Gaspard LEZIN

Stripe Connect Alternative: Compare Top Platforms

Find your Stripe Connect alternative. Compare top platforms, fees, global payouts, and APIs. Discover how USDC settlements simplify payments.

You usually don't start looking for a stripe connect alternative because of one bad week. It happens when the same issues keep showing up in operations. Payout timing gets harder to explain, cross-border revenue becomes messy to reconcile, and the simple pricing that felt fine early on starts eating margin.

That’s the point where payment infrastructure stops being a checkout decision and becomes an operating model decision.

For global SaaS companies, marketplaces, agencies, and creator businesses, the biggest problem often isn’t card acceptance itself. It’s what happens after the charge succeeds. Traditional fiat payout systems add conversion costs, banking delays, fragmented settlement, and a lot of manual handling that never shows up in the headline fee. If your customers are global but your payout stack still behaves like a domestic banking product, friction shows up everywhere.

A better alternative depends on what you need to optimize. Some businesses need enterprise acquiring and deep control. Others need broad local coverage. And some need a simpler model where users pay with cards, and the business receives USDC instead of waiting on bank rails. If your search is broader than just the Connect product, it helps to survey the wider field of alternatives to Stripe before committing.

Table of Contents

Where the pain usually starts

Why global payouts create more work than expected

Start with the money flow

Then check the operating model

Stripe Connect vs Adyen vs Suby a comparison

What each option fits best

How the flow works

Where it fits best

Headline fees hide the real bill

A better way to evaluate effective cost

SaaS subscriptions across many countries

Paid communities and creator memberships

Agencies and service businesses with global clients

Migration checklist

Choose based on the problem you need to remove

The Hidden Costs and Friction of Stripe Connect

A lot of teams stay with Stripe Connect longer than they want to because the initial setup is good enough. It’s widely known, developer-friendly, and it covers onboarding, identity verification, tax reporting, and payouts inside one system. But once a platform grows internationally, “good enough” starts carrying real cost.

Stripe Connect supports payouts to 46+ countries, and its standard blended pricing is 2.9% + $0.30 per transaction, which many platforms find expensive as volume grows, especially when compared with interchange-plus alternatives and broader global payout options, as noted by Routable’s review of Stripe Connect alternatives.

Where the pain usually starts

The first issue is rarely the visible fee. It’s the stack of small operational compromises around it.

A growing platform often ends up dealing with problems like these:

Margin compression: a blended rate is easy to understand, but it gets harder to justify when payment volume becomes meaningful and you still can’t shape pricing around different merchant profiles.

Payout unpredictability: finance teams want cleaner cash planning, while merchants want clarity on when money will arrive.

Cross-border drag: once sellers, contractors, or business owners sit in different countries, each payout workflow becomes harder to normalize.

Ecosystem lock-in: all-in-one convenience can become rigidity when you need a different payout model, wider coverage, or lower effective cost.

If you're trying to unpack what the fee line means in practice, this breakdown of Stripe fees for growing businesses is a useful companion read.

Practical rule: If your payment team spends more time explaining settlement than improving conversion, your current setup is already costing more than the invoice shows.

Why global payouts create more work than expected

Traditional fiat payouts create friction because each step depends on banking infrastructure, local rails, and currency handling. That means the checkout can feel modern while the settlement layer still behaves like an older financial workflow.

The hidden cost shows up in three places:

Friction point | What it looks like in practice | Why teams outgrow it |

|---|---|---|

Settlement timing | Different payout behavior by market and account setup | Harder forecasting and support overhead |

Currency conversion | Revenue collected in one currency, paid out in another | Margin leakage and reconciliation work |

Compliance handling | More onboarding and payout edge cases as footprint grows | Operations team becomes a payments team |

This is usually when the search for a stripe connect alternative gets serious. Not because the product failed, but because the business changed. A company serving global users needs a payout model that behaves consistently across borders, not one that keeps pushing complexity back onto finance, support, and product teams.

Core Features to Evaluate in a Payment Platform

Choosing a replacement gets easier when you stop comparing brands and start comparing operating models. A payment platform should match how your business earns, settles, and supports customers. If it doesn’t, the migration only swaps one problem for another.

Start with the money flow

The first filter is simple. Ask where money enters, where it settles, and what happens between those two points.

