Your business might be selling software subscriptions in the US, invoicing agency clients in Europe, and onboarding community members from Asia, all in the same week. Revenue looks healthy on paper, but the money itself is messy. One provider handles cards, another handles bank transfers, a third handles crypto, and your finance team is staring at multiple dashboards that never quite reconcile cleanly.

That's where many global businesses get stuck. They don't really have a sales problem. They have a payments operations problem. Customers want to pay with the method they already trust, while the business wants predictable settlement, clean reporting, and fewer surprises around declines, delays, and currency conversion.

A modern merchant payment solution isn't just a checkout widget. It's the layer that decides how money moves into your business, how it gets routed, how it settles, and how much friction your team absorbs along the way.

Table of Contents

- Your Global Business Has a Payment Problem

- The simple definition

- Traditional stack versus modern orchestration

- Why the category is getting bigger

- Acceptance that matches customer behavior

- Developer and finance tools that hold up under scale

- Security and operational basics

- How fiat settlement behaves in practice

- What changes with stablecoin settlement

- A practical side by side view

- The single balance model

- Four product paths, one settlement logic

- Why the card to USDC flow stands out

Your Global Business Has a Payment Problem

A familiar pattern shows up once a company starts selling internationally. Product and marketing teams celebrate new markets, then operations inherits the fallout. US customers pay by card. European customers ask for bank transfers. Other buyers want wallets. Some clients are comfortable paying in crypto. Each new method solves one conversion problem and creates two new back-office problems.

The first problem is fragmentation. You log into one dashboard to inspect card declines, another to confirm payouts, and a third to trace a customer payment that support says “went through.” Refunds, disputes, subscriptions, and invoices start living in separate systems. Nothing is broken enough to force a rebuild, but everything is inconvenient enough to slow the business down.

The second problem is settlement. Getting a payment accepted is only half the job. You still need the money to arrive in the format your business can use, whether that means a bank payout or stablecoins such as USDC. If your stack treats fiat and crypto as separate worlds, your team ends up managing separate balances, separate reconciliation flows, and separate assumptions about fees and timing.

Most payment complexity doesn't show up at checkout. It shows up a week later when finance, support, and ops try to explain where the money went.

That's why a merchant payment solution matters. The right one gives you a consistent way to accept different payment methods, route transactions intelligently, and settle funds in a way that fits your business model. For a SaaS company, that might mean recurring billing and clean webhooks. For an agency, it might mean invoicing globally while choosing settlement currency. For a creator business, it might mean subscriptions and gated access without stitching together separate tools.

What Is a Merchant Payment Solution

The simple definition

A merchant payment solution is the infrastructure that lets a business accept customer payments and turn those payments into usable funds. That includes checkout, authorization, routing, settlement, reporting, and the controls around refunds, disputes, and recurring billing.

The easiest way to think about it is as a universal translator for money. Customers speak in payment methods. Cards, wallets, bank transfers, BNPL, and crypto all behave differently. Your business speaks in operating needs. Reconcile revenue, reduce failed payments, control FX exposure, and get funds where they need to go. A payment solution sits in the middle and translates one side into the other.

If you want a useful primer on the provider layer itself, this explanation of what a payment provider does is a good companion read.

Traditional stack versus modern orchestration

In the traditional model, merchants often bolt together separate services. One gateway passes card data. One acquirer processes transactions. Another provider handles local payment methods. A separate tool might handle crypto. That setup can work, but it usually creates rigid dependencies. Adding a new provider often means engineering work, new reconciliation rules, and another operational surface area to manage.

A more modern architecture uses an orchestration layer. Instead of hard-wiring your checkout to one processor, the orchestration layer routes transactions across multiple providers and methods. According to Corefy's overview of payment infrastructure, this approach can recover 30% of initially declined transactions through dynamic routing and reduce interchange fees by 15-20% using network tokenization.

That matters because payment performance is rarely about one dramatic feature. It's the sum of smaller improvements, better retry logic, smarter routing, easier provider changes, and less dependence on any single payment partner.

