A customer is ready to buy. They've already decided the product is worth it, clicked the button, and landed on checkout. Then the form asks for card details, billing address, shipping address, phone number, and maybe another verification step before payment even starts.

That's where many businesses lose momentum. Not because the offer is weak, but because the checkout asks for too much work at the worst possible moment.

One click payment exists to remove that friction for returning customers. It turns a repeat purchase into a near-instant action, which matters even more when your buyers are on mobile, buying across borders, or paying for something they want access to right away. For internet businesses, that speed affects more than convenience. It affects completed sales, repeat purchases, and how easy it is to sell globally while keeping settlement predictable. In practical setups today, users pay with cards, and businesses can receive USDC.

Table of Contents

Why Faster Checkouts Matter for Global Business

A slow checkout doesn't just annoy customers. It breaks intent.

Consider a buyer who sees your product on Instagram, opens the link on their phone, and decides to pay during a commute or between meetings. If checkout feels long, they'll often postpone it. Many never come back. The problem gets worse when you sell internationally, because cross-border buying already carries uncertainty around payment success, card acceptance, and trust.

For the business, this shows up in very ordinary ways. More abandoned carts. More support messages asking whether another payment option exists. More lost repeat orders because coming back to buy again still feels like starting from zero.

Checkout friction often hides in small details

A payment flow doesn't have to look broken to underperform. It can be technically correct and still create hesitation.

Common friction points include:

- Too much typing: Long forms are a poor fit for mobile shoppers.

- Repeated information: Returning customers don't want to enter the same card details again.

- Weak continuity: A buyer who already trusts you expects the second purchase to feel easier than the first.

- Global complexity: Different regions, issuers, and payment rules can make an already long checkout feel even less predictable.

If you're reviewing your own flow, these Exclusive Addons for Elementor checkout tips are useful because they focus on reducing unnecessary fields and making checkout clearer for buyers.

The checkout page is where product demand either converts into revenue or leaks away through avoidable effort.

The business case for one click payment is straightforward. If a repeat customer already completed an earlier purchase and agreed to store their payment details, the second purchase shouldn't require another full form. A shorter path helps the buyer act while intent is still high.

That matters for stores, SaaS products, agencies sending payment links, and creators selling access to paid communities. In all of those cases, speed at checkout changes whether the customer completes the purchase now or drops off and forgets.

