If you ask ten founders what makes a payment processor reliable, most will talk about uptime, subscription features, and API quality. Those matter. But they don't answer the harder question. How reliably does your revenue arrive in a usable form once customers have paid?

That gap is bigger than most buying guides admit. Many SaaS payment comparisons focus on feature checklists and developer convenience, but rarely address reliability under cross-border, multi-currency, and payout-friction stress, even though a processor can look strong at checkout while creating hidden operational friction after payment capture, as noted in Fueler's review of SaaS payment processors. For an international SaaS startup, that's where reliability becomes a finance issue, not just a checkout issue.

A processor isn't reliable if your team spends hours reconciling currencies, waiting on delayed payouts, or guessing what settlement will look like in practice.

Table of Contents

- Global SaaS with a distributed team

- Companies selling into harder banking environments

- Paid communities and recurring access

- Operators who optimize for cash control

- How are disputes handled if the business receives USDC

- Is accounting harder when revenue settles in USDC

- Why accept both card and crypto if the goal is simple operations

What Does a Reliable Payment Processor Truly Mean

The usual definition of reliability is too narrow. Founders hear it and think system uptime, clean APIs, and support for subscriptions. In real operations, reliability means something stricter. It means your payment stack turns sales into predictable working capital without adding friction after the transaction is approved.

That's the missing layer in most comparisons. The processor may accept the payment just fine, but your finance team still deals with payout timing, reconciliation issues, currency conversion, and settlement uncertainty. Those aren't side issues. They shape hiring, vendor payments, and runway management.

Reliability starts after authorization

A global SaaS company doesn't just need a processor that can charge cards. It needs one that can move money across borders with as little operational drag as possible.

Three questions matter more than most founders initially think:

- How predictable are payouts: If payout timing feels inconsistent, cash planning gets harder fast.

- How much friction appears after checkout: FX conversion, reserve policies, manual reviews, and banking dependencies can turn accepted revenue into delayed revenue.

- How much control does finance have: A startup needs visibility into when funds settle and in what currency they arrive.

Practical rule: Don't evaluate a processor only on acceptance. Evaluate it on the full path from customer payment to spendable funds.

It's a common trap for many teams. They buy for developer speed and only later discover operational complexity. If you want a practical look at those issues, this guide on common pitfalls with global payment processors is worth reading because it focuses on the problems that appear after launch, not just during integration.

The real standard for a global SaaS

For a domestic company billing in one currency, traditional settlement friction can stay manageable for longer. For an international SaaS startup, it compounds quickly. You may collect revenue in one set of markets, settle in another, and run payroll or contractor payments somewhere else entirely.

A processor becomes more reliable when it reduces that spread between payment acceptance and usable money. That doesn't always mean the biggest brand wins. It often means the business model, geography, and treasury setup are aligned with the processor's settlement design.

The Six Pillars of Payment Processor Reliability

A good buying process needs a framework. Without one, teams compare glossy features and ignore the mechanics that affect cash flow every week.

Reliability starts after authorization

The first pillar is operational uptime and authorization quality. If payments fail at checkout, everything else is irrelevant. This is the visible part of reliability, and it's usually what vendors emphasize first.

The second pillar is settlement and payout predictability. A startup can survive a slightly less elegant dashboard. It won't enjoy unclear settlement behavior, payout delays, or fragmented money movement. Reliability means finance can plan around known flows.

The third is currency and FX management. Selling globally is easy to describe and much harder to settle cleanly. The more currencies you accept, the more exposed you become to conversion friction, reconciliation complexity, and margin leakage.

The six pillars in practice

The fourth pillar is developer experience and integration quality. This still matters. Bad documentation, limited webhooks, and rigid checkout flows slow teams down and create maintenance risk.

The fifth is compliance, disputes, and risk handling. SaaS founders often underweight this until chargebacks, authentication failures, or account reviews start affecting revenue. A processor needs workable controls, not just marketing language.

The sixth is pricing transparency. Not just headline processing cost. Real transparency means understanding where the money goes across acceptance, conversion, settlement, and payout.

