Gaspard LEZIN

Master BitPay: 2026 Merchant Guide & Pricing

Understand BitPay for merchants: how it works, features, pricing, and security. Our 2026 guide compares it to modern payment solutions.

If you're selling online across borders, the payment problem usually shows up in three places at once. Customers want a familiar checkout, your finance team wants predictable settlement, and your operations team doesn't want to chase failed transfers, FX surprises, or payout delays.

That tension is why bitpay still comes up in merchant conversations. It's one of the earliest names in crypto payments, and it remains relevant for businesses that want to accept digital asset payments without building the whole stack themselves. But for a modern internet business, the central question isn't whether bitpay works. The critical question is whether its model matches how you want to get paid.

Table of Contents

The pain points usually come first

What happens at checkout

Why the rate lock matters

What the merchant experience feels like

Merchant tools that matter

Where the wallet fits

What merchants actually pay attention to

How BitPay approaches wallet security

Comparing BitPay to Modern Payment Solutions

Choose based on your payout goal

A practical decision rule

The Challenge of Global Payments

A global business can be profitable on paper and still feel messy in practice. You might invoice a client in one currency, pay software vendors in another, and wait on settlement from a payment provider that wasn't designed for borderless sales in the first place.

That gets worse when you're selling digital products, subscriptions, consulting, or community access. The sale may be instant, but the money path often isn't. Mobile commerce only adds pressure because customers expect fast checkout on smaller screens, and every extra step creates drop-off. If you're optimizing that layer, Carti's Shopify mcommerce insights are worth reading because they connect payment friction directly to conversion behavior on mobile.

For many merchants, crypto payment processors like BitPay and Coinbase Commerce entered the picture as a way to reduce some of that friction. BitPay is one of the best-known examples. It processed over 600,000 cryptocurrency transactions in 2024, according to these BitPay statistics, which tells you there is still real demand for this payment path.

The pain points usually come first

Most owners don't start by searching for crypto payments. They start with practical problems:

Slow settlement: Revenue arrives later than the sale, which complicates cash planning.

Currency mismatch: You sell globally, but your payout setup still assumes local banking rails.

Operational clutter: Finance teams reconcile invoices, fees, conversion costs, and payout timing across multiple systems.

Businesses rarely switch payment infrastructure because it's interesting. They switch because the old flow creates too much admin and too much uncertainty.

If you're mapping those issues from first principles, this guide on how to accept international payments is useful because it frames the problem around settlement, fees, and customer experience instead of just checkout widgets.

BitPay matters in this discussion because it helped normalize the idea that a merchant can accept digital asset payments through a managed gateway. But once you move beyond that basic capability, the important questions become more specific. How does the payment flow work, what does the merchant control, and where do the trade-offs start to show?

