whether they shop online, on their phone, or in a physical store.

What This Means for Merchants

For a merchant on the ground, this unified model delivers some very real results. It leads to fewer failed payments because the platform has more data points to make smart routing decisions and retry transactions intelligently. It also allows your development team to move faster, since they're building on one consistent, global API instead of juggling multiple systems.

However, a platform this powerful comes with its own set of demands. It's truly built for large, global enterprises that have the engineering resources to handle a sophisticated integration. It's not a plug-and-play solution for most small or mid-sized businesses.

To really get what makes Adyen different, you have to look under the hood at its architecture. Most payment setups are a patchwork of different vendors cobbled together. Adyen threw that model out and built a single, unified system to handle the entire payment journey from start to finish.

This all-in-one approach is their secret sauce. It combines three key roles that are usually siloed: the payment gateway, the processor, and the acquirer. By owning the entire stack, Adyen gets a bird's-eye view of every transaction, which gives merchants a serious edge.

Let's unpack how these pieces fit together.

The Three Pillars of Adyen's Platform

Think of a traditional online payment. Your gateway talks to a processor, which talks to an acquirer, which finally talks to the customer's bank. It's like a game of telephone, and information gets lost at every step.

Adyen's model consolidates these into one fluid motion:

Payment Gateway: This is the front door. It’s what securely captures a customer's card details on your website, in your app, or at a point-of-sale terminal.

Risk Engine: Before the transaction goes any further, Adyen’s built-in risk tools screen it for fraud. Because it sees data across every channel and merchant, its system gets incredibly good at spotting shady patterns that a single-purpose tool might miss.

Acquiring: This is where Adyen truly breaks from the pack. As a licensed acquirer, it holds its own licenses and has direct connections to card networks like Visa and Mastercard. No more intermediaries, it speaks directly to the issuing banks.

This diagram shows how Adyen merges these distinct functions into one cohesive flow, cutting out the middlemen that complicate traditional payment processing.

As you can see, Adyen isn't just one piece of the puzzle; it built the whole thing.

Turning Data into Higher Authorization Rates

When you own the entire payment flow, you see everything. Every successful transaction, every decline, and every fraud attempt generates a wealth of data. Adyen puts this data to work with features like Adyen Uplift and Intelligent Payment Routing.

These aren't just fancy names. The system analyzes historical data in real time to make smarter routing decisions. For instance, if a specific bank is known to flag transactions from a certain country, Adyen can route it through a different acquiring connection where it has a higher chance of success. A failed payment isn't a dead end, it's a data point that helps the next transaction go through.

This is a world away from older systems where a "declined" message is the end of the story, costing you a sale and frustrating your customer.

The Power of Full-Stack Infrastructure

By handling the entire lifecycle, Adyen gains incredible control and visibility. In fact, its own vertically integrated infrastructure now handles 83% of its total transaction volume. This is what enables faster processing, better data, and a constant feedback loop to improve the system.

This data-driven optimization is what fuels Adyen’s key innovations. Their own reports show that features like Adyen Uplift can boost merchant authorization rates by up to 6%. You can explore the data yourself by reading Adyen's full report on its global processing volume.

This level of intelligent optimization is practically impossible when you’re juggling a separate gateway, processor, and acquirer. The data is too fragmented, and no single party sees the full picture.

Of course, Adyen is built for large, complex enterprises. For businesses looking for a more nimble way to handle global payments, modern alternatives have emerged. For example, Suby offers an API that lets any business accept card or crypto payments. Customers can pay with their cards, and businesses receive payouts in USDC. It’s a compelling model for SaaS companies and creators, especially with its native integrations for Discord and Telegram.

Practical Benefits of End-to-End Control

So, what does all this technical jargon actually mean for your business? It boils down to a few tangible benefits that hit your bottom line.

Higher Authorization Rates: Smart routing means fewer false declines and more approved payments. It’s that simple.

Deeper Data Insights: With a single source of truth, you get a unified view of your customers, whether they buy online, in-store, or in-app.