Some teams focus too much on checkout UX and not enough on settlement design. That’s a mistake. If the provider accepts payments cleanly but creates friction when you need to receive funds globally, you’ve only optimized the visible part of the system.

When reviewing options, look closely at these areas:

Fees and settlement model: You need more than a headline rate. Check whether the platform uses blended pricing, interchange-plus pricing, fixed monthly pricing, or an all-inclusive model.

Global reach: Coverage matters, but so does the payout method. A provider can support many countries while still making cross-border settlement operationally painful, which is why teams outside a single region often weigh a Razorpay alternative that settles the same way everywhere.

Currency handling: Ask whether you’ll keep dealing with conversion steps, banking intermediaries, and local payout edge cases.

A practical framework for that review is this guide to the best payment platform for international SaaS expansion.

Then check the operating model

Once the money flow makes sense, look at the day-to-day workload the platform creates for your team.

Onboarding and KYC: Fast onboarding matters, but so does flexibility. If sellers or business customers hit unnecessary friction, support tickets rise fast.

Developer experience: Good APIs and clear webhooks reduce long-term maintenance. Poor docs create hidden engineering cost.

Specialized tooling: Marketplaces need split payments. SaaS businesses need subscriptions. Creator businesses may need access control tied to payment events.

The right platform doesn't just process transactions. It reduces the number of manual exceptions your team has to handle every week.

Red flags are usually obvious once you know where to look. If pricing needs heavy negotiation before it makes sense, if settlement is still bank-first in a global business, or if onboarding forces users into rigid flows, the platform may fit the provider’s internal model better than your product.