How BitPay Payments Work

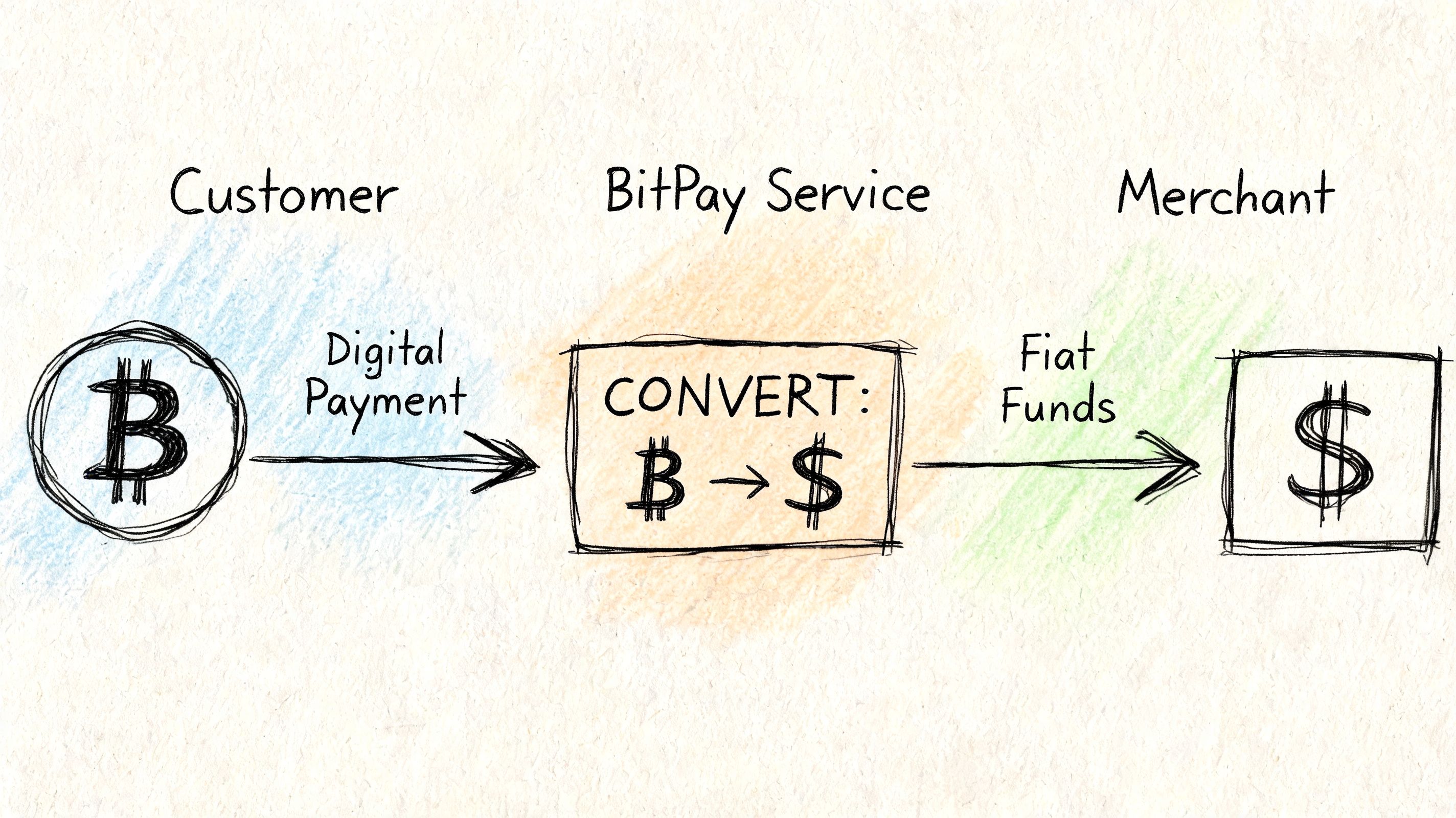

BitPay sits between the customer payment and the merchant settlement flow. In practical terms, it lets a business create a crypto payment request, present that request at checkout, and receive a confirmed payment status once the transaction clears.

What happens at checkout

The basic sequence is straightforward. BitPay's gateway generates an invoice with a 15-minute expiry and a locked exchange rate, then the customer pays from a compatible wallet, and the transaction confirmation triggers a merchant notification with the transaction details, as described in this BitPay gateway review.

For a merchant, that matters because the invoice acts like a temporary quote. The customer sees what to pay during that window, and the merchant isn't left wondering whether the final received value drifted during checkout.

A simple way to think about it is this:

The merchant creates an invoice inside the BitPay flow or through an integration.

The customer opens the payment request and chooses a supported wallet.

The rate is held briefly so the amount due stays consistent during checkout.

The network confirms the payment and BitPay updates the merchant status.

The merchant reconciles the order using the transaction details returned by the system.

If you're comparing this against other merchant setups, this overview of accepting crypto payments for business is a helpful contrast because it focuses on how businesses operationalize payment flows, not just how customers pay.

Why the rate lock matters

The locked rate is one of the more important parts of the BitPay model. Without it, every delayed payment becomes a pricing risk. With it, the merchant gets a short decision window that makes checkout more predictable.

That doesn't make the process frictionless for every customer. The user still has to complete the payment from a compatible wallet, which is a different behavior from card checkout. For crypto-native buyers, that's normal. For mainstream buyers, it's still a narrower path.

Practical rule: BitPay works best when your customer already understands wallet-based payments. It adds less value when your customer just wants to tap a card and move on.

For a quick visual walkthrough, this video gives context on the flow merchants are evaluating:

What the merchant experience feels like

From the business side, BitPay is less about a consumer wallet app and more about controlled payment acceptance. The merchant cares about whether an invoice can be issued cleanly, whether the order status updates reliably, and whether settlement arrives in the format the business expects.

That makes BitPay more useful for certain use cases than others. It's good when you want to add a digital asset payment option to an existing online checkout. It's less elegant when your core requirement is broad payment accessibility for non-crypto users.

