Gaspard LEZIN

Coinbase Commerce: A 2026 Guide for Merchants

Explore our detailed guide to Coinbase Commerce. Learn about its features, pricing, integrations, limitations, and how it compares for global business payments.

If you're running a global SaaS product, a paid community, or an online store, the payment problem usually shows up in the same places. Card fees chip away at margin. Cross-border payouts feel slower than the rest of your business. Chargebacks create operational drag. Then someone on the team says, “Should we just add crypto payments?”

That's usually when coinbase commerce enters the shortlist. It's one of the most recognized names in crypto payment infrastructure, and it has enough history in the market to deserve a serious look. But recognition alone doesn't answer the primary merchant question, which is simple: what will the business receive, how fast, and with how much operational certainty?

For merchants who care about predictable settlement in USDC, that distinction matters more than the checkout button.

Table of Contents

Why Businesses Are Exploring Crypto Payment Gateways

How the product evolved

The two operating models merchants should separate

What merchants can actually do with it

Why stablecoin direction matters

Payment links and buttons

Hosted and platform-led setups

API and webhook implementations

What the protocol does well

Where merchants need more clarity

Where coinbase commerce can fall short

When a different model fits better

Making the Right Choice for Your Business

Why Businesses Are Exploring Crypto Payment Gateways

A familiar example: a software company sells subscriptions globally, but its finance team still closes the month like it's handling a patchwork of regional payment systems. Customers pay one way, settlements arrive another way, and revenue forecasting gets messy because timing and fees aren't predictable enough.

That's why crypto payment gateways keep getting attention. The appeal isn't novelty. It's the possibility of borderless payments, faster settlement, and less dependence on legacy payment rails. For digital businesses, especially the ones serving customers across markets, that can solve a real operating problem.

A creator business sees the same pressure from a different angle. Paid access, recurring memberships, and one-time purchases all need a checkout that works internationally. But many teams don't want to hold volatile assets, reconcile multiple currencies, or explain wallet mechanics to customers.

Practical rule: A payment method is only useful if the finance team can predict what lands on the balance sheet.

That's where the evaluation gets more serious. Some merchants start with a broad search for a crypto payment gateway for online businesses, then narrow the list based on settlement preferences rather than brand familiarity.

Coinbase Commerce stays relevant in those conversations because it has been in the market long enough to shape expectations around crypto acceptance. But merchants looking at it today need to assess more than whether it can collect payment. They need to know whether it supports the business model they run, especially if the goal is simple revenue operations and settlement in USDC rather than exposure to whatever asset the customer used at checkout.

What Is Coinbase Commerce Explained

Coinbase Commerce is a merchant payment product built to help businesses accept digital asset payments online. It started as an early piece of infrastructure for crypto acceptance and became one of the first names many merchants encountered when they wanted an alternative to card-only checkout.

According to Coinbase's own deep dive, Coinbase Commerce launched in 2018, and it has grown to serve thousands of merchants worldwide while processing billions of dollars in onchain payments through its infrastructure, which shows how early it arrived in the market and how seriously merchants tested onchain settlement at scale (Coinbase Commerce deep dive).

How the product evolved

The original version of coinbase commerce made sense in a market where merchants mainly wanted a way to accept crypto directly. That first wave was about access. Could a business take payment online without relying entirely on the card networks or a traditional acquiring setup?

Over time, the market changed. Merchants became less interested in accepting “crypto” and more interested in which asset reaches treasury, how settlement works, and whether the payment flow introduces accounting complexity.

That's an important shift. A payment tool can look modern on the front end while still creating work on the back end.

