Stripe has become a dominant force in online payment processing, known for its developer-friendly APIs and robust infrastructure. However, as the digital economy grows, a one-size-fits-all solution rarely meets every business's specific needs. Companies are increasingly seeking alternatives to Stripe for a variety of reasons, from seeking more favorable fee structures to requiring specialized features that Stripe doesn't prioritize.

One of the primary drivers for businesses exploring other options is often the cost. Transaction fees, currency conversion rates, and charges for disputes or chargebacks can add up, impacting a company's bottom line. To better understand potential savings, you can use a detailed Stripe fee calculator to analyze how these costs affect your revenue. Beyond pricing, businesses might need support for specific payment methods, better global coverage in certain regions, or a platform that simplifies complex compliance requirements. For others, the ability to receive payouts in stablecoins like USDC after a customer pays by card is a critical operational advantage.

This guide is designed to help you navigate the crowded market of payment processors. We will explore a curated list of the best Stripe alternatives, including platforms like Adyen, Braintree, and our own solution, Suby. Each profile will offer a direct look at their ideal use cases, key features, pricing, and integration capabilities, complete with screenshots and direct links. Our goal is to provide a clear, actionable resource that helps you find the perfect payment platform for your SaaS, e-commerce store, or creative business.

1. Suby

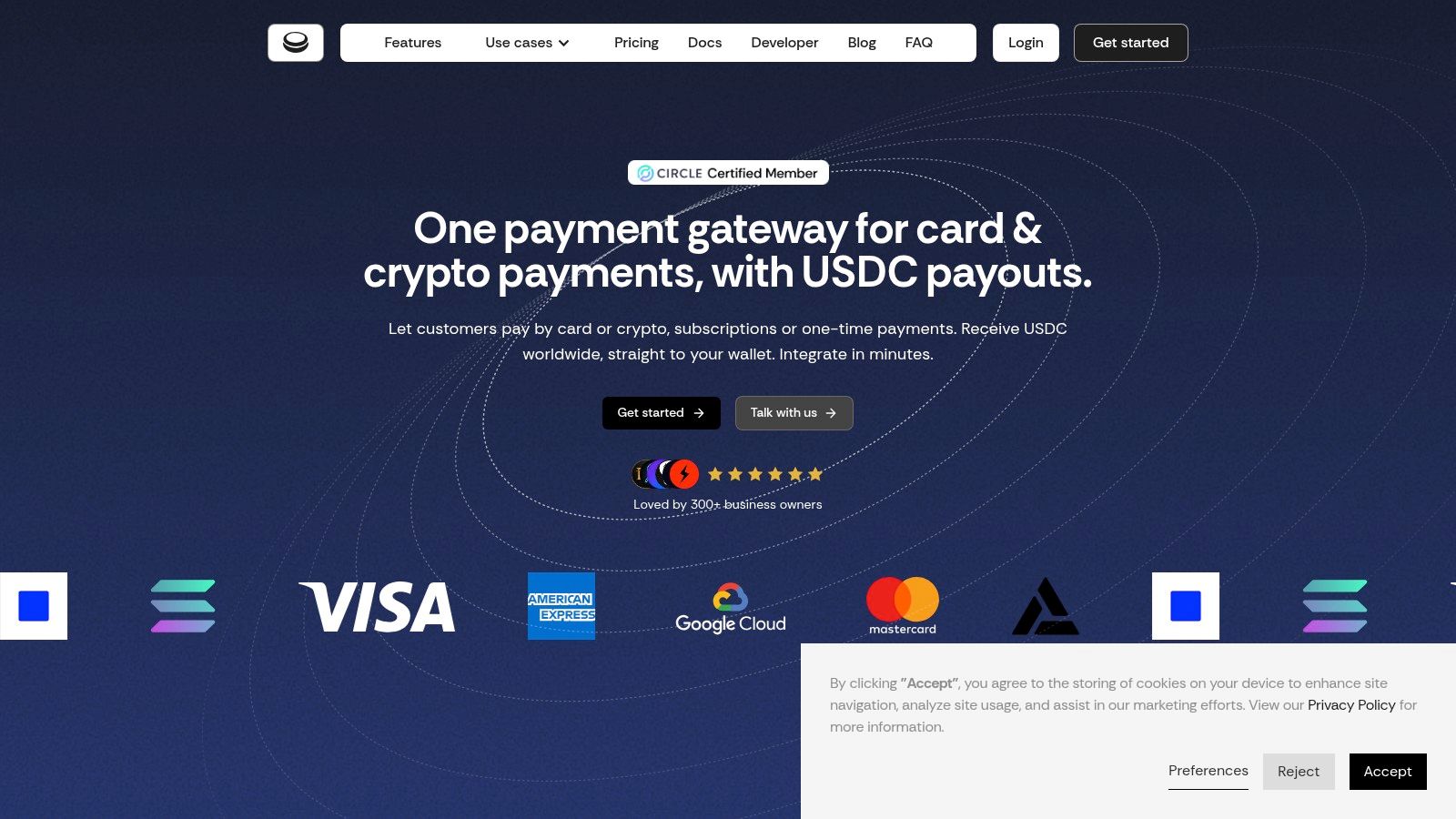

Suby presents a compelling and modern solution for internet-based businesses searching for robust alternatives to Stripe, especially those operating globally. It is designed from the ground up to solve cross-border payment friction by combining traditional card processing with stablecoin settlements. This approach allows merchants to accept payments from customers using Visa or Mastercard, while the revenue is settled directly into the merchant's USDC wallet.

