You've got customers in places you've never visited, but your payment stack still acts like you're a local business with a single bank account and a single market. That mismatch shows up fast. A customer's card works in one country and fails in another. A payout lands later than expected. Finance starts asking why revenue is leaking in conversion, fees, and reconciliation time.

That's the point where many software founders start looking for a platform for selling software worldwide without local entities. Most advice stops at two options. Either open local entities and absorb the admin burden, or hand everything to a merchant of record. In practice, there's a third path that matters for lean internet businesses. Keep checkout familiar for buyers, accept cards and crypto, and settle revenue directly in USDC so you're not waiting on old banking rails to catch up.

Table of Contents

- Selling Software Globally Is Broken

- The Modern Way to Sell Worldwide Without Local Entities

- Start with settlement, not checkout

- What to verify before you commit

- Choose the integration path that matches the sale

- Map the full flow before launch

- Treat subscriptions and access as the same system

- How do I handle taxes if I'm not registered in every country?

- Can I really sell software worldwide without local entities?

- Why does receiving USDC matter so much?

- Is receiving revenue in USDC secure?

- What kind of business is this model best for?

- What should I set up first?

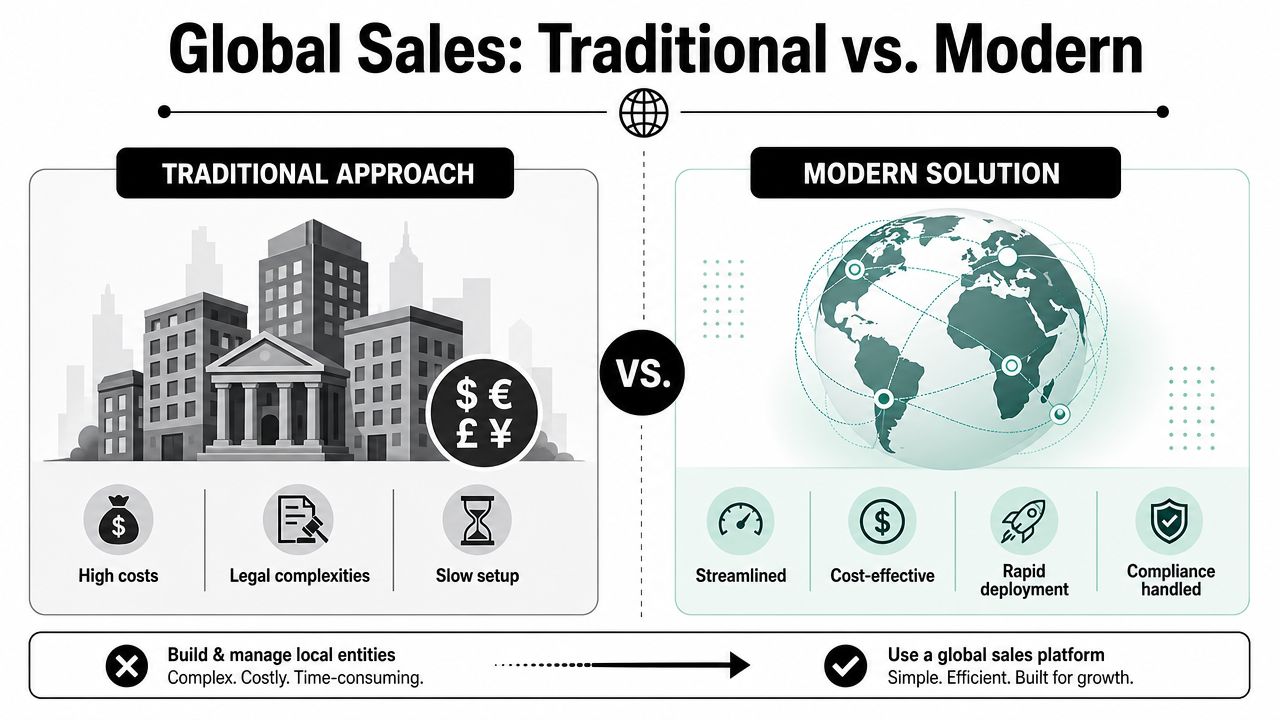

Selling Software Globally Is Broken

A founder in Brazil buys your software at 2 p.m. A customer in Germany renews overnight. A team in Singapore upgrades before you wake up. Sales happen globally from day one, but the money path still runs through payout schedules, banking cutoffs, currency conversion, and reconciliation work that has nothing to do with building product.