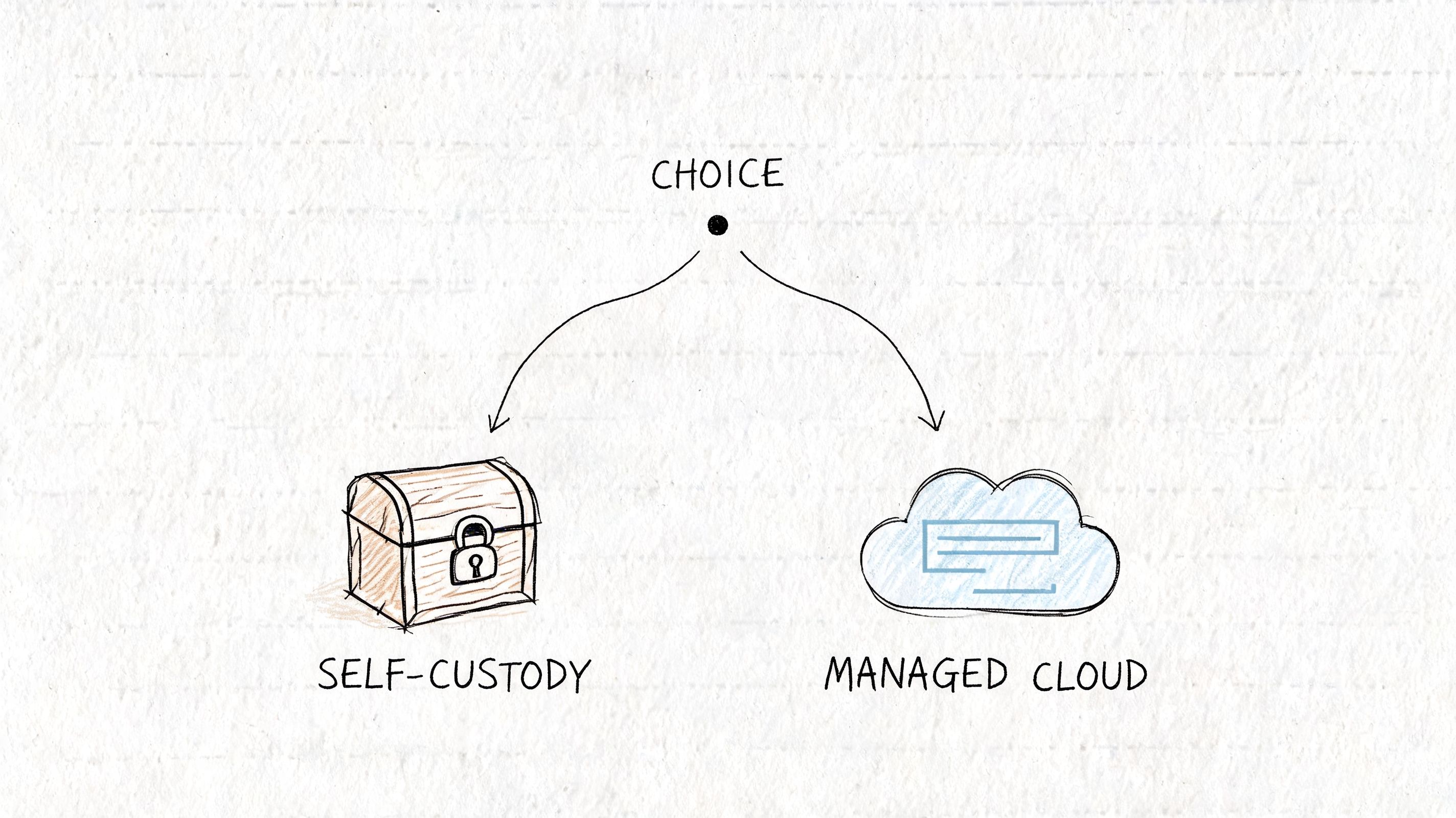

The two operating models merchants should separate

When businesses review coinbase commerce, they should mentally split it into two models.

The first is the direct crypto acceptance mindset. In that model, the merchant is comfortable with onchain flows and understands that receiving payment is only part of the story. Treasury handling, conversion, and withdrawal still need decisions.

The second is the managed settlement mindset, a preference among merchants for a service closer to mainstream payments. They care less about the specific asset the buyer used and more about the merchant-side result: clean settlement, lower friction, and predictable reporting.

A useful buying question is this:

Question | Why it matters |

|---|---|

Does the business want to hold what the customer paid with? | This affects treasury risk and reconciliation. |

Does finance need stable settlement? | This affects forecasting and margin control. |

Does the team want self-managed flows or a managed environment? | This affects operational overhead. |

Coinbase Commerce makes the most sense when the merchant is already comfortable with crypto-native operations. It becomes a harder fit when the business wants payments to feel more like standard commerce with stable settlement outcomes.

Core Features and Supported Payment Methods

For most merchants, coinbase commerce is attractive because it covers the basics of online crypto acceptance. You can set up ways to request payment, embed payment flows into a site, and support customer checkout without building everything from scratch.

What merchants can actually do with it

In practical terms, merchants usually look at coinbase commerce for a few common use cases:

Checkout collection: Add a payment option on a product page or checkout flow.