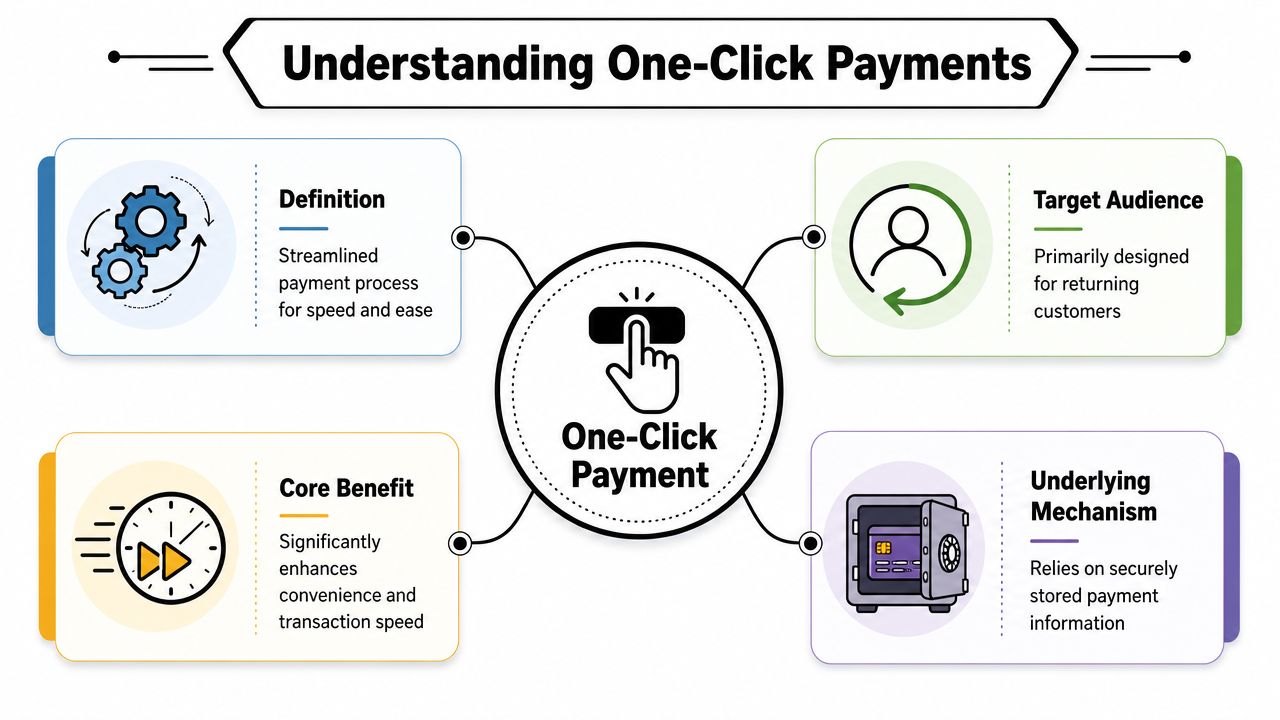

Understanding One-Click Payment

One click payment is a checkout method that lets a returning customer complete a purchase with a single click or tap by reusing stored, tokenized payment credentials instead of re-entering card details, as described in Tagada's glossary of one-click payments. The same source notes that this usually depends on a prior authenticated transaction where card-on-file consent was captured, which is why it works best for repeat customers rather than first-time buyers.

The simplest way to think about it

Think of it as a digital express lane. The first time a customer buys, they go through the normal checkout and approve the stored payment setup. After that, future purchases can skip most of the heavy lifting.

That's the point many readers miss. One click payment doesn't mean “payment with no prior setup.” It means “payment with no repeat data entry after setup.”

A simple comparison helps:

| Checkout type | What the customer does | Best for |

|---|---|---|

| Standard checkout | Enters card details and other information manually | First-time buyers |

| One click payment | Confirms a purchase using previously stored credentials | Returning customers |

This model emerged from the broader shift from manual card entry to tokenization and stored credentials, also noted in the Tagada reference above. That shift matters because online commerce changed where people buy, and mobile-first shopping made long forms much more painful.

Why it matters more on mobile

Typing a full card number, address, and security details on a phone is annoying. It's even worse when the customer is distracted, using poor connectivity, or trying to complete a fast repeat purchase.

That's why one click payment is closely tied to convenience. It shortens the path from “I want this” to “I bought this.”

If you want a complementary look at the wider checkout category, CartBoss has a helpful explainer on what is express checkout and how it differs from longer payment flows.

Practical rule: One click payment is strongest when the buyer already trusts the merchant and wants to repeat a familiar purchase with minimal effort.

For businesses, the value isn't abstract. Faster repeat checkout supports smoother reorders, easier upgrades, and less friction around paid access. For customers, it feels like the business remembered them and removed unnecessary work. That's what good payment UX should do.