Reduced Operational Complexity: One contract, one integration, and one reconciliation process. You’re managing a single relationship instead of three or more, which frees up huge amounts of time and resources.

Ultimately, this unified approach gives global businesses the tools to not just process payments, but to optimize them for growth.

Accepting Payments with Global and Local Methods

If you want to sell globally, you have to think locally. It's a simple truth that goes far beyond just accepting major credit cards. A shopper in Amsterdam fully expects to see iDEAL at checkout, while a customer in Brazil might see a missing PIX option as a dealbreaker and abandon their cart. This is where Adyen's entire philosophy really comes into focus: global reach built on deep local expertise.

For merchants, this means you can cater to all these local preferences without the nightmare of managing dozens of separate integrations. The real magic of Adyen is the ability to flip a switch and activate these local payment methods on demand, all from one platform. This flexibility lets you tailor your checkout to each market, which builds immediate trust and can dramatically boost your conversion rates.

The Power of Direct Acquiring Licenses

So, how do they pull this off? A huge piece of the puzzle is Adyen's status as a direct acquiring bank in key regions all over the world. Many payment processors are just middlemen; they rely on a patchwork of third-party banks to actually process transactions. Adyen, by contrast, holds its own licenses, allowing it to talk directly to the card networks (like Visa and Mastercard) and the customer's bank.

Think of it like flying direct versus taking a route with multiple layovers. The direct flight is faster, cheaper, and has fewer chances for your luggage to get lost. For a business, this translates to tangible benefits:

Higher Approval Rates: A direct line of communication means cleaner data and less risk of a transaction being mistakenly declined. Fewer intermediaries equals fewer points of failure.

Lower Costs: By cutting out the middlemen, Adyen can offer more competitive pricing. You're not paying layered fees that stack up when multiple providers each take a cut.

Faster Settlement: Direct connections streamline the entire payment lifecycle, getting funds from authorization to your bank account more quickly.

This direct model is fundamental to how Adyen serves large, international companies. It offers a level of control and efficiency that's almost impossible to match with a fragmented system of partners.

Global Reach Backed by Data

The numbers speak for themselves. Adyen is a payments giant, with deep roots in Europe contributing 56% of its revenue, it’s no surprise they are a top gateway choice in markets like Germany. North America is another stronghold, accounting for 25% of revenue. With support for over 100 payment types across more than 60 countries and new licenses in markets like India and Mexico, Adyen's network is constantly expanding. You can get a better sense of Adyen’s place in the market by exploring a detailed competitive analysis.

The core idea is simple but powerful: meet customers where they are. Offering a familiar payment method is one of the strongest signals of trust you can send to an international buyer, demonstrating that you understand and cater to their local market.

But for many modern internet businesses, accepting local currencies is only half the battle. The real friction often comes from managing cross-border payouts, converting dozens of currencies and wrestling with traditional banking delays. While Adyen is a master of acceptance, this settlement side can still be a headache.

This is where a different approach can be a game-changer. Our platform, Suby, provides a simple API for any business to accept payments by card or crypto. Here’s the crucial difference: while your customers pay with their card, you, the business owner, receive every single payment settled as USDC. This model completely eliminates currency conversion friction and banking delays, making it a perfect fit for global SaaS companies, creators, and online communities. We even offer native integrations for platforms like Discord and Telegram to make paid access and subscriptions easy.

Understanding Adyen's Fees and Settlement

When you're looking at any payment processor, it all boils down to two fundamental questions: "How much will this cost me?" and "How (and when) do I get my money?" With Adyen, the answers are refreshingly clear, thanks to its pricing model and the way it handles settlements. Getting a handle on these two areas is crucial to understanding the real value of their platform.

