Gaspard LEZIN

Optimize Your Stripe Subscription Management

Explore Stripe subscription management features, workflows, & pain points for global businesses. Discover modern alternatives offering predictable USDC payouts.

A familiar pattern plays out in a lot of SaaS teams.

You launch in one market, Stripe works, subscriptions go live, and finance is happy enough. Then growth starts coming from outside your home country. Customers pay in different currencies, support starts fielding payment failure complaints you can’t easily reproduce, and finance asks why settled cash doesn’t line up cleanly with booked revenue. The billing setup still works, but it starts demanding more operational attention than anyone expected.

That tension matters because subscriptions are still a strong business model. Stripe says recurring payment volumes on its platform grew 16% faster than one-time payments, and in a survey of 1,500 subscription companies, 81% said stable recurring revenue has become more important than ever for business sustainability, according to Stripe’s subscription and billing management report. The demand is real. The pressure to keep recurring revenue predictable is real too.

For domestic businesses, Stripe often feels like the default for good reason. It’s broad, mature, and well documented. But for companies selling across borders, the question isn’t whether Stripe is good. The question is whether a bank-centered system is still the right operating model when your customers, team, and cash flows are distributed globally.

I’ve seen this show up first in payouts and reconciliation, not in checkout. Checkout usually looks fine. The friction appears later, when finance needs clean reporting, product needs reliable entitlement rules, and leadership wants to know why “successful billing” still produces so much manual work.

If you’re evaluating your setup right now, this broader guide to the best international payment gateway is useful context before you go deeper on billing architecture.

Table of Contents

Introduction The Promise and Problem of Global Subscriptions

The core objects that run billing

What Stripe does well out of the box

Where product teams feel the complexity

Why webhooks are not optional

The active status problem

What a production-safe setup looks like

Cross-border payments create operational drag

Failed payments get harder outside your home market

Why finance teams feel this first

A different payout model

Where this fits best

Side by side comparison

The entitlement and state management difference

When each approach makes sense

Conclusion Choosing the Right Subscription Model for 2026

Introduction The Promise and Problem of Global Subscriptions

The early stage of international growth usually feels simple. You add a few countries, localize pricing, and watch new subscriptions come in while the core billing system stays the same. Product sees expansion. Finance sees more currencies. Operations starts seeing edge cases.

That’s where stripe subscription management often shifts from “billing feature” to “operating system.” The platform can support recurring payments, invoicing, trials, upgrades, downgrades, analytics, and global customer acquisition. But the further you move from a single-market business, the more work your team has to do around the edges.

A product leader usually notices it when entitlement logic gets messy. A finance lead notices it when payout timing becomes harder to forecast. Support notices it when a customer insists they paid, but their access changed at the wrong time.

Global subscriptions don’t usually break in checkout. They break in the gap between payment state, product access, and settled cash.

That’s the practical problem. Stripe is strong infrastructure, but global subscriptions involve more than billing events. They involve cross-border payment behavior, foreign exchange exposure, asynchronous payment outcomes, and bookkeeping across multiple systems. Those costs don’t always appear on day one, and they rarely sit inside a single dashboard.

For a domestic-first software company, that may be acceptable. For an internet-native business selling worldwide, it changes the economics of the stack. The question becomes less about feature depth and more about how much invisible operational work you’re willing to carry.

What is Stripe Subscription Management Core Features Explained

Stripe subscription management usually refers to Stripe Billing, the part of Stripe that handles recurring charges, invoices, pricing structures, and subscription lifecycle events. For a product team, it helps to think of it as a set of billing primitives rather than a complete business workflow.

Stripe has the scale to support serious billing workloads. Its billing analytics documentation says Stripe serves 4 million websites across 46 countries and handled peak traffic of 27,395 API requests per second with 99.999% uptime. The same analytics tooling supports cohort analysis and revenue retention views that can exceed 100% through expansion revenue, as described in Stripe’s subscription analytics documentation.

The core objects that run billing

At the center of Stripe Billing are a few core objects.

Products describe what you sell. That might be a SaaS plan, a premium membership, or access to a private community.

Prices define how the product is charged. You can set flat-rate, tiered, or seat-based pricing, and choose billing intervals from daily to yearly.

Subscriptions connect a customer to one or more prices and control renewal behavior over time.