Here's the practical difference:

| Model | What it feels like for the merchant |

|---|---|

| Separate point solutions | Fast to launch, harder to manage as payment methods and markets expand |

| Orchestrated infrastructure | More flexible, easier to route, swap, and optimize without rebuilding core business logic |

A short walkthrough helps make that architecture more concrete:

Why the category is getting bigger

This isn't a niche infrastructure category anymore. The payment gateway market is projected to reach USD 161.0 billion by 2032, with Asia-Pacific cashless transaction volumes rising from USD 494 billion in 2020 to USD 1,818 billion by 2030. That growth tells you something simple. More businesses need systems that can support global payment diversity without multiplying internal complexity.

Key Features Every Global Merchant Needs

Acceptance that matches customer behavior

A global merchant can't assume one payment method will carry every market. Cards still matter because they're familiar and widely accepted, but that's no longer the whole picture. By 2024, digital and mobile wallets are expected to account for 51.7% of global e-commerce payment methods, while cards are accepted by 76% of merchants and digital wallets by 68%. If your checkout only works well for cards, you're already behind customer preference in many regions.

That's why acceptance should be evaluated as a system, not a logo wall.

- Cards still need to work cleanly: They remain the baseline for many merchants and for recurring payments.

- Wallet support isn't optional anymore: It affects conversion in markets where customers expect a faster mobile-first flow.

- Bank methods matter for specific regions and invoice-heavy businesses: They can be essential for B2B or local market trust.

- Alternative methods widen coverage: BNPL and crypto can serve real demand, but only if they don't create separate operational silos.

Developer and finance tools that hold up under scale

The best checkout experience fails quickly if the surrounding tooling is weak. Developers need an API that's predictable, webhooks that arrive reliably, and documentation that makes edge cases obvious. Finance teams need a dashboard that reflects reality without hours of manual cleanup.

A capable merchant payment solution should support:

- API and webhook access: Your app needs real-time payment events for subscriptions, provisioning, retries, and internal reporting.

- Paylinks and hosted checkout options: These help sales, support, and finance teams collect payment without waiting on product releases.

- Recurring billing support: Essential for SaaS, memberships, retainers, and installment-style offers.

- Multi-currency handling: Customers should be able to pay in one currency while the business chooses how to receive funds.

- Unified reporting: One place to inspect payments, subscriptions, refunds, disputes, and payouts.

Practical rule: If your support team can't answer “Did this customer pay?” from a single system, your payment stack is already too fragmented.

Security and operational basics

Global acceptance is only useful if the system is dependable. Merchants should expect strong authentication flows, dispute handling, and compliance support that reduces operational risk instead of offloading everything back to the merchant.

This is also where many teams underestimate the value of native workflow support. For example, invoicing, subscription management, and community gating can all live close to the payment layer instead of being pushed into disconnected tools. That matters because each extra handoff creates more room for failed entitlements, delayed access, or manual reconciliation.

A useful way to judge feature depth is to ask whether the platform can support different business shapes without forcing a different stack for each one:

| Business need | What the payment solution should support |

|---|---|

| SaaS subscriptions | Recurring billing, retries, webhooks, payout flexibility |

| Cross-border e-commerce | Cards, wallets, local methods, multi-currency settlement |

| Agencies and freelancers | Invoicing, paylinks, clean reporting, payout choice |

| Communities and creators | Paid access, subscriptions, native integrations for access control |

A strong merchant payment solution doesn't just approve payments. It reduces the number of systems your team needs to operate.