Payment requests: Generate a payable request for a fixed amount.

Embedded commerce flows: Connect payment acceptance into an existing product or storefront.

Developer-led automation: Use APIs and webhooks for order handling and status updates.

That's enough for many digital businesses to get started. A software company can attach payment collection to a subscription signup flow. A creator can use it for one-time access sales. An agency can use it for invoice-like collection where the customer already understands digital asset payments.

Still, feature lists don't tell the whole story. The more important merchant question is whether these tools help you control what settles.

Why stablecoin direction matters

The broader Coinbase payments strategy has clearly moved toward stablecoins. Payments Journal noted that Coinbase Payments reflects a strategic pivot toward stablecoin infrastructure, and that Shopify went live on the platform, which signals that stablecoin acceptance is becoming more relevant for mainstream commerce rather than staying a niche add-on (Payments Journal coverage of Coinbase Payments).

That shift matters because stablecoin settlement aligns better with how businesses already think about revenue. Finance teams want consistency. They don't want every incoming transaction to create a treasury decision.

A practical way to evaluate supported payment methods is to separate them into two buckets:

Customer payment flexibility

This is the front-end view. Can buyers complete payment using the wallets and assets they already use?Merchant settlement predictability

This is the back-end view. Does the business receive an asset it wants to keep, book, and spend?

If you're advising a merchant, the second bucket usually matters more. A broad payment menu may look impressive, but if settlement still creates conversion work or asset exposure, the “support” is less valuable than it first appears.

A payment option isn't finished when the customer clicks pay. It's finished when finance is happy with the funds received.

Comparing Integration Options for Your Website

Integration choice shapes how coinbase commerce feels in production. The same payment processor can be lightweight and useful in one business, then frustrating in another, because the implementation path doesn't match the team's workflow.

A short product walkthrough helps if your team is deciding how technical the setup should be:

Payment links and buttons

This is the fastest route when a business wants to start accepting payments without a development sprint. Payment links and simple buttons work well for:

Freelancers and agencies that need quick collection for one-off invoices

Creators selling access or digital products without a full custom checkout

Small teams validating whether their audience will use crypto payments at all

The trade-off is control. These setups are convenient, but they tend to be less customized for your brand, your onboarding flow, and your internal payment logic.

Hosted and platform-led setups

Some merchants want a middle ground. They don't need a fully custom API build, but they also don't want a raw payment link pasted into an email.

Hosted or platform-driven options usually fit teams that want a smoother customer journey without maintaining much payment infrastructure. This can be the right choice for e-commerce operators, especially if they already have a storefront stack and only need crypto acceptance added with limited engineering effort.

Here's the practical comparison:

Integration path | Best for | Main compromise |

|---|---|---|

Payment links | Fast launch | Limited customization |

Hosted flow or plugin | Existing storefronts | Platform constraints |

API and webhooks | Product-led businesses | More engineering work |

For merchants that also need cleaner bookkeeping after launch, it helps to review guides on automating financial admin with Receipt Router. The integration question doesn't stop at checkout. It continues into reconciliation.

API and webhook implementations

The API route is the strongest option for product teams that want to control checkout logic, payment confirmation, entitlements, and downstream automation. If you're building account upgrades, gated features, or membership logic, this is usually the only option worth considering.

That said, API integrations raise the bar on implementation quality. You need to think through status handling, failed or expired payments, and how internal systems respond to asynchronous events.

If your team is still deciding between a simple checkout and a more controlled payment stack, this guide on how to accept crypto payments for a website or app is a useful companion because it frames the integration choice around operational needs, not just developer preference.

The True Cost and Settlement Model

The surface-level attraction of coinbase commerce is straightforward. It uses onchain infrastructure to make payments feel faster and cheaper than traditional rails. For the buyer, that can produce a smoother experience. For the merchant, the primary question is what happens after the payment is initiated.

What the protocol does well

Finextra's technical review describes Coinbase Commerce's Commerce Payments Protocol on Base as capable of near-instant settlement, around 200ms in optimal conditions, with transaction fees around one penny, using an operator model that sponsors gas and creates a gasless checkout experience for the user (Finextra deep dive on the protocol).

That architecture is worth understanding because it solves a common checkout problem. End users don't want to think about gas, wallet routing complexity, or multi-step chain interactions. The operator model abstracts much of that friction away.