Invoices record what’s owed for each billing cycle, upgrade, downgrade, or adjustment.

A simple example helps. Say you run a team collaboration tool with three plans. You’d create one product for each plan, attach monthly and annual prices, then create a subscription when a customer signs up. If they upgrade mid-cycle, Stripe can prorate the charge and generate the invoice automatically.

What Stripe does well out of the box

The main strength of Stripe’s billing model is flexibility.

You can combine several common needs inside one system:

Trials and onboarding offers let teams launch free trial periods without building separate billing logic first.

Proration handling helps when customers upgrade, downgrade, or change billing intervals mid-cycle.

Usage-based charging supports products where billing depends on consumption rather than a fixed seat count.

Customer self-service gives end users a portal to update payment methods or manage plan changes.

Lifecycle automation can trigger reminders, provisioning logic, refunds, and subscription updates.

For many companies, that’s enough to get from zero to a working recurring revenue model quickly. Product managers like it because the building blocks map reasonably well to how software plans are sold. Finance teams like it because invoices and recurring charges stay structured. Developers like it because the APIs are mature.

Later, once you’ve seen the object model in action, this walkthrough can help if you’re also thinking about Stripe usage-based billing and where it tends to require more custom logic.

A short product walkthrough makes this easier to visualize:

Where product teams feel the complexity

The trade-off is that Stripe gives you components, not business truth.

That sounds subtle, but it matters. A subscription product doesn’t just need invoices and charges. It needs clear answers to questions like these:

Question | Why it matters |

|---|---|

Has the customer paid for the current period? | Controls access and revenue recognition |

Should the user keep access during retries? | Affects churn, support load, and leakage |

What happens when pricing changes mid-cycle? | Impacts entitlement logic and invoice interpretation |

Which event should update the product database? | Prevents desync between Stripe and your app |

Practical rule: Stripe’s billing objects are strong primitives. Your team still has to define the operational rules that turn those primitives into customer access, finance logic, and internal reporting.

That’s why Stripe can feel elegant at demo stage and demanding in production. The platform gives you recurring payment infrastructure. It doesn’t remove the need to decide how your business interprets billing state.

