How do you pick a digital product idea that can make money beyond your home market from day one?

The idea matters, but payment setup decides how far it can go. A SaaS tool, paid community, template pack, or invoicing product can all sell globally if buyers can pay with the methods they trust and you can collect revenue without adding five separate tools to your stack.

That is the angle of this guide. Each idea comes with a practical monetization blueprint, not just a concept. The focus is simple: how to launch, what to charge for, and how to accept both card and crypto payments through one platform instead of stitching together a checkout app, a crypto plugin, a gating bot, and a billing system.

Suby fits that model directly. It gives businesses one API for card and crypto payments, plus built-in tools for Discord and Telegram access, recurring billing, and invoicing. In practice, that means you can test a product faster and keep operations simpler as volume grows. If you need context on the payment side before choosing a model, this guide on how to accept international payments is a useful starting point.

The sections below focus on ideas with clear buying behavior and a direct path to revenue. That includes subscription products, community access, digital downloads, invoicing flows, marketplaces, and developer-first payment layers. The common trade-off is straightforward. The more countries you want to sell into, the less room you have for a fragmented checkout.

Table of Contents

1. Global Payment Checkout for SaaS Platforms

What breaks first when a SaaS company starts selling internationally? Usually the checkout.

Teams can ship a strong product and still lose revenue at the payment step because the buying flow does not match how customers want to pay. One buyer wants a card. Another needs crypto. Finance wants settlement in one place. Ops wants fewer manual fixes. If those pieces live in separate tools, billing turns into a patchwork.

Suby gives SaaS companies one checkout for card and crypto payments, with funds routed into a single balance and payouts sent to a bank account or in stablecoins such as USDC. That creates a practical business model from day one. You can sell in more markets without building separate payment flows, and you can choose how you receive funds based on treasury needs, accounting setup, or payout speed.

Why this idea works

Software buyers already expect to complete a purchase online. The friction is no longer product education alone. It is whether the checkout supports the buyer's preferred payment method and whether the seller can settle those payments cleanly.

This idea fits B2B SaaS sold across multiple countries, usage-based tools, subscription products, and platforms that need one customer-facing checkout with flexible back-end settlement. It is especially useful for founders who want to accept global card payments now, add crypto for specific customer segments, and avoid rebuilding billing each time they enter a new market.

The monetization angle is straightforward. Charge monthly or annual subscriptions, sell setup or onboarding fees, add usage-based billing for teams with variable spend, and test higher-priced plans in regions where procurement is slower but contract value is higher. A unified checkout helps because it removes the usual split between "card revenue" and "crypto revenue." The customer chooses how to pay. The business chooses how to receive funds.

How to launch it without overbuilding

Start with the lightest version that can collect money reliably. For many SaaS companies, that means paylinks first, then an API integration after pricing, packaging, and renewal logic settle down.

Use this rollout order:

- Sell before you rebuild billing: Use paylinks for early deals, pilot customers, or manual closes.

- Connect payments to access control: Wire webhooks into your app so successful payments, failed renewals, and cancellations update account status automatically.

- Offer both payment rails early: Test card and crypto at launch if your customer base is international. Preference varies more than teams expect.

- Choose settlement deliberately: Receiving card payments as USDC can help if your company already manages vendor payments, treasury, or reserves in stablecoins. If accounting is simpler in fiat, route payouts to the bank account instead.

- Track one operating view: Keep payments, subscriptions, churn, and payouts in one dashboard so support and finance are not reconciling data across separate systems.

I have seen teams overbuild billing logic before they confirm what customers will buy. A simpler launch usually wins. Get the checkout live, learn which payment methods close deals faster, then add the deeper integration work.

For a practical breakdown of cross-border setup, taxes, and payment flow decisions, read this guide to accepting international payments.