That mismatch is the problem.

Software delivery is already global. Finance operations usually are not. You can ship access instantly, but getting paid in a form your business can use often depends on old cross-border banking rails. Cards may clear at checkout, yet settlement shows up late, net of fees, and in a currency that creates more accounting work on arrival.

For lean software teams, this creates a strange operating model. Growth looks international on the front end and painfully local on the back end. One processor handles checkout, another system handles tax records, the bank handles settlement on its own timeline, and finance has to reconcile the gaps manually.

The primary bottleneck is often finance operations.

Founders often assume the issue is checkout conversion. In practice, the harder problem is what happens after the customer pays. Revenue gets trapped between processors, correspondent banks, payout windows, and local restrictions. That is why many teams end up comparing merchant-of-record options first. If you want that route, this breakdown of the best merchant of record options for SaaS companies is a useful starting point, and this explanation of how MoR reduces risk for global SaaS covers the trade-offs well.

There is still a gap most MoR versus self-hosted guides miss. The bigger operational question is settlement. If your business is remote, global, and intentionally lean, you do not just need a way to charge cards. You need a payment layer that lets customers pay normally while your company settles into an asset that moves globally without waiting on a stack of local banking relationships.

That is where a USDC-native model changes the equation. With Suby, the checkout can stay familiar for the buyer, but settlement does not have to pass through the same slow banking path that creates delays, conversion loss, and reconciliation pain. Revenue lands in USDC, which gives operators a cleaner base for treasury, contractor payments, and cross-border cash movement.

The old model forces software companies to add legal and banking infrastructure before they have proof that a market is worth the overhead. A USDC-native layer supports a third path. Sell globally, keep operations centralized, and avoid building country-by-country finance infrastructure too early.

For a software business, that is a meaningful difference. It reduces operational drag, shortens the distance between sale and usable funds, and lets the team spend time on product and distribution instead of cross-border payment cleanup.

The Modern Way to Sell Worldwide Without Local Entities

A founder closes a sale in Germany on Monday, invoices a customer in Singapore on Tuesday, and by Friday is still waiting to learn when the money will clear, what fees were taken, and whether another bank document is now required. That is the core problem with selling software globally. Demand can be global from day one. Finance operations usually are not.

The old playbook assumed expansion started with legal structure. Pick a country, form an entity, open bank accounts, line up local compliance, then begin selling. For software, that sequence is often too heavy and too early. It pushes teams to build country-specific finance infrastructure before they know whether a market will produce enough revenue to justify it.

Analysts and expansion advisors have made the same point for years. Local-entity entry is slow, paperwork-heavy, and expensive enough that many software companies delay market entry or keep it narrow until they have more certainty. Agility PR makes that case clearly in this global expansion guidance. The practical takeaway is simple. Test demand first. Add legal structure later, once the economics are proven.

A quick comparison shows where the burden sits:

| Model | What you take on | What slows you down |

|---|---|---|

| Local entity route | Incorporation, banking, compliance, local operations | Setup cost, legal overhead, slow launch |

| Global platform route | Product, pricing, customer experience | Vendor selection, integration, operational design |

That comparison still misses one important layer. Merchant-of-record platforms reduce a lot of front-end complexity, especially around tax, seller liability, and regional compliance. Founders evaluating that path should understand how MoR reduces risk for global SaaS, because the trade-off is real. You give up some control in exchange for less legal and operational burden.