This model directly addresses common pain points like currency conversion spreads, SWIFT transfer delays, and unpredictable bank holds that often complicate international sales. For SaaS founders, freelancers, agencies, and community operators, Suby provides a direct path to predictable, fast-moving revenue without requiring local banking relationships in every market.

Key Strengths & Use Cases

Suby's architecture is built for speed and simplicity. Businesses can start accepting payments quickly through several methods, including an embeddable checkout, shareable payment links, or a flexible API for custom integrations. It's a strong fit for various business models:

- Global SaaS & E-commerce: Companies can sell subscriptions or one-time products worldwide and consolidate revenue in USDC, simplifying treasury management and forecasting. Customers pay with cards, and businesses receive USDC.

- Creators & Communities: Suby offers native integrations that automatically manage member access to Discord and Telegram servers based on payment status, a key feature for community managers.

- Agencies & Freelancers: Invoicing international clients becomes much simpler. A freelancer can send a payment link and receive funds in their USDC wallet, avoiding the high fees and delays typical of traditional bank wires.

Core Benefit: Suby’s main advantage is its ability to bypass the friction of the traditional banking system. By settling card payments in USDC, it gives businesses faster access to their funds with greater transparency, making it an excellent alternative for anyone frustrated with opaque payout schedules and cross-border settlement costs.

Pricing and Security

Suby's pricing is listed at a clear 4% per transaction on its official site, which covers both card processing and settlement. Payout fees vary by plan, so it's wise to consult the pricing page for current details. This transparent structure helps businesses forecast margins accurately without worrying about hidden fees.

Security is handled with enterprise-grade standards. Card payments are processed via a PCI-DSS Level 1–certified partner, and the platform includes built-in fraud protections like behavioral anti-bot detection and device fingerprinting to protect merchants. A notable benefit is that refunds are processed with zero fees.

Pros & Cons

- Unified card and crypto acceptance with direct USDC settlement.

- Fast onboarding with an embeddable checkout, payment links, and a developer-friendly API.

- Transparent transaction pricing and no-fee refunds.

- Built-in tools for managing subscriptions and community access (Discord/Telegram).

- Revenue settlement is in USDC, requiring businesses to manage a crypto wallet and integrate stablecoin revenue into their accounting.

- Companies needing direct fiat deposits into a traditional bank account must add an off-ramping step.

