Gaspard LEZIN

Nowpayments Alternative for Global Payouts

Searching for a Nowpayments alternative? Compare top crypto payment gateways on fees, USDC settlement, card payments, and developer APIs to find the best fit.

You’re probably not looking for a nowpayments alternative because the checkout button stopped working. You’re looking because the money flow after checkout has become messy.

A global SaaS company sees revenue arrive in different assets, finance has to reconcile conversions manually, product teams are waiting on payout clarity before rolling out new regions, and support gets dragged into payment questions that should’ve been solved by the processor. The visible fee is one issue. The operational drag behind it is the bigger one.

That’s where most gateway comparisons fall short. They compare a posted fee, a coin count, and a few integrations. They don’t spend enough time on settlement predictability, conversion overhead, reporting, and developer maintenance. Those are the costs that show up every month, long after the gateway is live.

Table of Contents

Where the frustration actually shows up

The real question behind the switch

Three provider models now define the market

Selection criteria have matured

Familiar brands now face a harder test

Payment acceptance is only the first layer

Settlement design affects daily operations

Headline fees rarely reflect the real cost

Developer experience decides how expensive “simple” becomes

Match the gateway to the business model

NOWPayments as the baseline

CoinGate for merchants that still think in fiat

A narrower settlement model for internet-native businesses

The comparison point that actually changes cost

What sits below the posted fee

Why predictability often beats a lower posted rate

For global SaaS companies

For e-commerce teams with existing fiat-heavy operations

For creators, communities, and internet-native businesses

A short decision filter

Migration checklist

Frequently asked questions

Does stablecoin settlement make accounting easier

What about disputes and refunds

Is card-to-USDC practical for global businesses

Do Discord and Telegram use cases need a separate tool

Why Businesses Seek Alternatives to NOWPayments

A common pattern looks like this. A company starts with a crypto gateway because it wants broader payment acceptance and faster cross-border sales. At first, that works. Then finance realizes the hard part isn’t collecting payment. It’s turning incoming funds into something usable and predictable for payroll, vendor payments, treasury, and reporting.

NOWPayments is often part of that first phase because it supports a wide range of assets and gives merchants flexibility. But flexibility can create extra work when the business needs consistency. If your customer pays one way, your internal team wants settlement another way, and your accounting stack expects something else, each handoff introduces friction.

Where the frustration actually shows up

The search for a nowpayments alternative usually starts with one or more of these issues:

Treasury mismatch: Revenue arrives in forms that don't match how the business holds operating funds.

Settlement uncertainty: Teams can't always predict what the final received amount will look like after conversion and network effects.

Support overhead: Payment operations spill into customer support because the payment flow is harder to explain than it should be.

Developer drift: Engineers keep revisiting payment logic for edge cases instead of moving on to product work.

Businesses rarely switch payment providers over one bad invoice. They switch because reconciliation, payouts, and support keep eating time every week.

This matters more for international SaaS than for simple one-off sales. Subscription products need consistency. Community products need clean access control. Agencies need predictable payouts. A gateway that accepts many assets can still be a poor fit if the operational model behind it stays fragmented.

The real question behind the switch

The practical question isn’t, “Can this processor accept crypto?” Most can.

The better question is, “What happens after the customer pays?” If the answer includes manual conversions, unclear payout timing, messy reporting, or extra finance work, then the effective cost is already higher than the headline fee suggests.

The Crypto Payment Processor Landscape in 2026

A SaaS finance team closes the month, sees healthy crypto sales, and still cannot answer a basic question quickly: what arrived, in which asset, and when it can be used. That gap explains how the market changed. Early processors competed on coin count. Buyers now care more about settlement predictability, conversion paths, reporting, and how much engineering time the integration will keep consuming after launch.

The category is also more segmented than it was a few years ago. Providers are no longer trying to solve the same problem in the same way. Some optimize for broad token acceptance. Some prioritize merchant control. Others narrow the model on purpose so treasury and reconciliation stay simple. For operators, that is a useful shift because the true cost of a gateway rarely sits in the headline processing fee alone.