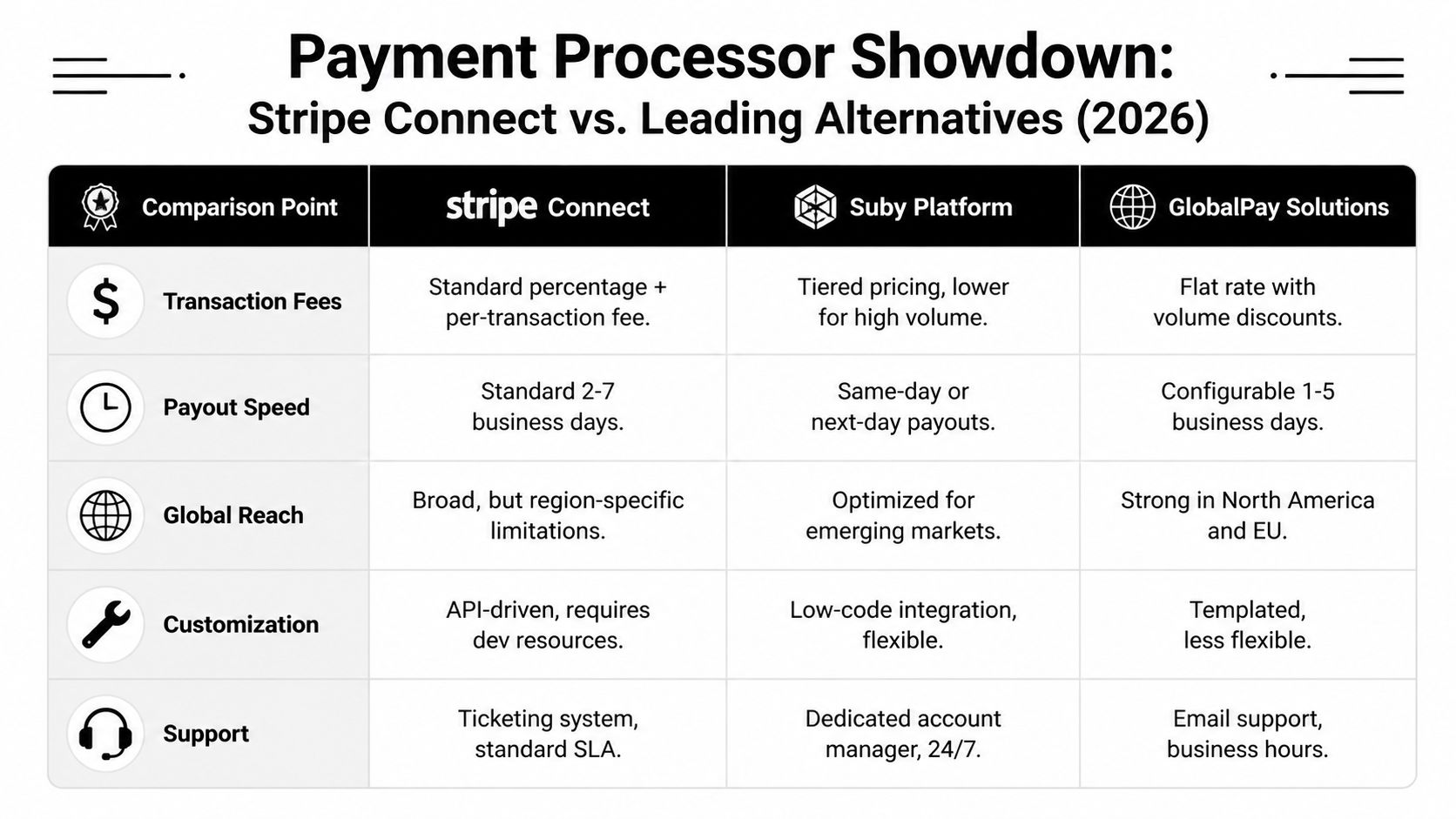

Stripe Connect vs Leading Alternatives in 2026

A familiar pattern shows up once a platform starts selling across borders. Checkout works. Revenue lands. Then finance starts chasing failed payouts, support starts answering settlement questions, and margins get thinner from FX spreads, banking fees, and reconciliation work that never appeared in the original pricing sheet.

That is the actual comparison in 2026. Stripe Connect is still a strong product for embedded payments. But many teams are no longer choosing between good and bad providers. They are choosing between operating models. One keeps payouts tied to the banking system. Another gives more acquiring control. Another settles directly in USDC and removes part of the fiat payout stack altogether.

A side by side view helps because these products solve different problems.

Feature | Stripe Connect | Adyen | Suby |

|---|---|---|---|

Core model | Embedded payments for platforms and marketplaces | Enterprise payments and acquiring | API for card or crypto acceptance with USDC settlement |

Pricing approach | Standard blended pricing in many common setups | Quote-based, often better suited to interchange-plus enterprise structures | All-inclusive pricing, depending on volume and setup |

Global payout orientation | Strong platform tooling, with payout constraints that become more noticeable in cross-border operations | Broad enterprise payment coverage with heavier implementation requirements | Built for global online sales with settlement directly in USDC |

Best fit | Platforms already deep in the Stripe ecosystem | Larger businesses needing enterprise control and omnichannel depth | Online businesses that want users to pay with cards and receive USDC |

Settlement style | Traditional fiat payout model | Traditional enterprise payout model | Customers pay with cards or selected crypto, businesses receive USDC |

Integration style | API-led | Enterprise integration and commercial process | API, webhooks, paylinks, embedded checkout |

Stripe Connect vs Adyen vs Suby a comparison

Stripe Connect still fits teams that want fast implementation inside a familiar developer stack. It handles onboarding, payment flows, and marketplace mechanics well. The friction usually appears later, once the business depends on cross-border payouts at scale and starts carrying the operational cost of bank rails, conversion steps, reserve logic, and exception handling.

Adyen serves a different buyer. It is better suited to businesses that treat payments as a core internal function and want tighter control over acquiring, routing, and enterprise payment operations. That can produce real gains, but it usually comes with a longer sales cycle, more implementation work, and a setup that smaller teams do not always have the headcount to support.

Suby addresses a different bottleneck. It lets customers pay by card or crypto while the business settles in USDC. For global internet businesses, that matters because the payout problem is often bigger than the checkout problem. If your team keeps losing time to banking delays, payout failures, and FX leakage, a USDC-based settlement model changes the economics more than another fiat processor with slightly different coverage.

It also changes treasury behavior. Instead of waiting for local bank settlement in each market, businesses can hold a digital dollar balance and decide when to convert, transfer, or deploy funds. That is a practical shift for SaaS platforms, marketplaces, and digital communities with global suppliers or creators.