Learn More: https://suby.fi

2. Adyen

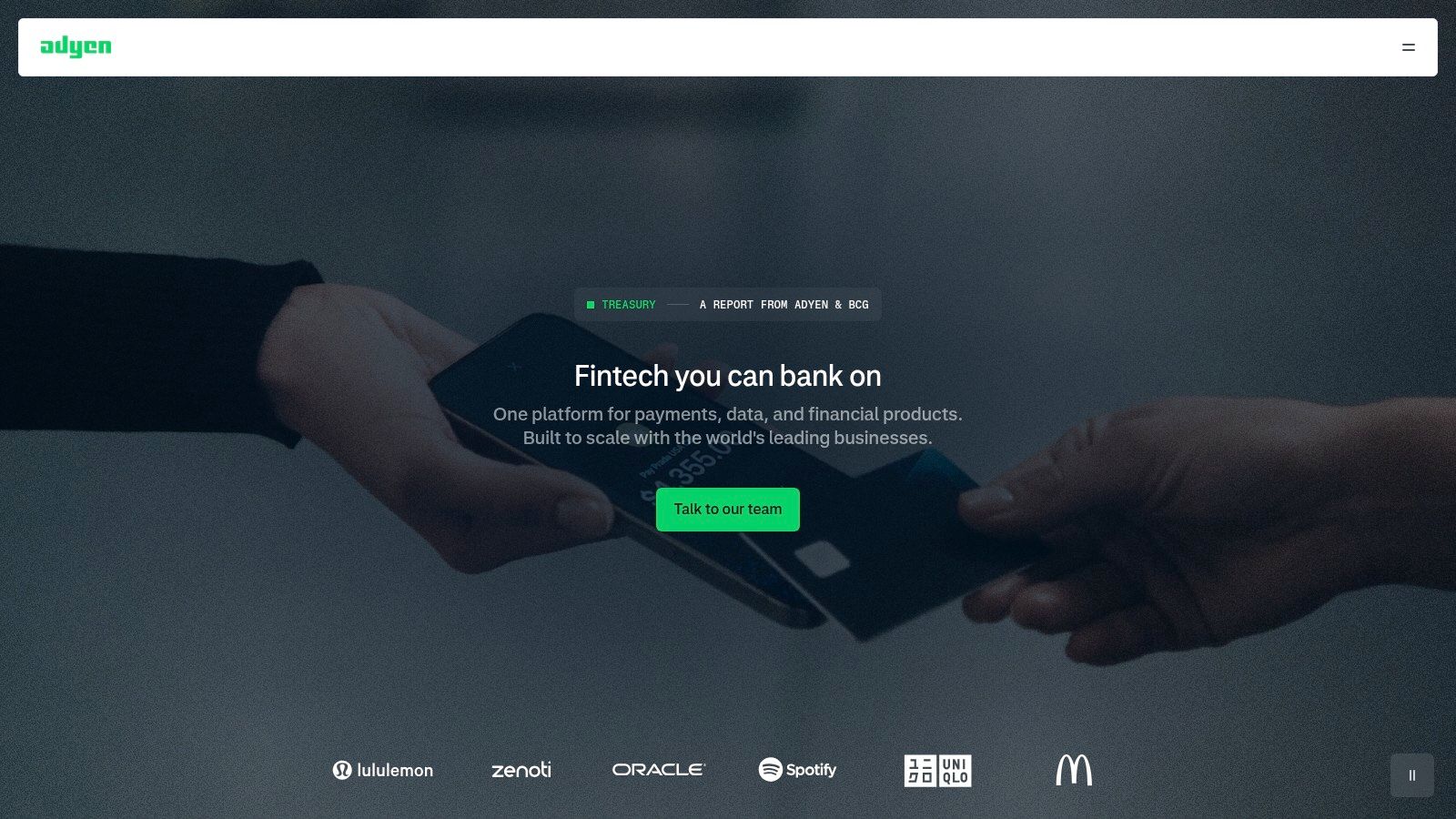

Adyen is a powerful, enterprise-focused payment platform that acts as a direct acquirer, processor, and gateway. Unlike many alternatives to Stripe that rely on a network of partners, Adyen's unified infrastructure provides end-to-end control over the payment flow. This direct connection to card networks like Visa and Mastercard often leads to higher authorization rates, reduced latency, and more detailed transaction data.

This structure is especially beneficial for large-scale international businesses. For instance, a global SaaS company can use Adyen to accept payments in over 150 currencies and receive settlements in their currency of choice, simplifying cross-border financial operations. Adyen's focus on providing the best international payment gateway solutions makes it a strong contender for businesses with a significant global footprint.

Why Choose Adyen?

Adyen stands out for its robust API and in-depth technical capabilities, designed for engineering teams that need granular control. Its single platform unifies online, mobile, and in-person payments, creating a consistent customer experience across all channels.

- Best For: Large enterprises, global e-commerce stores, and subscription businesses with high transaction volumes.

- Key Feature: Unified commerce platform with direct acquiring, which can improve payment acceptance rates.

- Pricing: Adyen uses a transparent Interchange++ model or a flat-rate fee per transaction. Pricing is typically customized and requires engagement with their sales team. It's not suited for very small merchants or startups due to minimum volume requirements.

- Limitation: The platform’s complexity and high technical bar mean it requires a dedicated development team to implement and manage effectively.

3. Checkout.com

Checkout.com is an API-first payment processor with a strong global presence, offering domestic acquiring in many key markets and a rapidly expanding footprint in the United States. Its modern infrastructure is built for businesses that require granular data and control over their payment stack. This makes it an excellent choice for SaaS companies and marketplaces looking to optimize their revenue with detailed analytics and flexible payment routing.

The platform’s Unified Payments API handles both pay-ins and payouts, supporting over 150 processing currencies. For an international e-commerce brand, this means they can accept local payment methods in various countries while consolidating financial reporting. Checkout.com’s emphasis on high data visibility and flexible commercial models positions it as a compelling alternative to Stripe for data-driven, enterprise-level businesses.

Why Choose Checkout.com?

Checkout.com appeals to companies with engineering resources that can take full advantage of its modular, API-driven architecture. The platform includes built-in fraud detection tools and rich analytics, allowing businesses to gain deep insights into transaction performance and customer behavior without relying on third-party tools.

- Best For: Global SaaS platforms, large e-commerce marketplaces, and companies that prioritize payment data analytics.

- Key Feature: Unified Payments API that provides granular control over the entire payment flow, from acceptance to settlement.

- Pricing: Uses flexible commercial models, including flat-rate or Interchange++. Pricing is customized and not publicly listed, requiring direct engagement with their sales team. The model is less suited for small businesses due to volume expectations.

- Limitation: Onboarding can be a lengthy process with significant due diligence, and its custom pricing is not transparent for smaller merchants or startups exploring options.