Exploring BitPay Features for Merchants

Most merchants don't buy payment infrastructure for one transaction. They buy it for repeatable operations. That means the useful question isn't just whether bitpay can accept a payment. It's whether the surrounding tools reduce daily work for finance, support, and ops.

Merchant tools that matter

BitPay's merchant value is in its business tooling. You can create payment requests, manage invoices, track transaction states, and work from a dashboard that helps with order handling and reconciliation.

The merchant toolkit usually matters most in these scenarios:

Online checkout collection: Useful for stores and digital services that want to add a crypto payment option without managing direct wallet operations themselves.

Invoice-based sales: Helpful for agencies, B2B sellers, and service businesses that bill customers manually or semi-manually.

Transaction monitoring: Important when support teams need to check whether a payment is pending, completed, or expired.

BitPay's business usage profile also says a lot about who finds it most practical. In May 2025, the internet sector captured the highest share of BitPay payments globally, with an average transaction size of $800, according to BitPay Decrypted 2025. That points to a merchant base using it for more substantial online and B2B-style transactions, not just impulse consumer purchases.

Where the wallet fits

BitPay also has a consumer wallet within its ecosystem. For merchants, that matters less as a standalone product and more as part of the broader payment environment. A customer already using the wallet may have a smoother experience paying a BitPay invoice than someone arriving cold at checkout.

Still, business owners shouldn't confuse wallet presence with merchant fit. The wallet can support the ecosystem, but it doesn't solve the main merchant questions, which are usually about settlement clarity, payment accessibility, and back-office simplicity.

A useful way to break down the platform is this small table:

Business need | BitPay feature relevance | Practical note |

|---|---|---|

One-off invoice collection | High | Works well when the buyer is already comfortable paying from a wallet |

Online product sales | Moderate to high | Better for crypto-aware audiences than for general consumer checkout |

Recurring access or memberships | Limited fit | Traditional merchant orientation shows here |

Cross-border business payments | Situational | Depends on settlement path and conversion requirements |

Some payment tools are strong at acceptance but weaker at monetizing internet-native products like subscriptions, gated communities, and paid access. That's an important distinction if your business lives online.

Many modern businesses begin to separate "can accept payment" from "fits our model." If you're selling software, access, memberships, or global services, the winning setup often isn't the one with the longest history, and it also helps you sidestep marketplace tolls like the Apple 30% payment cut on in-app sales. It's the one with the fewest moving parts after the payment succeeds.

BitPay Pricing Security and Compliance

For most merchants, pricing and risk management decide the conversation. A payment product can look capable in a demo and still create headaches if the fee model is unclear or the compliance process interrupts ordinary business activity.

What merchants actually pay attention to

BitPay's published merchant narrative centers on a standard processing fee, but experienced operators know that's only part of the picture. The more relevant issue is total payment cost after settlement choices, currency conversion, and cross-border handling are factored in.

A useful summary from this pricing guide for payment gateways is that headline processing fees rarely tell the full story. That framing matters with BitPay because analysis has shown that its model can have hidden cross-border costs due to currency conversion spreads and settlement delays, contrasting with models that settle natively in stablecoins with zero FX friction, as discussed in this BitPay statistics analysis.

So the practical merchant question isn't "Is the fee low?" It's "What lands net in my account or wallet, how long does it take, and what gets shaved off along the way?"

How BitPay approaches wallet security

On the security side, BitPay Wallet uses Hierarchical Deterministic multisignature architecture, which means multiple keys are required to authorize a transaction. The practical advantage is simple. Control isn't concentrated in one key, so a single point of failure doesn't automatically expose funds. The BitPay wallet overview describes this as a model that distributes trust and mitigates single points of failure.

For a business owner, "multisig" should translate to operational resilience, not technical jargon. If your team stores treasury funds or uses shared approval flows, multiple-key authorization is a meaningful control.

Here's the plain-English version:

One key isn't enough: Spending requires more than a single approval point.

Shared control is possible: That helps teams separate responsibilities.

Recovery and governance improve: Especially compared with setups that depend on one device or one person.

Compliance and security are not separate topics in payments. The stricter the controls, the more important it is to understand how reviews, holds, and approvals affect day-to-day operations.

There's also a tax and accounting angle that many businesses underestimate. If you're handling digital asset payments at any meaningful volume, someone has to track treatment, reporting, and records. For teams building that process, understanding crypto tax obligations is a useful companion resource.