How One-Click Payments Work Technically

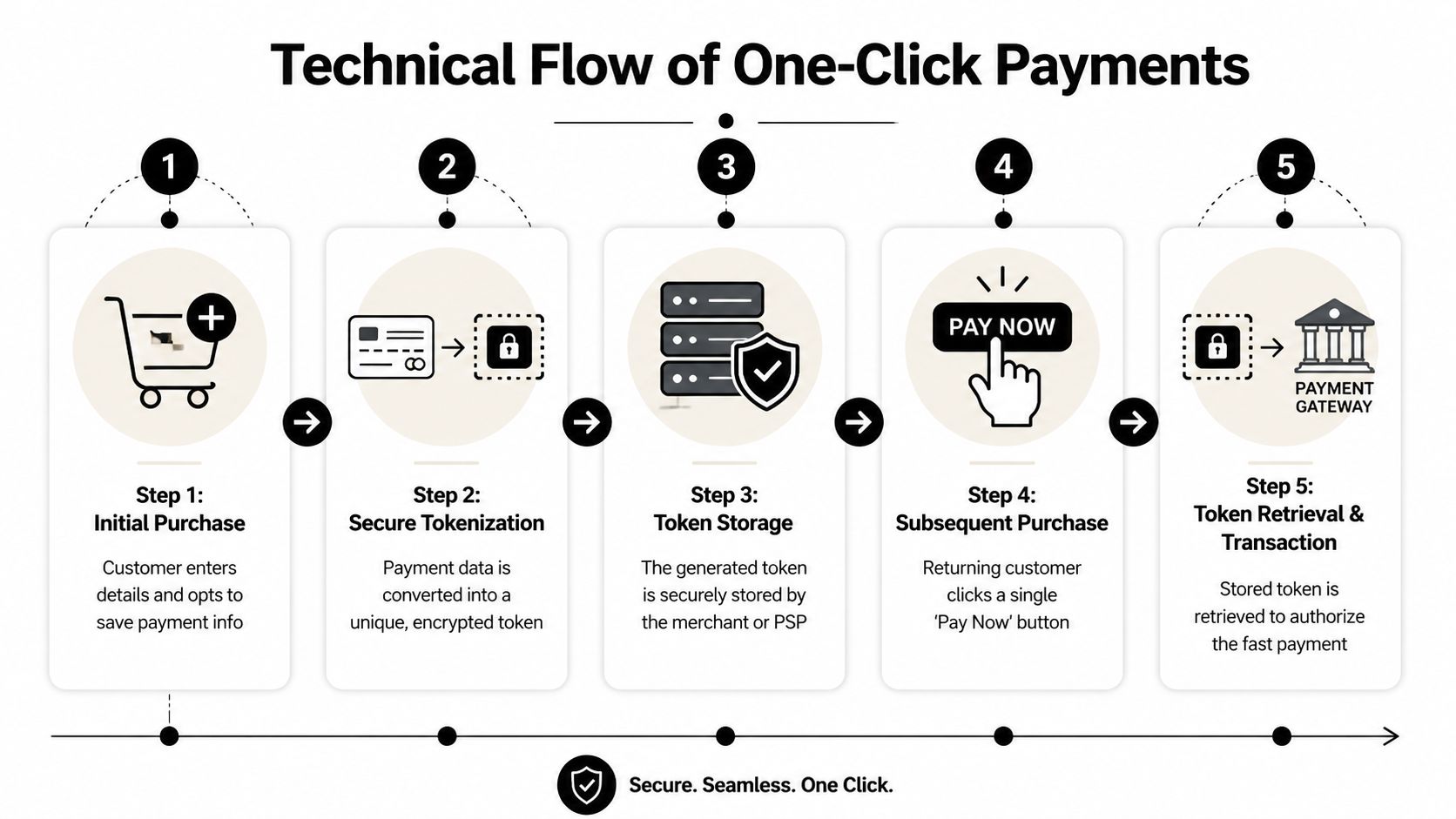

One click payment can sound mysterious from the outside, but the underlying model is fairly practical. It's a card-on-file flow. According to Stripe's overview of one-click payments, the customer completes an initial checkout where payment details are authorized and stored, and later purchases use those stored credentials with a single click or tap.

That setup reduces form-entry friction because previously saved billing information can be reused instead of asking for card data every time. The primary checkout gain comes from collapsing a multi-field process into a tokenized return-customer flow.

It starts with the first purchase

The first transaction still matters. That's where the customer enters payment details, completes authentication when required, and agrees to save the payment method for future use.

After that, the merchant or payment processor can recognize the returning customer and present a much shorter payment action.

The three moving parts

Teams typically only need to understand three core components:

Tokenization

The actual card data isn't meant to be reused directly in raw form. The system replaces sensitive card information with a token that represents it securely in later transactions.Saved credentials

The payment method becomes a stored card-on-file instrument tied to prior customer consent. That's what makes repeat checkout possible without repeating the full form.Authentication logic

Some transactions may stay almost invisible to the user. Others may still trigger checks, depending on processor rules, card status, or market requirements.

The result is simple from the customer's perspective. They click once. Behind the scenes, the payment stack identifies the stored method, retrieves the right token or reference, and submits the authorization request.