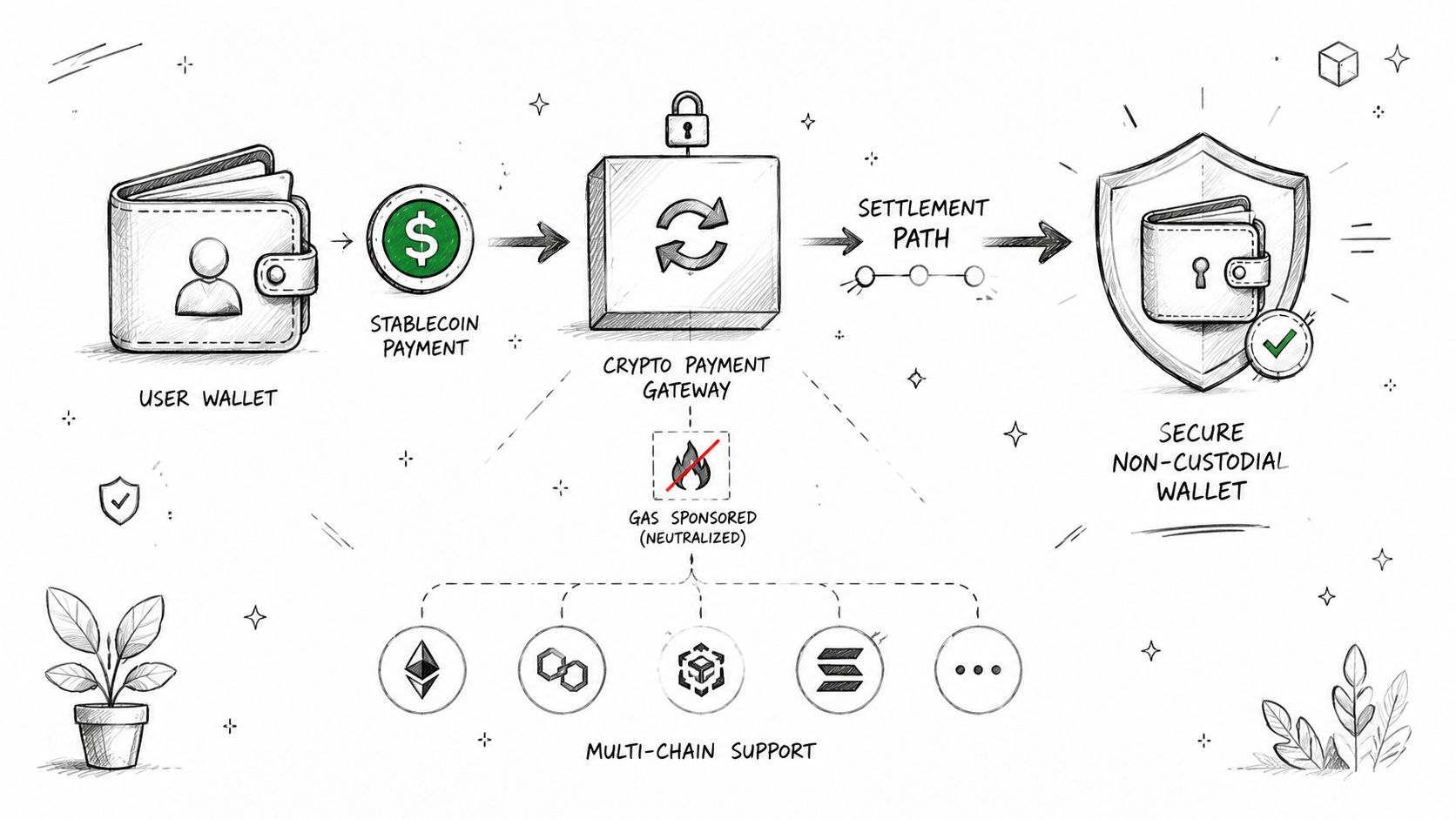

2. Crypto Payment Gateway for Web3 Applications

Some products attract users who already live in wallets. For those products, forcing a card-only flow is friction you don't need.

Suby Crypto is one of the four ways to use Suby. It acts as a crypto payment gateway that handles the swap, sponsors the gas, and settles to a non-custodial wallet or to the Suby balance. That matters because the buyer gets a cleaner checkout, while the business avoids building chain-specific complexity from scratch.