For teams dealing with fragmented routing, risk logic, or category-specific payment constraints, this explanation of how payment orchestration helps high-risk businesses is worth reading because it frames the infrastructure question above the processor level.

What each option fits best

The choice usually comes down to where the friction sits today.

Choose Stripe Connect when your business benefits from one known ecosystem, your payout requirements are still manageable, and reducing implementation effort matters more than changing the settlement model.

Choose Adyen when payments are strategic enough to justify a heavier rollout, and your team needs stronger control over acquiring and enterprise payment operations.

Choose a model centered on direct USDC settlement when the primary problem is not card acceptance. It is the cost and complexity of moving fiat across borders after the payment succeeds.

If you are comparing those trade-offs directly, this breakdown of an alternative to Stripe for global online businesses adds a useful operator-level view.

A Closer Look at Suby's Payment Model

A familiar pattern causes the payout mess. A customer pays successfully, revenue lands in one country, then finance has to push money through local rails, absorb FX spreads, wait on banking cutoffs, and reconcile the delays afterward. For global SaaS platforms, creator businesses, and internet-native services, that back half is often where margin and time disappear.

Suby changes the settlement model itself. Its API lets a business accept payments by card or crypto and receive funds in USDC. Buyers still pay with methods they recognize. The business settles into a digital dollar balance instead of depending on bank-based fiat payouts market by market.

How the flow works

The practical difference shows up after the transaction is approved.

The customer pays at checkout with Visa, Mastercard, or supported crypto assets.

The business runs collection through one system rather than pairing card acceptance with a separate payout stack.

Settlement arrives in USDC to the business wallet, which removes several of the usual banking steps tied to cross-border fiat payouts.

That matters because the usual friction is operational, not theoretical. Finance teams no longer have to track bank transfer timing across regions, explain why one country settles faster than another, or absorb repeated conversion handling every time funds move. USDC does not solve every treasury question, but it does remove a large share of the payout complexity that traditional processors leave behind.

For a global online business, the cleanest payout model is often the one that removes the bank transfer from the critical path.

Suby also includes paylinks, embedded checkout, API integration, webhooks, one-time payments, and recurring subscriptions. That gives technical teams enough control to plug payments into an existing product, while smaller teams can start with paylinks and avoid building a custom billing layer on day one.

Where it fits best

This model fits companies that sell internationally and do not want their settlement process tied to old banking assumptions.

SaaS products with global customers: keep card checkout familiar for buyers, then settle revenue in USDC instead of managing multiple payout currencies and local banking dependencies.

Creators and community operators: use native Discord and Telegram integrations to tie payments to access for subscriptions or paid communities.

Agencies and service businesses: accept card payments from clients and hold proceeds in USDC without routing every payout decision through cross-border bank infrastructure.

Suby uses an all-in pricing model starting at 5 percent, as noted earlier. The trade-off is straightforward. The headline rate may look higher than a basic processor quote, but some businesses prefer one predictable fee over a lower advertised rate that grows once FX, payout handling, reconciliation work, and settlement delays show up in practice.