Here's a plain-language version of the flow:

- First purchase: The customer enters card details and approves storage for later use.

- Secure storage process: The processor stores the reusable payment reference safely.

- Return visit: The customer comes back already recognized in the payment flow.

- Fast checkout action: Instead of retyping everything, they confirm and pay.

For teams planning implementation work, this developers' guide to API integration is a useful outside reference because it frames the operational side of payment integration clearly. If you want a more product-specific look at implementation patterns, this payment gateway API integration guide covers how API-based payment flows are usually wired into a business app.

What developers usually need to plan for

The main product questions aren't about whether one click is possible. They're about where it should appear and when it should fall back to a fuller flow.

A team usually needs to define:

- Who qualifies as returning: Logged-in users, recognized customers, or buyers coming through a recurring payment flow.

- What gets reused: Payment credentials, billing information, or both.

- When extra steps appear: Expired cards, unusual risk signals, or required verification can interrupt the fast path.

The best implementations treat one click payment as a smart shortcut, not a rigid rule. If the customer can move quickly, let them. If the transaction needs another verification step, handle it without making the whole system feel broken.

Security and Compliance in One-Click Payments

Security is the first objection many businesses raise. That's reasonable. Saving payment details sounds riskier than asking customers to type them each time.

In practice, properly implemented one click payment usually moves risk away from the merchant's own systems. Industry guidance from Segpay's one-click payment developer documentation notes that these flows generally rely on tokenization and PCI-compliant storage rather than merchants holding raw card numbers themselves. The same guidance says the first transaction is where consent to store details is obtained, and it also notes a technical constraint: one-click payments are not universally supported across all payment types, such as direct debit or crypto.

Why stored payments can be safer than manual handling

The important distinction is this: a business should not be trying to store raw card data itself unless it has the compliance structure to do so. Most shouldn't.

A better pattern is to let a compliant processor handle the sensitive layer while the business works with tokens, customer references, and payment status events. That reduces the merchant's direct exposure to highly sensitive payment data.

A clean model usually looks like this:

| Security question | Safer approach |

|---|---|

| Where is the card data kept | With a PCI-compliant payment processor |

| What does the business store | References, tokens, and customer payment metadata |

| When is consent captured | During the first payment setup or initial checkout |

Convenience doesn't require weaker controls. It requires smarter separation between customer-facing speed and back-end handling of sensitive data.

If you're evaluating operational responsibilities in more detail, this PCI compliance requirements guide is a useful reference for understanding what merchants should and should not own directly.

Where businesses get tripped up

Problems usually start when teams misunderstand what one click payment includes.

Common mistakes include:

- Treating every payment type the same: Card-on-file logic doesn't automatically map to every rail.

- Skipping explicit consent design: The customer has to understand that their details are being saved for later use.

- Assuming zero friction forever: Some transactions may still need extra verification or updates.

A secure one click flow should feel easy for the customer, but disciplined in the background. That means clear consent, processor-managed storage, and product logic that knows when to ask for more verification instead of forcing every transaction down the same path.

How to Offer One-Click Payments with Suby

The practical question for most businesses is simple. How do you put one click payment into the hands of customers without building a payment stack from scratch?

One option is Suby, which provides an API that allows businesses to accept payments by card or crypto, supports shareable paylinks, embedded checkout, and API-based payment flows, and lets customers pay with cards while businesses receive USDC. It also offers native integrations with Discord and Telegram for subscriptions, paid access, and online communities, according to Suby's global payment API article.

Three practical ways to launch

Different businesses need different levels of control. The three most common launch paths are:

Shareable paylinks

This works well when you want a fast setup. Agencies, freelancers, consultants, and smaller online sellers often use links in email, chat, invoices, or social profiles. The customer opens a hosted payment page, completes the first purchase, and later repeat payments can feel much faster once the stored payment setup exists.Embedded checkout

This is usually the better fit for websites, SaaS upgrade screens, and product pages where you want the payment flow to stay close to your brand experience. The key product advantage is continuity. A returning customer doesn't feel pushed into a long form every time they come back.API and webhooks

This path gives developers the most flexibility. It's useful when payment needs to be tied to account logic, entitlements, internal billing events, or custom checkout states. The payment experience can then react to whether the customer is new, returning, retrying a failed payment, or updating a saved method.