Three provider models now define the market

Fiat-oriented processors sit closest to traditional merchant operations. They usually appeal to teams that want incoming crypto converted into bank-friendly settlement with reporting that finance can use without extra interpretation. The trade-off is dependency on banking rails, conversion timing, and payout windows that may vary by corridor or currency.

Non-custodial or control-first processors give merchants more direct wallet ownership and fewer intermediaries. That can reduce counterparty dependence and suit technically strong teams. It also pushes more responsibility onto the merchant for treasury handling, reconciliation logic, and support workflows when payments arrive late, short, or on the wrong network.

Stablecoin-native models focus on operational consistency. Instead of maximizing every possible payout option, they narrow settlement to a predictable rail such as USDC. For many global internet businesses, that reduces hidden cost. Finance gets a cleaner ledger, treasury avoids repeated conversions, and developers spend less time building around edge cases. A practical example is the crypto payment processor model built around stablecoin settlement, which treats settlement design as a core product decision rather than a back-office afterthought.

Selection criteria have matured

Teams also screen providers with a broader set of stakeholders involved. Product wants a checkout that customers trust. Finance wants to know the settled amount without reverse-engineering fees and FX steps. Legal and operations want providers that help them streamline compliance in complex IT, especially across multiple entities, regions, and customer types.

This is why simple feature tables often miss the real decision. Two gateways can both accept crypto and still produce very different operating burdens once refunds, failed payments, conversions, and month-end close start piling up.

Familiar brands now face a harder test

NOWPayments still shows up on many shortlists because it is well known and supports a wide range of assets. That strength is real. It can also create complexity for businesses that do not want revenue arriving in many forms or teams making repeated conversion decisions after every payment cycle. The same scrutiny now applies to regional card processors, which is why teams evaluating a Razorpay alternative increasingly weigh settlement design rather than brand recognition.

The stronger processors in 2026 are not just easier to plug in. They are cheaper to run over time. The deciding factor is often whether the platform reduces settlement variance, conversion overhead, and developer maintenance, or instead moves those costs to another part of the business.

Core Comparison Criteria for Payment Gateways

A payment gateway should be judged as infrastructure, not as a widget. That means the evaluation has to go beyond checkout and into settlement, reporting, support burden, and implementation cost.

Payment acceptance is only the first layer

Start with the obvious part. What can the customer use to pay?

For some businesses, crypto acceptance alone is enough. For many online businesses, it isn’t. If you sell subscriptions, digital services, or community access globally, card acceptance matters because it broadens reach and lowers customer friction. A processor that only solves the crypto side may still leave money on the table if customers expect a familiar card checkout.

The second question is what the merchant receives. Customer choice and merchant settlement don’t have to be the same thing. In practice, separating those two layers often produces a cleaner operating model.

Settlement design affects daily operations

Settlement highlights the key trade-offs. Ask these questions early:

What asset does the business receive?

If the answer varies by customer payment choice, accounting gets harder.How predictable is the final settlement amount?

Predictability matters more than variety when you’re managing payroll, subscriptions, and vendor payments.How dependent is the flow on banking rails or manual conversions?

Every extra conversion step creates another point of delay or confusion.

A lot of teams underestimate this until month-end close. Then finance has to explain why gross payment volume, received funds, and usable treasury don’t line up cleanly.

Headline fees rarely reflect the real cost

Two gateways can post similar pricing and still create very different outcomes.

One may require extra conversion work, more support tickets, and more engineering effort. Another may look more expensive upfront but save time because the payout model is simpler and the reporting is cleaner. A useful evaluation looks at total cost of ownership, not just the first fee line on the pricing page.

Practical rule: If a provider’s fee is easy to understand but the settlement flow is hard to explain to your finance team, the cost model probably isn’t as simple as it looks.

Developer experience decides how expensive “simple” becomes

The best payment product for a buyer is often the one your engineering team can implement and maintain without constant exceptions.