The third option is more interesting for lean internet-native teams. Use a global payment layer that keeps checkout familiar for the buyer but changes settlement for the merchant. Instead of routing every payout through the same banking stack that creates delays, FX loss, and reconciliation work, revenue settles in USDC. That changes daily operations more than generally anticipated.

This is the operational difference that many MoR versus self-hosted guides skip. Buyers care that the card works. Operators care when funds arrive, what currency they arrive in, how predictable the payout is, and how easily that revenue can be used for treasury, contractors, vendors, and internal reporting. If checkout is modern but settlement still depends on fragmented bank rails, the hardest part of global sales is still there.

Suby is a concrete example of that model. The customer can pay through familiar methods, while the business settles in USDC and keeps finance operations centralized. For a remote software company, that means fewer banking dependencies, faster access to usable funds, and a cleaner path for cross-border cash movement. It is a different operating model, not just a different checkout provider.

If you are comparing structures, this overview of merchant of record options for SaaS is a useful reference point. A key decision is not only who handles tax and compliance. It is whether your payout system still forces you back into the same old banking bottlenecks.

The practical rule is straightforward. Start with the lightest structure that lets you sell compliantly, measure conversion and payment behavior by market, and keep settlement simple. Add local entities when there is a clear reason to do it, not as the default first step.

How to Choose Your Global Sales Platform

A lot of teams evaluate payment platforms from the front end in. They compare checkout widgets, payment methods, and subscription toggles first. That's understandable, but it misses the bigger operational question.

If you're selling internationally, the quality of your settlement system matters more than the beauty of your checkout.

Start with settlement, not checkout

The key decision isn't just payment acceptance. It's settlement predictability. For many business models, receiving revenue directly in USDC can materially outperform conventional cross-border payouts once you account for FX spreads, payout delays, and treasury operations, as discussed in FastSpring's perspective on selling software online.

That changes the evaluation order. Before you compare design or APIs, ask these questions:

- What do customers pay with? Card support matters because buyers want a familiar flow.

- What do you receive? If your payout path ends in bank delays, you haven't removed the hard part.

- How consistent is settlement? Predictability matters more than headline acceptance.

- Can you support recurring revenue cleanly? Subscriptions break fast when billing and settlement live in separate systems.

The platform I'd look for supports card and crypto acceptance, then settles merchant revenue in USDC. That model is especially useful for internet-native teams with distributed contractors, global expenses, or treasury needs that don't map cleanly to one local bank account.

What to verify before you commit

Don't rely on feature pages alone. Check the operating details.

Here's the shortlist I use:

- Settlement format: If the platform says users pay by card and businesses receive USDC, verify that in the docs and product pages.

- Recurring billing: Make sure subscriptions are native, not bolted on.

- Integration range: Look for paylinks, embedded checkout, API access, and webhooks.

- Fee clarity: Hidden cross-border costs usually show up outside the headline fee.

- Operational visibility: You need a dashboard for payments, subscriptions, and payouts.

- Community use cases: If you monetize access, Discord and Telegram support can remove a lot of manual work.