Where this fits best

This works well for crypto software, digital collectibles platforms, on-chain memberships, and treasury-funded communities. The strongest demand usually comes from products with international users who don't want banking friction.

Stablecoins now account for nearly 60% of total crypto payment activity and 52% of transaction volume, according to SQ Magazine's crypto payments industry statistics. That's why many teams prefer settlement in USDC or another stable asset instead of holding volatile tokens.

Practical rule: Don't sell crypto payments as novelty. Sell them as a faster, cleaner way for the right users to complete the purchase.

What to get right in the flow

If you're building this type of product, the details matter more than the headline feature.

- Show clear pricing: Use real-time swap visibility so users understand what they'll pay before confirming.

- Reduce friction: Gas sponsorship removes one of the most annoying steps for non-technical buyers.

- Protect treasury operations: If you don't want token exposure, settle to your chosen destination instead of holding everything in whatever asset the customer used.

- Display status updates: Confirmation screens and live transaction states reduce support tickets fast.

A short walkthrough helps clarify the experience:

3. Paid Community Access for Discord and Telegram

Private communities are one of the most overlooked digital product ideas because creators often treat them like audience-building channels instead of products. That's a mistake. If the community solves a clear problem, people will pay for access.

Suby Gating is built for this use case. It lets you gate Discord, Telegram, downloads, and courses behind a paywall, and Suby also offers native integrations with Discord and Telegram. Members can pay by card or crypto, and access can be granted automatically.

What people actually pay for

People rarely pay for “community” in the abstract. They pay for outcomes. That could mean deal flow, mentorship, niche research, templates, accountability, or faster access to people with hard-won experience.

There's also a clear content gap in the market. Mirasee's article on digital product ideas highlights how mainstream guides still focus on generic templates and courses while failing to explain how to monetize private communities with a unified fiat and crypto checkout.

A few strong examples:

- Creator circles: Paid Discord access for tutorials, office hours, and feedback.

- Expert groups: Telegram memberships for analysts, investors, or operators sharing research.

- Coaching communities: Tiered access where higher plans include live sessions or direct support.

- Member libraries: A private group combined with gated downloads or course materials.

How to keep churn under control

Community churn usually comes from weak onboarding or vague promises, not pricing alone.

Members stay when the value is obvious in the first week.

Spell out the benefit in the channel description. Deliver one fast win immediately after payment. If you offer tiers, make the difference between them easy to understand. And if you're exploring the business model itself, Suby's article on making money on Discord is worth reading.

4. International Invoicing with Currency Flexibility

Not every digital product is a download or a subscription. Sometimes the product is your service, packaged and sold efficiently. That makes invoicing part of the product experience.

Suby Invoicing is the version of Suby built for that job. Clients can pay how they want, and the business receives what it wants, where it wants, in its balance. That's useful for agencies, consultants, and freelancers who sell globally but don't want to manage a patchwork of billing methods.

Why invoicing is still a digital product

If you run a design studio, a dev shop, or a research practice, the sale often starts with a scoped offer and ends with an invoice link. The cleaner that link is, the faster you get paid.

This model works especially well for retainers, milestone billing, strategy sessions, implementation packages, and productized consulting. It also gives you more room to invoice in the client's preferred format while keeping your own treasury setup consistent.

A cleaner setup

A good invoicing flow is boring in the best sense. The client gets a clear amount, a due date, and familiar payment options. You get one system for collection and settlement.

Try this approach:

- Use invoice links: Clients act faster when the path from email to payment is short.

- Keep terms visible: Put due dates and scope notes in the invoice itself, not buried in a separate doc.

- Standardize settlement: If you prefer to receive to your bank account or in USDC, keep that consistent across clients.

- Batch operational work: Review payouts on a fixed schedule so invoicing doesn't turn into daily admin.

The winning move here isn't complexity. It's reducing the number of tools involved.