Look for these practical signals:

Clear API structure: Can your team model orders, subscriptions, paylinks, and webhooks without custom glue everywhere?

Useful reporting exports: Finance and BI teams need data they can work with.

Support for recurring billing: This matters for SaaS, memberships, and retained services.

Operational tooling: Disputes, refunds, failed payment handling, and access changes should not require manual workarounds.

Match the gateway to the business model

A global SaaS company and a creator monetizing a Telegram group don’t need the same setup.

One needs recurring billing, robust reconciliation, and predictable treasury management. The other may care more about fast launch, paylinks, and automatic access control. The right nowpayments alternative depends less on the processor’s marketing language and more on how well its operating model matches your own.

NOWPayments vs Alternatives A Detailed Comparison

A finance lead closes the month and finds revenue spread across multiple assets, payout timings, and export formats. The posted processing fee looked reasonable. The operational bill showed up later in reconciliation time, conversion decisions, and engineering support.

That is the useful lens for comparing NOWPayments with alternatives. The question is not only which gateway accepts more coins. It is which operating model creates the lowest total cost once settlement, treasury handling, and developer maintenance are included.

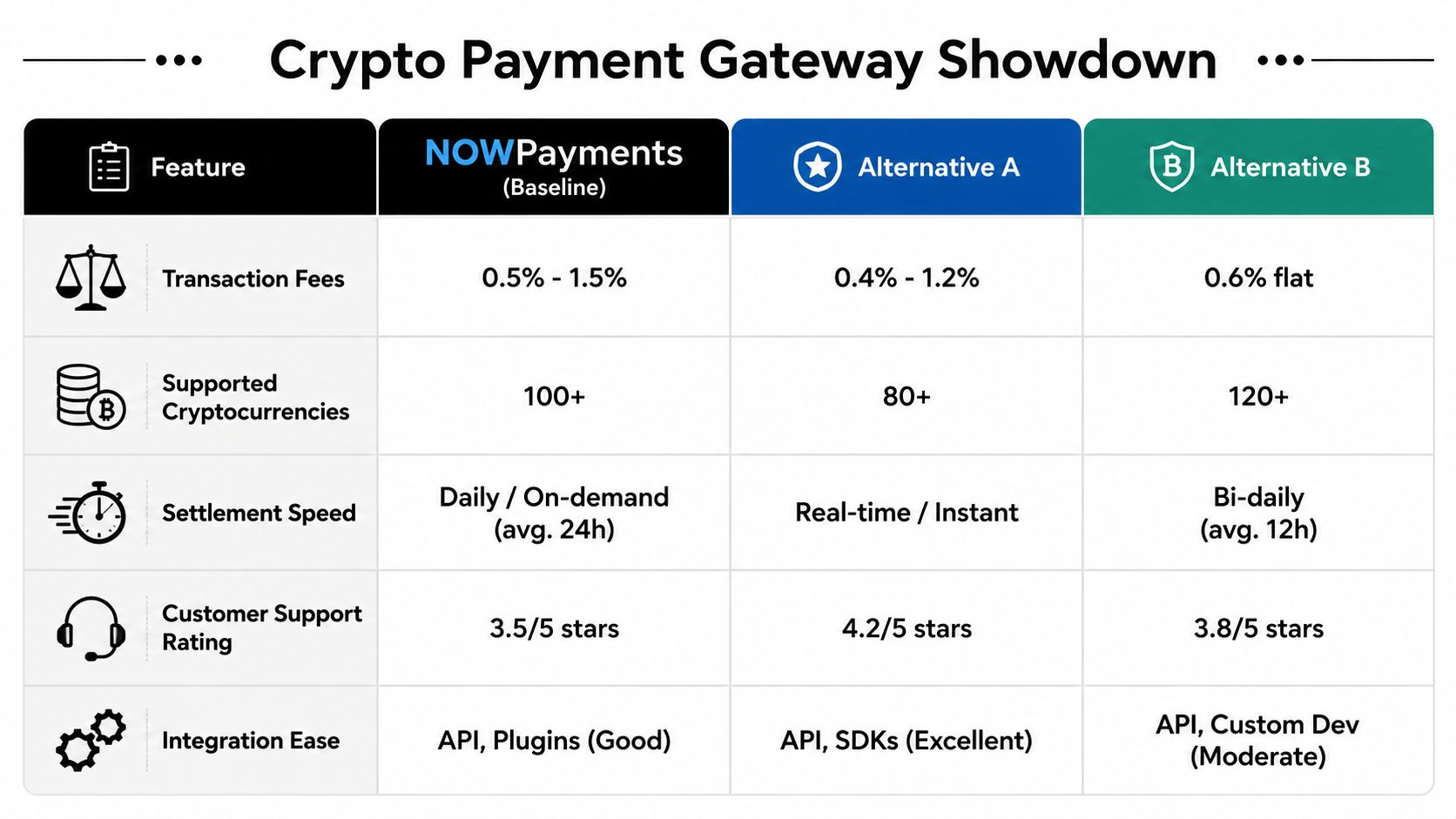

Payment Gateway Feature Comparison | NOWPayments | CoinGate | Suby |

|---|---|---|---|

Primary operating model | Broad crypto gateway | Crypto gateway with fiat conversion orientation | API for card or crypto acceptance with USDC settlement |

Customer payment methods | Crypto-focused | Crypto-focused with fiat conversion workflow | Card and crypto |

Merchant settlement emphasis | Flexible crypto acceptance | Fiat conversion and merchant familiarity | Businesses receive USDC |

Best fit | Merchants prioritizing wide asset support | Merchants that want closer alignment with fiat rails | Online businesses that want customers to pay with cards and businesses to receive USDC |

Operational trade-off | Flexibility can create extra treasury work | Fiat rails can add conventional payout dependencies | More opinionated settlement model |

NOWPayments as the baseline