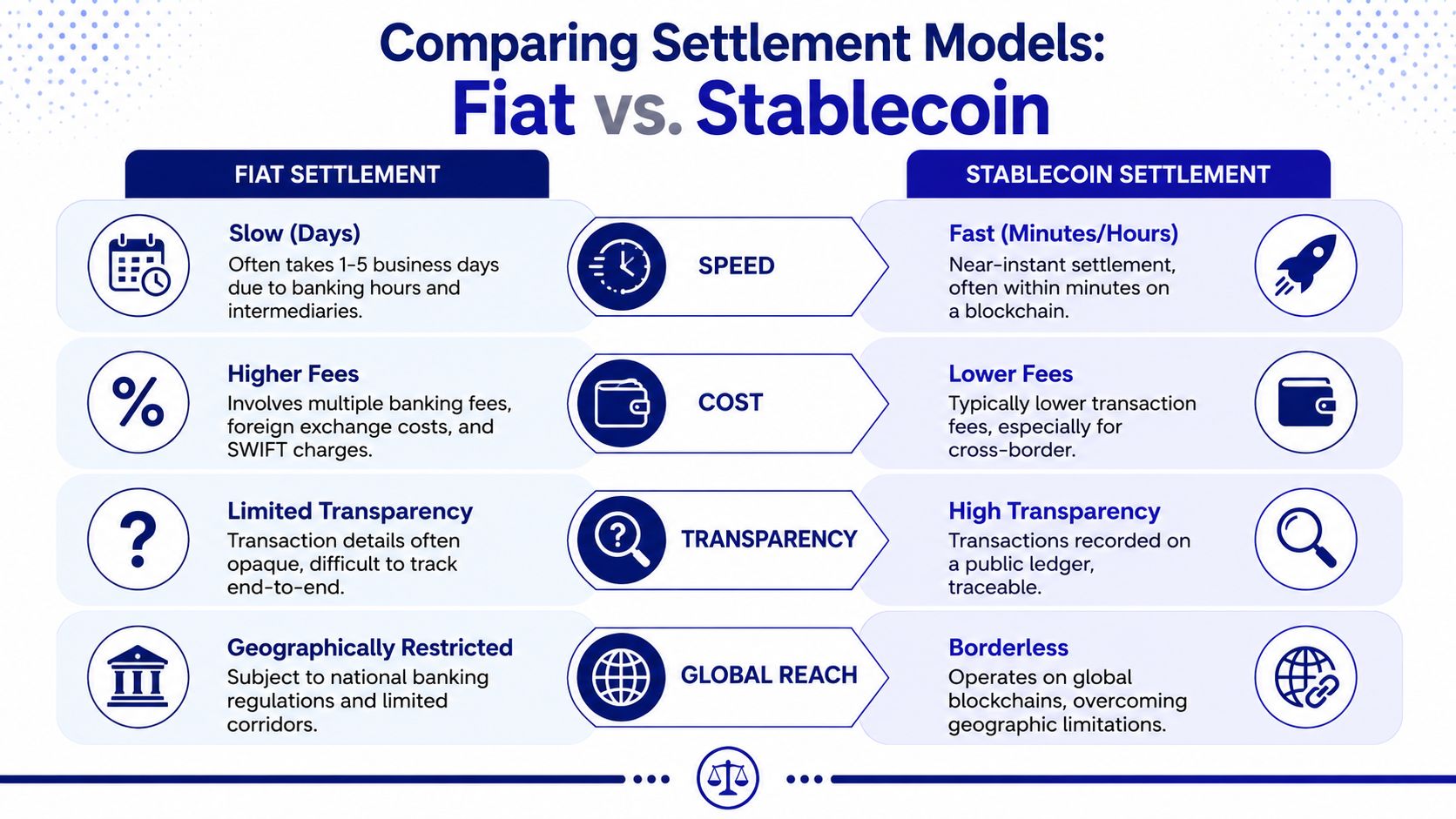

Comparing Settlement Models Fiat vs Stablecoin

How fiat settlement behaves in practice

Traditional fiat settlement works through the banking system. That means bank cutoffs, intermediary steps, local rails, and cross-border friction. For domestic payouts, that may be acceptable. For international businesses, it often becomes one of the least visible sources of cost and delay.

The issue isn't only speed. It's opacity. A merchant may know what the customer paid, but not fully understand what arrived after currency conversion, processing layers, and settlement timing. That makes forecasting harder and margin analysis less reliable.

What changes with stablecoin settlement

Stablecoin settlement changes the last mile of the flow. Instead of waiting for the banking stack to finish moving value across institutions and jurisdictions, funds can settle on-chain in a stable asset such as USDC. That can be especially useful for software businesses, agencies, and international merchants that already hold part of their treasury in digital dollars or need faster access to revenue.