The Technical Reality of Managing Stripe Subscriptions

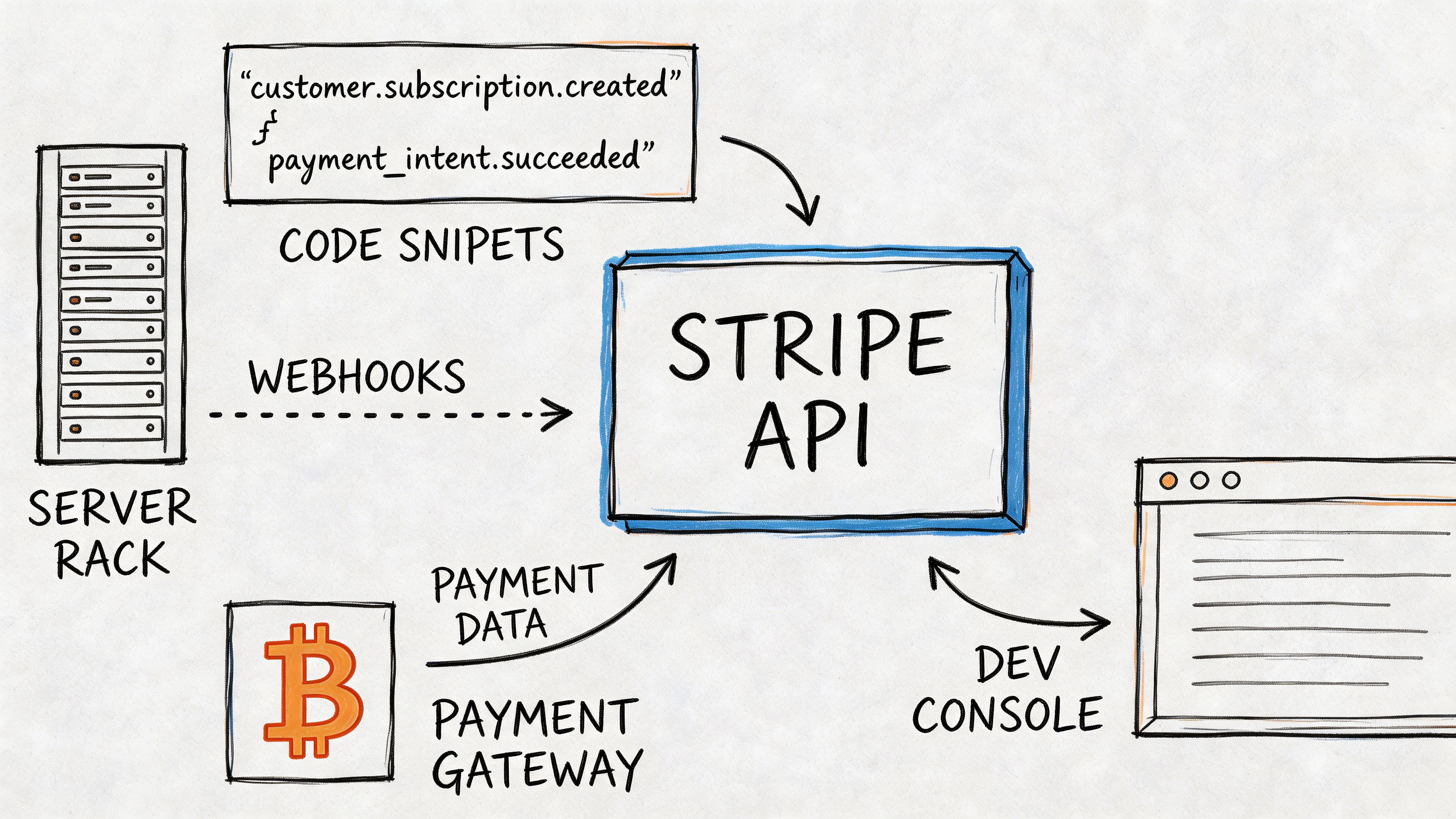

The biggest mistake teams make with stripe subscription management is assuming the API response in front of them is the whole truth. It isn’t. Subscription systems are event-driven, and many important events happen after the customer leaves the checkout flow.

Why webhooks are not optional

Stripe webhooks are the backbone of a reliable implementation. According to this technical deep dive on implementing Stripe subscription events with webhooks, client-side queries can’t reliably capture asynchronous events like renewals, failures, or cancellations. The same source notes that an ACH payment can fail after a subscription has been marked active, which means teams need webhook-driven logic to revoke access and keep systems in sync.

In practice, that means your backend needs to process events such as:

invoice.paid to confirm successful renewal

invoice.payment_failed to trigger dunning or access review

customer.subscription.updated to capture plan or status changes

customer.subscription.deleted to end entitlements cleanly

If those events don’t update your database atomically, the product state drifts away from the billing state. That’s how users keep access after failed renewals, or lose access after paying successfully.

The active status problem

A second issue is more specific, and more dangerous. In Stripe, the subscription status field can look valid while still hiding unpaid obligations.

A failed recurring invoice doesn’t always produce a billing state you can safely use for entitlements. If a later proration invoice gets paid, Stripe can still show the subscription as active even though the main recurring invoice remains unpaid. That’s not a minor reporting quirk. It can grant paid access to someone who hasn’t settled the core bill.

Don’t trust subscription status alone for entitlements. Treat it as an input, not a final answer.

For product and engineering teams, this changes the architecture. You stop asking, “What is the Stripe status?” and start asking, “What is our application’s current entitlement state based on all relevant invoices and events?”

What a production-safe setup looks like

A robust implementation usually includes three layers.

First, webhook ingestion with signature verification and retry-safe processing. Every event should be idempotent and traceable.

Second, application state in your own database. Stripe is the source of billing events, but your app needs its own customer access record.

Third, reconciliation logic that checks invoice history, open balances, and cancellation timing before access changes.

That’s where hidden engineering cost shows up. Stripe can absolutely support advanced subscription businesses, but your team ends up building a fair amount of billing intelligence around it. The more plans, currencies, regions, and edge cases you have, the more custom logic you own.

A simple rule helps: if billing failure can affect product access, build your own state model and treat external billing events as signals. Don’t let the frontend decide who is active.

Hidden Friction for Global Businesses

Organizations don’t feel the full cost of stripe subscription management until they operate across several markets. The billing engine still processes subscriptions. The strain shows up in finance, support, and operations.