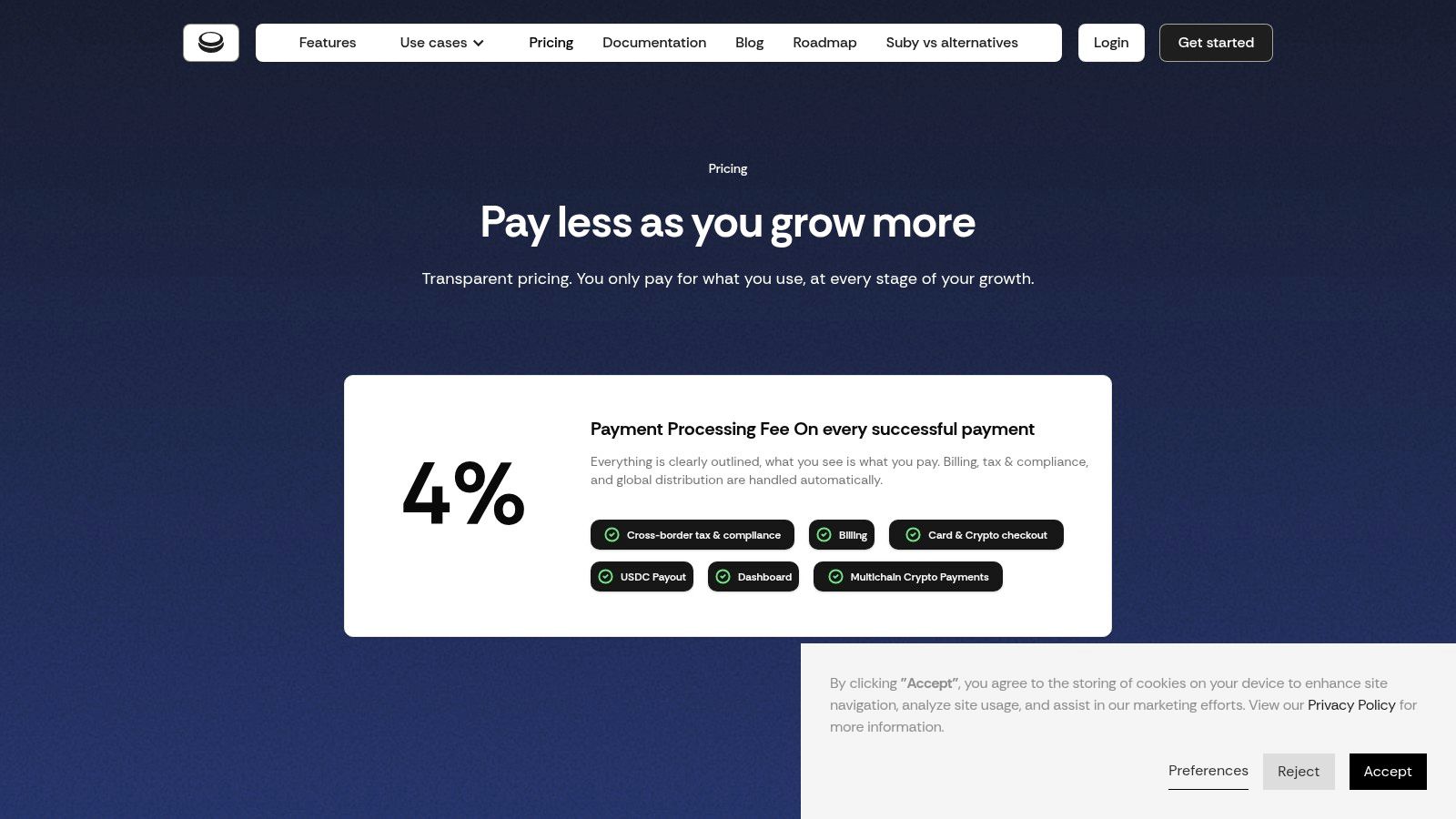

One example in this category is Suby. It provides an API that lets businesses accept payments by card or crypto, supports one-time payments and recurring subscriptions, offers paylinks and embedded checkout, and settles merchant revenue in USDC. It also includes native Discord and Telegram integrations for subscriptions, paid access, and online communities. The core operating model is simple: users pay with cards, businesses receive USDC.

A simple decision table helps keep this grounded:

| Evaluation area | Weak fit | Strong fit |

|---|---|---|

| Buyer experience | Limited methods, awkward checkout | Familiar card flow, clean checkout |

| Merchant settlement | Bank-dependent, delayed, unclear | Direct, predictable USDC settlement |

| Integration options | One rigid path | Paylinks, embed, API, webhooks |

| Business model support | One-time only | One-time plus subscriptions |

| Access monetization | Separate tools required | Native community integrations |

If you're lean, global, and trying to avoid banking friction, don't pick the platform that merely helps you charge cards. Pick the one that makes revenue operationally usable the moment the transaction is complete.