Here's the short version I use when advising founders:

- Checkout reliability: Can the processor support consistent payment acceptance in the markets you care about?

- Cash reliability: Do funds arrive in a form and timeline your business can use?

- Operational reliability: Can your product, finance, and support teams work with the system without extra manual overhead?

Reliability isn't one feature. It's the absence of surprises across the full payment lifecycle.

Founders looking for the most reliable global payment processor for a SaaS startup should score every option across all six pillars, not just the ones visible in a demo.

Comparing Traditional Global Payment Processors

The traditional leaders are strong for good reasons. They've spent years building broad acceptance, compliance infrastructure, and enterprise relationships. But they don't all solve the same problem, and they don't create the same kind of reliability for a startup selling internationally.

Traditional Processor Comparison

| Processor | Best For | Settlement Model | Key Friction Point |

|---|---|---|---|

| Stripe | SaaS teams that want strong developer tooling and subscription workflows | Traditional processor settlement to bank-linked payout flows | Cross-border payout and FX friction can become harder to predict as the business expands |

| Adyen | Larger companies that need deep payment infrastructure control | Enterprise-oriented bank-based settlement with direct acquiring advantages | Powerful, but often too operationally heavy for early-stage startups |

| Worldpay | Established businesses that value scale and long operating history | Traditional global merchant settlement through banking rails | Broad coverage, but typically less flexible for lean product teams |

Stripe

Stripe is the default recommendation in many SaaS discussions, and that's not hard to understand. Stripe presents itself as a unified payments platform for scaling startups and global enterprises, with availability in 195 countries and support for 135+ currencies, and it's described as trusted by brands such as DocuSign, Amazon, and Shopify in Stripe's SaaS payment processing guidance. That combination signals broad market acceptance and strong operational maturity.

For many startups, Stripe works well because it combines recurring billing infrastructure with international payment support, currency conversion, PCI-DSS compliance, and subscription-oriented tooling, which are highlighted in SwipeSum's overview of SaaS payment gateways. If your main goal is launching quickly with a familiar developer stack, it's a sensible choice.

The trade-off is that checkout strength doesn't automatically mean payout simplicity. Once a SaaS business starts selling across multiple regions, teams often care less about whether the processor can accept a card and more about how cleanly money settles afterward. That's where hidden FX spreads, payout timing, and banking dependencies start affecting the operating model.

For teams selling in Europe, it also helps to understand local collection choices early. This breakdown on choosing SEPA payment methods is useful because it highlights how payment method selection affects collection flow, customer experience, and back-office work.

Adyen

Adyen sits in a different category. It's built for businesses that want more direct control over payment infrastructure. Finix's processor comparison describes Adyen's value as coming from direct acquiring relationships, global market coverage, and authorisation-rate optimisation, which makes it attractive for companies with meaningful scale and payment operations sophistication, as outlined in Finix's guide to SaaS processors.

That infrastructure can be a serious advantage if you have a payments team, complex routing needs, or regional acquiring strategy. A larger platform might benefit from exactly that depth.

A startup usually experiences the other side of the equation. More control often means more operational complexity, more internal ownership, and a longer path from integration to stable day-to-day execution. If your core problem is primarily getting paid globally with minimal payout friction, Adyen can be more than you need.

The best enterprise payment architecture often isn't the best startup payment architecture.

Worldpay

Worldpay represents the historical model of reliability at scale. Chargebee's SaaS gateway comparison describes Worldpay by FIS as supporting over one million merchants worldwide, 300+ payment methods, and 126 currencies, which is strong evidence of broad global processing capability in the traditional system, according to Chargebee's payment gateway guide.

That scale matters. A processor serving that many merchants across so many methods and currencies has deep operational reach. For some businesses, especially established enterprises, that kind of history is reassuring.

The downside is practical. Legacy scale doesn't always translate into founder-friendly simplicity. A startup may value broad coverage, but it also needs clarity, speed of execution, and less settlement ambiguity. Worldpay can be powerful, yet still feel distant from the needs of a lean SaaS team that wants tight control over how revenue lands and how fast it becomes usable.