NOWPayments is usually the reference point for one reason. It supports a wide range of crypto assets and gives merchants flexibility in how they accept payments.

That flexibility helps if your sales motion depends on buyer choice. It is less helpful if your finance team wants one predictable settlement outcome every time. In practice, broad asset support can shift work downstream. Someone still has to decide what to hold, what to convert, and how to reconcile mixed inflows against invoices and reporting.

Developer teams may also find that broad support is only part of the job. The real test is how cleanly webhooks, order states, exports, and exception handling fit existing billing systems. A gateway can look simple on the pricing page and still create custom logic that stays in production for years.

CoinGate for merchants that still think in fiat

CoinGate tends to fit companies that want crypto acceptance without changing their internal accounting habits too much. If treasury, bookkeeping, and tax workflows are still organized around fiat, that model can reduce operational change.

The trade-off is dependency on fiat conversion and payout rails. For some businesses, that is the right compromise because it shortens the path from payment received to books updated. For others, it adds another layer of timing, counterparties, and payout coordination that can matter more than the headline transaction fee.

This is a familiar pattern in payments. The provider that feels easier for finance can be harder on margin predictability, while the lower-fee option can create more internal handling. The right answer depends on where your team is already staffed and what kind of settlement variance it can tolerate.

A narrower settlement model for internet-native businesses

Some businesses want fewer choices and more consistency. That is the logic behind a platform such as Suby’s Coinbase Commerce alternative.

Suby offers an API for card and crypto payments, with merchant settlement in USDC, and it includes integrations for Discord and Telegram use cases. The practical distinction is not feature breadth. It is the narrower settlement model. For SaaS, digital services, and membership businesses, that can reduce treasury cleanup and make revenue flows easier to explain internally.

A narrower model also has a cost. It is more opinionated. Companies that need broad asset optionality or multiple payout paths may find it less flexible than a general crypto gateway.