Your Integration Blueprint From Checkout to Settlement

A founder in Brazil launches on Monday, closes a customer in Germany on Tuesday, and wants usable revenue by Wednesday. That is where the integration decision stops being a product question and becomes an operations question. If checkout is easy but settlement still depends on bank rails, manual reconciliation, or payout delays, the stack is only half-built.

The practical goal is simple. Let buyers pay in the way they already expect, then settle revenue in USDC so the business can use it immediately across borders. That third model sits between classic merchant-of-record setups and fully self-built finance ops. For lean software teams, it removes a lot of the banking friction without forcing a heavy implementation.

Choose the integration path that matches the sale

Start with the lightest setup that fits the product and the way customers buy.

Paylinks work for direct sales. I use them when the deal starts in email, DMs, or a sales call and speed matters more than a custom frontend. They fit consulting offers, private betas, annual plans sold manually, and one-off invoices.

Embedded checkout fits most SaaS launches. The buyer stays on your site, the engineering lift stays low, and you still get a branded purchase flow that feels normal for card payments.

API-first integration makes sense when billing drives product behavior. Use it if payment should provision an account, assign a plan, trigger entitlements, revoke access after failed renewal, or feed internal reporting.

The common mistake is overbuilding too early. A custom billing system feels attractive until the team is also dealing with retries, refunds, failed renewals, tax edge cases, and payout visibility. For digital products with instant delivery, one connected payment layer is usually easier to run than a stack of separate processors, webhook glue, and bank payout workflows.

Map the full flow before launch

Write the payment flow twice. Once from the buyer's perspective. Once from the operator's perspective.

For the buyer, the path should be short and familiar:

- Select the product or subscription.

- Open checkout on-site or through a paylink.

- Pay by card or crypto.

- Get confirmation and access.

For the business, the sequence needs more precision:

- Payment is authorized and recorded.

- The order and subscription state are updated.

- Access, provisioning, or fulfillment is triggered.

- Revenue settles in USDC.

- Webhooks, dashboards, and internal records show the same final state.

If the team cannot explain that flow clearly, support issues show up fast.

I have seen the same failure pattern repeatedly. Payment goes through, but access does not. A refund is issued, but the subscription stays active. Funds arrive, but finance cannot tie the payout to the customer or product sold. None of these problems start at checkout. They start in the gap between checkout and settlement.

For teams that want stronger reconciliation or internal classification around payment events, a transaction identification API can help map transaction data back to your own customer and product logic.

Treat subscriptions and access as the same system

Recurring revenue exposes weak infrastructure faster than one-time sales. The billing event and the product event need to stay in sync.

That means connecting a few specific things:

- Subscription state and entitlements: paid, trialing, past due, canceled

- Customer communications: receipts, renewal notices, failed payment alerts

- Settlement visibility: confirmed revenue landing in USDC without waiting on bank payout cycles

- Webhook coverage: provisioning, deprovisioning, reporting, and support actions

This matters even more for products where payment controls access directly, such as Discord memberships, Telegram communities, templates, data products, or private software portals. In those cases, billing is part of product infrastructure.

Suby is useful here because the operating model stays straightforward. Buyers can pay with familiar methods, while the business receives USDC and can wire payment status into product logic through paylinks, embedded checkout, subscriptions, and webhooks. This global payment API for internet businesses shows the architecture well.

A good blueprint keeps the purchase experience familiar and the back office predictable. Customers pay normally. The company gets revenue it can use without waiting on a banking workaround.

Building Your Operational Playbook for Global Sales

Launching is the easy part. Running the system every day is where the quality of a global sales setup is demonstrated.

A lot of founders worry that selling without local entities means giving up control. In practice, the opposite can happen. If the platform is designed well, you get more visibility because payments, subscriptions, refunds, and payouts live in one operating layer instead of scattered tools.