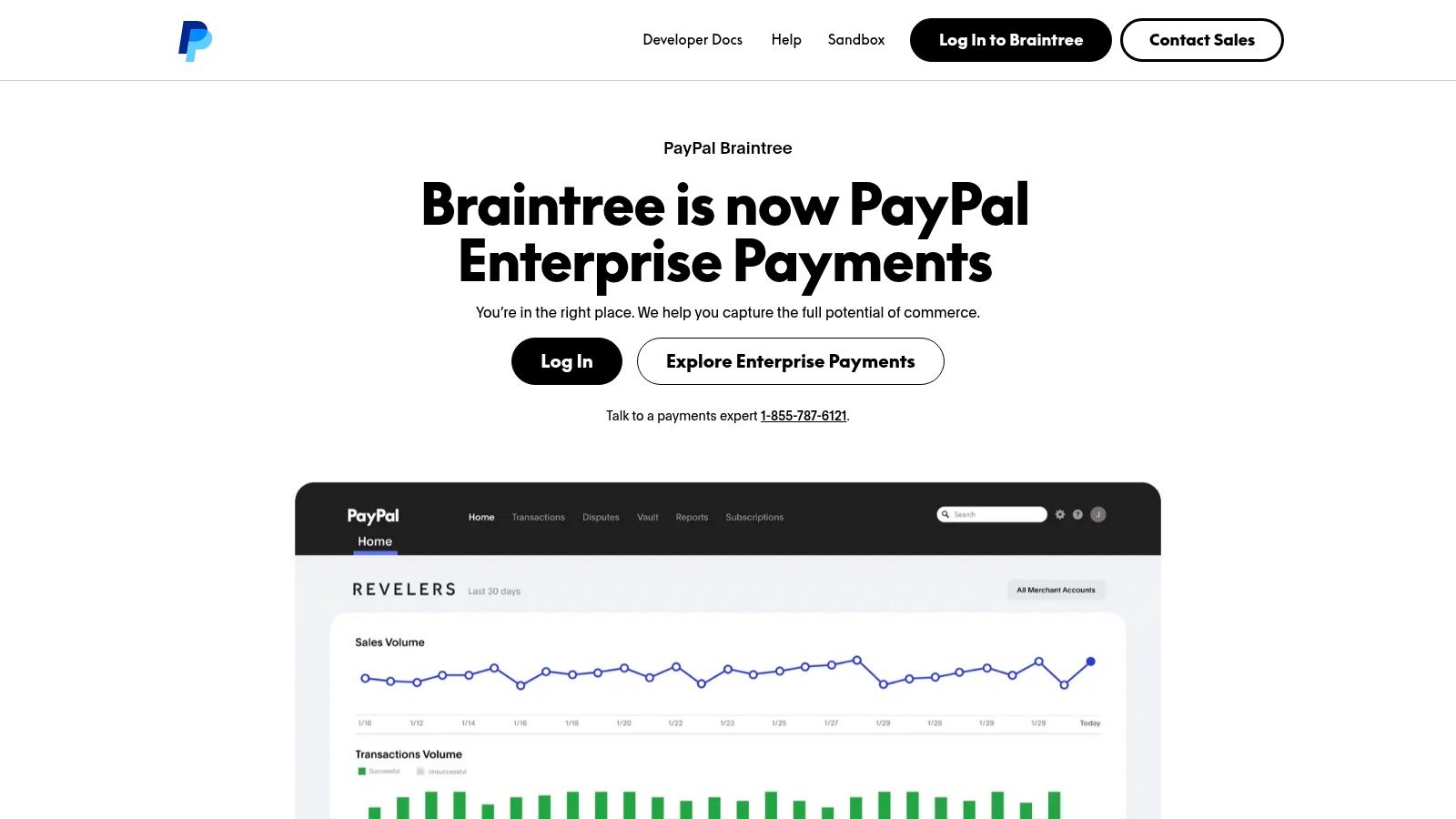

4. Braintree (by PayPal)

As a PayPal service, Braintree offers a full-stack payment gateway and acquiring solution that excels at combining traditional card payments with popular digital wallets. Its key strength lies in providing a single, unified integration for accepting credit cards, debit cards, PayPal, and Venmo. This makes it a compelling choice for consumer-facing businesses in the US, where leveraging the trust and user base of PayPal and Venmo can directly impact conversion rates.

This setup is particularly effective for e-commerce stores and SaaS companies targeting a broad consumer audience. For example, an online retailer can offer PayPal and Venmo as checkout options alongside standard cards, reducing friction for millions of users who prefer not to enter card details. Braintree’s focus on providing a payment gateway with PayPal and Venmo makes it a practical Stripe alternative for businesses aiming to maximize payment options in the US market.

Why Choose Braintree?

Braintree stands out by bundling PayPal's ecosystem into a developer-friendly package, complete with robust APIs (both GraphQL and REST) and transparent reporting. It supports recurring billing and a secure payment vault, allowing businesses to store customer payment methods for seamless repeat purchases and subscriptions.

- Best For: US-based e-commerce, consumer-facing SaaS, and marketplaces that can benefit from offering PayPal and Venmo.

- Key Feature: A single integration for cards, PayPal, and Venmo, which can boost conversion rates by catering to consumer preferences.

- Pricing: Braintree offers a standard flat-rate pricing of 2.59% + $0.49 per card or digital wallet transaction. Custom pricing is available for large-volume businesses. ACH Direct Debit is priced at 0.75% per transaction (capped at $5).

- Limitation: While it supports international payments, cross-border transactions and currency conversion can introduce additional costs and complexity compared to other global-first platforms.