BitPay is credible on security architecture. The bigger merchant challenge is usually not whether the wallet model is technically sound. It's whether pricing, compliance handling, and settlement design fit the way the business operates.

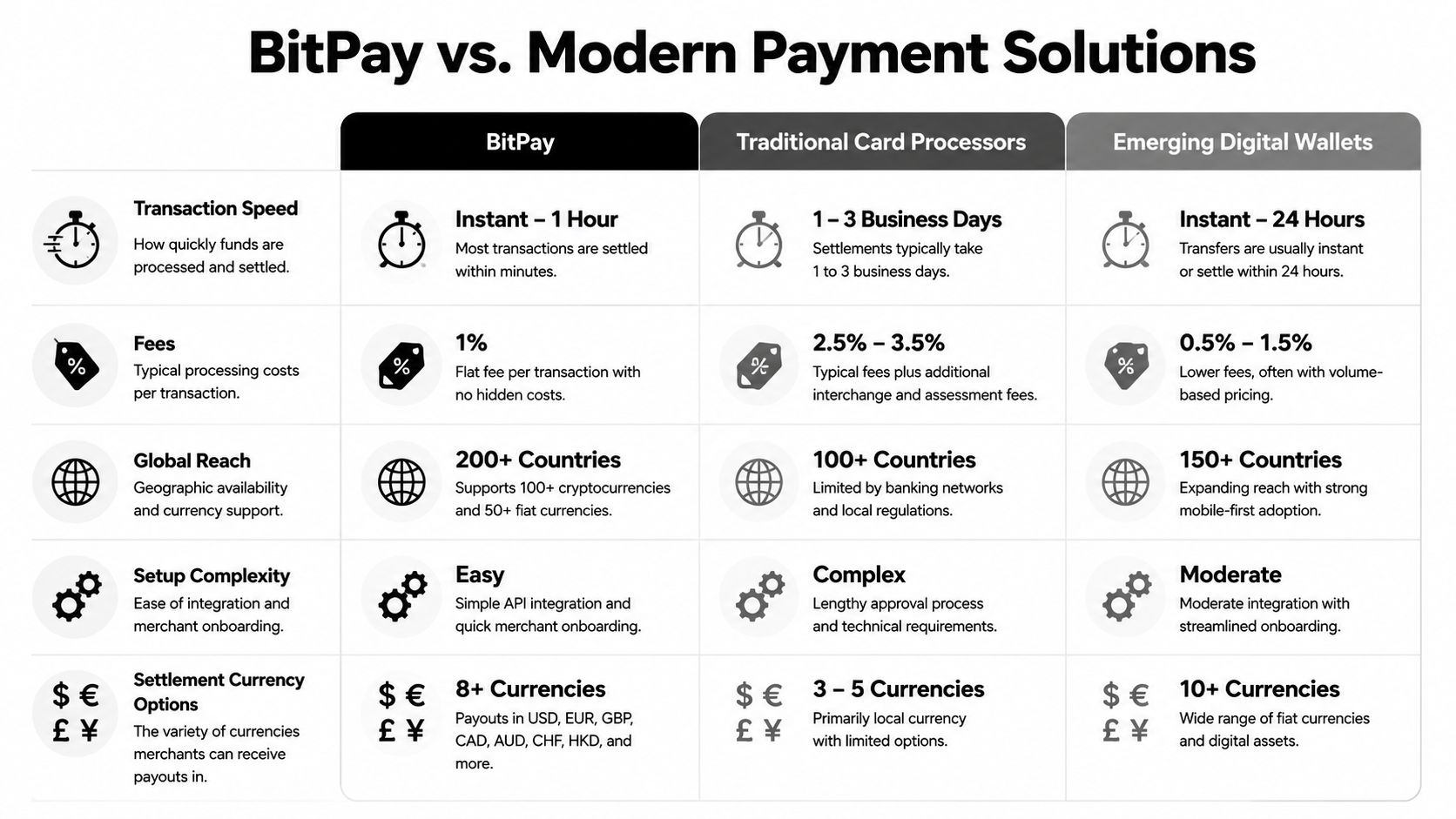

Comparing BitPay to Modern Payment Solutions

A global business selling across borders usually wants one outcome after checkout. Funds should arrive in a predictable currency, on a predictable timeline, with as little manual reconciliation as possible. That standard is what modern buyers and finance teams now bring to any comparison of BitPay.