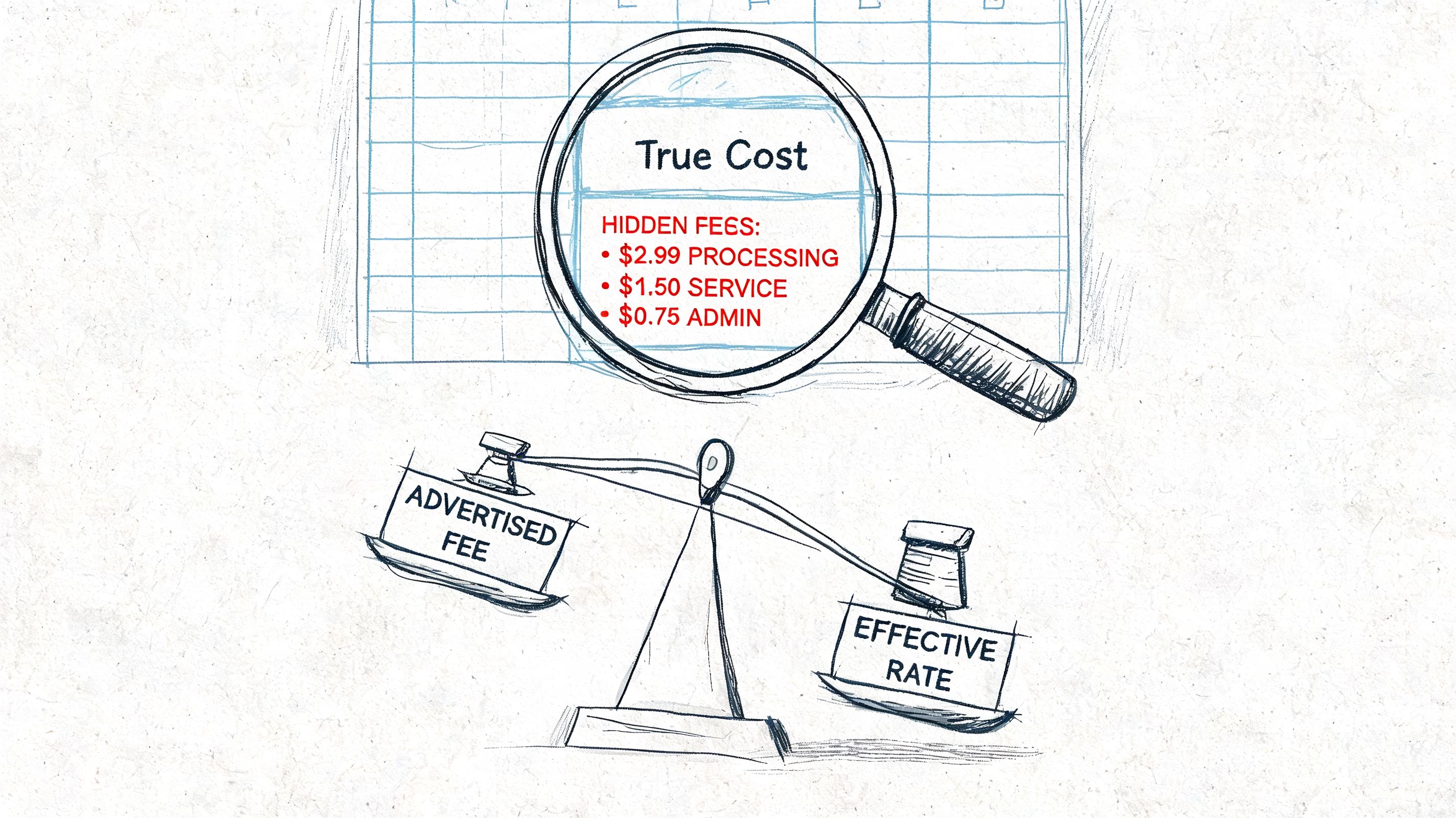

Analyzing the True Cost of Payment Processing

The advertised fee is the easiest number to compare, and often the least useful one.

When finance teams review payment cost, they tend to start with the processor rate because it’s visible on the invoice. But the true cost sits across multiple systems. Currency conversion, payout handling, reconciliation effort, delayed settlement, compliance overhead, and support work all affect what you ultimately keep.

Headline fees hide the real bill

A processor can look cheaper on paper and still cost more in practice.

That usually happens in three layers:

Direct cost: transaction fees, monthly platform charges, payout fees.

Indirect cost: FX spreads, cross-border transfer handling, conversion loss between collection and payout.

Operational cost: staff time spent on support, reconciliation, exception handling, and explaining settlement delays to customers or sellers.

Ryft’s 2026 comparison gives a useful real-world example of why this matters. In one case study, Tuft achieved a 62% reduction in processing costs after switching away from Stripe, driven by removing per-payout fees and avoiding Stripe’s typical 1-2% FX spread on cross-border transactions, according to Ryft’s marketplace payments analysis.

That example matters because it shows where many teams underestimate cost. They compare only the processing fee and ignore the layers around it.

Cost check: If money crosses borders, the payout model matters almost as much as the acceptance model.

A better way to evaluate effective cost

A cleaner evaluation is to map one payment from customer to final settlement and document every step where cost or delay appears.

Use a checklist like this:

Where is the customer charged? Card, wallet, transfer, or another method.

What currency is collected? This affects downstream conversion handling.

How does settlement happen? Bank payout, local rail, or direct wallet settlement.