Control risk without rebuilding finance ops

One of the hardest questions in cross-border software sales is how to manage tax, compliance, and legal risk cleanly when you're not opening local entities. That question matters more than most glossy payment pages admit. Valueleaf frames it well in its discussion of global expansion without setting up an office. The important point is clarity around who the seller of record is, how tax obligations are handled, and how buyer-facing simplicity is preserved.

That means your operational playbook should cover these areas early:

- Seller-of-record clarity: Know who is legally selling the product to the end customer.

- Refund handling: Make sure your team knows who can issue refunds and how that affects subscription state.

- Dispute process: Understand the evidence flow and internal owner before the first chargeback appears.

- Authentication and account security: Strong customer authentication and two-factor authentication should be part of the baseline.

- Payment security: A PCI-DSS Level 1 certified processing partner reduces exposure compared with rolling your own sensitive payment flow.

There's also a practical policy side to this. Decide in advance how your team handles refunds, account cancellation, failed renewals, and access revocation. If those decisions are improvised ticket by ticket, operations get messy fast.

Keep a short internal runbook. Who approves refunds, who handles disputes, who watches subscription failures, and who owns payout reconciliation.

Run the business from one dashboard

The fastest way to lose control is to split reporting across processor dashboards, bank statements, spreadsheets, and manual wallet checks. Global sales don't need more data sources. They need one operating view.

The dashboard should answer a few questions immediately:

| Question | Why it matters |

|---|---|

| What was paid today? | Revenue tracking and support verification |

| Which subscriptions renewed or failed? | Retention and access control |

| What was refunded or disputed? | Risk and customer ops |

| What settled out? | Treasury visibility |

| Where are churn signals appearing? | Product and pricing decisions |

For software teams, this is the difference between managing a system and reacting to one. If payouts, subscriptions, and payment events are visible in real time, finance and support can work from the same source of truth.

A lean global model only works if the back office stays lean too. That means fewer banking dependencies, fewer manual reconciliations, and fewer hidden status changes between checkout and settlement.

Frequently Asked Questions About Selling Globally

How do I handle taxes if I'm not registered in every country?

You still need to understand your own company's obligations in its home jurisdiction. But for buyer-facing transaction handling, many businesses use platforms that take on seller-of-record and tax workflow responsibilities in the sales layer. The key is to know exactly who is responsible for what before you launch in a market.

Can I really sell software worldwide without local entities?

Yes, in many cases that's the point of the model. Software can be delivered instantly online, and modern platforms exist to support cross-border checkout, licensing, invoicing, and subscriptions without requiring country-by-country physical infrastructure. The practical question isn't whether it's possible. It's whether your chosen setup handles settlement, compliance, and support cleanly enough for your business.

Why does receiving USDC matter so much?

Because card acceptance alone doesn't fix payout friction. If customers can pay easily but your revenue still moves through delayed banking rails, you haven't solved the operational problem. Receiving USDC creates a more predictable settlement path for businesses that operate internationally and want to avoid FX and bank-transfer uncertainty.

Is receiving revenue in USDC secure?

Security depends on both the payment platform and how you manage the wallet receiving funds. Teams that want direct control usually prefer a wallet setup they control themselves, along with clear internal policies for access, approvals, and treasury handling.

What kind of business is this model best for?

It fits digital businesses that can deliver value immediately online. SaaS is an obvious fit, but so are downloadable products, agencies billing international clients, digital memberships, and paid Discord or Telegram communities.

What should I set up first?

Start with checkout, subscription logic, and payout flow. Then test the full path with a small number of live transactions before scaling traffic. The businesses that do this well treat the payment system like product infrastructure, not just a finance plugin.

If you want a practical setup where customers can pay with cards and your business receives USDC, Suby is built for that model. It provides an API for card and crypto payments, supports one-time payments and subscriptions, and includes native Discord and Telegram integrations for paid access and online communities. For lean global teams, that's a direct way to sell internationally without adding local banking and entity overhead too early.