From a merchant-side perspective, the strong points are clear:

User friction is lower: Gas sponsorship makes checkout easier for buyers.

Settlement can be fast: The protocol is designed for rapid onchain movement.

Network costs are low: Very low transaction costs improve viability for smaller transactions.

Those are real advantages, especially for digital goods and global online services.

Where merchants need more clarity

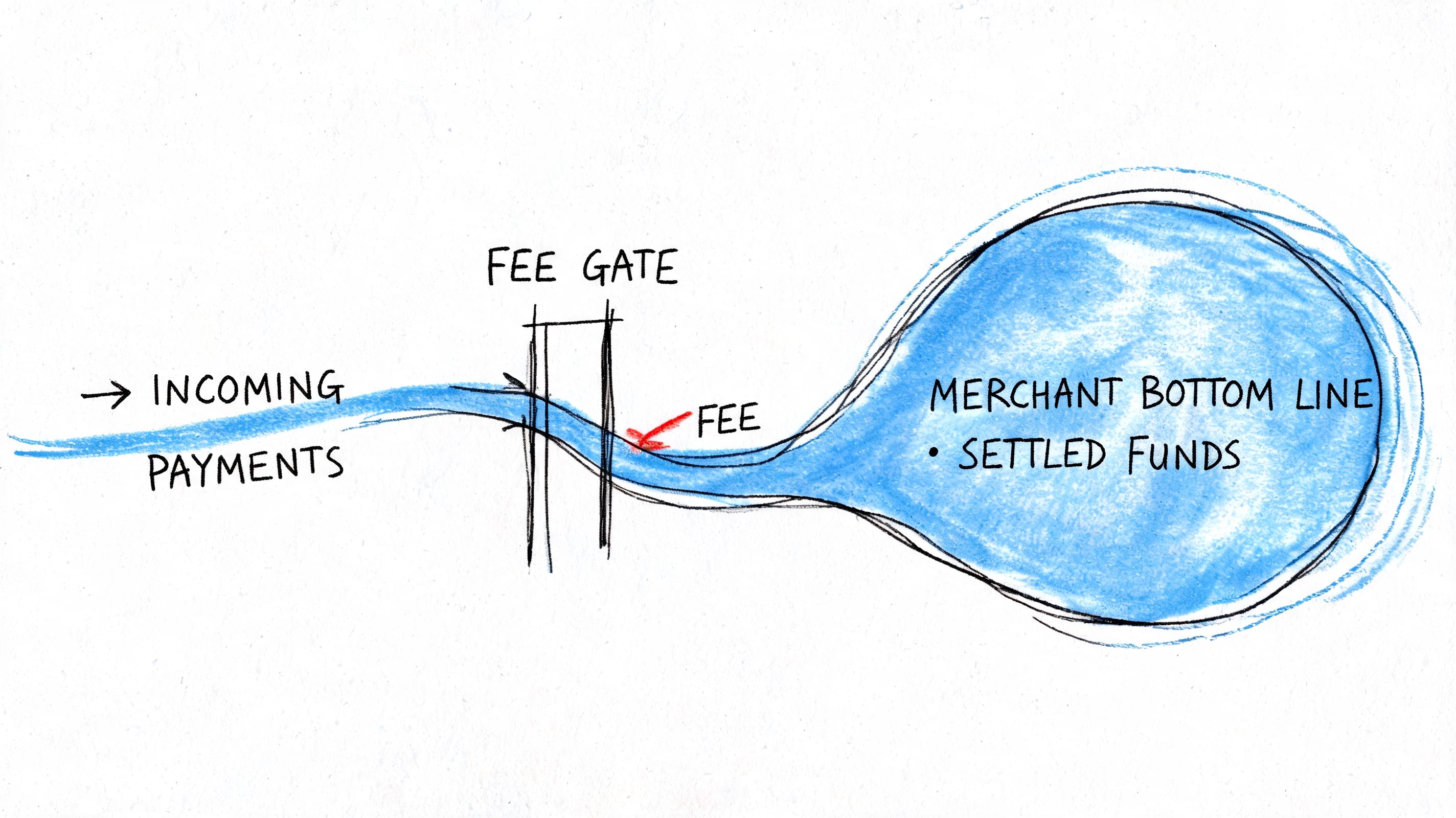

The gap is on the treasury side. Finextra also highlights that while the protocol can be efficient, the process and final asset for merchants can be complex, and public analysis often skips the total cost of ownership, including conversion costs or withdrawal friction.