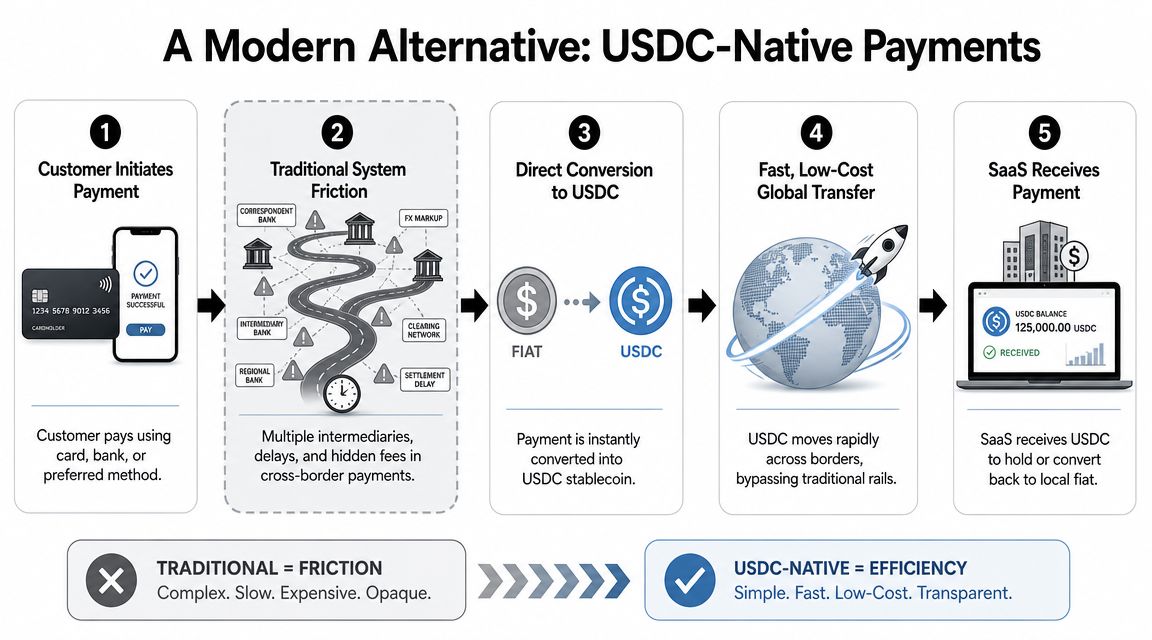

A Modern Alternative USDC-Native Payments

The biggest weakness in traditional processor selection is that the common approach involves comparing acceptance features while leaving settlement architecture unchallenged. If revenue still moves through the same slow, fragmented banking paths, a modern checkout can hide an old payout model.

Why settlement design matters

A USDC-native model changes the evaluation criteria. Instead of asking only how well a processor accepts payments, ask how directly it can turn revenue into a stable digital dollar balance the business controls.

Some enterprise-grade options are intentionally built around deep infrastructure control. Finix positions both itself and Adyen around functions like sponsor-bank relationships, compliance, underwriting, risk monitoring, pricing, and sub-merchant management, while also noting that this level of control can be overly complex for startups that mainly need fast, reliable payouts in practice, as discussed in Finix's infrastructure-focused comparison.

That creates room for a different design. Customers keep paying in familiar ways, such as card or supported crypto, and the business receives USDC instead of waiting on traditional bank-based settlement to shape the final outcome.

How the model works in practice

Here's why this can be more reliable for a global SaaS:

- Settlement becomes more predictable: You're not building treasury around fragmented local payout behavior.

- Currency handling gets simpler: Revenue lands in one digital dollar unit instead of bouncing through multiple banking conversions.

- Global operations become easier to coordinate: Teams can manage funds without needing a patchwork of foreign bank accounts.