Cross-border payments create operational drag

Global subscriptions introduce three recurring problems that domestic teams can underestimate.

Currency conversion exposure affects reporting and planning. Customers pay in one currency, fees may apply in another, and your accounting team still has to explain the final settled amount.

Payout timing uncertainty changes cash planning. Even when payment acceptance looks successful, treasury and finance still care about when usable funds arrive.

Reconciliation overhead grows quickly. Refunds, disputes, invoice adjustments, and regional payment behavior create more exceptions than a single-market model.

None of that means Stripe is broken. It means the system was built within the realities of traditional payment rails and bank settlement logic. If your business is global by default, those realities become a daily operating cost.

Failed payments get harder outside your home market

Involuntary churn is where this becomes expensive. Stripe’s own churn-focused research says one-third of businesses facing rising involuntary churn haven’t deployed third-party recovery tools, and international recovery rates often fall below 40% without custom tools, as discussed in Stripe’s article on better ways to combat subscription churn. The same verified data notes that some SaaS firms see 20-30% of revenue remain unrecovered annually in these conditions.

That problem usually gets worse once you operate beyond one domestic market. Authentication rules differ. Bank behavior differs. Retry success differs. A billing team that looked efficient in one country starts relying on extra dunning logic, payment recovery tooling, and more support intervention.

If you want a finance-side view of where these costs can hide, this breakdown of what Stripe fees look like in practice is worth reviewing alongside your own payment reports.

Cross-border churn isn’t only a payments problem. It becomes a support problem, a product-access problem, and a forecasting problem.

Why finance teams feel this first

Finance usually sees the hidden friction before product does.

They’re the team trying to answer practical questions:

Which subscriptions renewed successfully, versus which are still in retry flow?

What amount should count as earned revenue when exchange rates and fees affect the final settlement?

How should refunds or partial invoice outcomes map back to product access and monthly reporting?

Those questions often sound operational rather than strategic. But they shape pricing decisions, budget confidence, and expansion planning.

A lot of teams start with the assumption that “global-ready” means the checkout accepts many markets. In practice, global readiness also means your payout model, reconciliation flow, and recovery process still make sense when customers are spread across regions and payment behavior is less predictable.

A Modern Alternative for Global Commerce Suby

For businesses that don’t want to inherit all of that bank-centered complexity, a different model is emerging. Instead of optimizing around cards on the front end and bank payouts on the back end, the system keeps the familiar checkout while settling merchant revenue in a digital dollar balance.

A different payout model

Suby is built around a simpler flow. Customers pay with card or crypto, and businesses receive USDC. That changes the operational model more than the checkout experience.

The important difference isn’t just payment acceptance. It’s settlement.

With Suby, merchants can accept Visa or Mastercard, and also supported crypto assets including USDC, USDT, ETH, SOL, and BNB, while receiving revenue in USDC to their wallet. The platform supports one-time payments and recurring subscriptions, as described in the official Suby website and developer documentation.

That approach removes several sources of friction for international businesses:

No bank-dependent payout path means you’re not structuring operations around SWIFT transfers or local bank settlement delays.

Single-currency merchant settlement makes reconciliation cleaner because the business receives USDC regardless of how the customer paid.

Consistent payout logic reduces the need to track multiple domestic payout methods across regions.

Built-in recurring support means subscriptions don’t need a separate payments stack.

Suby also offers shareable paylinks, an embeddable checkout, API access, and webhooks. For creators and community operators, it includes native Discord and Telegram integrations for subscriptions, paid access, and membership control, according to the official Suby documentation.

Where this fits best

This model is most relevant for businesses that already operate like the internet does, not like a domestic bank account does.

That includes SaaS companies with international customer bases, agencies billing across borders, online communities selling paid access, and creators who want payment and access control in one system. It also suits teams that prefer not to build extra internal machinery just to normalize payout timing and billing outcomes after the transaction is approved.

There’s a straightforward product logic behind it. End users still get familiar payment methods. The merchant gets predictable settlement in USDC. That’s often a cleaner fit for cross-border commerce than stitching together cards, FX conversion, bank payouts, and manual reconciliation.