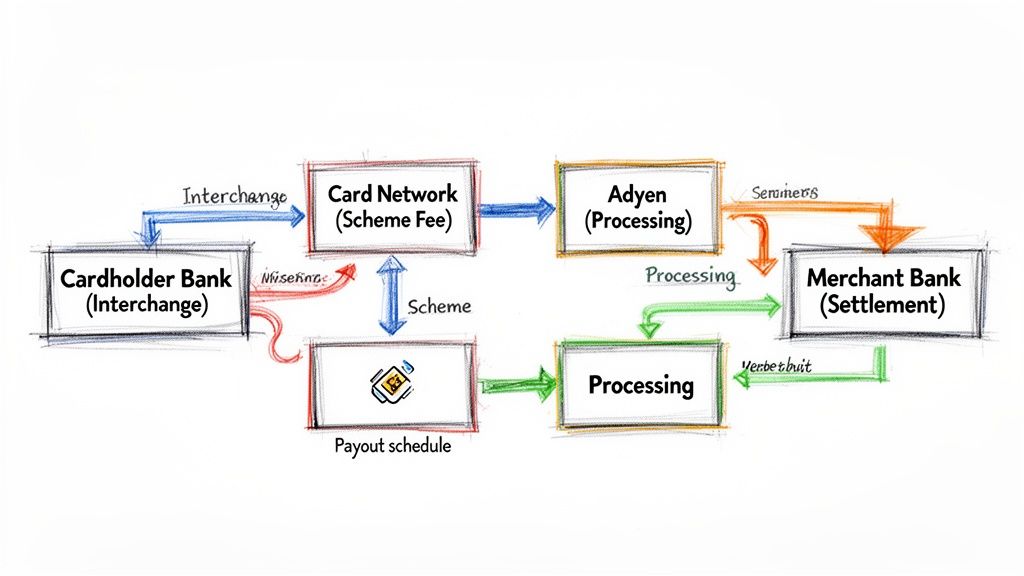

Unlike many competitors who favor a simple-but-often-expensive flat rate, Adyen champions a model called Interchange++. Think of it as an itemized receipt for every single card transaction. You see exactly what you're paying for, which is a level of transparency that large, detail-oriented businesses love.

Breaking Down the Interchange++ Model

So, what’s with the two "pluses"? Each one represents a separate cost component for every transaction you process through networks like Visa or Mastercard.

Interchange Fee (+): This is the main chunk of the cost. It’s a fee that goes straight to the customer's card-issuing bank. Essentially, it's the bank's compensation for taking on the risk and facilitating the payment. The card networks (Visa, Mastercard, etc.) set these rates, and they can change based on the card type (a basic debit card vs. a premium corporate card), the country, and how the transaction was made.

Scheme Fee (+): This is a much smaller fee paid directly to the card network itself, think Visa or Mastercard. It’s their fee for letting you use their payment infrastructure, the "rails" that connect all the banks and processors around the world.

Adyen's Processing Fee: This is what Adyen charges for its part in the process. It's typically a small, fixed fee plus a tiny percentage of the transaction amount. For example, in the US, Adyen’s pricing for Visa and Mastercard is simply their markup added on top of the interchange and scheme fees. This is what pays for their technology, acquiring license, and all the features on their platform.

This model is a world away from "blended" pricing, where you're quoted a single rate like 2.9% + $0.30 for everything. While blended rates seem simple, they hide the true costs. With that model, your low-cost debit card transactions are often subsidizing your more expensive corporate card transactions. Interchange++ rips off the band-aid and shows you everything.

The Settlement and Payout Process

Getting paid with Adyen is designed to be straightforward. Because Adyen processes everything through its single platform, it can collect all your funds in one place before paying you out. This is a game-changer for reconciliation.

Here's the typical flow:

Fund Consolidation: Adyen gathers all the money from your successful sales, no matter the payment method or original currency.

Currency Conversion: If you’re selling in multiple currencies, Adyen automatically converts them into your preferred payout currency (e.g., USD, EUR).

Payout to Your Bank: On a set schedule, Adyen wires the total collected amount, minus their fees, directly to your business bank account.

The real magic of Adyen's unified system is how it simplifies your accounting. You’re not trying to match up deposits from five different processors for ten different countries. Instead, you get one payout and one detailed report that breaks it all down: sales, fees, and settlements.

Even with Adyen's help, relying on the traditional banking system for payouts has its own headaches, especially for global businesses. You're still at the mercy of bank holidays, slow wire transfers, and unpredictable currency conversion markups from your bank.