Suby is one example of this model. It provides an API that lets businesses accept payments by card or crypto, while the business receives settlement in USDC. It also supports recurring subscriptions, paylinks, checkout embeds, webhooks, and native Discord and Telegram integrations for paid access and online communities. The practical point is simple. Users pay with cards, businesses receive USDC.

A short walkthrough helps if this model is new to your team:

This approach doesn't make every other processor obsolete. It solves a different problem. If your startup values bank-centric workflows, traditional settlement may still fit. If your pain sits in payout timing, FX friction, and capital trapped in legacy rails, USDC-native settlement is often the cleaner answer.

Operator view: The right question isn't "Can this processor accept payments globally?" It's "How many steps sit between customer payment and money my business can use with confidence?"

When to Choose a USDC-Native Processor

What makes a processor reliable for a global SaaS. Wide card acceptance, or getting usable cash to the business without FX leakage, payout delays, and banking workarounds?

Global SaaS with a distributed team

USDC-native settlement starts to make sense when finance is spending too much time cleaning up the side effects of getting paid. A SaaS company can sell across regions, pay contractors in multiple countries, and still run a small back office. Traditional settlement often turns that into manual treasury work, with separate payout rules, local banking dependencies, and extra conversions between the customer payment and the cash the company can use.

A USDC-settlement model fits best when the business wants one predictable unit for revenue, faster access to funds, and fewer operational steps after checkout.

That matters even more for early-stage teams managing runway. Founders talking to leading SaaS investors for startups usually get asked about growth efficiency. Payment operations rarely show up in the deck, but hidden settlement costs still drag on margins and cash planning.

Companies selling into harder banking environments

Traditional processors can still be the right choice if the main priority is bank-based coverage in established corridors. The trade-off appears after payment capture. Some markets have uneven payout rails, slower banking cycles, or more expensive currency conversion paths. A processor may approve the charge successfully and still leave the business waiting, converting, and reconciling.

USDC-native settlement is a stronger fit when customer geography is broad but banking quality is inconsistent. The benefit is less about checkout novelty and more about reducing dependence on each local corridor to deliver funds cleanly.

Paid communities and recurring access

This model also fits businesses that sell recurring access outside a standard SaaS app. Operators running paid communities, education products, private groups, or membership programs often need billing, access control, and settlement to work together without extra tooling between them.

That is where products like Suby are practical. The appeal is not branding. It is the operating model. A customer can pay through familiar methods, while the business settles in USDC and keeps subscription revenue in a form that is easier to track and redeploy.

Operators who optimize for cash control

The strongest signal is usually treasury discipline.

If the founder or finance lead cares about how quickly revenue becomes usable, how often funds get clipped by FX spreads, and how much manual reconciliation sits between payment acceptance and deployment, a USDC-native processor deserves serious consideration. This is often the better fit for startups that are global by default and want reliability defined by total cost of ownership, not just processor logos on a pricing page.