Who touches the payment operationally? Finance, support, compliance, or engineering.

How often do exceptions happen? Refunds, failed payouts, manual reviews, or edge cases.

This walkthrough gives a good visual explanation of why payment cost analysis has to go beyond the processor fee.

The key point is simple. A lower nominal rate does not guarantee a lower effective rate. For global businesses, the cheapest system is often the one that removes the most moving parts after the payment succeeds.

Use Cases for Global and Digital-Native Businesses

The easiest way to judge a stripe connect alternative is to stop thinking like a buyer of software and start thinking like an operator. What matters is whether the payment model reduces friction in the business you already run.

SaaS subscriptions across many countries

A SaaS company selling internationally usually wants a normal card checkout for customers and a clean revenue flow on the back end. Traditional payout models often create work after the sale. Finance has to track currencies, reconcile different settlement patterns, and explain why collections are global but payouts still feel local and fragmented.

A card-to-USDC settlement model changes that. The buyer still pays in a familiar way, but the business receives USDC. That makes the payout side more consistent for a company serving users across many markets without wanting to build its own global treasury workflow.

Paid communities and creator memberships

This use case is often ignored in payment comparisons because it doesn’t look like a classic marketplace or SaaS stack. But creators and community operators have the same global settlement problem, just with less back-office capacity to handle it.

For a paid Discord or Telegram community, the practical need is simple. Collect subscription revenue, grant or revoke access automatically, and avoid manual admin every billing cycle. Sellers who outgrew a storefront tool often look at a SellHub alternative for the same reason: they want global card payments paired with USDC payouts in one place. When the payment layer and access management sit in the same system, operators spend less time cleaning up failed renewals and less time matching payments to memberships.

A creator business doesn't need more financial plumbing. It needs one system that turns payment status into access status.

Agencies and service businesses with global clients

Agencies often have a different pain profile. They’re not managing thousands of sellers, but they are dealing with international invoices, client payment preferences, and settlement lag that feels out of proportion to the job size.

When clients can pay by card and the business settles in USDC, the team avoids a lot of the delay and uncertainty that comes with cross-border bank transfers. For agencies paid from different continents, that can simplify cash collection without forcing clients into unfamiliar payment behavior.

The common thread across all three cases is straightforward. Customers keep a familiar checkout experience. The business gets a more predictable settlement path.

Your Migration Plan and Final Decision Framework

Migration gets easier when you treat it like an operating change, not just a vendor switch. The businesses that handle this well usually start by documenting their current payment flow in plain language. How customers pay, where money lands, who reconciles it, and where support pain shows up.

Migration checklist

Before moving away from your current setup, check these items:

Map your real workflow: Document checkout, settlement, refunds, disputes, and reporting as they work today.

List hidden costs: Include FX handling, payout timing issues, manual reconciliation, and support overhead.

Audit dependencies: Note billing logic, webhooks, merchant onboarding flows, and any tooling attached to payment events.

Plan customer communication: If invoices, checkout pages, or payout expectations change, tell users early.

Run a controlled rollout: Start with a contained segment before moving your whole volume.

Choose based on the problem you need to remove

This is the simplest framework I’ve found useful:

Choose Stripe Connect if you still want one familiar platform stack and your biggest concern is staying inside a well-known ecosystem.

Choose Adyen if your business has enterprise payment requirements, deeper acquiring needs, and the internal resources for a larger implementation.

Choose a card-to-USDC model if your core problem is global payout friction, currency conversion drag, and dependence on slow banking rails.

The wrong decision is usually the one that optimizes the checkout while leaving the settlement problem untouched.

Suby is a payment gateway and payment processor. Your customers pay with card, bank transfer, Apple Pay, Google Pay, Klarna, and more, or stablecoins, and you get paid out to your bank account, or directly in stablecoins (USDC, EURC) to your wallet, anywhere in the world, no bank account required. If your business wants customers to pay with cards while your team gets paid out to a bank account, or in stablecoins (USDC, EURC) to a wallet, with a simpler global settlement flow, Suby is built for that model. It offers an API, recurring subscriptions, paylinks, and webhooks, plus native Discord and Telegram integrations for paid access, so a Stripe Connect alternative fixes the payout problem, not just the checkout.