This is where alternative settlement rails come in. Our platform, Suby, for example, offers an API that lets you accept card or crypto payments. But here's the key difference: regardless of how your customer pays, you, the merchant, receive your funds settled instantly as USDC in your digital wallet. This completely bypasses the delays and costs of the old-school banking system. For businesses wanting to make their global revenue more predictable, we wrote a guide on innovations in cross-border payments.

Integration Options and Modern Alternatives

Getting Adyen up and running isn't a simple plug-and-play exercise. Let's be clear: integrating a platform this powerful is a serious project, typically reserved for large enterprises that have dedicated development teams on standby. Adyen provides an impressive toolkit for connecting your business to its global payment engine, giving you immense flexibility for building sophisticated, custom payment flows.

At the heart of it all are Adyen’s extensive APIs and SDKs. These are the tools that give your developers granular control over every pixel of the checkout experience, every risk management rule, and every piece of data that flows back into your systems. For a business with complex e-commerce logic or one that needs to unify online and in-person payment data, that level of control is non-negotiable.

Adyen’s Technical Integration Paths

Adyen offers a few different ways to connect, each representing a trade-off between how much control you have and how much development work is required.

API Integration: This is the deep-end-of-the-pool option. You get full, raw access to build a payment flow from scratch. It's the right choice for businesses that want to own the entire user interface and orchestrate complex payment logic themselves.

Web Drop-in & Components: Think of these as pre-built, customizable Lego blocks for your checkout. They handle the sensitive work of collecting payment details, which simplifies your PCI compliance, but you can still style them to match your brand. It’s a smart middle ground.

Hosted Payment Page (HPP): This is the fast track. Adyen hosts the entire payment page for you, dramatically reducing your PCI compliance burden. The trade-off? You have very little control over the look and feel of the customer's experience.

While these options are robust, they all demand a significant technical investment. For a lot of modern internet businesses, especially those that need to be nimble, a more streamlined approach is often a better fit.

A Modern Alternative for Internet Businesses

While Adyen is busy serving global giants, a new wave of payment solutions has emerged for businesses that value speed, simplicity, and cash flow above all else. These platforms are built for the new economy of SaaS companies, online creators, and global e-commerce brands that can't afford to be bogged down by a massive engineering project.

Our platform, Suby, was designed for exactly this purpose. We provide an API that allows any business to accept payments by card or crypto. Your customers get a smooth, familiar checkout, but your revenue settles directly into your digital wallet as USDC.

This model completely sidesteps the delays and headaches of the traditional banking system, like sluggish cross-border transfers and unpredictable currency conversion fees. Creators weighing this against a membership platform often want to know what percent Patreon takes once its platform and processing cuts are layered together.

The core idea is to combine a conventional payment experience for customers with a modern, efficient settlement process for businesses. Users pay with their card, and businesses receive stablecoin payouts, simplifying global commerce.

With Suby, merchants can create shareable payment links in seconds, embed a checkout optimized for conversions, or build a custom integration using our straightforward API and webhooks. Customers can pay with Visa or Mastercard, or use crypto assets like USDC, USDT, ETH, SOL, and BNB. No matter how they pay, the merchant gets paid in USDC directly to their wallet.

This is particularly useful for businesses built around online communities. With native integrations for Discord and Telegram, Suby handles subscription management and access control automatically. This lets creators focus on creating great content instead of wrestling with payment admin. If you want to see how the technical side works, check out our guide on payment gateway API integration.

Of course, Adyen and Suby are just two options. It's always a good idea to explore broader strategies and other platforms by mastering how to collect payments from customers for your specific business. The right choice ultimately comes down to your business model, your technical resources, and your priorities for growth.

Diving into Adyen: Your Questions Answered

So, you’re looking into Adyen. It's a massive platform with a lot of moving parts, and it’s completely normal to have questions. Let's get straight to the point and tackle some of the most common things people want to know.

Who Is Adyen Really For?