5. Digital Product Distribution with Instant Access

What makes a digital product easy to sell at scale? Fast delivery, clear access, and a checkout that doesn't force buyers into one payment method.

This model works because the product is already finished before the sale happens. A creator can sell a course, template pack, ebook, software license, or resource bundle once, then deliver it automatically to buyers in different countries without adding manual work to every order. The business gets margin from repeatable distribution. The buyer gets the product right away.

Where this model fits best

Instant-access products are a strong fit for solo creators, educators, indie software teams, and small media brands. The common trait is simple fulfillment. Once payment clears, the buyer should receive a file, a license key, a private page, or an onboarding email within seconds.

Common examples include recorded courses, Notion and spreadsheet templates, downloadable guides, design asset bundles, prompt libraries, stock packs, and software keys. If you're comparing storefront options and delivery setups, Suby's guide to the best platforms for selling digital products is a useful companion to tools that help you sell digital products with Marketsyai.

Monetization blueprint

The pricing is usually straightforward. Sell one product, sell a bundle, or offer a low-ticket entry product that leads to a higher-value upsell. The operational part is where many founders lose sales.

Suby gives you one checkout for global card and crypto payments, which matters if your buyers include both mainstream consumers and wallet-native users. That reduces a common early problem. Founders often patch together one tool for card payments, another for crypto, and a third for delivery. The result is more failure points, more support requests, and harder reconciliation.

A practical setup looks like this:

- Start with paylinks: They are enough for many first products and let you test demand without building a full store.

- Trigger delivery from payment confirmation: Send the download, license, or access email automatically after a successful payment.

- Show the delivery method before purchase: Buyers should know whether they will get a file, an email link, a dashboard login, or a license code.

- Use bundles carefully: A bundle can raise average order value, but only when the products solve a related problem.

- Keep failed-payment support simple: Have a clear fallback process for buyers who paid but missed the access email.

One mistake shows up often. Sellers focus on the product page and ignore the handoff after checkout. That handoff is part of the product. If the file link breaks, the login email lands late, or the access instructions are vague, refund requests rise even when the product itself is solid.

6. Subscription Management Across Global Markets

Why do subscription businesses with strong products still leak revenue every month? The problem is usually billing operations, not demand. Charges fail, renewal timing feels unclear, and buyers in different regions hit payment friction before they ever evaluate the product itself.

Recurring revenue works when the value repeats and the payment experience stays predictable. That makes this a strong digital product idea for SaaS tools, paid research, premium education, creator memberships, and community access with ongoing benefits. It is a weaker fit for products people buy once, use heavily for a week, then ignore.

The monetization model needs to be clear from the start. A simple monthly plan gets the widest trial volume. An annual plan improves cash flow and usually lowers churn if the product has already proven retention. A freemium offer can help acquisition, but only if there is a clear upgrade trigger such as usage limits, premium content, team access, or faster support.

Suby is useful here because it lets founders run recurring billing and accept global card and crypto payments through one platform instead of stitching together separate tools by region or payment type. That matters on day one. A customer may want to subscribe with a card, while another prefers to pay from a wallet. If both can complete the same subscription flow and you can track renewals, failed payments, churn, and payouts in one dashboard, the business is easier to operate.

A practical setup looks like this:

- Start with one core plan: Too many tiers slow decisions and create support questions.

- Add annual pricing only after monthly retention looks healthy: Annual plans hide churn problems if the monthly offer is weak.

- Show renewal terms before checkout: Billing date, trial length, cancellation policy, and renewal amount should be visible.

- Set up failed-payment recovery: Retries, reminder emails, and account status rules should be defined before launch.

- Separate customer payment choice from your settlement choice: Let buyers pay how they prefer while you control how funds are received and reconciled.

The trade-off is straightforward. More payment options can raise conversion across markets, but they also increase edge cases around renewals, refunds, and support. That is why unified subscription tracking matters more than marketing copy about recurring revenue.

Good subscriptions earn the next charge. They do not rely on confusion, forgotten renewals, or hard-to-find cancellation steps.