The economics matter too. Finix notes that 78% of cross-border e-commerce merchants lose profit due to opaque FX spreads, which can erode 2-5% of revenue. If your provider can offer transparent FX rails, that's not a niche feature. It's a direct margin question.

For teams exploring the talent and architecture side of this shift, this stablecoins and tokenized deposits position is a useful signal of where payment infrastructure work is heading.

You can also compare different cross-border payment solution models to see how payout design affects operations.

A practical side by side view

| Factor | Fiat settlement | Stablecoin settlement |

|---|---|---|

| Payout path | Banking rails and intermediaries | On-chain transfer |

| Cross-border FX visibility | Often harder to predict | Can be more transparent when pricing is explicit |

| Treasury use case | Familiar for bank-based operations | Useful when businesses want digital dollar settlement |

| Operational fit | Strong for conventional bank payout flows | Strong when merchants want faster access or direct wallet receipt |

If your customers pay globally but your settlement model is still local-first, finance ends up carrying the mismatch.

The important nuance is that this isn't an either-or decision for every business. Many merchants need both. They want to accept cards, wallets, bank methods, and crypto, then choose whether revenue lands in a bank account or in stablecoins. That flexibility is where the single-balance model becomes interesting.

How to Evaluate and Choose a Solution

Look past the headline transaction fee

Most merchants start by comparing visible fees. That's understandable, but it's rarely enough. The cheaper-looking option can become the more expensive one once you account for failed payments, engineering maintenance, reconciliation effort, support delays, and FX leakage.

A payment stack should be evaluated as part infrastructure, part operating model. If the provider locks you into one processor, one payout path, or one reporting view, your internal costs rise even if the advertised fee looks fine. If the system gives you orchestration, better routing, and more payout control, the economics can improve in less obvious ways.

That's why the orchestration layer matters so much in evaluation. As noted earlier from Corefy's infrastructure analysis, dynamic routing and tokenization can improve conversion and cost outcomes. You don't need to treat that as abstract technical detail. It directly affects how many payments succeed and what each payment costs to process.

Questions worth asking before you sign

A useful selection process sounds less like procurement jargon and more like operational skepticism. Ask questions that expose how the system behaves after launch.

- How many balances will my team manage: If fiat and crypto sit in separate systems, your reconciliation complexity goes up immediately.

- Can we choose our settlement method: Some businesses need bank payout, some need stablecoins, and some need both depending on geography or treasury policy.

- How hard is it to add a payment method later: If every expansion requires code rewrites, your future roadmap is already constrained.

- What does the developer experience look like: Review API docs, webhook behavior, test environment quality, and event clarity.

- How does support work when something fails: Payment issues usually surface under urgency, not during a calm planning session.

- What does finance see daily: Clean dashboards, payout visibility, and usable exports matter more than flashy demo flows.

Good payment infrastructure saves engineering time, but great payment infrastructure also saves finance and support time.

One more practical filter helps. Ask the vendor to describe a real payment journey end to end. Customer pays with a card. Payment is authorized. Revenue is recorded. Refund happens. Dispute happens. Payout happens. If that story becomes fuzzy halfway through, the product probably is too.

A Modern Approach Suby for Global Payments

A useful way to judge any payment platform is to follow one real transaction from checkout to settlement. A customer enters card details. The payment is approved in the familiar card rails. Finance does not want the proceeds split across a card processor, a crypto wallet, and a separate reporting tool. The modern model aims to keep that money path in one operational system.

One concrete example of this model is Suby, which presents itself as payment infrastructure for internet businesses operating across borders. The product direction is straightforward. Customers can pay with familiar methods such as cards, wallets, bank methods, BNPL, or crypto, while the merchant chooses how funds are settled, including bank payout or stablecoins such as USDC.

The single balance model

The interesting part is not just payment method coverage. It is the single-balance design.

Many providers let you accept both fiat and crypto, but they still treat them as separate systems. One dashboard for cards. Another wallet flow for stablecoins. Another reconciliation process for payouts. That setup works until volume grows, refunds start to matter, and finance has to explain where cash sits.