The comparison point that actually changes cost

Teams often compare gateways by features and base fees, then discover later that reporting and reconciliation drive the bigger expense. I have seen this happen repeatedly with global software businesses. The pain rarely starts at checkout. It starts when finance asks why the same revenue stream lands in different forms week to week.

That is why gateway evaluation should sit next to data and reporting requirements. The more clearly a company defines how payment data needs to flow into finance and analytics, the easier it is to spot hidden implementation cost. The same discipline used in choosing the right BI tool applies here. Clean downstream reporting usually starts with a payment system that settles in a format the business can effectively use.

Pick the provider whose settlement model your finance, engineering, and support teams can operate without extra translation. That is usually the option with the lower real cost.

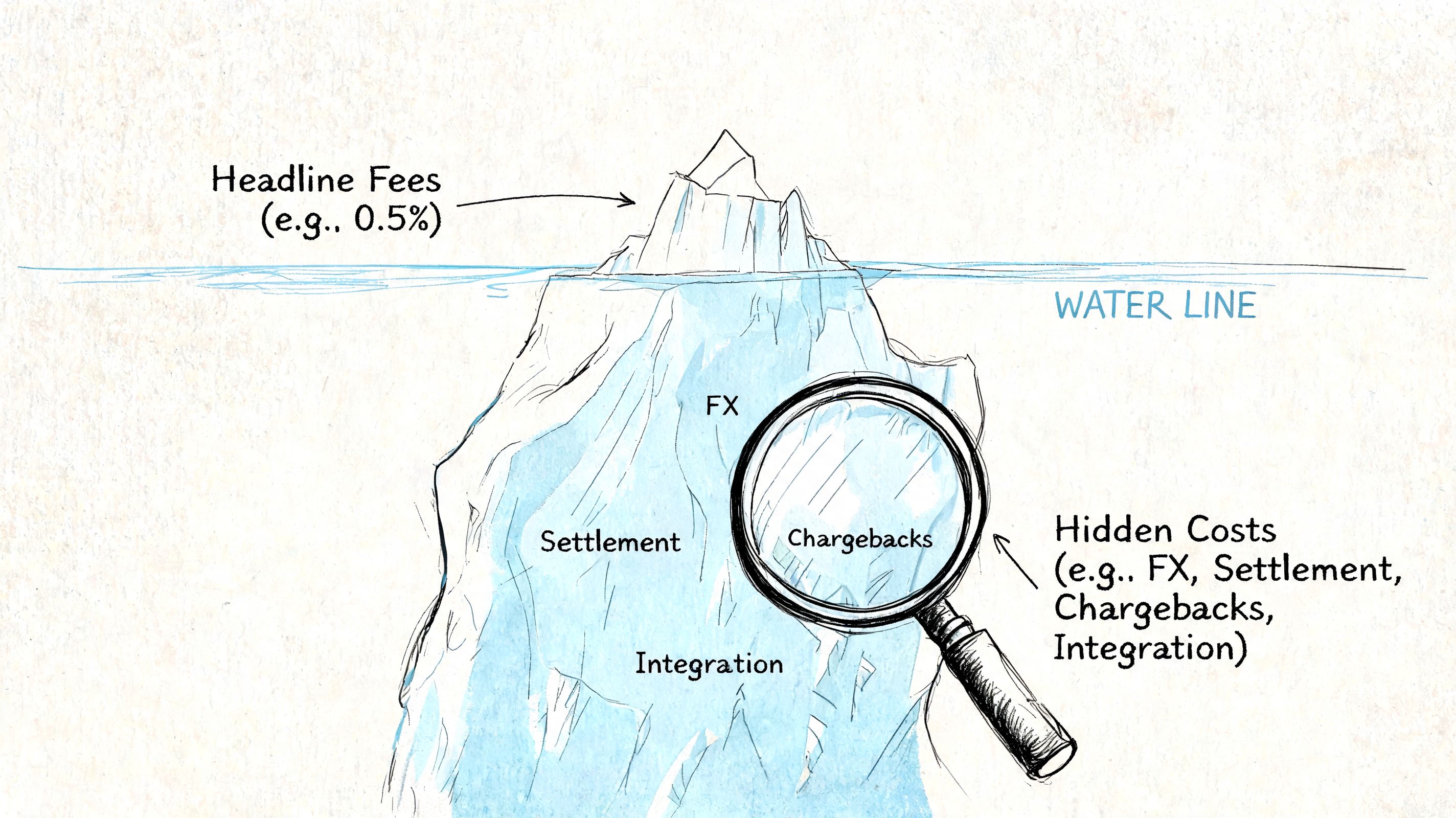

Analyzing the True Cost of Payment Processing

A finance lead approves a gateway because the fee looks lower on paper. Two months later, engineering is maintaining exception logic, support is chasing payout questions, and accounting is cleaning up asset conversions at month-end. That is how payment costs drift far above the posted rate.

A nowpayments alternative should be judged on total cost of ownership, not just transaction pricing. The costs that matter most sit below the posted fee. Settlement predictability, conversion exposure, reconciliation effort, and developer maintenance usually have a bigger effect on margin than a small difference in processor commission.

What sits below the posted fee

Hidden cost usually shows up in four places.

Conversion overhead: If customers pay in volatile assets but the business reports, budgets, or pays vendors in fiat or stablecoins, someone has to absorb and manage that conversion step.

Operational handling: Payment exceptions create support tickets, manual reviews, and payout follow-up. Those costs sit in headcount and response time, not on the pricing page.

Treasury inconsistency: Mixed-asset settlement makes revenue harder to forecast and harder to explain internally, especially for subscription businesses that need clean MRR reporting.

Developer maintenance: Edge cases do not disappear after launch. They become background work for engineers who should be focused on product, not payment cleanup.

Many gateway comparisons often fall short. They treat payment acceptance as the product and ignore the operating model that comes after the transaction clears.

Why predictability often beats a lower posted rate