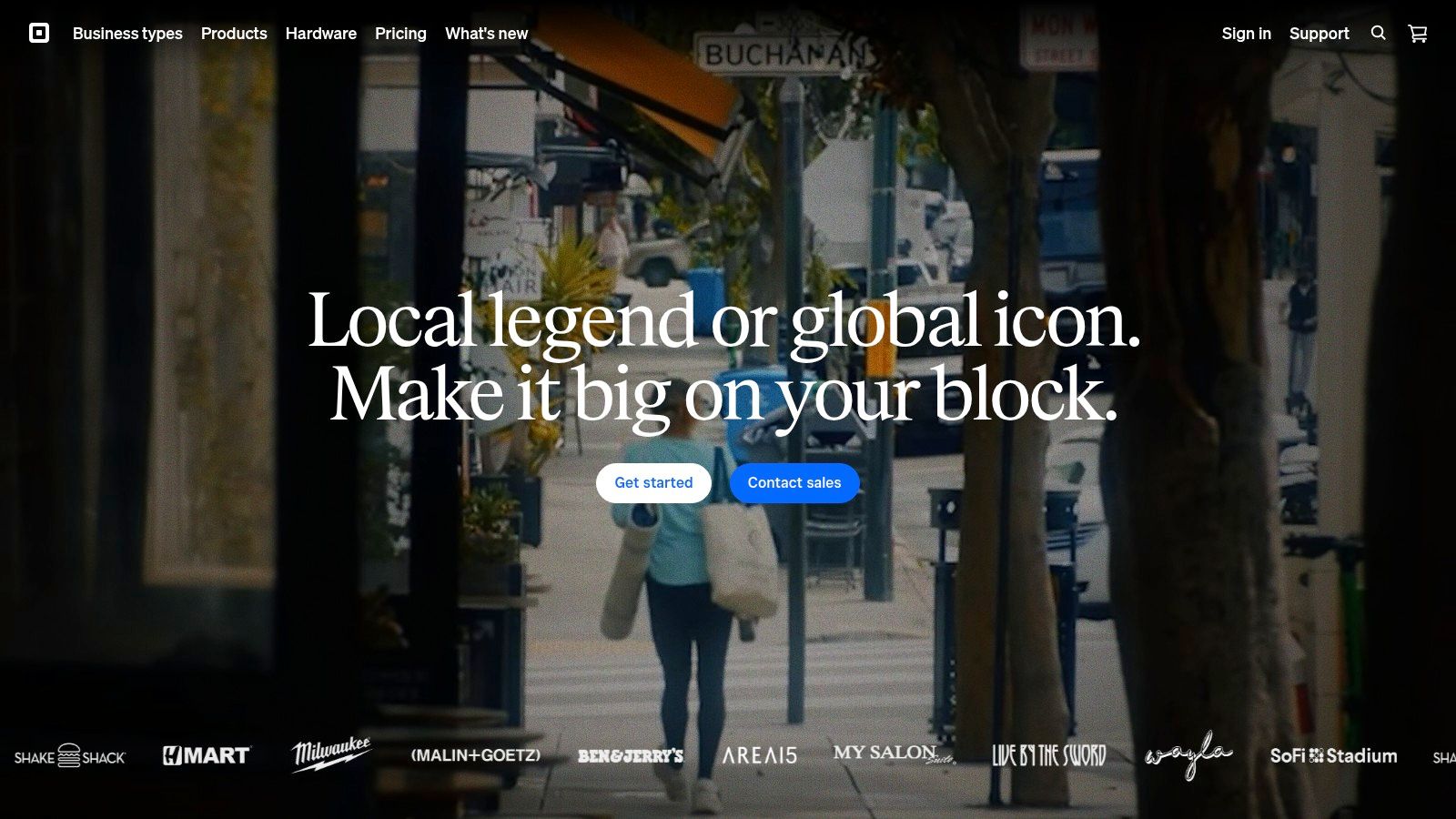

5. Square

Square is renowned for its seamless integration of online and in-person payments, making it a strong alternative to Stripe for businesses with a physical presence. Its ecosystem combines developer-friendly online APIs and a Web Payments SDK with robust point-of-sale (POS) hardware. This unified approach is ideal for retailers, restaurants, or service providers who need to manage transactions both on their website and at a physical location, all through a single provider.

The platform simplifies getting started with a clear API, comprehensive documentation, and tools for invoicing and subscriptions. A local coffee shop, for example, could use Square’s POS for in-store purchases and its online API to sell merchandise or coffee subscriptions on their website. This creates a connected experience where customer data and sales analytics are centralized, offering valuable business insights across all sales channels.

Why Choose Square?

Square excels with its straightforward setup and simple pricing, which is especially appealing to small and medium-sized businesses (SMBs). Its core strength lies in providing a unified stack for hybrid online and POS businesses, removing the complexity of managing separate systems for different sales environments.

- Best For: SMBs, retailers, service businesses, and any company needing both online and in-person payment processing.

- Key Feature: A complete ecosystem that combines online payment APIs with physical POS hardware and software.