Suby describes a different model in its product materials. Fiat and crypto activity are recorded in one balance ledger, with settlement options that include USDC, plus balance views in major fiat terms and payment support described in Suby's API introduction. The practical effect is easier to understand than the architecture. Your team sees one revenue pool instead of stitching together separate payment buckets by hand.

That changes day-to-day operations. A card payment, bank payment, wallet payment, or stablecoin payment can be handled as entries in one system of record. Finance gets a cleaner reconciliation process. Support gets a clearer answer when a customer asks what happened. Product teams get more freedom to add payment methods without creating a second back office for each one.

Four product paths, one settlement logic

Suby packages this model into several product flows tied to different business needs:

- Suby Payments: API-based acceptance for card and crypto payments in one checkout flow.

- Suby Crypto: Crypto payment acceptance with conversion handling, gas sponsorship, and settlement to a wallet or platform balance.

- Suby Gating: Paid access controls for channels, downloads, courses, and communities.

- Suby Invoicing: Invoices where the buyer uses one payment method and the merchant settles in another.

The common thread is operational consistency. A SaaS company might use the API for self-serve checkout and invoicing for larger accounts. A creator business might combine paid community access with recurring payment collection. A team evaluating those flows can review the event model and implementation details in this payment gateway API integration guide.

Why the card to USDC flow stands out

The card-to-stablecoin path is where this model becomes concrete. A buyer pays with a card because that is what they already trust and understand. The merchant receives USDC because that may fit treasury operations better than waiting on cross-border bank settlement.

That flow solves a fragmentation problem many guides skip past. Customer preference and merchant settlement preference do not need to be the same thing. Traditional setups often force a business to choose between broad card acceptance and crypto-native settlement. A single-balance model connects both.

For a global SaaS company, this can reduce the gap between revenue collection and usable working capital. For an agency, it can simplify client billing while keeping settlement in the asset the business wants to hold. For a digital product company, it can keep checkout familiar without creating a separate reporting process for crypto receipts.

A few practical details matter here:

- Pricing varies by payment method: exact costs are listed on Suby's pricing page.

- Merchant of Record support is part of the product story: company materials describe support around payment processing, tax handling by location, and disputes.

- Payin and settlement are decoupled: the payment method used by the customer does not have to dictate how the merchant receives funds.

That separation is the operational advantage. Customers pay in the way that feels normal to them. The business settles in the format that best fits its treasury, accounting, and cross-border cash movement.

Integration Steps and Common Pitfalls

A practical rollout path

Organizations should integrate a new payment layer in stages. Start with the smallest production use case that still touches your real business logic. That might be a paylink flow, a hosted checkout, or one invoice workflow before you move into deeper API control.

A practical rollout usually looks like this:

- Map your payment journeys: One-time payments, subscriptions, invoicing, gated access, refunds, and payout needs.

- Review the API and event model: Make sure your developers understand the expected webhook lifecycle and failure cases. A good starting point is this payment gateway API integration guide.

- Test settlement expectations early: Don't wait until go-live to verify what lands where, in what currency, and on what timeline.

- Connect internal owners: Product, finance, support, and engineering should all validate the same payment flows from their own perspective.

Mistakes that slow teams down

The most common integration mistake is treating payments as a frontend task. Checkout is visible, so it gets attention. Reconciliation, payout logic, entitlements, and support workflows are less visible, so teams leave them vague until a customer issue exposes the gap.

A few traps come up repeatedly:

- Skipping edge-case testing: Refunds, duplicate webhooks, partially failed subscription events, and payout exceptions deserve real test time.

- Ignoring documentation quality: If the docs are hard to follow in sandbox, production incidents will be worse.

- Choosing for today only: A provider that works for one region and one payment method may become a migration project later.

- Accepting dual infrastructure by default: If card flows and crypto flows require separate systems, the burden lands on ops.

The healthiest payment integrations are boring after launch. That usually means the team did the hard thinking up front.

If you're looking for a payment layer that supports card, wallet, bank, and crypto payins while letting the business choose settlement to a bank account or stablecoins like USDC, Suby is worth reviewing. It offers API-based payments, invoicing, crypto payment flows, and native Discord and Telegram integrations, with pricing based on the payment method used.