BitPay still has a clear use case. It gives merchants an established way to accept certain digital assets through a managed invoice and processing flow. If the business serves customers who already hold crypto and are comfortable paying from wallets, that can be enough.

Its fit is narrower than many teams expect.

BitPay works best for merchants that want to add crypto acceptance as one payment rail inside a broader stack, not for companies trying to simplify global settlement end to end. The distinction matters because the strongest payment products in 2026 are no longer judged only by checkout acceptance. They are judged by what the business receives after the sale and how much operational friction remains.

BitPay can make sense for:

Crypto-native or crypto-familiar buyers: Customers already understand wallet payments and do not need a card-first checkout experience.

Higher-consideration purchases: A hosted invoice flow is easier to justify for larger transactions than for impulse purchases.

Merchants adding optional crypto support: The business keeps its main card and banking setup and offers BitPay as a supplemental rail.

The pressure point is settlement. BitPay came from a processor model built to help merchants accept volatile digital assets without having to operate every part of the crypto flow themselves. Many newer providers start from a different assumption. The customer can pay with familiar methods, while the merchant settles directly in a stablecoin such as USDC.

That leads to a different operating model.

Criteria | BitPay model | Stablecoin-native model |

|---|---|---|

Customer experience | Best suited to wallet-based payers | Better for broader audiences if card payment is supported |

Settlement outcome | May involve conversion steps before funds reach the merchant | Merchant receives stablecoins directly |

Cross-border operations | More dependence on processor timing, payout routes, and conversion handling | Cleaner for businesses already managing international treasury in stablecoins |

Reconciliation | Can be more complex if payment method and settlement currency differ | Simpler if revenue lands in one consistent currency |

Recurring access businesses | Useful for acceptance, less tailored to access automation | Better fit when billing, subscriptions, and access control are part of the product |

Suby is one example of that newer model. It offers card and crypto acceptance with settlement in USDC, plus Discord and Telegram integrations for subscriptions, paid access, and community payments. That is a different product direction from BitPay's merchant processor roots, and for internet-native businesses it often matches the actual requirement more closely.

Many global merchants do not need more ways to accept crypto. They need fewer payout variables after the transaction clears.

Audience fit matters too. BitPay is strongest in a classic merchant acceptance scenario. A software company, creator business, agency, or community operator may care more about recurring billing, automated access, and stablecoin treasury flows than about a traditional crypto invoice experience. In those cases, the better question is not "Can this provider accept crypto?" It is "Will this provider reduce settlement friction for the finance team?"

That is where the trade-off becomes concrete. A payment stack can advertise a straightforward processing fee and still create hidden cost through FX spreads, extra conversion steps, payout delays, or fragmented reporting across countries. Stablecoin-native systems are not automatically better for every merchant, but they do remove part of that complexity when the business already wants to hold or use digital dollars across borders.