- Pricing: Square uses a transparent, flat-rate pricing model (e.g., 2.9% + 30¢ for online transactions in the US) with no monthly fees for its standard plan. This makes costs predictable, though it can become more expensive than Interchange+ models for high-volume merchants.

- Limitation: The flat-rate pricing can be less cost-effective as transaction volume grows. Additionally, its ACH payment functionality does not support recurring charges for stored-credential subscriptions.

6. Authorize.Net (Visa)

Authorize.Net is one of the most established and widely recognized payment gateways in the United States, offering a mature and reliable infrastructure. Acquired by Visa, it functions as a flexible bridge between a merchant's website and the payment processing network. This makes it a dependable choice for businesses that already have a merchant account and are looking for a secure gateway to handle online transactions.

Unlike some modern platforms, Authorize.Net gives merchants flexibility. You can use it as a standalone gateway connected to your existing merchant account or opt for an all-in-one package that bundles the gateway with a merchant account from one of its resellers. This versatility makes it a practical, though sometimes more complex, alternative to Stripe for businesses that prefer to keep their banking relationships separate from their payment technology.

Why Choose Authorize.Net?

Authorize.Net stands out due to its longevity in the market, resulting in a broad feature set and extensive compatibility with a wide array of payment processors and shopping carts. Its fraud detection suite is robust, providing multiple layers of protection against suspicious transactions.

- Best For: US-based e-commerce businesses, merchants with existing processor relationships, and companies needing advanced fraud prevention tools.

- Key Feature: High flexibility through its "gateway-only" option, allowing businesses to plug Authorize.Net into their preferred merchant account provider.

- Pricing: The platform typically involves a monthly gateway fee (around $25) plus a per-transaction fee. The All-in-One plan offers a rate of 2.9% + 30¢ per transaction, but pricing can vary significantly depending on the reseller.

- Limitation: The pricing structure can be less straightforward than integrated solutions, and its user interface feels dated compared to newer competitors. International payment support is not as seamless as other global-first platforms.

7. Worldpay (part of Global Payments)

As one of the world's largest payment acquirers, Worldpay provides the scale and infrastructure needed for enterprise-level transaction processing. Acquired by FIS and later becoming part of Global Payments, Worldpay operates as a direct acquirer and processor with an extensive global reach, making it a common choice for large multinational corporations looking for reliable payment solutions. Its platform is built to handle high volumes of transactions across numerous countries and currencies.

This makes Worldpay a formidable player for businesses that have outgrown simpler payment gateways and require a more direct, robust processing relationship. For example, an international retail chain can use Worldpay to unify its online and in-store payment systems across different regions, accepting payments in over 110 currencies. This capability positions Worldpay as a strong, albeit complex, alternative to Stripe for established global enterprises.

Why Choose Worldpay?

Worldpay stands out due to its sheer scale and deep-rooted presence in the global payments industry. It provides a direct line to card networks, which can be beneficial for optimizing costs and acceptance rates at high volumes. The platform also offers a subscriptions API and enterprise-grade tools for customized payment flows.

- Best For: Large enterprises, multinational retailers, and high-volume e-commerce businesses that need a direct acquiring relationship.

- Key Feature: Extensive global acquiring network with support for over 110 currencies and various local payment methods.

- Pricing: Pricing is highly customized and requires direct engagement with a sales team. It's typically based on volume and business specifics, making it unsuitable for startups or small businesses. Public pricing is not readily available for its core enterprise services.

- Limitation: The platform can be complex to integrate, and its customer service and pricing structures can vary significantly by region. The lack of transparent pricing makes it difficult for smaller merchants to evaluate.

8. Paddle (Merchant of Record)

Paddle operates as a Merchant of Record (MoR) specifically designed for SaaS and software companies. Instead of just processing payments, Paddle legally acts as the reseller of your product, taking on the complex burden of global sales tax, VAT, and GST compliance. This model means Paddle handles tax calculation, collection, and remittance in every country your customers are in, which significantly simplifies international expansion.

This approach is especially valuable for subscription-based businesses that want to sell globally without building a dedicated finance and legal team to manage cross-border tax laws. For example, a UK-based software tool can sell to customers in the US, Australia, and the EU, and Paddle will automatically handle the respective sales tax and VAT obligations. This makes Paddle a compelling alternative to Stripe for founders who prioritize speed to market and operational simplicity over granular payment control. You can get a deeper understanding of this model by reading more about what a Merchant of Record is.

Why Choose Paddle?

Paddle stands out by bundling payments, subscriptions, invoicing, and tax compliance into a single platform. This all-in-one solution is built to help SaaS businesses scale faster by offloading the entire financial infrastructure and compliance headache, allowing teams to focus solely on their product.

- Best For: SaaS and software companies, particularly subscription-based businesses, aiming for rapid global sales without dealing with international tax compliance.

- Key Feature: The Merchant of Record model, which handles all global sales tax, VAT, and GST liability, fraud, and chargeback disputes on your behalf.