What the customer sees

The customer experience should feel simpler than the architecture behind it.

A typical flow looks like this:

- The customer makes an initial purchase and agrees to save payment details.

- The payment layer stores the reusable credentials securely through the processor.

- On a later purchase, the business recognizes that customer as eligible for a faster repeat checkout.

- The buyer confirms the payment with minimal interaction.

That's where one click payment earns its keep. It turns repeat intent into a lighter action.

For product teams, the real win isn't only faster payment. It's removing repeat effort from customers who already decided they trust you.

This matters even more for global sales. Many businesses want customers to pay in a familiar way, usually by card, while keeping their own settlement side predictable. A setup where users pay with cards and the business receives USDC is often easier to operate than juggling multiple local banking relationships, delayed payouts, and currency conversion overhead.

Use Cases Beyond Simple E-commerce

Many people hear “one click payment” and think about a shopper buying the same product again. That's part of the story, but it's not the whole one.

The stronger use cases often show up in digital businesses where speed is tied to access. SaaS upgrades, paid newsletters, creator memberships, community subscriptions, coaching programs, and premium content all benefit when a returning customer can pay without repeating the same admin work.

Communities and memberships

Take a creator running a paid Discord group. A new member joins through a payment link, pays with a card, and gets access. A month later, renewal or plan expansion should not feel like a brand-new checkout.

That's where one click payment fits naturally. The customer already knows the creator, the offer, and the payment relationship. If they need to re-enter full details every time, the payment flow feels heavier than the product itself.

For community businesses, this matters in several ways:

- Paid access feels immediate: Members want to join and start participating right away.

- Renewals stay simple: Less re-entry means fewer interruptions around ongoing membership.

- Access management gets cleaner: Payment and entitlement can stay tied together instead of being handled manually across separate tools.

Subscriptions and repeat digital purchases

The same logic applies to SaaS and digital services. If a customer is upgrading a plan, renewing a subscription, or buying another seat, they don't want the experience to resemble a first-time checkout.

There's another operational angle that often gets ignored. Modern one-click systems still live inside real authentication and risk controls. Segpay's additional one-click documentation notes that these flows can reduce declines by detecting expired or soon-to-expire cards and letting customers update details during checkout, while also raising an important question about how frictionless payment interacts with stronger verification and access tradeoffs in global markets, as described in its one-click payment risk and authentication notes.

That point matters for businesses selling internationally. Not every customer has the same card stability, issuer behavior, or ability to pass every extra verification step on demand.

A product manager should design for that reality:

- Keep the fast path available when the payment method is healthy and the customer is clearly recognized.

- Handle updates gracefully when the card has expired or needs attention.

- Expect some exceptions in regulated or higher-risk contexts, especially across borders.

A frictionless payment experience isn't the same as a no-control payment experience. Good systems know when to speed up and when to pause.

This is why one click payment is useful beyond retail. It supports businesses that sell access, continuity, and repeat value, not just products in a cart.

The Future of Frictionless Commerce

One click payment is no longer a niche checkout idea. It's a practical standard for businesses that expect repeat purchases, mobile traffic, and global customers.

The reason is simple. Returning buyers shouldn't have to prove they're first-time customers every time they pay. When the payment setup already exists, a faster path respects the customer's time and protects buying intent.

The technical side is mature enough to support that expectation. Card-on-file flows, tokenization, consent capture, and processor-managed storage make one click payment workable without forcing merchants to hold sensitive data themselves. At the same time, modern payment systems still need to handle expired cards, extra verification, and regional compliance requirements without turning the experience into a dead end.

For internet businesses, the next step is operational. The checkout should feel familiar to the buyer, while settlement should stay predictable for the business. That's why the model of users paying with cards while businesses receive USDC is increasingly relevant for cross-border commerce, subscriptions, and paid online access.

If you want to add a faster checkout flow without building the payment stack yourself, Suby is one option to review. It lets businesses accept payments by card or crypto, supports paylinks, embedded checkout, API workflows, and Discord or Telegram monetization, while keeping the core model simple: users pay with cards, businesses receive USDC.