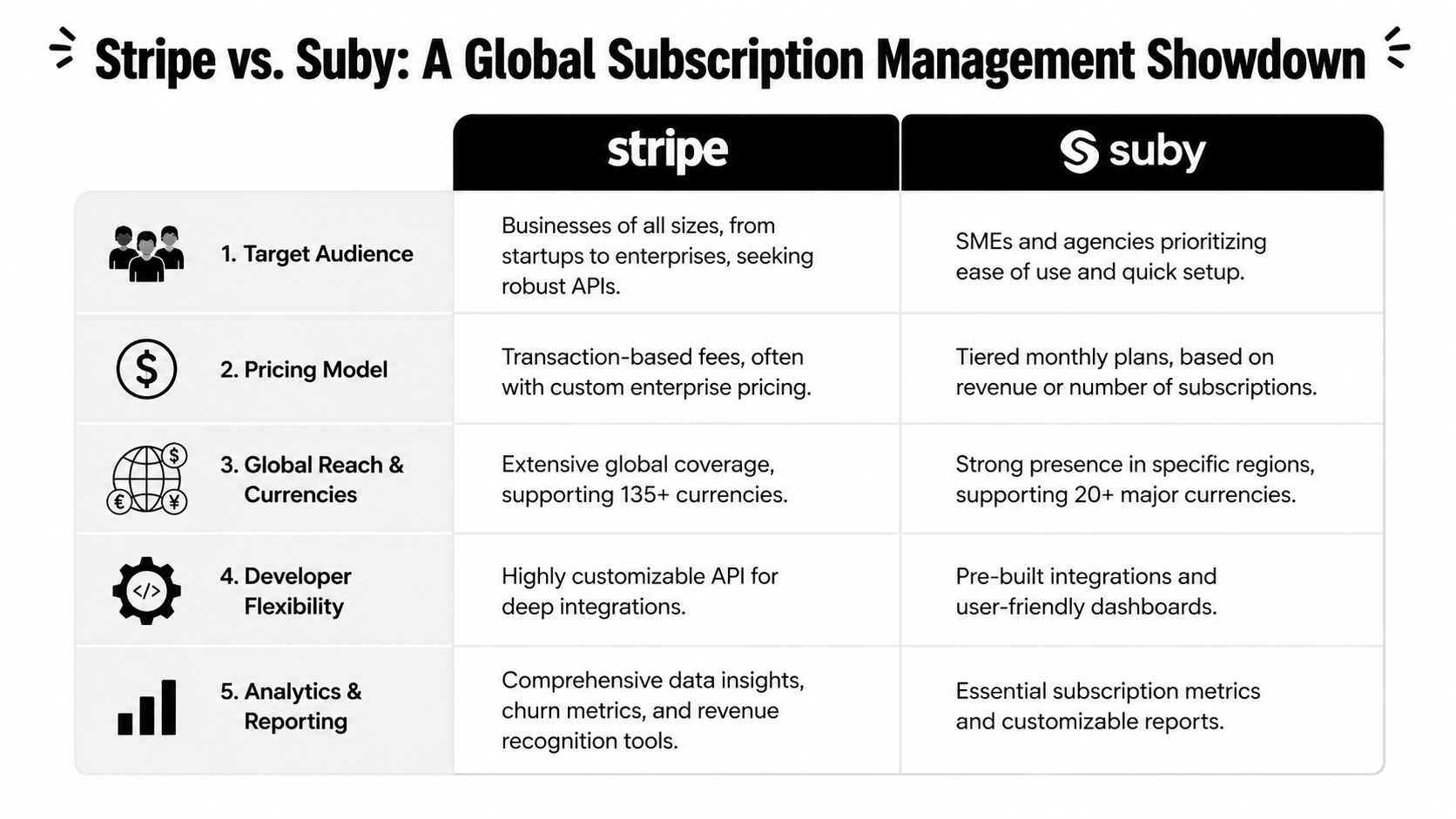

Stripe vs Suby A Comparison for Global Businesses

The most useful comparison isn’t “which platform has more features.” It’s “which operating model creates less friction for the way your business sells.”

Side by side comparison

Here’s the practical difference between a traditional billing stack and a flexible-settlement model that pays out to your bank account, or in stablecoins (USDC, EURC) to your wallet.