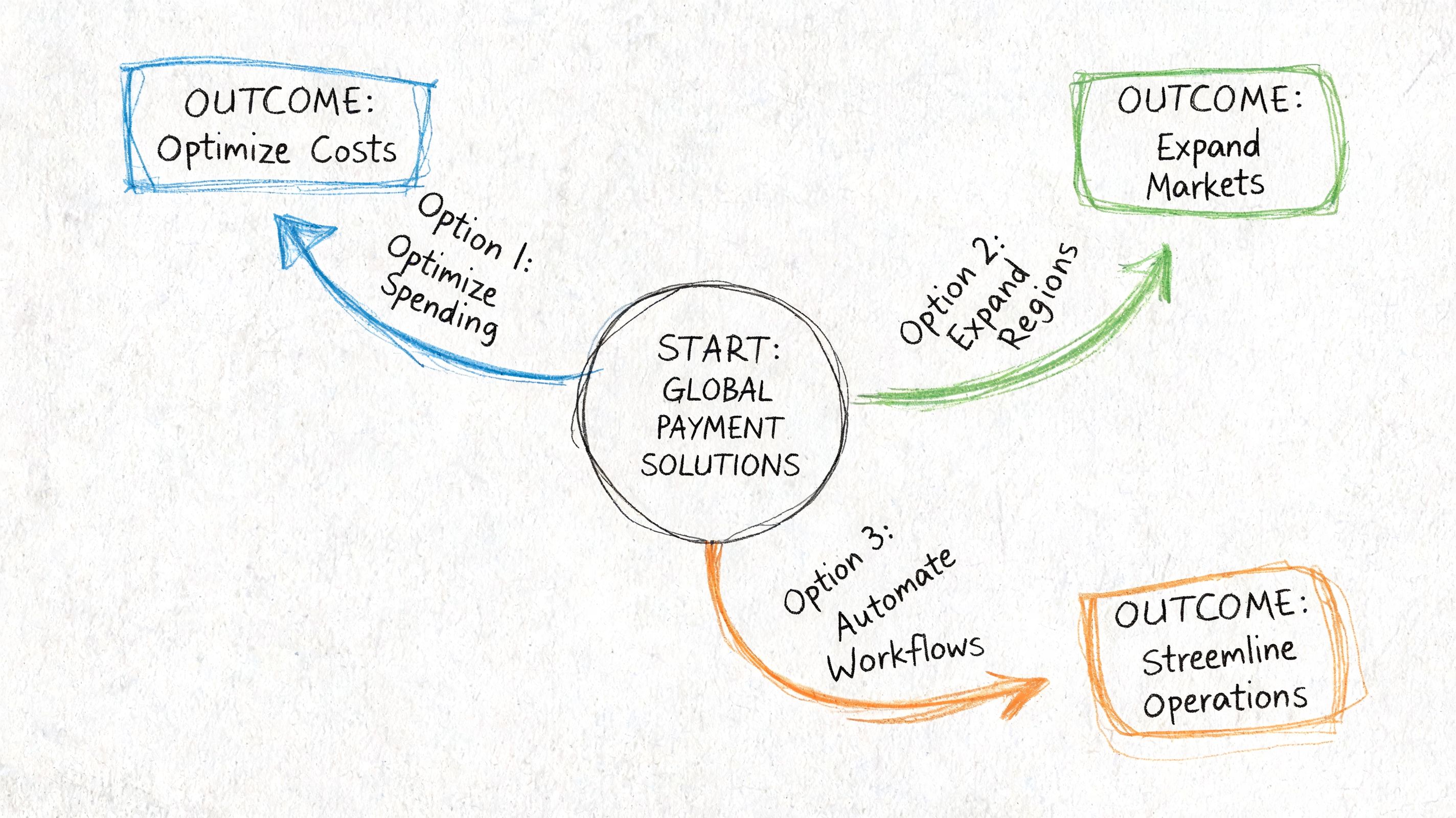

Choosing the Right Global Payment Strategy

The right answer depends on what you're optimizing for. Not every business needs the same payment setup, and not every payment problem is really a checkout problem.

Choose based on your payout goal

If your goal is to add a recognized crypto payment option for customers who already use wallets, bitpay is still a reasonable tool. It has real merchant infrastructure, an established invoice flow, and a long operating history in this category.

If your goal is broader, the answer changes. A SaaS business, agency, or creator brand selling globally usually wants three things at once:

Easy checkout for the customer

Predictable settlement for the business

Less cross-border admin after the sale

BitPay addresses the first point for a specific type of customer. It addresses the second and third only partly, because the merchant still has to think carefully about settlement design, cost leakage, and use case fit.

A practical decision rule

Use BitPay when your payment demand is clearly crypto-native and your team is comfortable with that operational model.

Choose a stablecoin-native payment strategy when your business is global by default and you want cleaner cash flow. That matters most when you sell subscriptions, digital services, retainers, software, or community access across multiple countries, where recurring billing details like the prorated charge meaning shape how upgrades and mid-cycle changes are handled.

A simple way to evaluate your next move is to ask:

Who is the payer? Wallet-native user or mainstream card buyer?

What do you want to receive? Mixed settlement outputs or one stable payout currency?

How much manual work happens after payment? Reconciliation, conversion, access fulfillment, support follow-up.

The best payment setup is the one that reduces work after the transaction, not just the one that completes the transaction.

For many businesses, that means moving closer to a model where users pay with cards and the business receives USDC directly. It gives customers a familiar buying experience and gives operators a cleaner settlement layer for global commerce.

Suby is a payment gateway and Merchant of Record. Your customers pay with card, bank transfer, Apple Pay, Google Pay, Klarna, and more, or stablecoins, and you get paid out to your bank account, or directly in stablecoins (USDC, EURC) to your wallet, anywhere in the world, no bank account required. With native Discord and Telegram access and built-in subscriptions, it leaves global merchants far fewer payout variables after the transaction clears than a wallet-first crypto processor like BitPay, where buyers still need a compatible wallet to pay.