The founders who handle this well treat subscription billing as part of the product. They write renewal emails carefully, keep plan logic simple, and review failed payments every week. That discipline is often the difference between a subscription business that compounds and one that stalls.

7. Agency and Freelancer Payment Collection Platform

Many service businesses still treat payments as back-office admin. They should treat them as part of the offer.

A design agency, development shop, or solo consultant can turn billing into a digital product by productizing common services, attaching a clear purchase path, and removing the awkward follow-up cycle. That's especially useful for international work, where clients may want one payment method and the business may want another settlement option.

Productized services sell better

Retainers, audits, creative packages, and fixed-scope builds are easier to buy when the scope is standardized. Buyers hesitate less when the commercial side feels structured.

This works well for brand packages, monthly dev retainers, campaign strategy, implementation sprints, and fractional advisory work. It's less effective for vague “custom solutions” that still require five rounds of discovery before anyone can pay.

A practical payment setup

Suby Invoicing is a good fit when you want clients to pay by card or crypto while you receive funds in the way you choose. Customers pay how they want, businesses get paid the way they choose. That's not a slogan here. It's the practical value.

A few habits make a big difference:

- Put payment links in proposals: Don't make the client ask for the next step.

- Keep terms short and visible: Long legal copy belongs in the contract, not the core payment prompt.

- Automate recurring retainers: Manual monthly invoicing creates avoidable delays.

- Use one balance: It's easier to manage float and payouts when collections land in one place.

The best billing systems for service firms are the ones clients barely notice.

8. Cross-Border E-Commerce Checkout Optimization

Cross-border e-commerce lives or dies at checkout. If the payment methods feel unfamiliar, buyers leave. If the settlement side is messy, the merchant pays for that complexity later.

A unified checkout has a real edge. Suby is payment infrastructure for the global internet economy. Businesses can accept cards, wallets, bank methods, BNPL, and crypto, then settle to a bank account or in stablecoins, in the currency they want. Pricing depends on the payment method used, so check Suby's pricing page for exact figures.

Where the upside is

Consumer behavior is already moving toward more flexible digital payment habits. The global BNPL market is projected to reach $37.21 billion in 2030, and the global digital wallet market is projected to reach $68 billion in 2026, according to Corefy's payment processing industry statistics. If you sell internationally, supporting only one or two familiar methods is increasingly restrictive.

This model fits online retailers, digital goods stores, cross-border brands, and niche commerce businesses expanding outside their home market.

What to simplify first

Don't begin with edge cases. Fix the obvious pain points first.

- Show relevant methods upfront: Buyers should see familiar options early in the flow.

- Make currency clear: Don't surprise people at the final step.

- Keep refunds easy: Suby supports zero-fee refunds, which helps trust when something goes wrong.

- Separate customer choice from business settlement: Let the buyer pay their way while you keep treasury operations consistent.

The best checkout usually feels local to the buyer and standardized to the business.

9. Marketplace and Multi-Vendor Payment Splitting

A marketplace becomes interesting when it removes friction for both sides. Buyers want one smooth payment. Sellers want fast, understandable payouts. Operators want clean reconciliation.

That's why payment splitting is one of the more durable digital product ideas for founders. You're not just selling listings or access. You're selling trusted transaction flow between two parties.

Why this is a strong platform play

This model works for freelance marketplaces, creator platforms, digital asset stores, expert networks, and service exchanges. It's strongest when the platform's value increases as more buyers and sellers participate.

Suby's operating model supports this direction well. Payins from different methods land in one balance, and payouts can go out in another currency or format. That gives platforms room to support vendors with different preferences, including bank payout or stablecoin settlement.

How to avoid payout chaos

Marketplace payment logic breaks when the rules aren't clear.

Sellers care less about fancy dashboards than they do about knowing when they'll be paid and in what form.

Keep these principles in place:

- State payout timing upfront: Don't make vendors guess.

- Offer payout choice where useful: Some sellers want bank payouts, others prefer stablecoins like USDC.

- Test refund paths early: Split payments get messy fast if you only model the happy path.