For higher-volume SaaS and digital services companies, the better question is simple. What does it cost to turn customer payments into usable revenue every single week?

A gateway with a lower advertised fee can still be more expensive if settlement arrives in multiple assets, conversion timing is inconsistent, or finance needs manual reconciliation to close the books. I have seen teams save a fraction of a point on processing, then give it back through treasury handling and engineering time within the same quarter.

That is why a stablecoin-native model deserves serious consideration. If a provider settles in USDC by default, the business avoids part of the volatility, conversion uncertainty, and reporting noise that often follow broad crypto acceptance models. Suby's narrower approach is less flexible than a general-purpose processor, but it reduces the number of moving parts that finance and engineering need to support. That trade-off matters more than feature count for companies optimizing for operating efficiency.

If you want a practical breakdown of how listed fees diverge from day-to-day operating cost, this guide to payment gateway pricing for stablecoin-based businesses is a useful reference.

A posted fee is one input. The harder question is how much labor and variance sits between payment receipt and clean, usable revenue.

Here is the framework I use with payment teams during vendor reviews:

Cost layer | Questions to ask |

|---|---|

Processor fee | What is charged per transaction, and are there separate withdrawal or settlement charges? |

Conversion cost | Will finance need to convert assets after receipt, and who carries timing risk on that conversion? |

Operations cost | How many payment states, exceptions, and support issues need manual handling? |

Engineering cost | What custom logic, monitoring, and reconciliation work will the team still own after launch? |

This walkthrough gives a useful visual explanation of how hidden payment costs accumulate over time.

The lowest total cost often comes from the gateway that creates the least internal friction. Clear settlement, fewer conversions, and less exception handling usually matter more than shaving the headline fee. That is the standard to apply when evaluating any nowpayments alternative.

Choosing Your NOWPayments Alternative A Recommendation Framework

The best choice depends on the shape of your business, not on a generic top-five list.

For global SaaS companies

If you run subscriptions across multiple markets, focus on predictability first. You need recurring billing support, clean reporting, and settlement that doesn’t create treasury ambiguity.