- Pricing: Paddle offers a pay-as-you-go model with a flat fee per transaction that includes all features. While this is simple, the fees can be higher than direct payment processors for businesses with very high transaction volumes.

- Limitation: As an MoR, Paddle becomes the legal seller, which can limit certain custom billing flows or direct contractual relationships with some enterprise partners.

9. Helcim

Helcim targets cost-conscious businesses in the US and Canada with its transparent and often more affordable interchange-plus pricing model. Instead of a flat rate like Stripe, Helcim passes the direct interchange cost from card networks to the merchant, plus a small, fixed markup. This approach means businesses with favorable transaction profiles, like those with lower-risk card types, can see significant savings as their volume grows.

The platform is designed for small to medium-sized businesses that have outgrown simple flat-rate models and want to optimize payment processing costs without committing to monthly fees. For a SaaS or e-commerce company scaling its operations, Helcim's automatic volume discounts provide a predictable path to lower fees. This makes it a compelling alternative to Stripe for businesses focused on margin improvement.

Why Choose Helcim?

Helcim's main appeal is its transparent interchange-plus pricing with no monthly fees, a combination not commonly found in the market. It bundles a suite of merchant tools, including invoicing, a virtual terminal, and POS software, making it a well-rounded solution for businesses managing both online and offline sales.

- Best For: US and Canadian SMBs, e-commerce stores, and service businesses looking to reduce processing costs as they scale.

- Key Feature: Automatic volume-based discounts on its interchange-plus pricing, rewarding businesses for growth.

- Pricing: Interchange-plus pricing with a small markup. For online transactions, the rate is Interchange + 0.50% + 25¢, with rates dropping as volume increases. ACH payments are competitively priced at 0.5% + 25¢, capped at $6 per transaction.

- Limitation: Payouts typically take 1–2 business days, as same-day funding is not a standard feature. Additionally, some merchants have reported occasional holds on payouts during risk reviews, a common practice but one to be aware of.

10. Stax by Fattmerchant

Stax, formerly known as Fattmerchant, disrupts the standard payment processing model with its subscription-based pricing. Instead of a percentage fee on every transaction, Stax charges a flat monthly fee, allowing merchants to access direct interchange rates with a 0% markup. This interchange-plus model can significantly reduce processing costs for businesses with substantial transaction volume, making it a noteworthy alternative to Stripe for established US-based companies.

This approach is particularly effective for businesses that have predictable, high sales figures. For example, a large retail store or a high-volume service provider processing over $20,000 per month could see material savings compared to a typical flat-rate structure. Stax's focus on providing transparent, membership-based pricing gives businesses a more predictable way to manage their payment processing expenses as they scale.

Why Choose Stax?

Stax stands out by eliminating percentage-based markups in favor of a membership plan, which is ideal for cost optimization at scale. The platform provides a robust toolkit that includes API access for custom integrations, hosted payment pages, recurring billing, and Text2Pay functionality, catering to a wide range of business needs.

- Best For: High-volume US merchants, professional services, retail, and businesses looking to lower their effective processing rate.

- Key Feature: Subscription-based pricing with direct interchange pass-through, which can substantially lower costs at scale.

- Pricing: Stax operates on a monthly subscription model, which gives merchants access to interchange rates without an added percentage. Plans start at $99/month, with additional small per-transaction fees. Some features like ACH and chargeback tools may incur extra costs.

- Limitation: The monthly subscription fee makes it less cost-effective for new or low-volume businesses. The primary benefits are realized by merchants with higher monthly processing volumes.

11. Amazon Pay

Amazon Pay is a wallet-based checkout service that lets customers pay on third-party websites using the payment and shipping information stored in their Amazon accounts. By presenting a familiar and trusted interface, it can significantly reduce checkout friction and cart abandonment. It works best as an incremental payment option alongside a primary processor rather than a complete replacement, making it a strategic addition for e-commerce stores looking to boost conversions.

This setup is especially effective for retailers selling physical goods. For example, an online apparel store can add Amazon Pay as a checkout button, allowing millions of Amazon shoppers to complete a purchase in just a few clicks without creating a new account or typing in their address. For certain U.S.-based businesses, Amazon Pay's Express Payouts feature provides access to funds within 24 hours, improving cash flow.

Why Choose Amazon Pay?

Amazon Pay stands out by tapping into the massive Amazon user base, offering a checkout experience that customers already know and trust. Its Checkout v2 provides a streamlined flow optimized for both web and mobile browsers. It also supports integrations with other payment methods like Affirm and allows customers to use Amazon Shop with Points.

- Best For: E-commerce merchants looking to increase conversion rates by offering a trusted, low-friction checkout option.

- Key Feature: The ability for customers to use their existing Amazon account credentials and stored payment information, which simplifies the buying process.

- Pricing: Transaction fees are competitive and vary by region. For U.S. domestic transactions, the fee is 2.9% + $0.30, but different rates apply for cross-border payments. Express Payouts are available to eligible U.S. merchants at no extra cost.

- Limitation: It is not a full-service payment processor for all business types and works best as a supplemental wallet. Merchants may also be subject to Amazon's reserve policies, which can temporarily hold a portion of funds.