- Give vendors visibility: Earnings history and payout status reduce support overhead.

The operational win is consistency. The strategic win is becoming the platform sellers trust to handle money correctly.

10. Developer-First Payment Integration for Web Applications

Need payments to happen inside your product instead of sending users to a generic storefront?

A developer-first integration makes sense when billing is part of the user experience itself. That includes SaaS upgrade flows, fintech apps, embedded commerce, gated tools, and custom workflows where pricing, access, or settlement rules depend on what the user does inside the app. In those cases, the payment layer has to fit your product logic, not the other way around.

Suby Payments gives teams one stack for cards and crypto from day one. The practical advantage is consolidation. One checkout, one API, one webhook system, and one operations dashboard are easier to build around than separate tools for fiat, crypto, links, and recurring billing. That matters more as volume grows and support questions shift from “Did the charge go through?” to “Why did this renewal fail?” and “How do we settle this customer in the right format?”

Where this model works best

This approach is strongest when founders want control over the payment experience without building a payments product from scratch.

Good fits include:

- SaaS products with upgrade paths: trigger plan changes, trials, and renewals from inside the app

- Fintech or wallet apps: accept user payments while keeping settlement logic flexible

- Web tools with gated usage: charge for credits, premium features, or usage-based access

- Embedded commerce products: sell inside a host app, plugin, or partner environment

- Hybrid Web2 and Web3 apps: accept cards and crypto through one system instead of stitching together separate providers

The trade-off is straightforward. You get more control, but your team also owns more implementation detail. That means event handling, failed payment states, retries, subscription changes, and support workflows need to be designed early.

Build it in stages

Teams often try to fully integrate billing before they know how customers want to pay. That slows launch and creates rework.

A better sequence looks like this:

- Start with paylinks: get real transactions live fast, validate pricing, and collect payment feedback before deeper engineering work

- Add API-based checkout next: bring the payment flow into the product once the buying journey is clear

- Treat webhooks like production infrastructure: payment success, failure, refund, and subscription events should be idempotent and logged

- Use the docs early: Suby's API introduction covers the core implementation path

- Handle failure states clearly: tell users whether the issue is a declined card, expired session, chain confirmation delay, or network error

- Test mobile behavior: even technical buyers complete purchases on phones, especially for renewals and quick upgrades

The monetization angle is what makes this idea stronger than a pure developer tool. You are not only offering integration convenience. You are creating a billing system that can accept global card payments, crypto payments, one-time purchases, and recurring revenue through one platform from the start. That reduces integration sprawl and gives founders room to sell internationally earlier.

A good developer-first payment setup should save engineering time now and reduce billing complexity six months from now. If it only helps with checkout and creates more reconciliation work later, it is not doing enough.

Top 10 Digital Product Ideas Comparison

| Solution | Implementation complexity | Resource requirements | Expected outcomes | Ideal use cases | Key advantages |

|---|---|---|---|---|---|

| Global Payment Checkout for SaaS Platforms | Medium, API integration | Moderate dev effort; payments ops | Unified global checkout; faster international launch | B2B SaaS, subscription platforms, marketplaces | Single API for 300+ methods; settle to bank or stablecoins |

| Crypto Payment Gateway for Web3 Applications | High, blockchain & wallets | Crypto engineering, wallet ops, monitoring | Frictionless on‑chain payments; gas management | NFT marketplaces, DAOs, crypto-native apps | Multi-chain support, gas sponsorship, non‑custodial settlement |

| Paid Community Access for Discord and Telegram | Low, mostly no-code | Minimal dev; community admin overhead | Monetized communities; instant gated access | Creators, DAOs, membership groups on Discord/Telegram | One-click gating, auto role assignment, recurring options |

| International Invoicing with Currency Flexibility | Low–Medium, invoicing + FX | Accounting integration; FX monitoring | Simplified cross-border billing; flexible settlement | Agencies, freelancers, service providers | Branded invoice links, oracle FX, settle to bank or USDC |