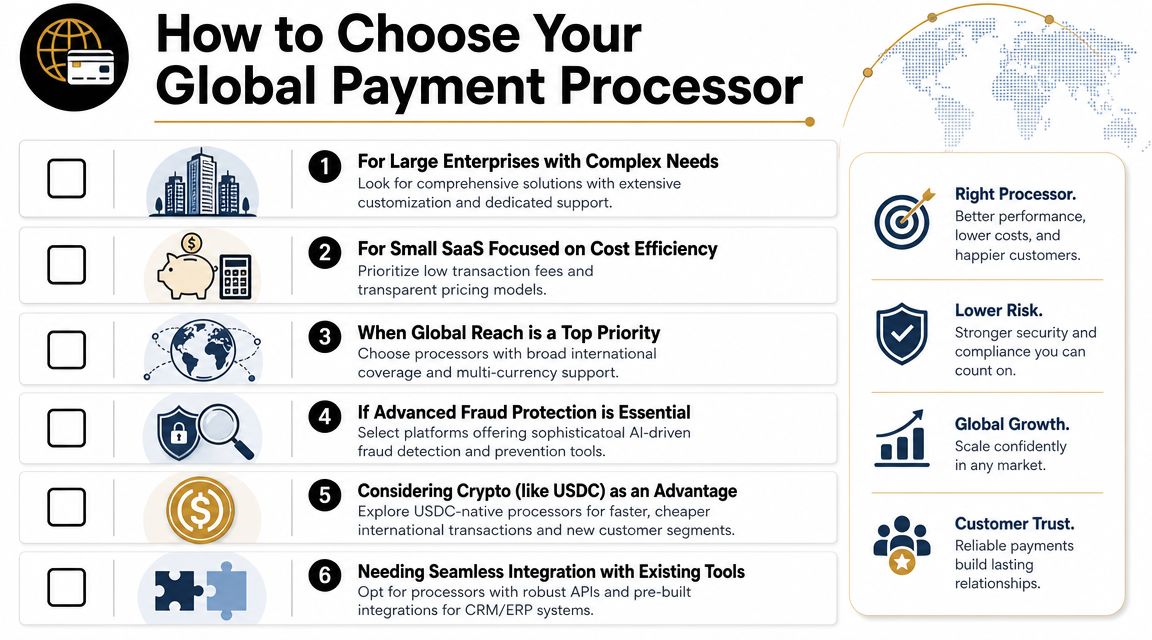

How to Choose Your Global Payment Processor

A good decision starts with your operating model, not the vendor homepage.

A practical decision framework

Choose an enterprise processor if your company needs direct acquiring depth, internal payment operations control, and dedicated optimization across regions. That profile often aligns better with larger organizations than startups.

Choose a developer-first traditional processor if your priority is fast deployment, broad ecosystem support, and standard SaaS billing flows. That can still be the right answer for a company with relatively simple treasury needs.

Choose a USDC-native processor if your business is global by default, wants predictable settlement, and doesn't want FX and banking friction sitting between payment capture and usable cash. If you're also comparing implementation paths, this guide helps understand payment integration complexities before you commit engineering time.

What to prioritize first

Use this shortlist:

- Your revenue geography: Where customers pay from matters less than how revenue settles afterward.

- Your treasury tolerance: If finance can absorb banking friction, traditional processors stay viable longer.

- Your internal resources: More infrastructure control can be valuable, but only if your team can operate it.

- Your expansion path: If international growth is core to the model, use a processor built for cross-border settlement simplicity.

If you're evaluating options for cross-border growth specifically, this guide to the best payment platform for international SaaS expansion is a useful next read because it looks at processor choice through expansion risk, not just checkout features.

For the founder searching for the most reliable global payment processor for a SaaS startup, the answer isn't universal. But the pattern is clear. Reliability today is less about who can accept a card, and more about who can deliver revenue with the least friction, the fewest surprises, and the most control.

Frequently Asked Questions

How are disputes handled if the business receives USDC

If the customer pays by card, dispute handling still needs to be treated like professional card payment operations. The settlement asset changes the treasury side of the flow. It doesn't remove the need for proper dispute management, evidence handling, and customer support processes.

Is accounting harder when revenue settles in USDC

For many teams, it's mostly a workflow decision. The key is to set a clear internal policy for how finance records USDC receipts, reconciliation, and any later conversions or treasury movements. Talk to your accountant early so the treatment is consistent from the start.

Why accept both card and crypto if the goal is simple operations

Because customer preference and internal settlement don't need to be the same thing. A business can widen payment acceptance while keeping one cleaner settlement output internally. That's often a better setup than forcing customers into a single payment method.

If you're fundraising for a SaaS company while redesigning billing infrastructure, this list of leading SaaS investors for startups can also help you identify investors who already understand subscription businesses and operational scaling.

If your team wants a payment stack where customers can pay by card or crypto and your business receives USDC, Suby is built for that model. It offers an API, checkout flows, recurring subscriptions, paylinks, and native Discord and Telegram integrations for paid access and online communities. For global internet businesses that care about predictable settlement more than legacy banking complexity, it's a practical option to evaluate.