12. BitPay

BitPay is a well-established crypto payment gateway designed for businesses looking to accept digital currency payments. It supports major crypto assets and stablecoins, providing merchants with a direct way to tap into the growing market of crypto-native customers. The platform offers a suite of tools including e-commerce plugins, direct invoicing, and pay-by-email links, making it a functional alternative to Stripe for specific use cases.

This gateway is particularly useful for companies aiming to facilitate international transactions without relying on traditional card networks. For example, an online retailer can use BitPay to sell globally, allowing customers to pay in their preferred digital asset while the business receives settlement in their chosen currency, including fiat or stablecoins. BitPay's core function is to be the most straightforward crypto payment processor for e-commerce, abstracting away much of the on-chain complexity for the merchant. To understand the operational aspects of this model, you can learn more about accepting crypto payments for business.

Why Choose BitPay?

BitPay stands out for its simple setup and broad support for different digital currencies. It provides easy-to-integrate plugins for major e-commerce platforms like Shopify and WooCommerce, lowering the barrier to entry for merchants who want to start accepting crypto without extensive development work.

- Best For: E-commerce stores, freelancers, and businesses wanting to attract crypto-savvy customers and offer a non-card payment option.

- Key Feature: Direct settlement in fiat currency or stablecoins, which protects businesses from the volatility of crypto assets.

- Pricing: BitPay charges a 1% transaction processing fee across all plans. It offers volume-tiered pricing that becomes more predictable for businesses with high crypto sales volume.

- Limitation: The user experience for customers can be affected by network congestion and transaction fees on certain blockchains. Also, recourse for payment disputes is limited compared to the chargeback systems of traditional card payments.

Top 12 Stripe Alternatives — Features & Pricing

Final Thoughts

Our journey through the world of payment processing has revealed one clear truth: while Stripe is a powerful and popular platform, it is far from the only option. The best choice for your business depends entirely on your specific model, scale, and strategic goals. Finding the right fit among the many alternatives to Stripe requires a thoughtful evaluation of what matters most to you.

This article has explored a dozen distinct platforms, each with its own strengths. From enterprise-grade solutions like Adyen and Checkout.com, which offer deep global reach and granular data, to developer-focused tools like Braintree, there is a solution for nearly every scenario. We've seen how platforms like Paddle simplify international tax and compliance by acting as a Merchant of Record, a critical function for many SaaS companies. We also examined options like Square and Helcim, which excel at unifying online and in-person sales, a must-have for businesses with a physical presence.

How to Choose Your Payment Partner

Making the final decision can feel overwhelming, so let's distill the process into actionable steps. Before you commit to a new provider, work through this checklist:

- Define Your Core Needs: Are you a SaaS business focused on recurring subscriptions? An e-commerce store with high-volume, low-margin sales? An agency invoicing international clients? Your business model is the single most important factor.

- Map Your Customer Base: Where are your customers located? Your payment gateway must support the currencies and preferred payment methods in those regions. A provider with strong European coverage, for example, is essential if you're targeting the EU market.

- Analyze the True Cost: Don't just look at the advertised transaction fee. Dig deeper into monthly charges, PCI compliance fees, chargeback penalties, and costs for add-on features like fraud protection or invoicing. For many businesses, a predictable, flat-rate structure is far more valuable than a seemingly low but complex percentage-based fee.

- Evaluate Technical Requirements: How much developer-power can you dedicate to integration? Some platforms offer simple, embeddable checkout widgets, while others provide robust APIs that require more technical expertise. Consider the long-term maintenance and the need for a solution that can grow with you.

- Consider Payouts and Cash Flow: How and when you get paid is just as important as how you accept payments. Traditional systems can involve settlement delays of several days and currency conversion fees. If you prefer faster, more direct access to your funds, especially in a stable digital currency, this should be a primary consideration.

Key Takeaways for Your Decision

Ultimately, your choice is a strategic one. For large, multinational corporations, the extensive customization and data offered by Adyen or Worldpay might be the deciding factor. For small businesses just starting out, the straightforward pricing and transparent fees of a provider like Helcim could be more appealing.

If your business operates globally and you’re looking to simplify your financial operations, receiving funds in a stablecoin like USDC can be a game-changer. It removes the friction of currency conversions and long bank settlement times. This is where modern solutions like Suby are creating a new path, focusing on the core need of getting businesses paid quickly and efficiently. By allowing customers to pay with their cards while merchants receive USDC, it addresses a key pain point for international SaaS companies, creators, and freelancers.

The search for alternatives to Stripe isn't about finding a "better" platform in a general sense. It's about finding the platform that is demonstrably better for your business. Take the time to assess your needs, run the numbers, and don't be afraid to choose a solution that breaks from the traditional mold if it aligns with your vision for growth.

Ready to modernize your payment stack with the speed and efficiency of stablecoin payouts? Suby provides a powerful API and no-code tools that let your customers pay with their card while you receive USDC directly. It's one of the most direct alternatives to Stripe for businesses seeking global reach without the complexity of traditional banking. Learn more and get started with Suby today.