| Digital Product Distribution with Instant Access | Low, paylinks/automation | Basic delivery infra; customer support | Immediate delivery; global sales with low ops | Course creators, template/software sellers, authors | Instant access, multi-method payments, global reach |

| Subscription Management Across Global Markets | Medium, recurring & dunning | Dev for billing workflows; analytics | Predictable recurring revenue; churn visibility | SaaS, membership platforms, content subscriptions | Automated billing, dunning, cohort reporting |

| Agency and Freelancer Payment Collection Platform | Low–Medium, invoicing system | Client onboarding, accounting hooks | Faster collections; reduced FX complexity | Design agencies, dev shops, consultants | Multi-currency invoices, automated reminders, reconciliation |

| Cross-Border E‑Commerce Checkout Optimization | Medium, checkout UX + localization | Checkout dev, inventory integration, analytics | Higher conversion; simpler international ops | Retailers selling internationally, global marketplaces | Payment localization, 300+ methods, reduced cart abandonment |

| Marketplace and Multi‑Vendor Payment Splitting | High, split & reconciliation logic | Significant dev, vendor onboarding, support | Automated payouts; simplified platform cash flow | Marketplaces, gig platforms, creator platforms | Automatic splitting, per-vendor payout prefs, real-time reporting |

| Developer‑First Payment Integration for Web Applications | Low–Medium, API/SDK work | Developer time, sandbox testing | Custom embedded checkout; full control over UX | Fintech startups, SaaS, web3 apps, marketplaces | Rich SDKs/docs, webhooks, fast integration pathways |

From Idea to Income Your Next Steps

What turns a digital product idea into actual revenue? In practice, the winner is usually the offer that solves one clear problem and gives buyers a payment flow they already trust.

As noted earlier, demand is growing across education, media, templates, memberships, and software. That does not mean you should chase every category. Pick the format that fits your audience, your skill set, and the way you want to operate day to day.

Start smaller than your ambition tells you to. A paid Discord or Telegram group, a narrow SaaS tool, a productized service, or a downloadable bundle often reaches paying users faster than a broad platform with too many features. Shipping a focused version gives you real buying signals, real support questions, and a real conversion baseline. That is more useful than positive feedback from people who never intended to pay.

Payment design should happen early.

Founders often treat checkout, billing, and payout preferences as back-office work. It is not. If a buyer wants to pay by card and your product only accepts crypto, some portion of demand disappears. If an international client wants an invoice in their currency and you only bill in yours, sales cycles get longer. If you want to receive stablecoins but your customer wants to use a card, you need infrastructure that handles both sides without forcing workarounds.

That is the practical advantage of a unified setup. Suby combines card payments, crypto payments, invoicing, subscriptions, and gated access in one system. A creator can sell community access in Discord or Telegram. A SaaS founder can run recurring billing with card and crypto checkout. An agency can send invoices to clients who want familiar payment options while choosing its own settlement preference on the back end.

The trade-off is straightforward. Separate tools can work if your model is simple and local. Once you sell across borders, support recurring billing, or want to offer both card and crypto from day one, stitched-together systems create extra reconciliation work, more failure points, and more customer support.

One setup I see work well for internet businesses is simple. The customer pays with a card. The business receives USDC. That flow reduces friction for the buyer while giving the operator more flexibility on treasury and cross-border movement of funds. It is not the only model, but it is a practical one for global businesses that want faster setup and fewer payment dead ends.

If the offer itself still feels fuzzy, map the buyer, the buying moment, and the payout flow before you polish branding or add features. It also helps to review the broader product development stages so you do not overbuild too early. A clear problem, a narrow first offer, and a payment stack that supports global card and crypto acceptance from the start usually beats a bigger idea with messy operations.

If you want to launch without stitching together separate tools for checkout, subscriptions, crypto payments, invoicing, and gated access, Suby is worth a serious look. It gives you one platform for card and crypto payments, plus native Discord and Telegram integrations for paid communities, subscriptions, and digital access. Customers can pay how they want. Your business can receive funds the way it chooses.