Let's be clear: Adyen is built for the big players. Think large, global enterprises that are juggling massive transaction volumes and complex sales operations. Their sweet spot is a multinational company that needs to process payments across different countries and channels, online, in-app, and in their physical stores.

These are the kinds of businesses that can really put Adyen's unified platform and direct acquiring licenses to work. They typically have in-house engineering teams ready to dig into a sophisticated API and need the kind of granular data and control that only an all-in-one system can provide.

If you're a smaller business, a startup, or don't have a team of developers on standby, Adyen's high processing minimums and the sheer complexity of integration can be a real roadblock.

What's Adyen's Killer Feature Compared to Competitors?

Adyen’s biggest trump card is its single, unified technology platform. Most competitors stitch together services from different partners, a separate gateway, processor, and acquirer. Adyen built everything from the ground up, all under one roof.

This all-in-one design delivers three massive wins:

Insanely Rich Data: Because they control the entire transaction from start to finish, you get a complete picture of customer spending across all your channels.

Higher Authorization Rates: The system uses all that data to make smarter routing decisions, which means more approved payments and fewer frustrating false declines.

Operational Sanity: You're dealing with one contract, one integration, and one reconciliation process for your entire global payments operation. This is a game-changer for finance and tech teams.

How Does Adyen’s Pricing Actually Work?

Adyen uses a transparent pricing model called Interchange++. It’s different from the simple, blended rates you might see elsewhere. Instead, they break down the cost of every single transaction into its three core components:

Interchange Fee: This is the fee that goes directly to the customer's bank.

Scheme Fee: This fee goes to the card network, like Visa or Mastercard.

Adyen's Fee: This is Adyen's cut for processing the payment and providing their acquiring services.

While this model can feel more complex upfront, it gives you total transparency. For big businesses with high transaction volumes, it almost always ends up being more cost-effective than a flat-rate fee structure.

What Are the Real Benefits of "Unified Commerce"?

Unified commerce is all about erasing the lines between how and where a customer shops. Adyen’s platform is designed to connect the dots between your online store, mobile app, and physical locations.

For a business, this opens up some powerful possibilities. You can finally recognize the customer who bought a pair of shoes online and is now returning them in-store. Or you can create a loyalty program where points earned in the app can be spent at a retail kiosk. It gives you that elusive single view of the customer, which is pure gold for marketing, customer service, and business strategy.

Is Adyen a Good Choice for Taking Payments Internationally?

Absolutely. In fact, handling international payments is one of Adyen's greatest strengths. A huge part of this is their direct acquiring licenses in key regions and their massive library of local payment methods.

The scale here is hard to overstate. In just the second half of 2023, Adyen processed around 12 billion payment transactions across the globe. They're the engine behind giants like Spotify, Uber, and Microsoft, supporting over 250 payment methods in 187 currencies. If you're an enterprise going global, their infrastructure is tough to beat. You can explore more data on Adyen's impressive global transaction growth on ElectroIQ.

The bottom line is that Adyen’s unified platform is engineered to tame the complexity of global commerce for large-scale businesses. By consolidating technology, data, and reconciliation, it offers a level of control and insight that a patchwork of different systems just can’t provide.

But even with Adyen, the underlying traditional banking system can create friction. Modern internet businesses still have to deal with wire transfer delays and currency conversion costs.

This is where a different approach can make a lot more sense. Our platform, for instance, uses a simple API that lets businesses accept payments by card or crypto. The key difference? Your customers pay however they want, but you receive all your revenue settled directly as USDC to a digital wallet. This is perfect for global SaaS companies, creators, and online communities that need fast, predictable cash flow without the usual banking headaches.

Suby is a payment gateway and payment processor. Your customers pay with card, bank transfer, Apple Pay, Google Pay, Klarna, and more, or stablecoins, and you get paid out to your bank account, or directly in stablecoins (USDC, EURC) to your wallet, anywhere in the world, no bank account required. Where enterprise-grade Adyen payment processing is built for global giants with dedicated engineering teams, Suby gives lean SaaS companies, creators, and online communities the same global card acceptance with fast, predictable settlement and no traditional banking delays.