That's the point many merchants miss when comparing processors.

A business doesn't book “checkout smoothness” as revenue. It books the asset that lands after all processing logic, conversion decisions, and withdrawal steps are accounted for. If the merchant's finance function wants stablecoin settlement in USDC, then the important questions become more operational:

What asset does the business ultimately receive?

Is conversion automatic or optional?

If conversion is involved, where does that happen in the flow?

How easy is it to move settled funds into treasury or operating wallets?

Merchant lens: Cheap acceptance isn't the same as predictable settlement.

For businesses that want stability, the best payment architecture often isn't the one with the broadest crypto support. It's the one where the customer can pay in a familiar way while the business receives USDC every time, without separate treasury work after each sale.

That's why many global merchants now evaluate processors less like crypto tools and more like settlement systems. The front-end payment method matters. The back-end settlement outcome matters more.

Key Limitations and Alternative Solutions

The main issue with coinbase commerce isn't that it fails at payment acceptance. It's that some businesses need a broader commerce tool than it provides.

Where coinbase commerce can fall short

One clear limitation is payment scope. Coinbase Commerce is built around crypto acceptance. If a merchant also needs to accept card payments, it doesn't solve that requirement on its own. For many internet businesses, that's a hard constraint because customers still expect card checkout as the default path.

Another limitation is compatibility friction. Blockchain Technology News reports that Coinbase Commerce now only accepts some cryptocurrency payments from users with Coinbase accounts, rejecting payments from self-custodial wallets in those cases, which creates a meaningful merchant-side problem when customers expect wallet flexibility (Blockchain Technology News coverage of the wallet restriction).

That matters in practice because merchants don't just need “supported assets.” They need checkout completion across the customer base they serve.

A simple decision lens helps:

If your buyers are already inside the Coinbase ecosystem, coinbase commerce may be workable.

If your customers expect broader payment flexibility, friction rises quickly.

If your business depends on card acceptance alongside crypto, you'll need another layer anyway.

When a different model fits better

For merchants focused on stable revenue, the better option is often a processor built around settlement outcomes rather than pure crypto acceptance. That's where alternatives become relevant.

One example is Suby, which provides a single API for accepting both card and crypto payments while settling merchant revenue in USDC. It also offers native integrations with Discord and Telegram for use cases like subscriptions, paid access, and online communities. The practical difference is simple: users can pay with cards or crypto, and the business receives USDC.

That model fits several merchant types more naturally than coinbase commerce:

Business type | What usually matters most | Better-fit payment model |

|---|---|---|

SaaS company | Recurring billing and stable settlement | Card plus crypto, merchant receives USDC |

Creator community | Paid access and automated member management | Integrated payments with community tooling |

Agency or freelancer | International collection with less payout friction | Familiar payer options, stablecoin payout |

If you're comparing tools directly, this review of a coinbase commerce alternative for merchants is useful because it frames the choice around settlement design and payment coverage, not just brand recognition.

Merchants rarely regret adding payment flexibility. They often regret adding payment complexity.

Making the Right Choice for Your Business

Coinbase commerce still has a valid place in the market. If your business wants crypto acceptance, your team is comfortable with crypto-native operations, and your customer base matches the platform's constraints, it can be a practical option.

But that isn't the same as saying it fits every online business. Many merchants don't want a crypto gateway first. They want a payment system that produces stable, predictable USDC revenue, works for global customers, and doesn't force finance or operations to clean up the back end after checkout.

That's the key test. Start with the settlement outcome you need, then work backward to the processor.

For teams doing a broader vendor review, it's worth also looking at independent roundups that compare top payment processors for 2026. A wider comparison helps clarify whether you need a crypto acceptance tool, a stablecoin settlement layer, or a hybrid model that supports both card and crypto at checkout.

If your buyers pay in different ways but your business wants to receive the same asset every time, your shortlist should favor processors designed around that reality.

Suby is a payment gateway and Merchant of Record. Your customers pay with card, bank transfer, Apple Pay, Google Pay, Klarna, and more, or stablecoins, and your business gets paid out to your bank account, or directly in stablecoins (USDC, EURC) to your wallet, anywhere in the world, no bank account required. With paylinks, embedded checkout, an API, subscriptions, and native Discord and Telegram flows for paid access, it closes the card gap and the treasury work that come with a crypto-only gateway like Coinbase Commerce, so the same asset settles every time no matter how the buyer paid.