NOWPayments can work if broad crypto acceptance is central to your customer strategy and your finance team is comfortable managing the downstream complexity. A more stable settlement-oriented option makes more sense if your internal goal is consistency rather than flexibility.

For e-commerce teams with existing fiat-heavy operations

A fiat-oriented provider like CoinGate is easier to defend when your accounting team wants familiar rails and your existing stack is built around fiat settlement. Teams migrating off a regional card processor for the same reasons often reach the same conclusion, which is a recurring theme in our take on a modern Moneymotion alternative. This path can be sensible if your business treats crypto as an extra checkout option rather than a treasury layer.

The limitation is that you may still inherit the delays and dependencies of more traditional settlement patterns. For some teams, that’s acceptable. For others, it defeats the point of modernizing payments.

For creators, communities, and internet-native businesses

This segment has different pressure points. Speed to launch matters. Access control matters. Customer payment flexibility matters. The cleanest setup is usually the one that combines payment collection with what happens after payment, especially for subscriptions and gated communities.

A stablecoin-settlement model is often the practical fit here because it removes the need to interpret multiple incoming payment forms. That’s especially useful when users pay with cards and the business wants the same treasury outcome every time.

If your product sells access, not just transactions, the payment provider should reduce manual admin after purchase, not create more of it.

A short decision filter

Use this when narrowing your shortlist:

Choose NOWPayments if wide crypto asset support is your main requirement and your team can absorb more payment operations internally.

Choose CoinGate if your business wants crypto acceptance but still prefers a fiat-oriented settlement posture.

Choose a stablecoin-native processor if your priority is one predictable merchant-side payout model across card and crypto payments.

That last category is often the most practical for companies selling globally online because it aligns checkout flexibility with simpler treasury handling. Users pay with cards, businesses receive USDC. That’s easier to operate than a mixed settlement stack.

Migration Checklist and Frequently Asked Questions

Switching processors is mostly an operations exercise. The technology matters, but the migration usually succeeds or fails based on how well you map your current payment flow before you touch production.

Migration checklist

Audit current payment flows: Document how customers pay today, how refunds work, where disputes are handled, and what finance exports each month.

List settlement requirements: Decide what your business wants to receive after every transaction.

Review developer docs before pricing: A lower fee won’t help if the API creates more custom work.

Test reporting early: Make sure finance can use the exports and webhook events without spreadsheet patchwork.

Plan customer communication: If checkout changes, update billing emails, help center articles, and internal support scripts.

Run parallel validation: Keep the old flow available during rollout long enough to verify settlement, reconciliation, and support handling.

Frequently asked questions

Does stablecoin settlement make accounting easier

It often does, because the business works from a more consistent settlement outcome. The main benefit is operational clarity. Finance teams spend less time interpreting mixed incoming payment forms.

What about disputes and refunds

You should check the provider’s documented workflow before migrating. For card acceptance, dispute handling and refund operations matter as much as checkout quality. If those processes aren’t clear in the documentation, expect support overhead later.

Is card-to-USDC practical for global businesses

Yes, especially for online businesses that sell internationally and want customer-side familiarity without merchant-side banking friction. The appeal is simple. Customers can pay with cards, while the business receives USDC in a predictable format.

Do Discord and Telegram use cases need a separate tool

Not always. If your business monetizes memberships, paid access, or private communities, it’s more efficient when payments and access management sit in the same system. That avoids manual updates and reduces failed-access support tickets.

If your team wants a simpler way to accept payments globally, Suby is a payment gateway and payment processor worth reviewing. Your customers pay with card, bank transfer, Apple Pay, Google Pay, Klarna, and more, or stablecoins, and you get paid out to your bank account, or directly in stablecoins (USDC, EURC) to your wallet, anywhere in the world, no bank account required. It also includes native Discord and Telegram integrations for subscriptions and paid access. As a NOWPayments alternative, the value is the predictable settlement rail: one merchant-side payout model instead of revenue arriving in scattered assets that finance has to reconcile every month.