Feature | Stripe | Suby |

|---|---|---|

Merchant settlement model | Settles through traditional payment and banking flows | Customers pay with cards or crypto, businesses receive USDC |

Cross-border operating complexity | Often requires more attention around currencies, payout timing, and reconciliation | Keeps merchant-side settlement in one stable unit |

Subscription infrastructure | Mature billing primitives for plans, invoices, trials, and lifecycle events | Supports recurring subscriptions with API, webhooks, paylinks, and checkout |

Access management | Usually requires custom product logic around billing status and entitlements | Also supports subscription lifecycle management, plus native Discord and Telegram access flows |

Best fit | Teams comfortable building around a bank-centered payments stack | Internet-native businesses that want card acceptance with USDC settlement |

If you’re comparing checkout stacks more broadly, this review of payment gateway options for Shopify stores is a useful outside perspective because it highlights how payment choice affects operations, not just conversion.

The entitlement and state management difference

The hardest operational issue in Stripe isn’t always acceptance. It’s state.

Verified implementation guidance shows Stripe subscription status can be misleading. If a recurring invoice fails but a later proration invoice is paid, the subscription may still remain active, which can cause revenue leakage. The same verified source notes this can affect 5-10% of subscriptions in some environments, based on the analysis in Flycode’s article on managing Stripe billing lifecycle and reporting.

That matters because product access is rarely based on one field in real life. Teams end up checking invoice states, webhook events, retry outcomes, and local database records to determine who should have access right now.

With a system designed around unified payment and access workflows, some of that extra interpretation can be reduced. The less your team has to infer from fragmented billing states, the less custom infrastructure you need just to enforce entitlements correctly.

The real comparison is not API breadth versus simplicity. It’s how much operational logic your team must own after the payment succeeds.

When each approach makes sense

Stripe still makes sense for many businesses. If you’re tied to conventional banking flows, have in-house engineering for webhook-heavy billing logic, and mostly operate within traditional financial rails, it remains a strong choice.

Suby fits a different profile:

Global-first sellers that want a consistent merchant settlement outcome

Developers who want API and webhook access without building around bank payout complexity

Creators and communities that need payments tied directly to access control

Businesses that want cards on the front end and USDC on the back end

That last point is the core distinction. Users pay with familiar methods. The business receives USDC. For many cross-border teams, that’s less a feature than an operating simplification.

Conclusion Choosing the Right Subscription Model for 2026

Stripe is a capable subscription platform. For many companies, especially those working comfortably inside the traditional banking system, it remains a reasonable default. It gives teams broad billing functionality, mature APIs, and the flexibility to model a wide range of pricing and renewal flows.

But global subscription businesses usually discover that billing capability and operational simplicity are not the same thing.

The friction tends to show up after launch. Webhooks become mandatory. Entitlement rules need custom logic. Failed payments create product-access edge cases. Finance spends more time reconciling currencies, settlement timing, and invoice outcomes than anyone expected when the original implementation was scoped.

That doesn’t make Stripe the wrong choice. It makes it a choice with hidden operating costs, especially for internet-native businesses selling across borders.

A stablecoin-native model changes that trade-off. If customers can still pay with cards, while the business receives USDC in a predictable settlement flow, a lot of the usual cross-border mess gets pushed out of the core operating path. That matters for SaaS teams, agencies, creators, and online communities that don’t want to build finance and billing workarounds into the product itself.

The right subscription model for 2026 depends on what your company optimizes for.

If you want deep billing primitives and you’re comfortable managing the complexity around them, Stripe can work well. If you want faster settlement logic, cleaner cross-border operations, and a setup that matches how online businesses sell globally, a system built around card acceptance and USDC payouts may be the better fit.

The practical test is simple. Look past checkout conversion and ask what happens next. How much manual work sits between a successful payment, a clean payout, and correct customer access. That’s where the underlying cost of your subscription stack shows up.

Suby is a payment gateway and payment processor. Your customers pay with card, bank transfer, Apple Pay, Google Pay, Klarna, and more, or stablecoins, and your business gets paid out to your bank account, or directly in stablecoins (USDC, EURC) to your wallet, anywhere in the world, no bank account required. With recurring subscriptions, paylinks, webhooks, and native Discord and Telegram access flows, it lets a global Stripe subscription management setup standardize on one settlement outcome, instead of building finance and billing workarounds into the product to reconcile currencies and payout timing after every charge.